Key takeaways

- Revenue growth for telecom operators in the Middle East has been driven by increased data usage facilitated by 4G/5G network expansion, price improvements, subscriber growth in the fixed broadband segment, and rising contributions from the enterprise (B2B) segment.

- The average Year-over-Year (YoY) revenue growth for Middle East telcos improved from 3.9% in Q3-2023 to 5.2% in Q3-2024.

- In Q3-2024, the 35 telecom operators analysed generated a combined revenue of ~USD 18.5 billion. Nearly 71% of these operators experienced positive revenue growth, with seven reporting double-digit YoY gains.

- Telecom operators focused on enhancing operational efficiency and implementing effective cost control measures to improve profitability.

- Nearly 79% of telcos demonstrated positive EBITDA growth in Q3-2024, with 12 operators, or about 41% of the total, achieving double-digit growth.

- The average EBITDA margin remained stable at approximately 39% for the 29 telecom operators analysed in Q3- 2024.

- Capital expenditure (CAPEX) is expected to stabilize as telecom operators in key markets complete network deployments. As telcos transition from traditional connectivity providers to technology and solution-driven entities, investment in digital infrastructure and offerings is likely to increase, alongside ongoing spending for fibre deployment and new 4G/5G network rollouts.

- Nearly 54% of the 28 telecom operators in the Middle East increased their YoY CAPEX spending in Q3-2024. The average capital expenditure (CAPEX) intensity remained stable at around 14%, as network deployments and expansions reached completion.

- Despite adverse macroeconomic conditions in select geographies, the average ARPU remained steady at USD 12.6 in Q3-2024, supported by increased adoption of 4G/5G technologies and strategic price hikes in countries like Turkey, Egypt, and Qatar.

- Among the 15 telcos analysed, nearly 67% reported net profit growth in Q3-2024, compared to approximately 80% in Q3-2023. Macroeconomic challenges coupled with increase in expenses impacted the net profit margins.

- Telcos in Middle East continue to adopt advanced technologies and form strategic partnerships to enhance network capabilities, improve customer experiences, and drive digital transformation.

Revenue analysis of Middle East telcos: Q3-2024

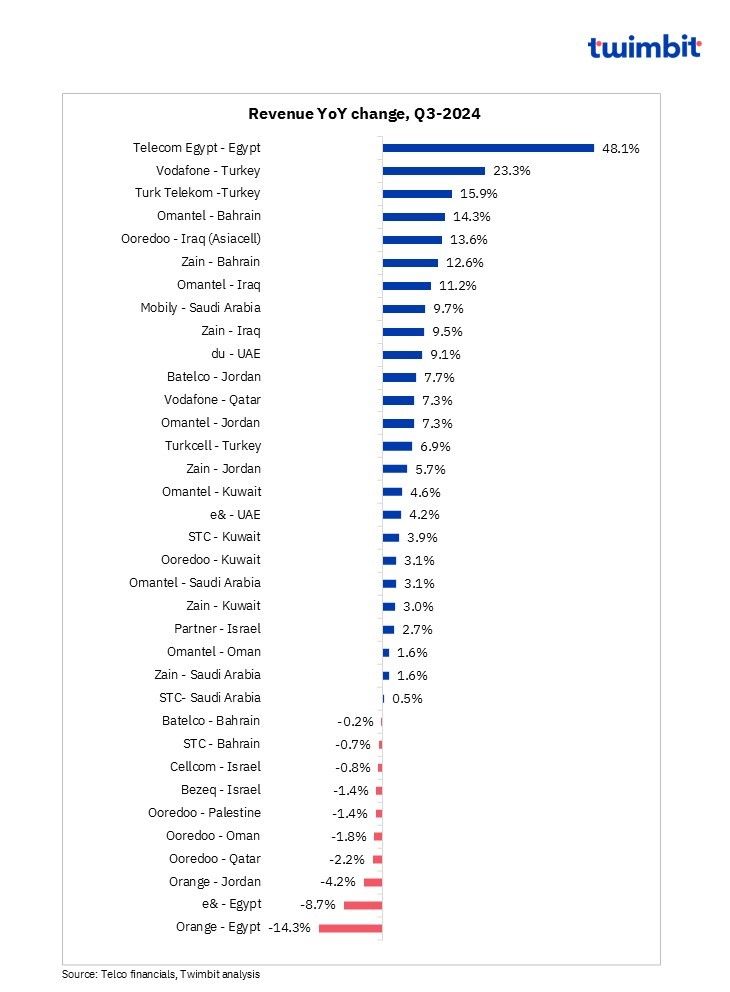

Average revenue growth for Middle East telcos increased from 3.9% in Q3-2023 to 5.2% in Q3-2024

In the third quarter of 2024, telcos in the Middle East region reported a total revenue of ~USD 18.5 billion, marking net revenue addition of approximately USD 970 million on YoY basis.

