Key Takeaways

- Annual revenue growth for Middle East telcos moderated to 4.8% in FY-2023, reaching ~USD 69.2 billion. This is lower than the 5.3% YoY growth in FY-2022. A positive trend is that 85% of analysed telcos reported revenue growth, with five achieving double-digit increases.

- The average ARPU level remains stagnant at ~USD 13 over the last 2 years in the Middle East region. ARPU growth rates have stagnated or declined in major GCC countries due to increased competition and a challenging macroeconomic environment.

- Telcos strategically target the Enterprise (B2B) segment with “Beyond Connectivity” offerings as an alternate revenue stream. Telcos are repositioning themselves as one-stop shops to cater to the full spectrum of their customers’ digital service requirements.

- Telcos are also aligning their business focus on new and innovative adjacent offerings like AR/VR, Metaverse, IoT, Smart home to boost revenue generation beyond traditional technology offerings.

- Telcos are also pursuing selective acquisitions and strategic partnerships to enhance their resiliency. This enables them to monetise their existing infrastructure investments and cater to the evolving needs of their customers.

- Telcos embrace Artificial Intelligence (AI) to facilitate greater process efficiency. Leading telcos like STC, Mobily, e& are strategically integrating AI to boost profitability and enhance operational efficiency.

- With the 5G network deployment and launch completed across most of the Middle East countries, the CAPEX spending reduced in FY-2023. Nearly one-third of telcos analysed reported a YoY decline in CAPEX spending in FY-2023 compared to FY-2022.

- The overall EBITDA margin for 28 telcos remains stable at ~38%, driven by a focus on cost efficiency and healthy revenue growth.

- In FY-2023, nearly 75% of the 28 analysed telcos showed positive EBITDA improvement, including 9 telcos witnessing a double-digit EBITDA growth. Marginal EBITDA decline (under 2%) was reported by ~11% of the telcos.

- The YoY change in EBITDA rate was relatively higher for Iraq-based telcos owing to the cancellation of sales tax on telecom services starting December-2022.

- Around 88% of the 16 telcos analysed reported growth in net profit, except for Batelco – Bahrain and Israel’s Cellcom.

- Return on Capital Employed (ROCE) improved for most telcos, with 77% of the telcos (including group conglomerates) in FY-2023 reporting growth, thereby indicating better capital utilisation.

- Telcos should continue to invest and monetise their 5G infrastructure for innovative service offerings. The robust GCC economy, the Government’s digitalisation programs and the surge in smart city projects also create significant demand for 5G capabilities.

- Telcos focus on cybersecurity implementations to address vulnerabilities arising from rapid 5G rollout and evolving network complexities. Prioritising protection of key network infrastructure is the key to managing the increasing number of cyberattacks and data breaches.

Revenue analysis of Middle East telcos: 2023

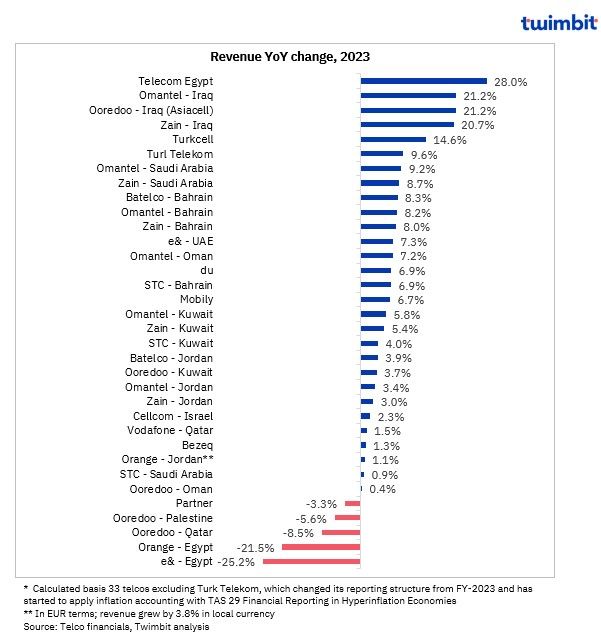

Average revenue growth* for Middle East telcos has slowed from 5.3% in FY-2022 to 4.8% in FY-2023

Nearly 36% of telcos recorded higher YoY revenue growth rates in FY-2023. Despite the slowdown, the telcos generated a combined revenue of ~USD 64.8 billion (USD 69.2 billion, including Turk Telekom).

Cumulatively, this represented a YoY growth of ~USD 3 billion in FY-2023 (~3.4 billion, including Turk Telekom). Furthermore, 85% of the telcos reported positive revenue growth, with 5 telcos achieving double-digit growth.

Exhibit 1: Revenue trend of telcos in the Middle East (YoY basis), 2023

Telecom Egypt

Revenues increased 28% YoY to reach ~USD 1.8 billion (EGP 56.7 billion) in FY-2023. Within fixed line, voice and data subscribers grew by 7.7% and 8.6% in FY-2023 to reach 12.5 million and 9.5 million subscribers. Telecom Egypt also recorded positive YoY revenue growth across all business segments.

- Home & Consumer (15.3%)

- Enterprise (8.4%)

- Domestic wholesale (27.9%)

- International carriers (58.8%)

- International Customers & Networks (72.9%)

Omantel – Iraq

Revenues increased 21.2% YoY to ~USD 962.1 million (RO 370.4 million) in FY-2023. Factor such as removal of tax on telecom services and local currency appreciation against USD led to revenue growth.

