Key highlights

Malaysia’s economic growth expanded by 3.30% in Q3 2023, with the Central Bank also maintaining a 3% interest rate due to moderating inflation.

The Central Bank also anticipates robust domestic demand to counterbalance export slowdowns. GDP has also surpassed pre-pandemic levels, and the country aims for a 4% growth in 2023, driven by domestic spending, improved labour conditions, and tourism.

- The top 9 banks in Malaysia recorded an average growth of 5.94% in their loan portfolio, from USD 50.18 billion in Q3 2022 to USD 53.16 billion in Q3 2023.

- The growth was mainly driven by mortgage and hire purchase financing.

On the other hand, deposits grew by 5.65% from USD 54.55 billion in Q3 2022 to USD 57.63 billion in Q3 2023.

Revenue

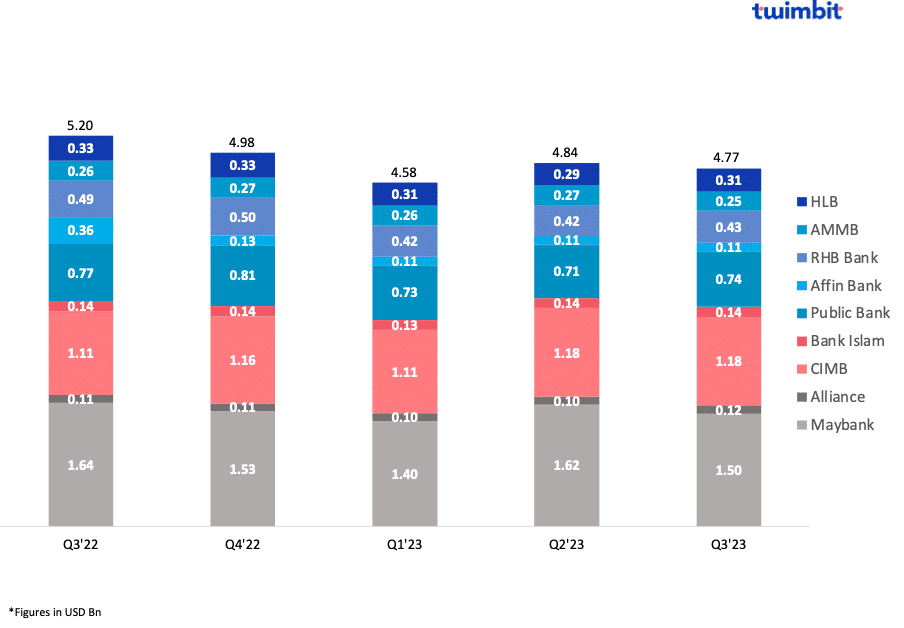

Net revenues for the top 9 banks in Malaysia declined by 8.37% YoY

The net revenues from the top 9 banks in Malaysia declined from USD 5.2 billion in Q3 2022 to USD 4.8 billion in Q3 2023 (Exhibit 1).

Exhibit 1: Net revenues of the top 9 Malaysian banks

- Alliance Bank, CIMB, and Bank Islam reported an increase of 9.88%, 6.22% and 1.36%, respectively

- Affin Bank, RHB, Maybank, HLB, AMMB, and Public Bank reported a decline of 69.12%, 10.69%, 8.95%, 7.07%, 5.15% and 4.15%, respectively

Alliance Bank

- Highest YoY growth at 9.88%

- Net revenues increased from USD 107 million in Q3 2022 to USD 117 million in Q3 2023

This growth was driven by 2 key factors – net interest income and non-interest income.

- 6% increase in the bank’s net interest income (excluding Islamic financing income) from USD 68.57 million in Q3 2022 to USD 72.72 million in Q3 2023

- 68.66% increase in the bank’s non-interest income (excluding Islamic non-interest income) from USD 11.89 million in Q3 2022 to USD 20.05 million in Q3 2023

The non-interest income was also driven by higher client-based income, which increased by USD 5.83 million and higher treasury and investment income, which increased by USD 3.35 million.

Affin Bank

- Highest YoY decline at 69.16%

- Net revenues decreased from USD 360 million in Q3 2022 to USD 111 million in Q3 2023.

This decline was primarily attributed to 2 key factors – net interest income and non-interest income.

- 36.79% decline in net interest income from USD 59.44 million in Q3 2022 to USD 37.57 million in Q3 2023

- 84% decline in non-interest income from USD 258.22 million in Q3 2022 to USD 41.27 million in Q3 2023

The decline in non-interest income was due to a 96% decline in other income for the bank, which declined from USD 237.41 million to USD 10.27 million. This decline was also due to the bank receiving more than the usual income as dividends from its subsidiaries in 2022 and then returning to normal in 2023.