Approximately 71% of telcos in Q3-2024 reported positive revenue growth, with 7 telcos achieving double-digit growth, led by Telecom Egypt and Vodafone – Egypt.

Exhibit 1: Revenue trend of telcos in the Middle East, Q3-2024

Key highlights

- Price improvements and an expanding subscriber base facilitated revenue growth for telcos like Telecom Egypt, Turk Telecom, Turkcell and Mobily – Saudi Arabia, Vodafone – Qatar.

- 4G/5G network expansions by operators like Ooredoo in Iraq and Kuwait, du in the UAE, and Zain in Bahrain and Saudi Arabia have led to increased data usage, thereby boosting their revenues.

- Ooredoo Iraq’s revenue growth can be attributed to favourable market dynamics, an increase in customer numbers, and higher adoption of data services.

- Growth in fixed-line, primarily fibre broadband subscribers, has contributed to revenue increases for telecom companies such as Bezeq in Israel, du, Telekom Egypt, Turk Telecom, Turkcell, and Zain in Jordan and Bahrain during Q3-2024.

- Price increases across all retail segments, coupled with a 7.9% YoY growth in fixed broadband subscribers and a 38% YoY growth in fixed data ARPU, propelled a 48.1% revenue growth for Telecom Egypt.

- Strong YoY fibre uptake (50% growth in Q3-2024), including a 100-basis point increase in customers of Unified Broadband Service to 81%, facilitated overall revenue growth for Bezeq in Israel.

- The enterprise (B2B) segment is emerging as a significant growth opportunity, prompting telcos to invest in digital infrastructure capabilities and monetise enterprise offerings. Companies such as Etisalat, Ooredoo, du, Vodafone Qatar, Telekom Egypt, Vodafone Turkey, and Zain Group have reported positive revenue contributions from enterprises through their Cloud, ICT offerings, and managed services.

- Telecom Egypt’s enterprise revenue increased by 51.1% YoY in Q3-2024, reaching USD 46.4 million (EGP 2.3 billion), supported by managed data and access services.

- Focused strategy execution in ICT/Managed services and FinTech, yielded positive results for Vodafone Qatar in the enterprise segment.

- e& Enterprise revenue reached USD 185.2 million (AED 680 million) in Q3-2024, driven by sustained revenue growth in cybersecurity and cloud services, alongside strong performance in Saudi Arabia. Strategic acquisition of Glasshouse and a six-year partnership agreement with AWS is expected to further propel revenue growth.

- In addition to these, digital offerings such as e& Life have facilitated growth for e& Group, while the expansion of Fintech segments like Tamam and Bede has contributed to revenue growth for Zain in Saudi Arabia and Bahrain.

- Zain Group reported its highest quarterly revenue since FY-2021, attributed to strong operational performance in its main markets of Kuwait, Iraq, and Saudi Arabia, operational efficiency of its networks and FTTH services, and gains from new growth avenues in the Gulf and Middle East markets.

- In Q3-2024, Zain Group’s data revenue grew significantly, accounting for a substantial portion of its overall revenue in key operating geographies such as Kuwait (35%), Saudi Arabia (40%), Jordan (51%), and Bahrain (46%).

- Omantel Group witnessed revenue growth across most Middle Eastern countries, primarily driven by increased data revenue.

- STC continues to invest in digital infrastructure, including 5G, fibre optics, and data centres, as well as advanced technologies like cloud computing, IoT, and fintech, while enhancing its cybersecurity capabilities.

- STC Kuwait’s revenue grew 3.9% YoY in Q3-2024, driven by an increase in mobile and fixed subscribers, which offset stagnant revenue in Saudi Arabia and a decline in Bahrain, both of which experienced a decrease in mobile subscriptions.

- However, the telecom landscape in the Middle East region was marked by mixed fortunes, as revenue declined for few telcos during the period.

