Executive summary

The Middle East telecom sector exited Q2 2025 with steady yet uneven momentum. Industry revenues rose by an average of 6.4% YoY, with more than four-fifths of operators expanding and nearly a third delivering double-digit growth. Core connectivity remains the sector’s anchor, as mobile, broadband, and ICT adoption continue to fuel topline expansion, even in mature markets. Operators such as Mobily, Orange MEA, and Turk Telekom highlight how diversified portfolios across retail, fixed, and enterprise services create resilience against persistent macroeconomic headwinds.

Beneath these stable figures, however, a structural transformation is underway. Connectivity is increasingly commoditized, and growth is being redefined through digital platforms. STC, Zain Kuwait, and Ooredoo Qatar illustrate this pivot as fintech, cloud, and hyperscale partnerships are now driving higher-value revenues, positioning telcos less as pipe providers and more as ecosystem architects.

Enterprise services are emerging as the structural engine of this reinvention. Etisalat UAE’s private 5G initiatives, Du’s wholesale and ICT expansion, and STC Bahrain’s enterprise partnerships demonstrate how deep integration into corporate, and government digital agendas is unlocking durable revenue pools. In a market where consumer momentum is slowing, B2B is becoming the most reliable frontier.

Profitability reinforces this narrative. Industry-wide EBITDA rose 8.4% YoY, with margins climbing to 41.6%. Crucially, profitability is decoupling from topline growth. Du, Telecom Egypt, and Mobily expanded margins through disciplined efficiency programs, optimized product mixes, and adjacency in digital services. By contrast, Ooredoo Iraq and Zain KSA faced pressure as competitive volatility and political conditions constrained performance.

Capital expenditure is the clearest signal of strategic intent. Average capex intensity rose to 17.3%, with nearly two-thirds of operators lifting investment. Funds are being redirected from coverage expansion toward AI, cloud, and advanced 5G capabilities. Etisalat UAE, Turkcell, and Zain Kuwait are making bold, future-ready bets, while operators in saturated markets such as Cellcom, Bezeq, and Partner are exercising restraint, focusing on network optimization.

ARPU dynamics underscore this divergence. Markets such as Telecom Egypt, Turkcell, and Bezeq, where users were successfully migrated to postpaid and premium tiers saw tangible gains. In contrast, Cellcom, Partner, and Du, operating in intensely competitive or politically constrained environments, experienced ARPU declines, with growth more volume-driven than value-led.

At the frontier, the industry is widening its ambition. Etisalat UAE launched a next-generation platform fusing cloud and AI, STC announced a 6G research collaboration with Nokia, and Orange Jordan opened a 5G innovation lab and agriculture boot camp. These initiatives reflect a sector intent on shaping ecosystems and future standards, not merely carrying traffic.

In sum, the region’s telcos remain anchored by resilient connectivity but are increasingly defined by three forces: the pivot from pipes to platforms, the rise of enterprise as the growth engine, and capex as a value unlock. Profitability is being reshaped by efficiency and adjacencies, and the winners will be those capable of delivering today while building the digital platforms of tomorrow.