Profitability

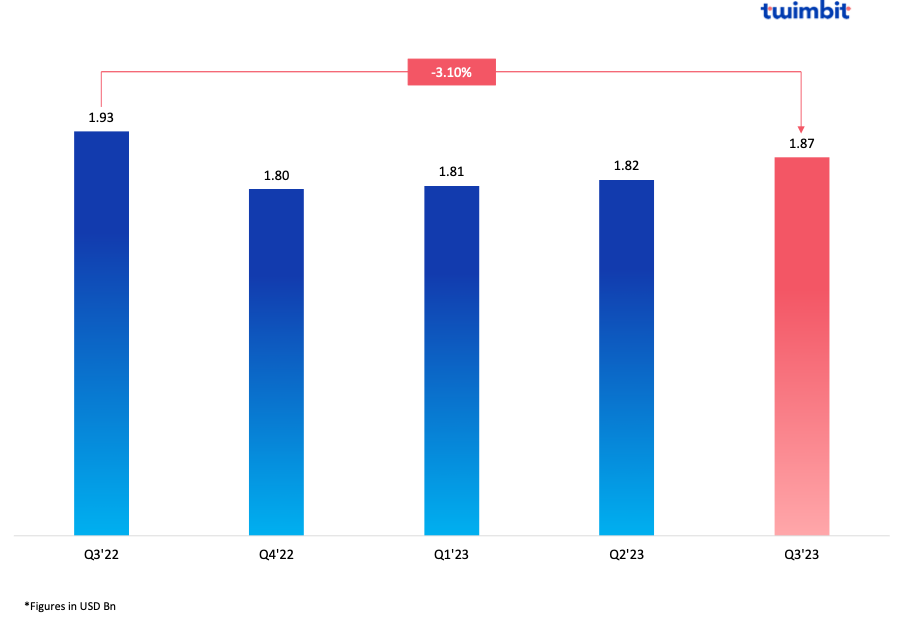

Net profits for the top 9 banks in Malaysia declined by 2.54% YoY

The top 9 banks in Malaysia aggregated their net profits from USD 1.93 billion in Q3 2022 to USD 1.88 billion in Q3 2023 (Exhibit 2).

On average, the top 3 Malaysian banks were AMMB, Alliance, and CIMB, which led the chart with an average net profit of USD 185 million in Q3 2023. AMMB, Alliance, and CIMB’s net profits grew by 30%, 17%, and 13%, respectively.

On the other hand, Affin Bank reported the highest decline in net profits at 88.54%, followed by RHB at 18.34%.

Exhibit 2: Consolidated net profits of the top 9 Malaysian banks

Fee-based income

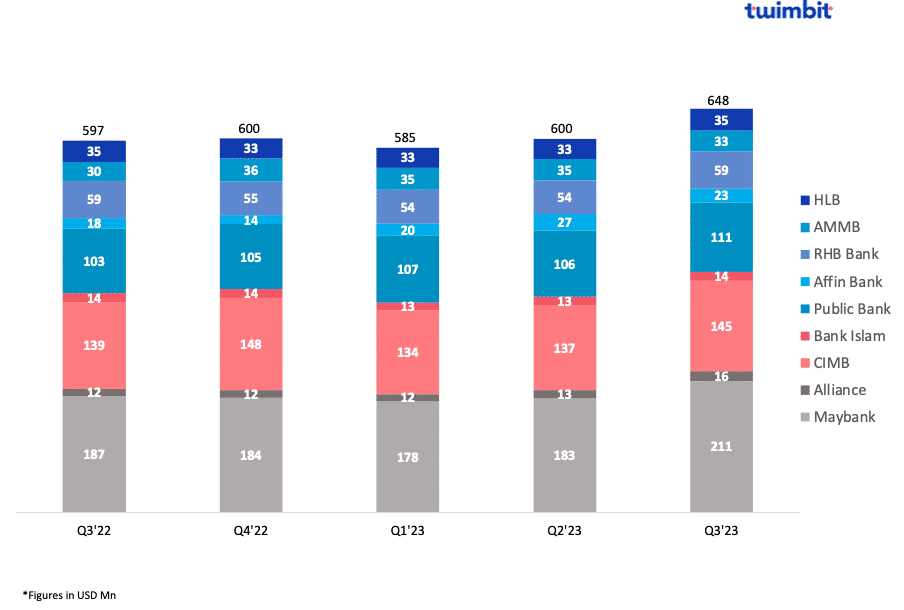

Fee income for the top 9 banks in Malaysia grew by 8.52% YoY

The top 9 banks in Malaysia witnessed a growth in fee income from USD 597 million in Q3 2022 to USD 648 million in Q3 2023 (Exhibit 3).