- While Egyptian operators (e& – Egypt and Orange – Egypt) struggled with economic pressures such as currency devaluation and inflation, Telecom Egypt emerged as a beacon of resilience facilitated by strong market position and diversified service portfolio to achieve revenue growth.

- Conversely, telcos in Israel (Partner and Bezeq) and Palestine (Ooredoo) encountered revenue declines due to weakening cellular performance and a challenging operating environment.

- Favourable regulatory developments are expected to enhance the competitive landscape in the region, as telecom companies strive to increase the adoption of their 5G services.

- By awarding 5G licenses to Orange Egypt, Vodafone Egypt, e& Egypt, and Telecom Egypt, Egypt’s National Telecom Regulatory Authority (NTRA) is likely to intensify competition among providers and pave the way for digital advancement.

- Additionally, Zain’s acquisition of new frequencies in the 600 MHz band in Saudi Arabia for 5G services and Zain Iraq’s (Asiacell) collaboration with Vodafone for the launch of 5G services are expected to elevate the region’s 5G positioning on the global landscape.

EBITDA analysis of Middle East telcos: Q3-2024

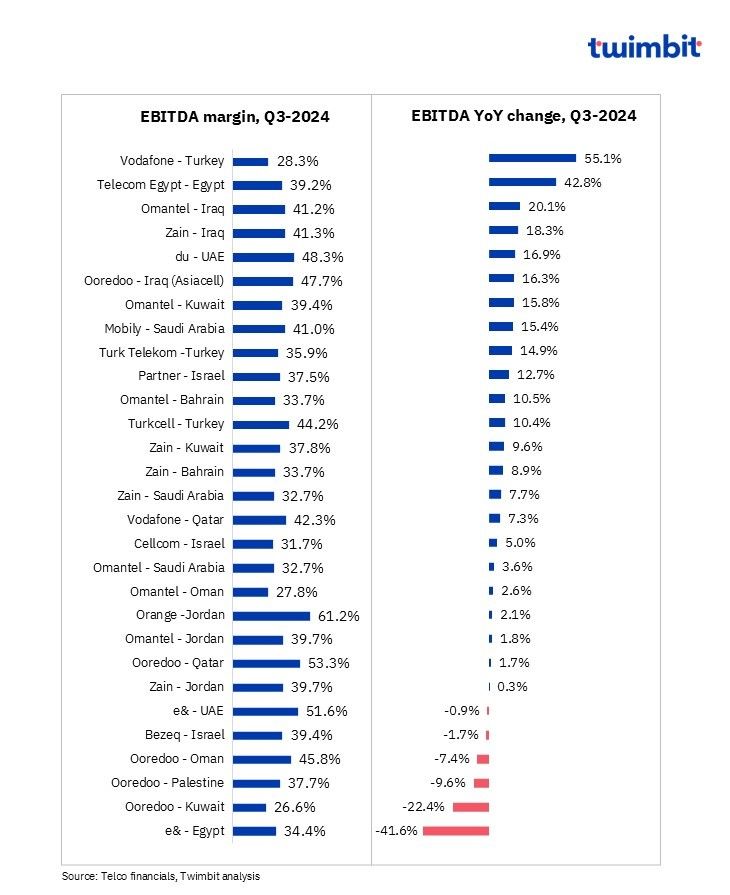

Average EBITDA margin for Middle East telcos stabilised at ~39% in Q3-2024

In Q3-2024, approximately 79% of telecom operators in the Middle East reported positive EBITDA growth, with 12 telcos (or about 41% of the total), achieving double-digit growth. This was led by robust revenue increase, enhanced operational efficiencies, and effective cost control measures. Nearly 24% of the telcos experienced slight EBITDA variations within a manageable range of -3% to +3%.

Exhibit 2: EBITDA and EBITDA margin trends of Middle East telcos, Q3-2024

Key highlights

- Strong top-line revenue growth, complemented by strategic cost optimization initiatives, facilitated EBITDA growth for many Middle East telecom operators.

- Telecom Egypt, Vodafone Turkey, and Turk Telecom demonstrated strong financial performance, achieving significant revenue growth and higher EBITDA margins. These companies also implemented successful cost-saving measures to enhance profitability.

- Telecom Egypt’s robust growth reflected its top-line revenue expansion and cost optimization efforts.