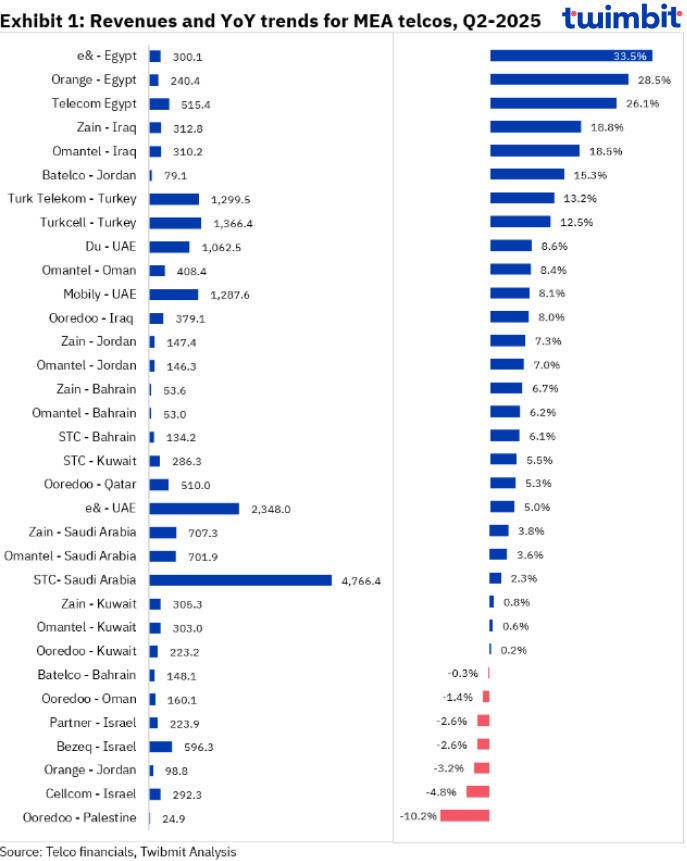

Revenue analysis of MEA telcos: Q2-2025

Average revenue growth for MEA telcos in Q2-2025 is 6.4% on a YoY basis.

The 33 telcos achieved a combined revenue of USD 19.7 bn in Q2-2025, with net additions of USD 1.1 bn.

About 79.0% of the telcos reported positive revenue growth, with ~24% achieving double-digit growth.

- From pipes to platforms: Telcos as digital ecosystem architects: As connectivity commoditizes, MEA operators are redefining their growth DNA through fintech, cloud, and platform services. The emerging winners are those able to orchestrate ecosystems rather than simply provide networks.

STC Saudi Arabia: While overall revenue grew modestly at 2.3% YoY, STC’s platform shift is reshaping its business model. Fintech revenues surged 24.1%, cybersecurity expanded 36.8%, IoT rose 55.2%, and cloud advanced 32.1%, collectively reinforcing its transition from a traditional telco into a full-spectrum digital platform architect.

Zain Kuwait: Revenue rose just 0.8% YoY, but stronger B2B adoption and early monetization of 5G-Advanced illustrate how platform-driven models can scale quickly, unlocking diversification beyond retail consumer services.

Ooredoo Qatar: A 5.3% YoY revenue uplift was propelled by hyperscale partnerships, underscoring how telcos can evolve from connectivity providers to orchestrators of cloud ecosystems with higher-value roles in the digital economy.

- Sustained growth in core connectivity: Core connectivity remains a key driver of expansion across the MEA region, with mobile, broadband, and ICT adoption delivering steady topline momentum despite saturation in more mature markets.

Mobily UAE: Revenue grew 8.1% YoY, underpinned by balanced performance across segments, highlighting how diversified legacy streams continue to buffer against macroeconomic pressures.

Turk Telekom Turkey: Achieved 13.2% YoY growth, led by strong gains in broadband, corporate data, and mobile, with fixed broadband reinforcing its role as a dependable source of recurring revenue.

e& Egypt: Recorded exceptional 33.5% YoY revenue growth, enabled by accelerated 5G rollout, strategic partnerships, and aggressive customer acquisition initiatives.

- B2B as the structural growth driver: The growth trajectory is increasingly enterprise-led, with private 5G, ICT, and cloud redefining telco value creation. Operators embedding into corporate and government digitalization agendas are accessing more resilient and scalable revenue streams.

e& UAE: Posted 5.0% YoY growth as cybersecurity, cloud, and IoT expansion across domestic and international operations underscored how even mature markets can unlock incremental value through B2B.

Zain Kuwait: Delivered modest 0.8% YoY revenue growth, underpinned by large-scale enterprise contracts, validating B2B’s ability to drive scale in mature markets.

Du UAE: Achieved 8.6% revenue growth, with ICT and wholesale services fuelling demand as enterprises and government accelerate digital transformation.

STC Bahrain: Grew revenues 6.1% YoY through ecosystem partnerships modernizing enterprise connectivity, reducing reliance on legacy streams, and diversifying its revenue base.