Alliance Bank reported the highest increase in fee income at 33.43% YoY, from USD 12 million in Q3 2022 to USD 16 million in Q3 2023. This growth was due to the following:

- An increase in the bank’s processing fees from USD 0.19 million in Q3 2022 to USD 0.83 million in Q3 2023.

- An increase in the bank’s other fee income from USD 0.33 million in Q3 2022 to USD 3.62 million in Q3 2023.

- Other fee income constitutes income from wealth management, bancassurance fees, FX sales and trade fees.

Bank Islam reported a marginal increase of 2.56% YoY in its fee income from USD 34.60 million to USD 35.48 million.

Exhibit 3: Fee income of the top 9 banks in Malaysia

Net interest margins (NIM)

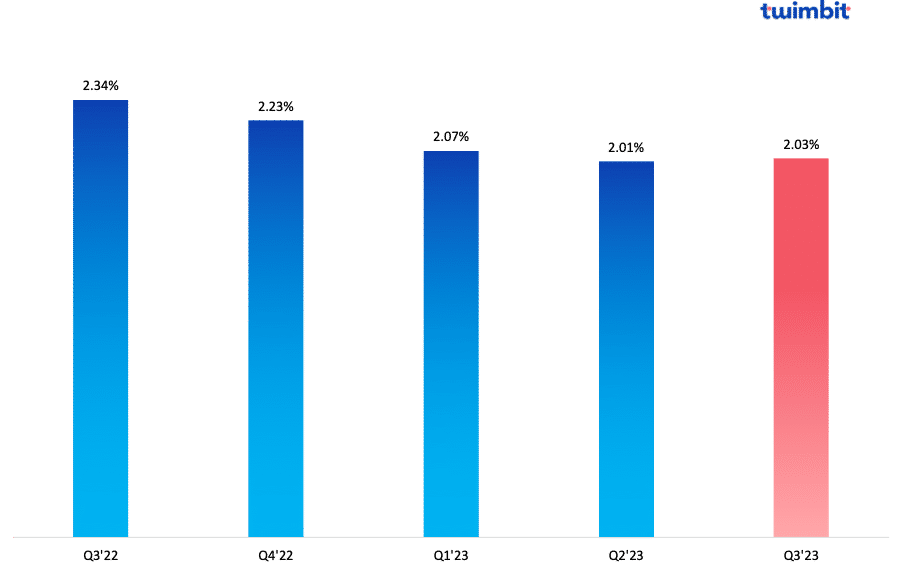

NIM declined by 31 basis points in Q3 2023

The average NIM dropped from 2.34% in Q3 2022 to 2.03% in Q3 2023 (Exhibit 4). Malaysian banks tend to have lower NIM compared to the APAC average of 3.16% in Q2 2023.

In Q3 2023, all the banks reported a decline in their NIMs, with Affin Bank reporting the highest decline from 2.01% to 1.46%.

Malaysia’s NIM is expected to bottom out by the end of 2023 and will likely remain flat in 2024 due to slower loan growth.

- Business loans grew only 2.1% in August compared to 2.3% in July.

- Household loans grew by 5.6% compared to 5.5% in July.

- Mortgage and auto loans grew by 7.1% and 9.1%, respectively.

Exhibit 4: Consolidated net interest margins of the top 9 banks in Malaysia

The declining NIMs in Malaysia are due to the following factors:

- Rising funding costs – 100 basis points have raised Malaysia’s overnight policy rate (OPR) from 2% to 3%. This has led to higher funding costs for banks, as they must pay more interest on deposits.

- Competition for deposits – Banks compete for deposits, especially in the current rising interest rate environment. This puts downward pressure on deposit rates, squeezing the banks’ margins.

- Slowing loan growth – Loan growth is expected to slow further in 2023 due to the rising interest rate environment. This will reduce the banks’ interest income and further decline their NIMs.

If left unchecked, these factors could pose a potential issue towards the profitability of Malaysian banks moving forward.