- Vodafone Turkey’s EBITDA growth was supported by service revenue increases, ongoing digitalization initiatives, and a continued focus on cost efficiency.

- Zain Group’s EBITDA increased across all operating regions due to relatively higher YoY revenue growth.

- Ooredoo Group reported EBITDA declines in three of its operating regions: Oman, Kuwait, and Palestine.

- In Oman, a decline in top-line revenue owing to competitive market situation impacted EBITDA, while in Kuwait, one-off bad debt provisions and increase in operating expense impacted EBITDA.

- The ongoing conflict in the Middle East adversely affected the EBITDA growth of Ooredoo Palestine and Bezeq Israel, primarily due to reduced roaming revenue. However, Israel-based Partner and Cellcom demonstrated resilience by achieving EBITDA growth through strategic cost reductions and growth in their fixed-line segments.

- Partner’s adjusted EBITDA increased by 12.7% YoY in Q3-2024, driven by a pre-tax profit of approximately USD 6.5 million (NIS 24 million) from leasing certain fibre optics (in the IRU model) to a business customer, growth in fixed-line service revenues, and reduced provisions for legal claims and other liabilities.

- Cellcom’s EBITDA growth was led by increased contributions from the fixed segment. Additionally, overall revenue growth, particularly from equipment sales, facilitated top-line revenue growth, resulting in improved EBITDA performance.

CAPEX analysis of Middle East telcos: Q3-2024

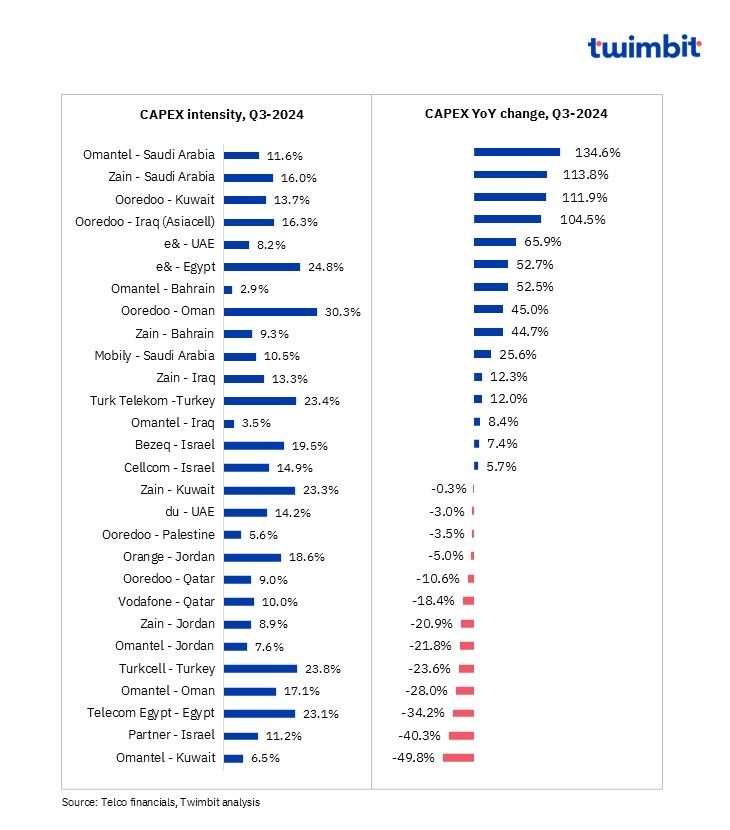

CAPEX intensity remained stable at ~14% (decline of 0.5% YoY) in Q3-2024, as network deployments across select key markets reaches completion

Nearly 54% of the telcos in Middle East reported a growth in YoY CAPEX spending in Q3-2024. CAPEX allocations are projected to stabilize as telcos reach completion of their 4G and 5G network deployments. However, new additional spending for fibre deployment, new 4G/5G network rollout coupled with investment in digital infrastructure for enterprises and digital capabilities is likely to propel the growth.

Exhibit 3: CAPEX and CAPEX intensity trends of Middle East telcos, Q3-2024

Key highlights

- Investment in 4G and 5G network expansion, fibre rollout, and digital capability enhancements continues to drive capital expenditure (CAPEX) in the Middle East.

- Zain Group’s CAPEX increased across most of its operating geographies, primarily allocated for expansion of 4G/5G networks, IT and BSS modernization, data centre upgrades, and transmission capacity enhancements.

