Key takeaways

- The average year-over-year (YoY) revenue growth for Middle East telcos improved from 3.9% in Q2-2023 to 4.3% in Q2-2024.

- The 34 telcos analysed in Q2-2024 generated a combined revenue of USD 17.5 billion. Nearly 71% of these telcos experienced positive revenue growth, with four telcos reporting YoY gains exceeding 10%.

- The average EBITDA margin remained stable at approximately 40% in Q2-2024 for the 28 telcos analysed.

- In Q2-2024, nearly 75% of telcos demonstrated positive EBITDA growth, with eight telcos achieving double-digit growth.

- The average capital expenditure (CAPEX) intensity rose to 13% in Q2-2024 due to slight increase in spending for network deployments and expansion. Nearly 52% of the 27 telcos in the Middle East increased their year-over-year CAPEX spending in Q2-2024.

- The competitive landscape and challenging macroeconomic conditions contributed to a marginal 2.5% YoY decline in ARPU in Q2-2024. Nearly 58% of Middle East telcos experienced a year-over-year decline in ARPU in Q2-2024.

- Of the 15 telcos analysed, nearly 53% reported net profit growth in Q2-2024, compared to approximately 67% in Q2-2023. The ongoing conflict in Middle-east alongwith intense competition impacted the market in countries like Israel, Jordan, Kuwait, Saudi Arabia.

Revenue analysis of Middle East telcos: Q2-2024

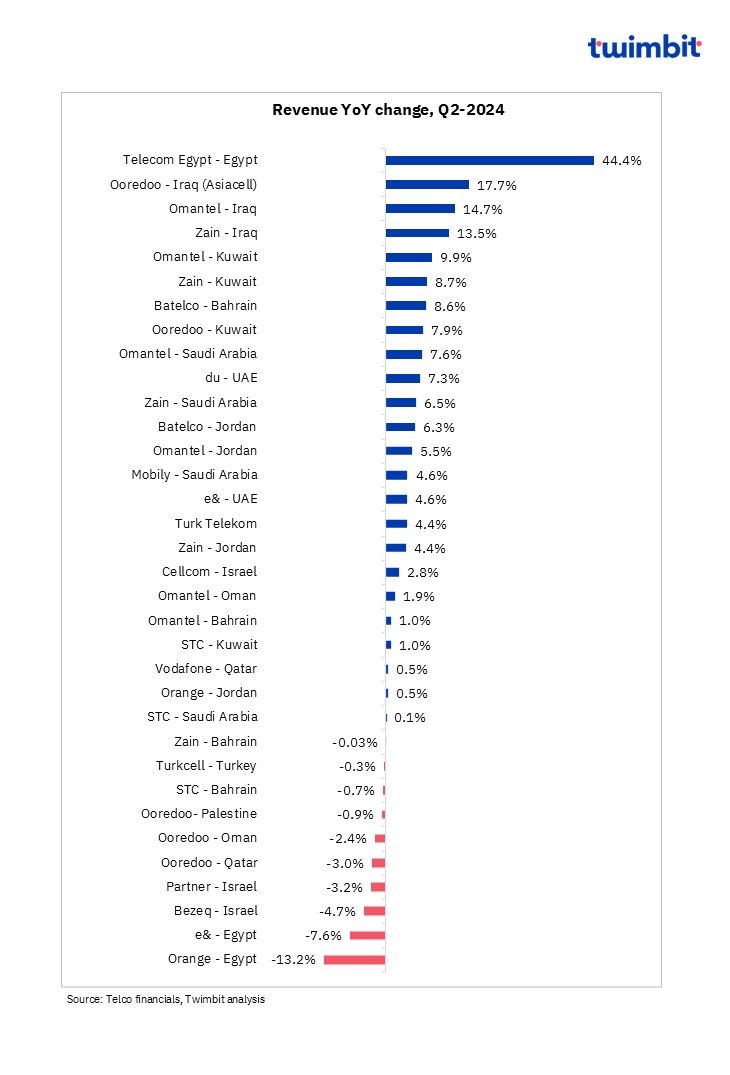

Average revenue growth* for Middle East telcos increased from 3.9% in Q2-2023 to 4.3% in Q2-2024

In the second quarter of 2024, telcos in the Middle East region reported a total revenue of USD 17.5 billion, marking net revenue addition of approximately USD 676 million on YoY basis.