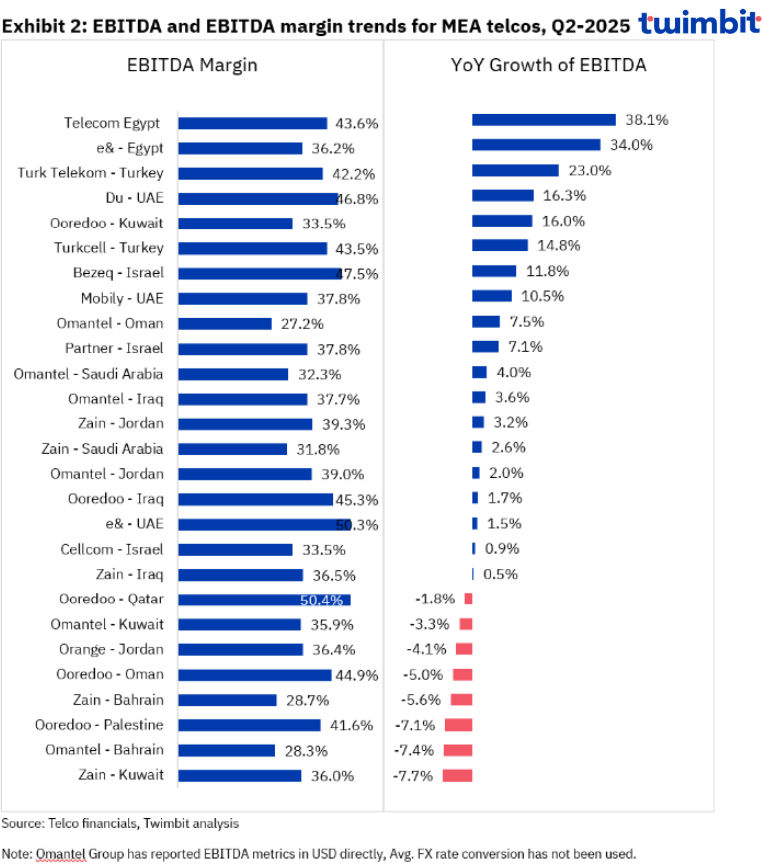

EBITDA analysis of MEA telcos: Q2-2025

The average EBITDA margin reported at to 41.6% in Q2-2025. Cumulative EBITDA grew by 8.4% YoY in the same period.

MEA telcos showed that profitability is increasingly decoupled from topline growth. Efficiency gains, digital adjacencies, and disciplined product mix shifts allowed several operators to expand or defend margins, even in mature or highly competitive markets.

- Efficiency anchored in scale, mix, and expansion: Operators combining disciplined cost management with subscriber scale and high-margin service expansion delivered EBITDA growth significantly ahead of topline performance.

Du UAE: EBITDA increased 16.3% YoY with margins rising to 46.8%, reflecting disciplined cost control, a favorable product mix of value and unlimited data plans, and 10.8% mobile subscriber growth driving profitability beyond revenue gains.

Mobily UAE: EBITDA rose 10.5% YoY with modest margin expansion, supported by revenue growth, stronger operating profits, lower expenses, and joint venture gains, offsetting ongoing competitive and operational pressures.

Telecom Egypt: Delivered a 38.1% EBITDA increase, outpacing revenue growth, fueled by 5G service launches and expansion in enterprise and data segments that reinforced margin improvement.

- Margins under pressure despite modest EBITDA growth: In several markets, operators delivered only incremental EBITDA gains, with margin expansion constrained. While customer growth and disciplined execution supported performance, rising costs and structural headwinds limited efficiency improvements.

Ooredoo Iraq: EBITDA rose 1.7% YoY, but margins declined 300 bps to 45.3%, as intensifying competition offset the benefits of a growing customer base.

Zain KSA: EBITDA increased 2.6% YoY, with margins stable at 31.8%, underscoring the limited ability to convert topline momentum into stronger efficiencies.

Zain Iraq: EBITDA grew 0.5% YoY, as cost optimization measures were offset by higher operating expenses in a volatile and challenging market environment.