- This increase in CAPEX has enabled Zain to enhance market penetration in Saudi Arabia and facilitate 4G and 5G network expansion in Bahrain.

- Zain Iraq partnered with Nokia to deploy advanced microwave technology, enhancing network capacity and customer experience.

- Ooredoo Group CAPEX increased ~30% YoY to USD 256.6 million (QAR 935 million), led by investments in Iraq, Kuwait, Oman, Algeria, Tunisia, and Qatar.

- In Sep- 2024, Ooredoo secured a QAR 2 billion, 10-year financing deal with QNB, Doha Bank, and Masraf Al Rayan to expand data centres, marking Qatar’s largest tech transaction.

- CAPEX witnessed a significant increase in Iraq and Kuwait for network expansion (including site and fibre) alongwith increased digital spendings.

- e& Group focused CAPEX on network expansion and modernization, enhancing capacity.

- In the UAE, spending targeted 5G rollout and network quality improvements.

- In Egypt, spending increased YoY for network rollout and capacity.

- Telcos in Israel (Bezeq and Cellcom) continued to focus on the expansion of their fibre infrastructure primarily to increase their market share, by increasing their home broadband penetration.

- CAPEX for select telcos declined due to prior committed investments and near completion of the infrastructure deployments.

- Turkcell’s CAPEX decreased owing to reduced spending in fixed, mobile, and international segments which accounted for 78% of total CAPEX in Q3-2023 as compared to 56% in Q3-2024.The focus now has shifted to data centres and solar renewable investments.

- Telecom Egypt’s CAPEX declined YoY, as the telco accelerated its spending in 2023 to pre-empt potential currency fluctuations and rising interest rates imposed by the Central Bank.

ARPU analysis of Middle East telcos: Q3-2024

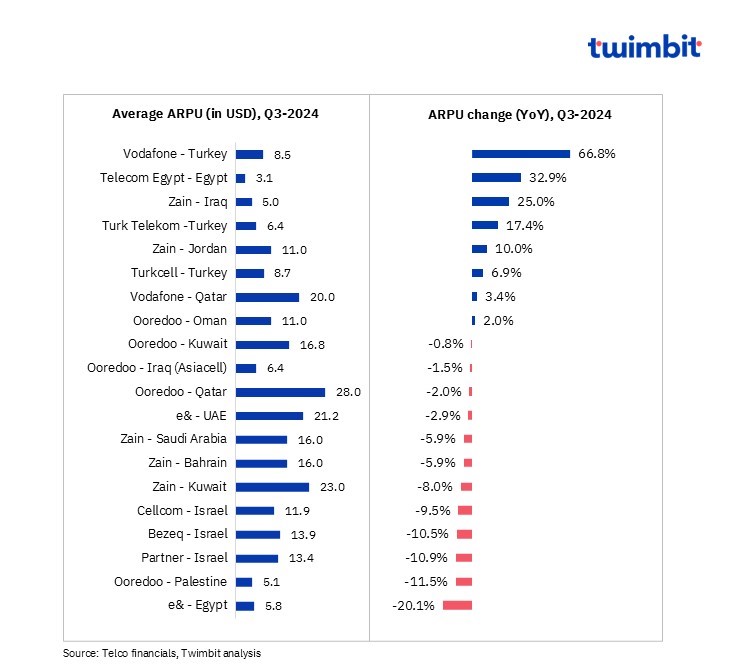

Average ARPU remained stagnant (0.4% YoY growth), at USD 12.6 in Q3-2024

In Q3-2024, nearly 40% of telecom operators in the Middle East reported YoY ARPU growth, facilitated by increased adoption of 4G/5G technologies and strategic price increment in select countries.

However, adverse macroeconomic conditions in geographies like Israel, Palestine, and Egypt exerted a counterbalancing effect on overall ARPU growth. Approximately 25% of the 20 telecom operators maintained stable ARPU levels, with YoY change ranging from -3% to 3%.

Exhibit 4: ARPU trends of telcos in the Middle East, Q3-2024

Key highlights

- Strategic pricing adjustments have driven ARPU growth for telecom operators in select regions. Price increases in Turkey (implemented in two phases: mid-February and end-June/early-July) and Egypt, along with a focus on postpaid segments in Qatar, have elevated ARPU levels.