Approximately 71% of telcos in Q2-2024 reported positive revenue growth, with 4 telcos achieving double-digit growth.

Exhibit 1: Revenue trend of telcos in the Middle East, Q2-2024

Key highlights

- Telcos like Telecom Egypt and Mobily – Saudi Arabia experienced revenue growth with improvement in price and expanding subscriber base.

- Network expansion by telcos such as Ooredoo – Iraq (Asiacell) and du in the UAE led to a surge in data usage, consequently boosting their revenue.

- Zain Group and Omantel Group witnessed revenue growth across most Middle Eastern countries, primarily driven by increased data revenue. Bahrain was an exception for Zain, where revenue remained relatively stagnant.

- Despite decline in YoY ARPU, telcos such as Cellcom – Israel, e& – UAE, Zain – Kuwait, Zain – Saudi Arabia registered revenue growth, primarily led by increased subscriber numbers.

- In Egypt, the revenue of e& – Egypt and Orange – Egypt was negatively affected by macroeconomic challenges such as currency devaluation and inflation. However, Telecom Egypt’s strong market position and diversified service portfolio enabled it to achieve revenue growth.

- Telcos operating in Israel (Partner and Bezeq) and Palestine (Ooredoo) experienced a decline in revenue, primarily attributed to reduced cellular revenue amidst a challenging operating environment.

Telecom Egypt – Egypt

Revenue increased by 44.4% YoY, reaching USD 631.7 million (EGP 20.5 billion) in Q2-2024, primarily led by growth in Retail services segment.

- Retail services segment revenue grew 46% driven by growth in both Home & Consumer and Enterprise segments.

- Home & Consumer segment revenue surged 44.7% YoY, driven by growth in revenue from data (up 48.6%) and voice (up 26%). Price hikes and growing subscribers (8%) drove this growth.

- Enterprise solutions segment revenue grew 51.4% YoY, primarily due to managed data revenue increasing 39% in Q2-2024.

Ooredoo – Iraq (Asiacell)

Revenue rose by 17.7% YoY to USD 342.8 million (QAR 1.3 billion) in Q2-2024, driven by customer additions, increased adoption of data services and favourable market dynamics.

- Overall subscriber count increased by 7.2% YoY to 18.3 million in Q2-2024, whereas ARPU grew by 4.6% YoY to USD 59.2 million (QAR 22.8).

Omantel – Iraq

Revenue increased 14.7% YoY to ~USD 261.8 million (RO 100.8 million) in Q2-2024, primarily driven by 15% YoY increased in airtime, data & subscription revenue to USD 260.5 million (RO 100.3 million).

Zain – Iraq

Revenue grew by 13.5% to USD 262.9 million (KWD 80.8 million) in Q2-2024, driven by a 7.3% rise in subscriber count and data revenue.

- A 24% YoY growth in B2B revenue alongwith contributions from its “Digital Services” and “oodi” also resulted in overall revenue growth.

Omantel – Kuwait

Revenue increased by 9.9% YoY to USD 301.3 million (RO 116 million), primarily led by 49.3% increase in Trading income (Point in time) to USD 104.7 million (RO 40.3 million), which offset the decline in airtime, data & subscription revenue.

Orange – Egypt

Revenue declined by 13.2% YoY to USD 178.2 million (EUR 165 million) in Q2-2024. Despite a 6% increase in mobile access and 9% increase in fixed access base, Orange could not offset the impact of high inflation.

e& – Egypt

Revenue decreased 7.6% YoY to USD 224.8 billion (AED 825.6 million) due to negative impact in foreign exchange movements due to Egyptian Pound (EGP).

- However, in local currency, revenue increased 42.6% YoY in Q2-2024, driven by growth in mobile data and voice service revenue alongwith overall subscriber growth.