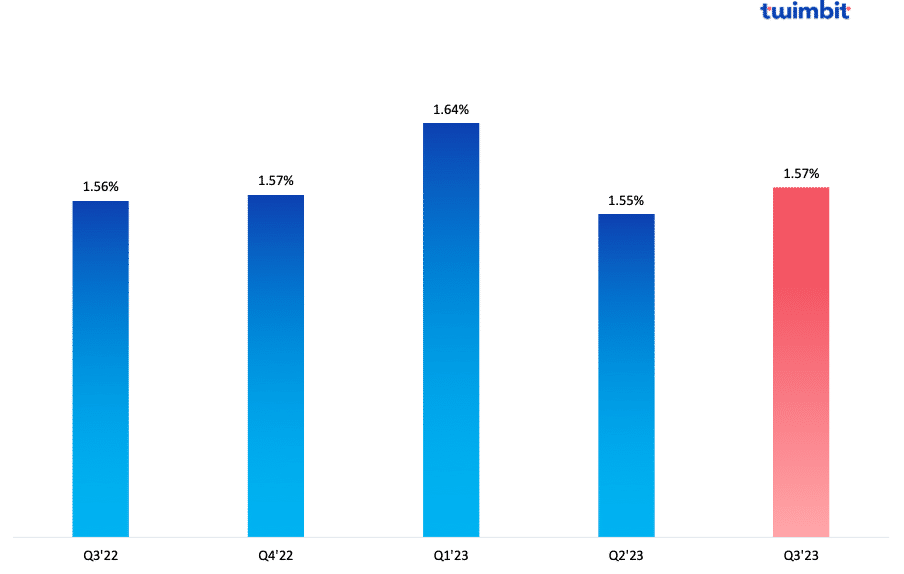

Non-performing loans (NPL)

NPLs for the top 9 banks in Malaysia increased by 1 basis point

The top 9 banks in Malaysia reported a minute increase in the average non-performing loans, from 1.56% in Q3 2022 to 1.57% in Q3 2023 (Exhibit 5).

Exhibit 5: Consolidated non-performing loans of the top 9 Malaysian banks

- 5 of the 9 banks analysed reported declining NPLs

- Bank Islam reported the highest NPL decline at 19%, from 1.20% in Q3 2022 to 0.97% in Q3 2023

- Alliance Bank reported the highest NPL growth at 32.11%, from 1.90% in Q3 2022 to 2.51% in Q3 2023

HLB and RHB reported an increase of 16.33% and 14% respectively. However, their current NPLs are low at 0.57% and 1.79%.

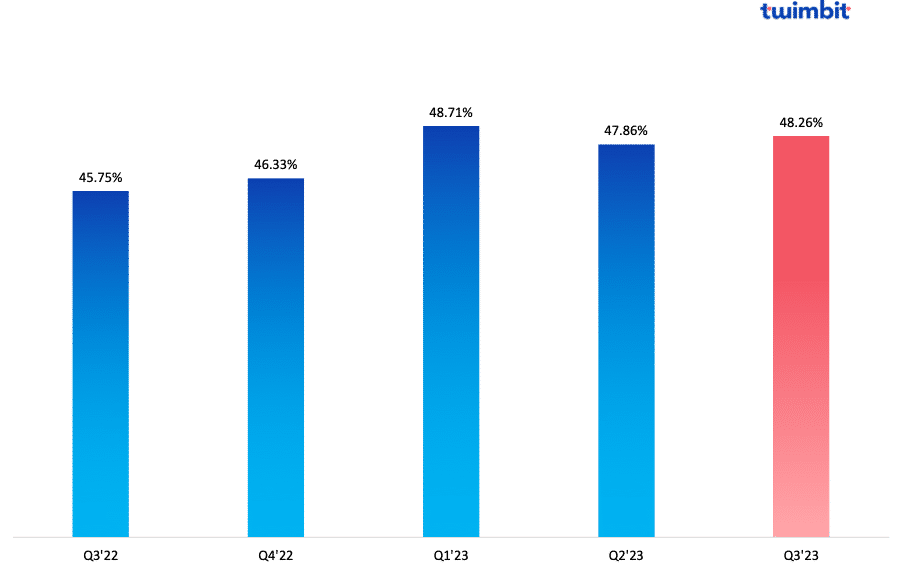

Cost efficiency (CE)

CE for the top 9 banks in Malaysia declined by 251 basis points between Q3 2022 and Q3 2023

The average cost efficiency for the top 9 banks in Malaysia stood at 48.26 % in Q3 2023, up from 45.75% in Q3 2022 (Exhibit 6). This indicates operational inefficiencies among these banks.