- Digital adjacencies as margin multipliers: Investments in fintech, cloud, and digital services are reshaping operator margin profiles. Unlike hardware or prepaid-led revenues, these adjacencies generate structurally higher EBITDA contributions and support long-term profitability.

Turkcell Turkey: EBITDA rose 14.8% YoY, driven by topline growth, cost efficiencies, and high-margin services, with fiber expansion and robust data center and cloud revenues strengthening profitability.

Ooredoo Kuwait: EBITDA increased 16.0% YoY with margins up 400 bps to 33.5%, reflecting service revenue growth combined with disciplined cost optimization.

Zain KSA: EBITDA grew 2.6% YoY with stable margins, supported by an improved product mix, while diversification into MVNO and fintech through subsidiaries such as Tanam expanded profitability levers.

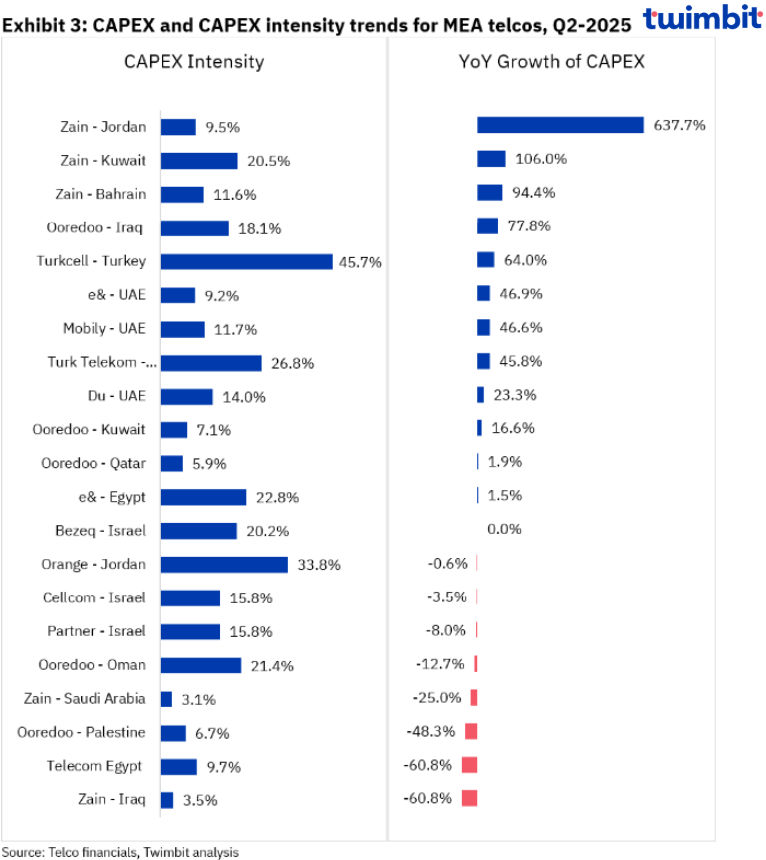

CAPEX analysis of MEA telcos: Q2-2025

Average CAPEX intensity stood at 17.3% in Q2-2025.

Nearly ~62.0% of the 21 telcos analysed reported YoY CAPEX growth in Q2-2025, owing to modernisation of network and investment in new innovations.

Expansion of networks and building new-age digital network to unlock more potential value remained the Capex focus for the quarter.

- Capex as a signal of strategic intent: Investment priorities are increasingly shaping competitive trajectories. Beyond coverage, capex now reflects targeted bets on data centers, AI, and 5G ecosystems that will define operator positioning for the decade ahead.

e& UAE: Capex rose 46.9% YoY, driven by network upgrades, private networks, and phasing decisions, underscoring its focus on building a premium, future-ready infrastructure base.

Ooredoo Qatar: Capex remained stable, but allocations prioritized AI cloud data centers and enterprise 5G integration, signaling a strategic pivot toward digital infrastructure over legacy network expansion.

Turkcell Turkey: Capex surged 64.0%, largely non-operational, reflecting investments in 5G and service modernization to reinforce its positioning as a future-ready operator.