Bezeq – Israel

Revenue declined 4.7% YoY to USD 596.4 million (NIS 2.2 billion), as the Core decreased 0.9%, to USD 528 million (NIS 1.94 billion), due to lower revenues from infrastructure projects in Bezeq Fixed-Line and lower roaming revenues in Pelephone impacted by the war.

Partner – Israel

Revenue declined by 3.2% YoY to USD 223.9 million (NIS 823 million), due to a 5.7% decrease in cellular revenue, which offset growth in the fixed-line segment.

- Cellular revenue decreased by 5.7% YoY, primarily driven by an 11.6% decline in services revenue. This decline was partially offset by a 13% increase in equipment revenue.

- Additionally, a 1.3% decrease in cellular subscriptions (predominantly in the postpaid segment) and a 9% decline in ARPU contributed to the overall revenue decline.

- Fixed-line revenue increased by 3% YoY, driven by a 4.8% increase in service revenue. This growth was primarily attributable to a 21% increase in fibre-optic subscribers, reaching 0.4 million.

- However, equipment revenue declined by 23.1% YoY to USD 2.7 million in Q2-2024.

Ooredoo – Qatar

Revenue decreased 3% YoY to USD 473.2 million (QAR 1.8 billion) in Q2-2024. Revenue in Q2-2023 was higher owing to the FIFA 2022 contracts for B2B services, revenue from Data centre carve out and one-off Project revenue.

- Decline in mobile blended ARPU (owing to decline in both prepaid and postpaid segment) and fixed line ARPU decline resulted in overall revenue decline.

EBITDA analysis of Middle East telcos: Q2-2024

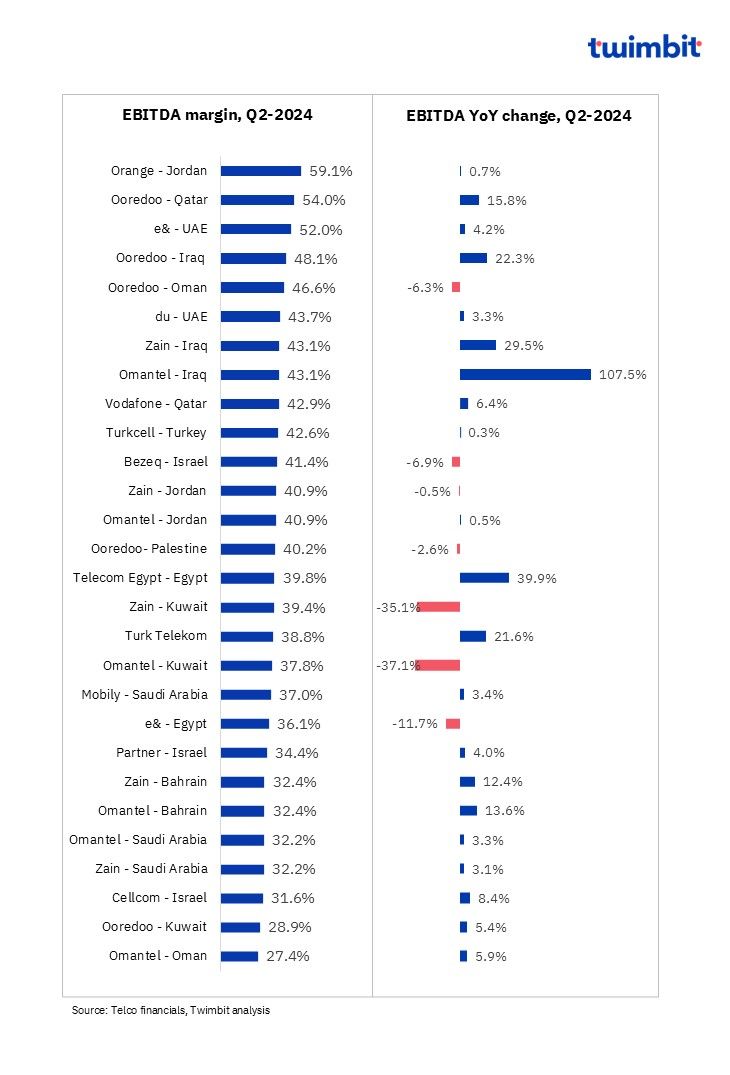

Average EBITDA margin for Middle East telcos stabilised at ~40% in Q2-2024

In Q2-2024, nearly 75% of telcos reported positive EBITDA growth, with 8 telcos recording double-digit EBITDA growth. However, only 18 % of telcos reported a slight EBITDA variation within a manageable range (-3% to +3%).