- Telecom Egypt – Egypt: ARPU increased by 32.9% YoY to USD 3.1 (EGP 98) in Q3- 2024, driven by a price increase across all retail segments in January 2024. Additionally, higher data usage contributed to the ARPU growth.

- Vodafone – Turkey: Value-accretive customer base management alongwith price adjustments and continued customer base expansion, resulted in double-digit service revenue growth, resulting in higher ARPU levels.

- Turk Telekom – Turkey: ARPU grew by 17.4% YoY to USD 6.4 (TL 196.8), supported by growth in both prepaid (1.1% YoY) and postpaid ARPU (20.7% YoY). This was facilitated by a strong focus on higher postpaid plans and varied prepaid tariffs through promotional campaigns.

- Turkcell – Turkey: ARPU increased by 6.9% YoY to USD 8.7 (TL 270.9), driven by a 7.1% growth in postpaid subscriptions, strategic price adjustments, and successful upselling efforts.

- Vodafone – Qatar: The telco revamped its postpaid portfolio by introducing new plans with enhanced features, resulting in ARPU growth of 3.9% for postpaid and 4.5% for prepaid subscribers YoY in Q3-2024.

- Data revenue growth significantly contributed to ARPU increases for Zain Group in Iraq and Jordan.

- During Q3-2024, ARPU in Iraq rose by 25% YoY to USD 5 (reaching a new high during the quarter), whereas reported a 10% YoY growth in Jordan to USD 11.

- Conversely, a challenging operating environment led to ARPU declines for telecom operators in Israel and Palestine.

- Ooredoo – Palestine: ARPU declined by 11.5% YoY to USD 5.1 (QAR 18.5), despite an increase in the subscriber base. The telco offered free integrated bundles, including voice and data packages, to ensure continued connectivity.

- Partner – Israel: ARPU decreased by 10.9% YoY to USD 13.4 (NIS 49), due to lower roaming revenues and cessation of revenue recognition from Hot Mobile.

- Cellcom – Israel: ARPU fell by 9.5% YoY to USD 11.9 (NIS 43.7).

- Bezeq – Israel: ARPU declined by 10.5% YoY to USD 13.9 (NIS 51), impacted by the war’s effect on roaming revenues, partially offset by higher ARPU from cellular plans, despite overall subscriber growth, including 5G and postpaid subscribers.

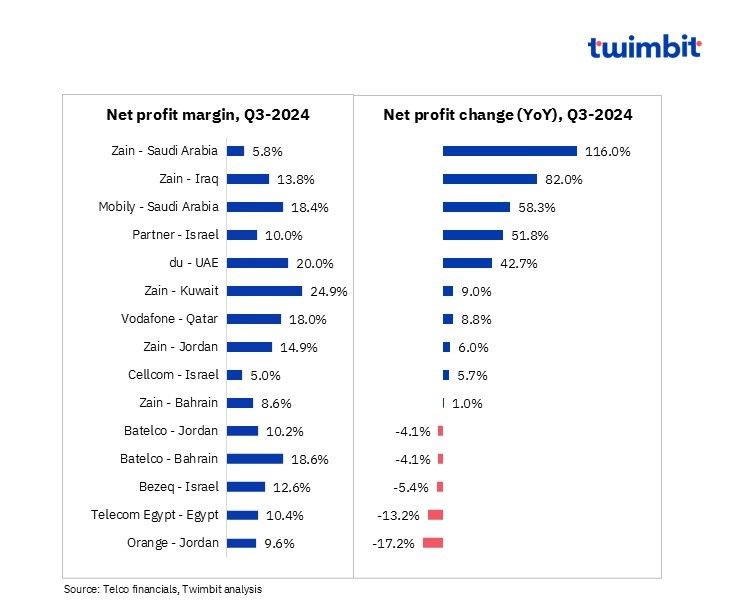

Profitability analysis of Middle East telcos: Q3-2024

Increased expenses coupled with macroeconomic factors outclass revenue growth rates impacting the profitability of telcos in Middle East

Among the 15 telecom operators analysed, approximately 67% reported net profit growth in Q3-2024, compared to around 80% in Q3-2023. This decline indicates underlying expenses and macroeconomic factors overshadowing the impact of revenue growth However, this performance is an improvement over Q2-2024, where only 53% of telcos experienced growth.