- AI and next-gen networks as differentiators: Capex intensity is highest in markets prioritizing AI-driven networks, hyperscale cloud, and digital modernization. While capital-heavy, these investments position operators to differentiate in an otherwise commoditized sector.

Zain Bahrain: Capex surged 94.4%, directed toward AI initiatives and ecosystem modernization to strengthen long-term competitiveness.

Du UAE: Capex rose 23.3% YoY, with investments focused on hyperscale data centers and the National Hyper Cloud in partnership with Microsoft.

Zain Kuwait: Capex increased 106.0% YoY, allocated to Open AI-RAN, advanced 5G deployments, indoor coverage enhancements, and digital system upgrades, reinforcing commitment to next-generation infrastructure.

- Capital discipline in saturated markets: In markets where large-scale rollouts are complete, operators are exercising restraint. Investment strategies are shifting from aggressive expansion toward optimizing existing infrastructure and deploying capital more selectively.

Cellcom Israel: Reduced Capex 3.5% YoY as 5G deployment reached maturity in major cities, signalling a pivot from network expansion to efficiency-driven optimization.

Bezeq Israel: Maintained flat Capex at 20.2% intensity, reflecting capital discipline while sustaining competitiveness amid the near completion of nationwide 5G and fibre rollout.

Partner Israel: Cut Capex 8.0% YoY, balancing financial prudence with targeted upgrades in a politically and economically sensitive market environment.

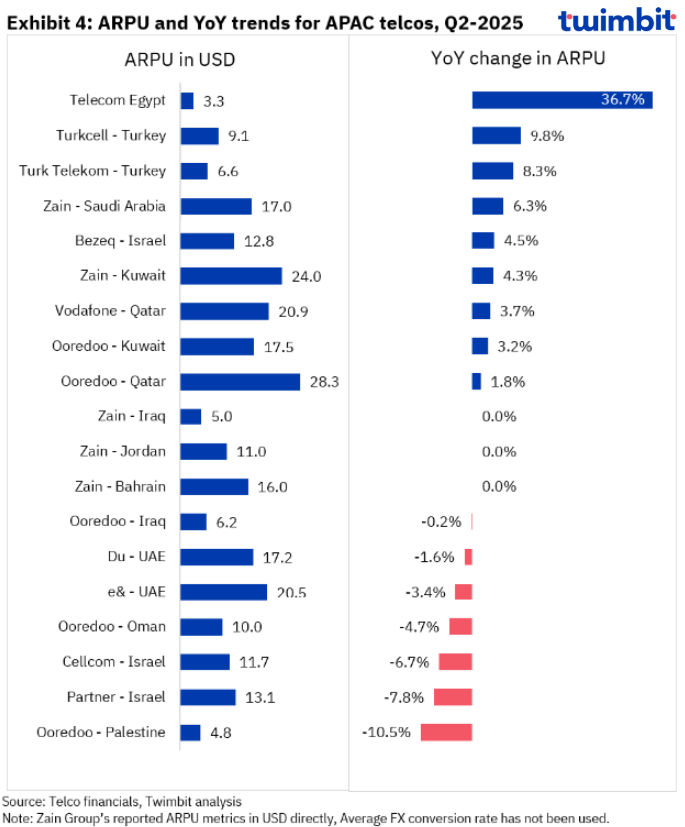

ARPU analysis of MEA telcos: Q2-2025

Varied changes to YoY ARPU growth with 9 telcos out of 19 reporting growth in ARPU.

The ARPU analysis for the 19 telcos analysed is as follows:

12 out of 19 telcos had stable ARPUs with YoY change ranging from +/- 5%.

Average ARPU reported at ~USD 13.4 for Q2-2025.

- The rise of postpaid as the ARPU engine: The structural shift from prepaid to postpaid is redefining revenue quality. Postpaid subscribers deliver higher spending power, lower churn, and greater stability, making this migration central to sustaining ARPU growth.

Vodafone Qatar: ARPU rose 3.7% YoY, supported by stronger postpaid additions relative to prepaid.