Exhibit 2: EBITDA and EBITDA margin trends of Middle East telcos, Q2-2024

Key highlights

- Telcos like Omantel-Iraq, Telecom Egypt, and Cellcom-Israel demonstrated strong financial performance, achieving significant revenue growth and higher EBITDA margins. These telcos also successfully implemented cost-saving measures to further improve their profitability.

- The ongoing conflict in the Middle East adversely affected the EBITDA growth of Ooredoo – Palestine and Bezeq – Israel, primarily due to a decline in roaming revenue. However, Israel based Partner exhibited resilience by achieving EBITDA growth through strategic cost reductions in its fixed-line segment.

Telecom Egypt – Egypt

EBITDA increased 39.9% YoY to USD 251.3 million (EGP 8.1 billion) in Q2-2024 driven by strong topline growth coupled with cost optimisation initiatives taken, thereby softening the inflation pressure owing to currency devaluation.

Zain – Iraq

EBITDA surged by 29.5% YoY to USD 113.4 million (KWD 34.8 million) in Q2-2024. The growth was driven by a combination of strong revenue growth and reduced expenses, resulting in a significant increase in net profit before interest and tax.

Turk Telekom – Turkey

EBITDA increased 21.6% YoY to USD 403.2 million (TL 12.8 billion) in Q2-2024, driven by a 4.1% reduction in operating expenses, owing to lower direct costs and network and technology costs.

Omantel – Kuwait

EBITDA declined 37.1% YoY to USD 113.7 million (RO 43.8 million), due to increase in expenses resulting in ~57% reduction in Net profit before interest and tax.

e& – Egypt

EBITDA declined by 11.7% YoY to USD 81.1 million (AED 297.8 million). However, in constant currency EBITDA sustained outstanding double-digit growth of 36.5% attributed to revenue growth.

Bezeq – Israel

EBITDA declined by 6.9% YoY to ~USD 246.8 million (NIS 907 million), owing to reduced telephony revenues and increase in operating expenses owing to growth in advertising and salary related expenses.