Exhibit 5: Net profit trends for Middle East telcos, Q3-2024

Higher revenue growth, primarily driven by data and digital services, along with effective cost management initiatives, facilitated profitability for the majority of telecom operators, including Zain (in Saudi Arabia, Iraq, Bahrain, Jordan, and Kuwait), Mobily, Partner Israel, and Vodafone Qatar.

Conversely, macroeconomic challenges, coupled with increased expenses—such as a 2.5x rise in interest expenses and foreign exchange losses, resulted in a 13.2% YoY decline in net profit for Telecom Egypt in Q3-2024.

Key strategic developments: Q3-2024

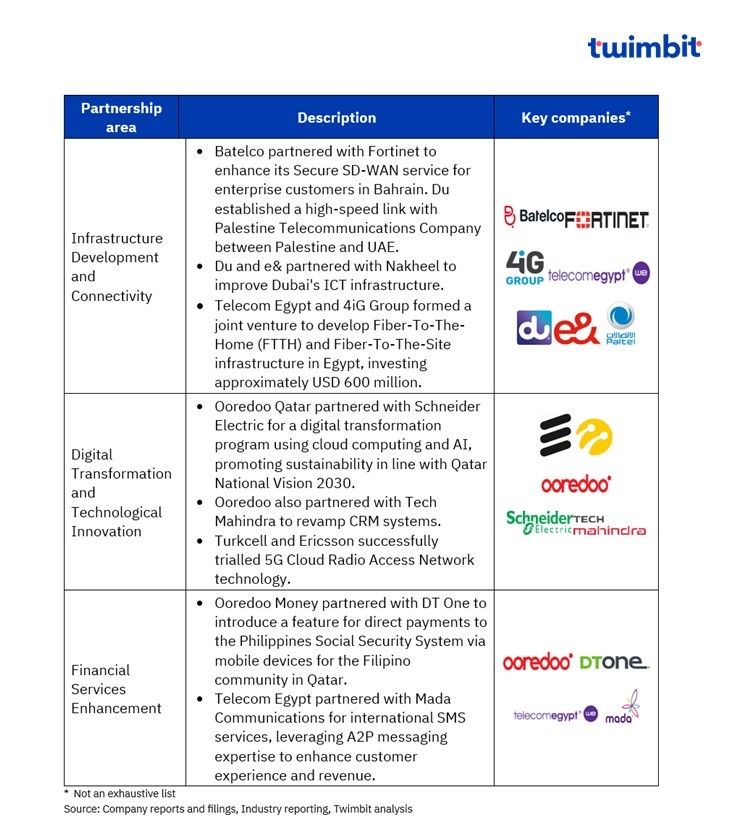

Key strategic partnerships and alliances: Q3-2024

- Telcos in Middle East actively pursue partnerships to drive digital transformation and enhance service offerings. Collaborations focus on improving network infrastructure, cybersecurity, customer experience, and financial services. These initiatives highlight the industry’s commitment to innovation and meeting the evolving needs of customers in the region.