Bezeq Israel: ARPU increased 4.5% YoY to USD 12.8, driven by growth in postpaid and 5G adoption.

Turk Telekom: ARPU grew 8.3% YoY, with a 10.7% postpaid ARPU uplift offsetting prepaid declines.

Turkcell: ARPU expanded 9.8% YoY as customers continued migrating from prepaid to higher-value postpaid plans.

- Consumer upgrading as a profit lever: Where operators can push customers into higher-value plans, through data-heavy bundles, 5G, or enterprise-lite offerings. ARPU accelerates well beyond subscriber growth.

Telecom Egypt: A standout 36.7% ARPU growth YoY, fueled by an expanding base of higher-value postpaid consumers and higher ARPU in both retail and enterprise solution segments.

Turkcell: ARPU uplift tied to richer service bundles, combining connectivity with TechFin and content services.

Bezeq Israel: Gains from premium 5G adoption underline how technology upgrades directly translate into higher spending per user.

- ARPU pressure in saturated markets: In markets where growth depends on aggressive promotions, intense competition, or macro instability, ARPU is declining, even as customer numbers grow. This points to structural fragility.

Cellcom Israel: ARPU fell 6.7% YoY to USD 11.7, as cellular subscriber base decline combined with macroeconomic headwinds pushed ARPU down.

Partner Israel: ARPU declined 7.8% YoY, from USD 14.2 to USD 13.1, highlighting vulnerability to political and economic uncertainty.

Du UAE: A marginal 1.6% YoY ARPU decline to USD 17.2, despite revenue growth, signals that topline expansion is coming more from volume than from value per user.

Frontier Innovations shaping the industry

Next-generation connectivity platform (TrustNet+5G+AI Net)

e& UAE has launched the Next-Generation Connectivity Platform, integrating TrustNet, 5G, and AI Net into a single managed solution. The platform enables enterprises to access seamless and secure connectivity across private and hybrid networks while linking directly to hyperscalers such as AWS, Microsoft Azure, and Oracle Cloud. This positions e& UAE as a front-runner in converged cloud-networking services, tailored to accelerate digital economy adoption.

6G research collaboration

At the 2025 LEAP tech event, STC Group and Nokia entered a strategic partnership to advance 6G research and innovation in the Middle East. The collaboration focuses on building testbeds and proof-of-concept projects leveraging Software-Defined Access Networks (SDAN) on fibre-to-the-home infrastructure. Anchored in Saudi Arabia’s Vision 2030 agenda, the initiative underscores STC’s ambition to shape next-generation telecom standards and transition from a national operator to a global digital leader.

5G lab & agriculture boot camp

Orange Jordan has rolled out two flagship innovation programs to accelerate 5G adoption. The Orange 5G Lab, located in Amman’s Digital Village, provides startups, enterprises, and students with a dedicated environment to develop 5G-enabled applications in VR/AR, IoT, and enterprise connectivity. Complementing this, the 5G Agriculture Boot Camp ran as a two-month program applying 5G, IoT, and AI to real-world agricultural use cases, including pest management and precision farming, demonstrating how sector-specific innovation can drive broader ecosystem impact.

Research Methodology and Assumptions

- The “Middle East Telcos Performance Benchmarks – Summer 2025” report offers crucial insights into the performance of telecom companies. It analyses key financial indicators such as Revenues, EBITDA, CAPEX and ARPU for Q2-2025 (April – June 2025).

- This report utilises data collected from telecom firms and extensive secondary research. Twimbit follows a calendar year for its data analysis, with FY representing January to December.

- To maintain consistency and enable accurate comparisons, the report applies a constant currency conversion rate, reflecting the average USD exchange rate for April – June 2025. (Note: Except EBITDA metrics for Omantel group & ARPU metrics for Zain group)

- The report evaluates Revenue and EBITDA for 33 and 27 telecom companies, respectively. CAPEX and ARPU analyses cover data from 21 and 19 companies, respectively.

- Blended mobile ARPU has been incorporated wherever relevant for a more holistic view.