CAPEX analysis of Middle East telcos: Q2-2024

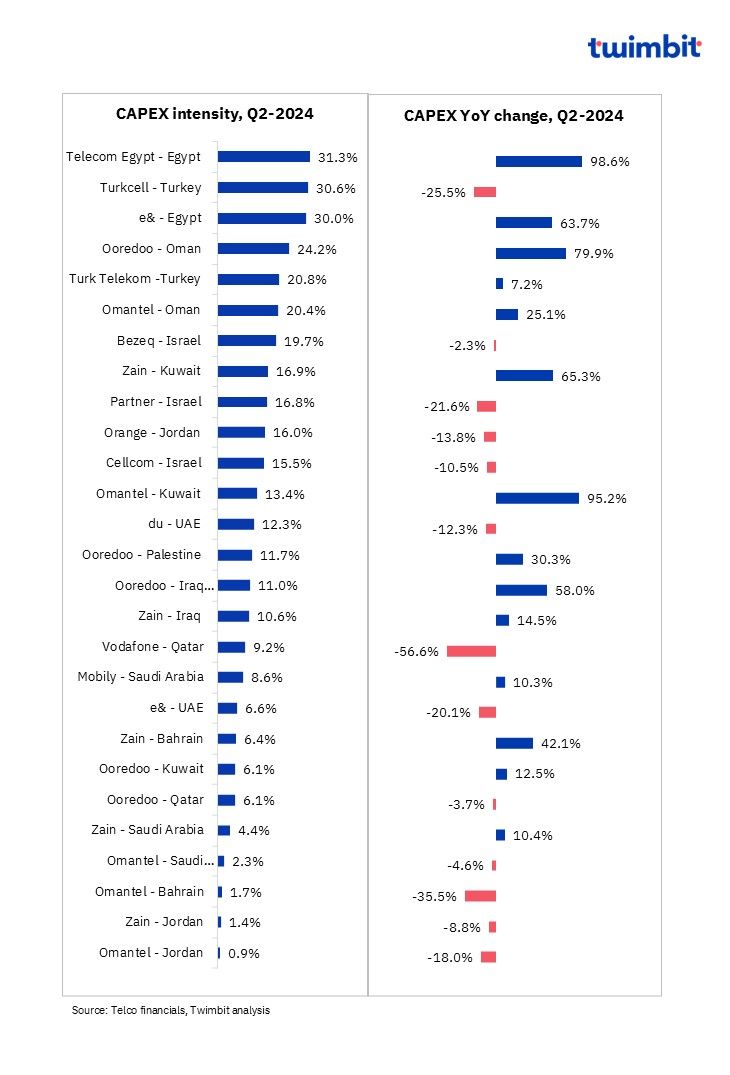

CAPEX intensity increased to 13% of overall revenue for telcos in the Middle East, as spending increased marginally for network deployments and expansion

Nearly 52% of the telcos in Middle East reported a growth in YoY CAPEX spending in Q2-2024. CAPEX allocations are projected to stabilize as companies complete their 4G and 5G network deployments.

Exhibit 3: CAPEX and CAPEX intensity trends of Middle East telcos, Q2-2024

Key highlights

- e& – Egypt expanded its network coverage and capacity, while Telecom Egypt focused on upgrading its access network and international cable infrastructure.

- Zain Group increased its CAPEX in most of its operating countries to enhance its 4G and 5G network infrastructure.

- Israel-based telcos reported a YoY decline in CAPEX spending in Q2-2024. Partner-Israel’s spending decreased due to the completion of its fibre optic deployment in FY-2023. Bezeq – Israel’s spending moderated in both fixed-line and mobile segments, reflecting ongoing network investments.

- Near-completion state of network deployments resulted in reduced CAPEX spending by telcos such as Partner – Israel and e& – UAE. The moderated CAPEX spending of du – UAE aligns with typical phasing pattern, as it prioritizes 5G expansion, fibre deployment, and IT and network infrastructure transformation.

Telecom Egypt – Egypt

CAPEX spending surged form USD 99.4 million (EGP 3.2 billion) in Q2-2023 to USD 197.5 million (EGP 6.4 billion) in Q2-2024, driven by increase in spending across Access network, Transmission, International cable and Customer care.

- Spending for Access network (accounting for 67% of the In-Service capex) grew 5x times to ~USD 133 million (EGP 4.3 billion).

Zain – Kuwait

With aims to strengthen its 4G and 5G network presence, CAPEX spending reported an increase of 65.3% YoY to USD 51.2 million (KWD 15.7 million) in Q2-2024. CAPEX intensity increased from 11.1% in Q2-2023 to 16.9% in Q2-2024.

Turkcell- Turkey

Turkcell – Turkey CAPEX spending reduced 25.5% YoY to USD 336.8 million (TL 10.7 billion) in Q2-2024, due to reduction in licence and related costs, leading to a reduction in CAPEX intensity of 30.6% YoY in Q2-2024.

Partner – Israel

Following the completion of the independent fibre optic network deployment, CAPEX spending decreased to USD 37.5 million (NIS 138 million) in Q2-2024, leading to a 390 bps YoY reduction in CAPEX intensity, reaching 16.8% for the quarter.