Exhibit 6: COnsolidated cost-efficiency ratio of the top 9 banks in Malaysia

All the banks analysed reported an increase in their cost efficiency. Alliance Banks and HLB reported the highest increase at 10.85% and 10.83%, respectively.

Bank Islam and Affin Bank reported a cost-efficiency ratio of 59.70% and 68.10%, respectively. All the other banks have their cost efficiency ratio below the threshold value, with Public Bank leading with an impressive ratio of 33.70%.

This lack of operational efficiency could stem from the compressions in net interest margins, resulting in elevated cost-efficiency ratios for these banks.

Initiatives by the top banks in Malaysia

- #1 Public Banks

Partnership with Pro-Net:

- Public Bank has partnered with Proton New Energy Technology to provide financial products and services for the latter’s customers.

- Pro-Net is Malaysia and Thailand’s exclusive importer and distributor of smart vehicles.

- Both parties will also embark on digitalisation via systems integration with smart Malaysia.

- #2 Maybank

Cross-border QR Pay Service to China:

- The bank expanded its cross-border QR Pay service to China, making it the first initiative of its kind for a Malaysian bank.

- The expansion aims to benefit over eight million Maybank MAE app users visiting China and more than 700,000 Maybank QRPay merchants in Malaysia, facilitating transactions made by visitors from China.

- Malaysian MAE app users can make cashless payments with Alipay merchants in China. Users scan the QR code, enter the payment amount, and receive instant payment confirmation with details in CNY and RM.

- The strategic initiative results from Maybank’s collaboration with Payments Network Malaysia (PayNet) to assist Malaysians travelling to China and inbound Chinese tourists visiting Malaysia.

- #3 CIMB

Branch with Green features:

- The bank unveiled its first branch with integrated sustainable features at IOI City Towers, Putrajaya.

- The branch comes equipped with tailored facilities and services, including a priority ATM lane with improved accessibility for customers with special needs, as well as wheelchair services and designated low counters for over-the-counter transactions.

- The branch also includes features that will reduce energy consumption and emissions, including energy-efficient cooling and lighting systems, sustainable materials and recycled content and reused office furniture.

- #4 AMMB

Amplifying MSMEs program:

- The bank has collaborated with Bank Simpanan Nasional (BSN) to focus on nurturing and uplifting micro, small and medium enterprises.

- The partnership aims to provide participants with essential financial and business knowledge through workshop programs covering financial literacy, financial management, business management, operations management, and digital transformation.

- The initiative targets the expansion of 200 selected MSMEs that have previously benefited from the BSN microfinancing scheme, aiming to elevate them to a higher level of business growth.

- The goal is to facilitate access to essential financial services, meeting the evolving business requirements of the MSMEs.

- #5 Bank Islam

Be U:

- The bank introduced “Be U,” a fully cloud-native digital banking platform that is expected to set the standard for future digital banks in Malaysia.

- Be U aims to provide a seamless and branch-free banking experience that targets the younger, digital-native generation. Its user-friendly interface empowers users to manage finances effortlessly.

- Be U caters to the younger demographic, offering features like a zero-balance savings account, fund transfers, and a Nest feature for goal-oriented savings.

- Be U focuses on early-stage working professionals, providing essential financial services. As users’ financial stability grows, Be U plans to offer a broader range of Bank Islam’s products and services.

- Over the next 12 months, Be U introduce new functionalities, including term deposits, a gig marketplace, debit cards, personal financial management, micro-financing, and micro-takaful.

Malaysian banking industry outlook for Q4 2023

While the Malaysian banking sector maintains strong asset quality, there is predicted to be an impending rise in loan delinquencies. The surge is attributed to increased loan instalments and heightened cost pressures, particularly affecting highly leveraged borrowers and small to medium-sized enterprises in vulnerable sectors. Despite this, the deterioration will be manageable, projecting an industry NPL ratio below 2% in 2023.

In Q3 2023, after three consecutive quarters of contraction, there was relief as the average NIM of the top nine banks remained stable at 2.03%. This is attributed to easing competition for deposits and a 25 basis points overnight policy rate (OPR) hike in May, alleviating pressure on NIMs. However, the respite may be short-lived, as deposit competition is expected to intensify in the fourth quarter.

To learn about how the leading Indian banks performed in Q3 2023, click here.

To learn about how the top 3 Singapore banks performed in Q3 2023, click here.

To learn about how the top 5 Indonesian banks performed in Q3 2023, click here.

To learn about how the leading banks in the Philippines performed in Q3 2023, click here.

To learn about how the leading banks in South Korea performed in Q3 2023, click here.