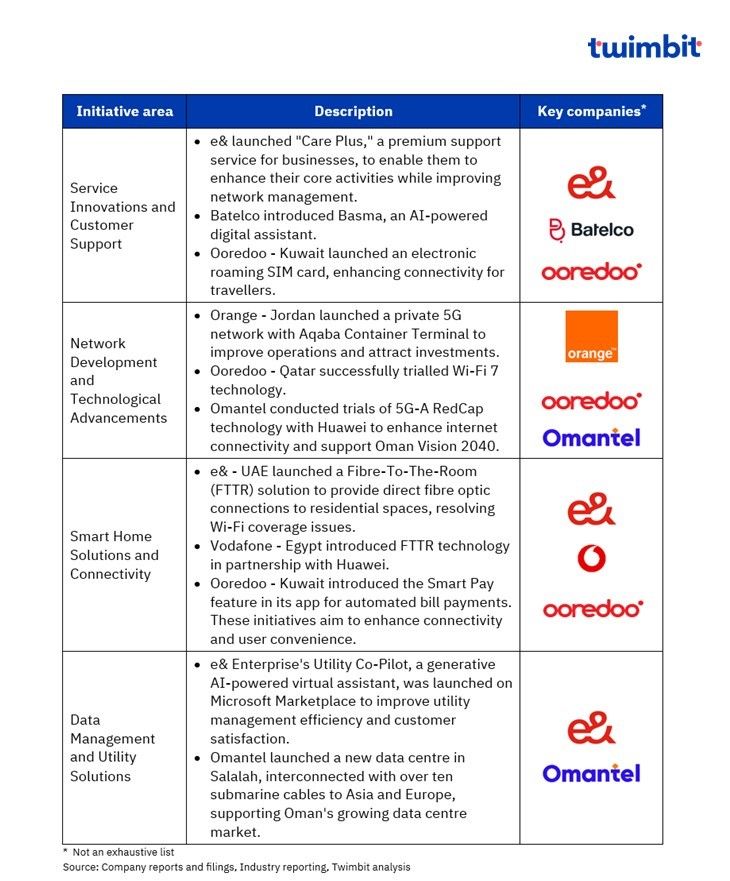

Key strategic initiatives: Q3-2024

- The Middle East telecom industry continues to innovate rapidly to enhance customer experience and support digital transformation. From personalized support services to advanced technologies like 5G and AI, the telecom providers continue to invest in cutting-edge solutions to meet evolving customer needs and drive growth.

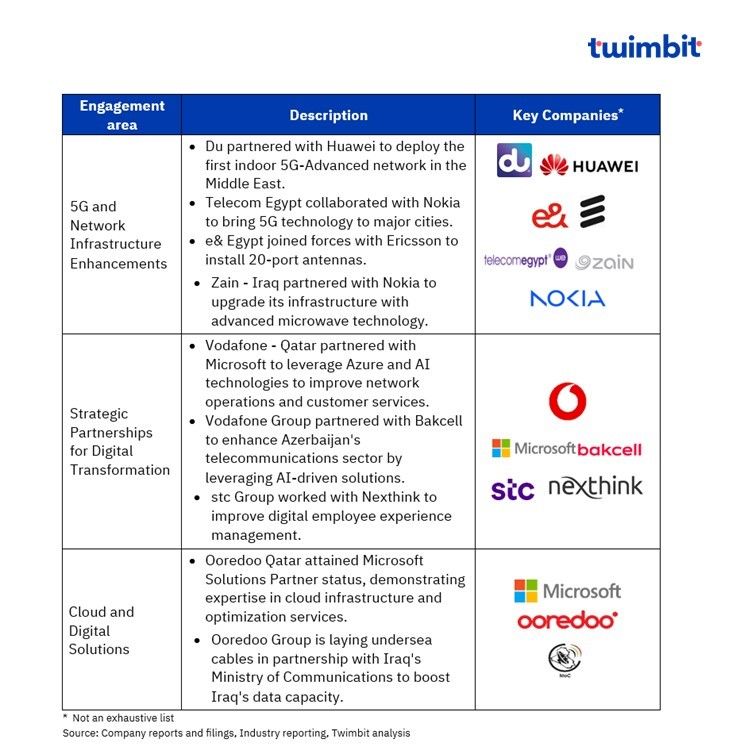

Key contract wins: Q3-2024

- Telcos in Middle East continue to adopt advanced technologies and form strategic partnerships to enhance network capabilities, improve customer experiences, and drive digital transformation. From deploying 5G networks and upgrading infrastructure to leveraging AI and cloud solutions, these collaborations demonstrate a commitment to innovation and meeting the evolving needs of customers and businesses.

Research Methodology and Assumptions

- The “Middle East Telcos Performance Benchmarks: Autumn 2024” report offers crucial insights into the performance of telecom companies. It analyses key financial indicators such as Revenues, EBITDA, CAPEX, ARPU, and Net Profit for Q3-2024 (July – September 2024).

- This report utilizes data collected from telecom firms and extensive secondary research. Twimbit follows a calendar year for its data analysis, with FY representing January to December.

- To maintain consistency and enable accurate comparisons, the report applies a constant currency conversion rate, reflecting the average USD exchange rate for July – September 2024.

- The report evaluates Revenue and EBITDA for 35 and 29 telecom companies, respectively. CAPEX and ARPU analyses cover data from 28 and 20 companies, respectively. Net profitability assessment is based on data from 15 telecom firms.

- Blended mobile ARPU has been incorporated wherever relevant to provide a more holistic view.

- The data presented in this report is based on the most current information available at the time of compilation. As such, it may not reflect subsequent developments. This report is intended for informational purposes only and should not be relied upon as a substitute for independent research.