ARPU analysis of Middle East telcos: Q2-2024

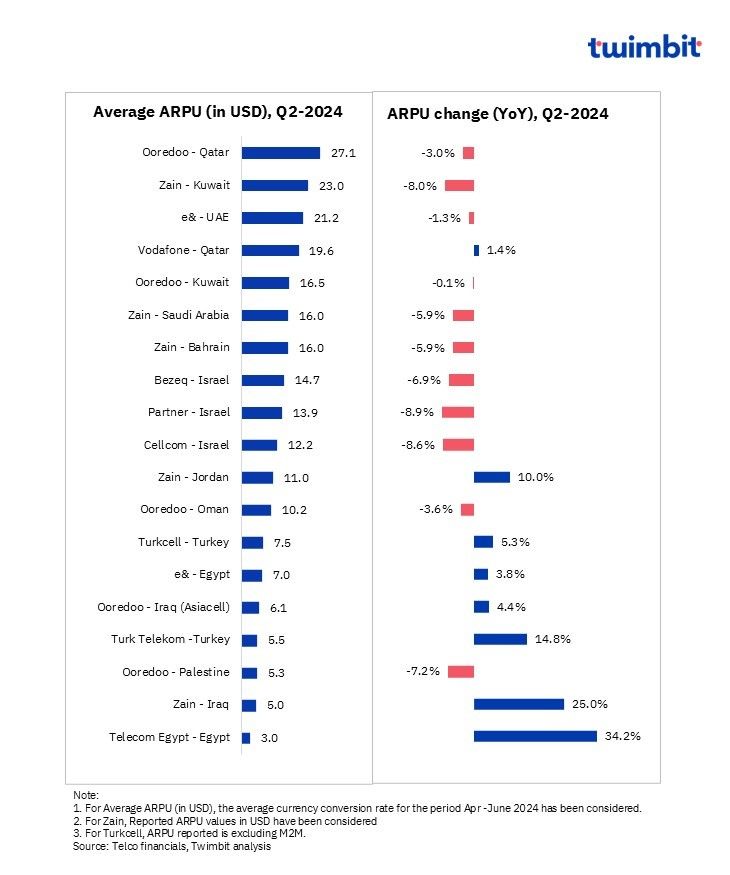

Increased competition intensity and a challenging macroeconomic environment led to average ARPU decline marginally by 2.5% YoY in Q2-2024

Nearly 58% of Middle East telcos reported declining YoY ARPU in Q2-2024. Around 21% of the 19 telcos maintained stable ARPU levels, with YoY changes ranging from -3% to 3%. Notable examples include Ooredoo – Qatar, Ooredoo – Kuwait, Vodafone – Qatar, e& – UAE.

Exhibit 4: ARPU trends of telcos in the Middle East, Q2-2024

Strategic price adjustments led to the ARPU growth of telcos in Egypt and Turkey. Telcos in Turkey completed price revisions in two-phases: mid-February and end-June/early-July, resulting in upliftment of ARPU levels.

- Telecom Egypt – Egypt: ARPU increased 34.2% YoY to USD 3 (EGP 98) in Q2-2024, driven by price increment implemented in January -2024 across all the retail segments. Additionally, increased data usage also contributed to the ARPU upliftment.

- Turk Telekom – Turkey: ARPU grew 14.8% YoY to USD 5.5 (TL 174.5), driven by growth in both prepaid and postpaid ARPU facilitated by intensive focus on higher postpaid plans along with varying prepaid tariffs through promotional campaigns.

- Turkcell – Turkey: ARPU grew 5.3% YoY to USD 7.5 (TL 237.6), driven by growth in post-paid subscriptions (growth of 6.8%), strategic price adjustments, successful upselling efforts.

The growth in data revenue significantly contributed to an increase in average revenue per user (ARPU) for Zain Group in Iraq and Jordan.

- Zain – Iraq: ARPU increased 25% YoY to USD 5 achieving a new high level during the quarter.

- Zain – Jordan: ARPU increased 10% YoY to USD 11.

Challenging operating environment resulted in ARPU decline for telcos based in Israel and Palestine.

- Ooredoo – Palestine: ARPU declined 7.2% YoY to USD 5.3 (QAR 19.7)

- Partner – Israel: ARPU declined 8.9% YoY to USD 13.9 (NIS 51)

- Cellcom – Israel: ARPU declined 8.6% YoY to USD 12.2 (NIS 44.8)

- Bezeq – Israel: ARPU declined 6.9% YoY to USD 14.7 (NIS 54) due decreased roaming revenue due to war. However, its ARPU increased from NIS 43 in Q1-2024 to NIS 44 in Q2-2024 led by growth in 5G and postpaid subscriptions.

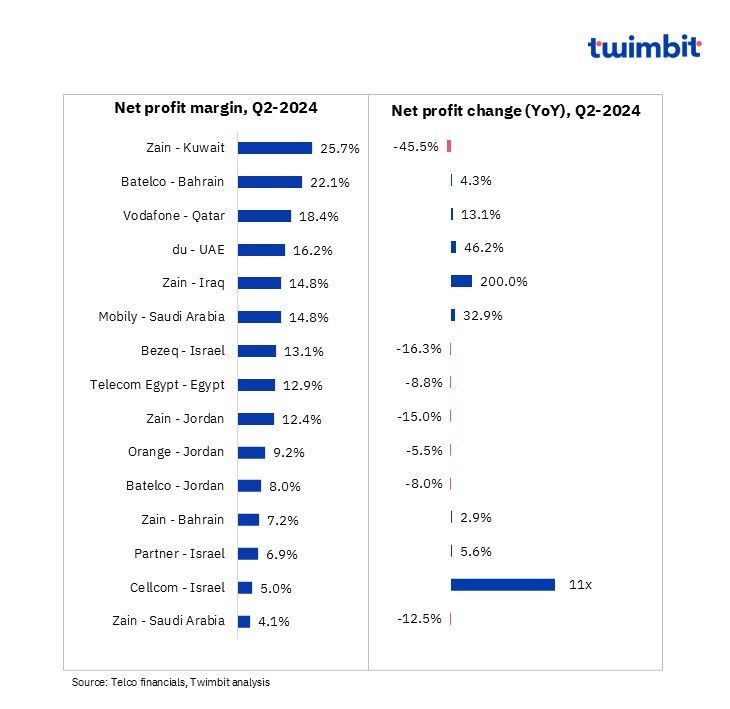

Profitability analysis of Middle East telcos: Q2-2024

Growth in net profit has been a challenge for telcos amidst competition and a challenging economic environment

Out of the 15 telcos analysed, nearly 53% of the telcos reported net profit growth in Q2-2024 compared to ~67% of the telcos in Q2-2023.

Exhibit 5: Net profit trends for Middle East telcos, Q2-2024

Key highlights

- Higher revenue growth rate primarily attributed to data and digital services facilitated profitability growth of the telcos such as Zain Iraq.

- Macroeconomic challenges, increased expenses, relatively lower revenue growth rate owing to increased competition led to profitability decline for some of telcos like Telecom Egypt, Orange – Jordan to mention a few.

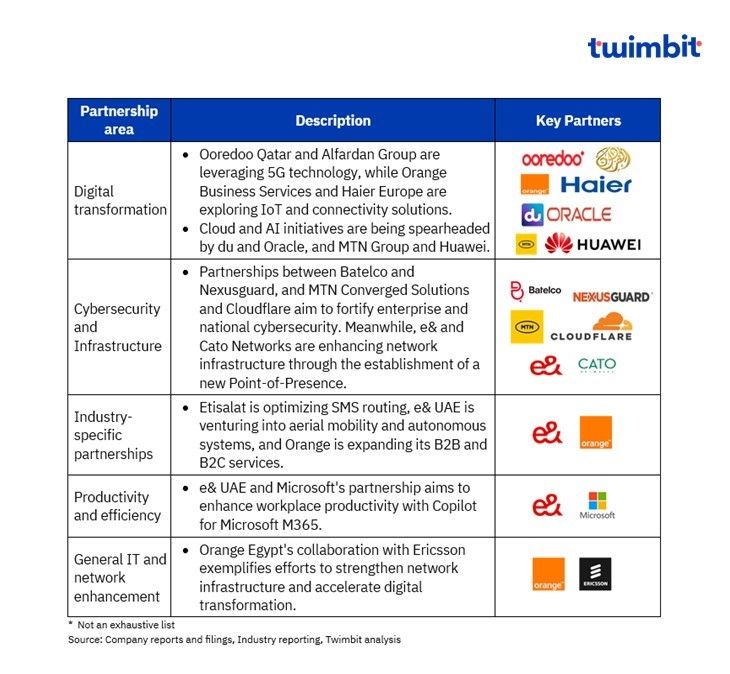

Key strategic developments: Q2-2024

Key strategic partnerships and alliances*: Q2-2024

Telecommunications companies are forming strategic partnerships to enhance cybersecurity, drive digital transformation, and optimize operations. Key areas of focus include cloud, AI, IoT, 5G, and network infrastructure.

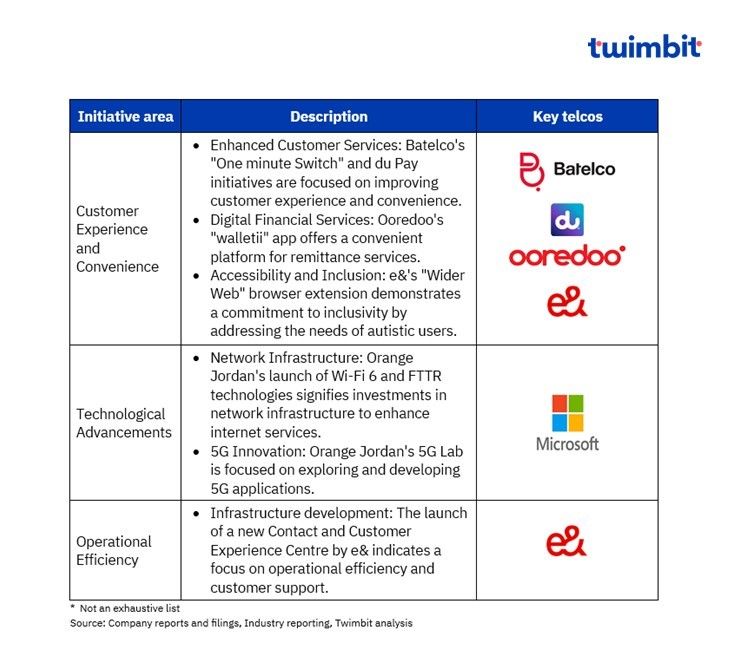

Key strategic initiatives*: Q2-2024

Telecom providers are prioritizing customer experience, digital innovation, and network expansion, with key initiatives centred around enhancing and offering services, financial solutions, accessibility, and advanced technologies.

Key contract wins*: Q2-2024

Telcos in the Middle East are strategically aligning with technology partners to drive digital transformation and enhance operational efficiency. Key areas of focus include leveraging AI for innovation and customer experience, modernizing network infrastructure, and delivering specialized solutions for industries such as public sector and utilities.

Research Methodology and Assumptions

- The “Middle East Telcos Performance Benchmarks: Summer 2024” report offers crucial insights into the performance of telecom companies. It analyses key financial indicators such as Revenues, EBITDA, CAPEX, ARPU, and Net Profit for Q2-2024 (April – June 2024).

- This report utilizes data collected from telecom firms and extensive secondary research. Twimbit follows a calendar year for its data analysis, with FY representing January to December.

- To maintain consistency and enable accurate comparisons, the report applies a constant currency conversion rate, reflecting the average USD exchange rate for April – June 2024.

- The report evaluates Revenue and EBITDA for 34 and 28 telecom companies, respectively. CAPEX and ARPU analyses cover data from 27 and 19 companies, respectively. Net profitability assessment is based on data from 15 telecom firms.

- Blended mobile ARPU has been incorporated wherever relevant to provide a more holistic view.

- The data presented in this report is based on the most current information available at the time of compilation. As such, it may not reflect subsequent developments. This report is intended for informational purposes only and should not be relied upon as a substitute for independent research.

Click here for more contents on telecom

Related Middle East telcos performance insights

Global telecom vendors performance indicators – Summer 2024