Ooredoo -Iraq (Asiacell)

Revenues increased 21.1% YoY to USD 1.2 billion (QAR 4.5 billion) in FY-2023. 2 key factors drove this revenue growth:

- Overall subscriber count increased by 3.5% YoY in FY-2023 to reach 17.7 million

- Additionally, it also reported a 25.9% YoY growth in ARPU

Zain – Iraq

Revenues increased 20.7% YoY to USD 974.2 million (KWD 299.4 million) in FY-2023. Favourable market dynamics alongwith strengthening of the Iraqi dinar against the US dollar in FY-2023.

Turkcell

Revenues increased 14.6% YoY to USD 4.6 billion (TL 107.1 billion) in FY-2023. Turkcell Türkiye accounted for ~88% of the Group revenue and reported 18% YoY revenue growth to reach ~USD 4 billion (TL 91.953 billion).

- Consumer business revenue increased 18.7% YoY, driven by subscriber net additions in mobile and fixed segments, price adjustments, and upsell efforts

- Corporate revenues increased by 20.3% YoY, driven by a 23% increase in digital business services revenue

- Standalone digital services revenues from consumer and corporate segments grew 19.4% YoY due to the expansion in the standalone paid user base

- Wholesale revenues grew 3.3% YoY to USD 0.3 billion (TL 6.5 billion)

e& – Egypt

Revenues declined 25.2% YoY to USD 997.4 million (AED 3.7 billion) in FY-2023.

- 12.7% increase in subscriber count to reach 33.9 million could not offset the mobile revenue decline of 18.4% YoY to USD 898.6 million (AED 3.3 billion)

- Fixed revenues declined 28.6% to reach USD 59.9 million (AED 218.9 million)

- Equipment revenues declined ~14% YoY to reach USD 16 million (AED 58.9 million)

However, in local currency terms, revenues grew 19.1% despite heightened inflationary pressures and the end of the national roaming agreement with Telecom Egypt in Dec 2022.

Orange – Egypt

Revenues declined 21.5% YoY to USD 842.9 million (EUR 779 million) in FY-2023. Despite a 3.3% increase in mobile access and an 8.6% increase in fixed access base, Orange could not offset the high inflation in FY-2023.

Ooredoo – Qatar

Revenues declined 8.5% YoY to ~USD 2 billion (QAR 7.3 billion) in FY-2023.

- Mobile segment revenue declined 11% YoY to USD 942.2 million (QAR 3.4 billion)

- Fixed segment revenues declined 6% YoY to USD 883.7 million (QAR 3.2 billion)

- Whole business revenues declined 53% YoY to USD 49.7 million (QAR 181 million)

The revenue was also affected by the discontinuation of low-margin transit businesses, the challenging economic environment and increased competition in the mobile segment. Excluding the impact of the FIFA World Cup and its related revenues of USD 99 million (~QAR 360 million) in FY-2022, revenue growth remained almost flat.

Ooredoo – Palestine

Revenues declined 5.6% YoY to USD 108.8 million (QAR 396.6 million) in FY-2023. This decline was due to a challenging macroeconomic environment: the local currency depreciated 9% against the US dollar (reporting currency). Excluding the negative impact of foreign exchange, revenues increased by 2%.

Partner

Revenue for the Israel based telco declined 3.3% YoY to USD 909.5 million (NIS 3.3 billion) in FY-2023.

- Overall cellular revenue declined 6.4% YoY to ~USD 601 million (NIS 2.2 billion) in FY-2023

- The prepaid subscriber base reduced by 11,000, resulting in declining cellular services revenue.

- Telcos strategically focused on value packages in the postpaid segment and profitability improvement measures in the prepaid segment

- The decline in interconnect charges by 13.1% YoY and cellular equipment by ~1.2% YoY

EBITDA analysis of Middle East telcos: 2023

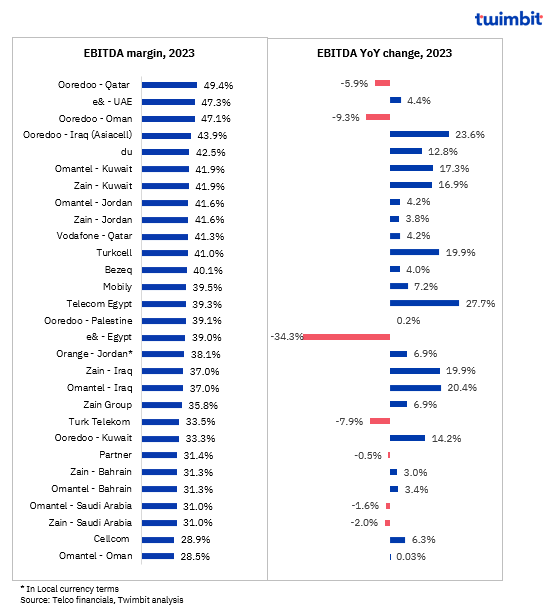

Average EBITDA margin for Middle East telcos stabilised at ~38.7% in FY-2023

In FY-2023, nearly 75% of telcos reported positive EBITDA, with 9 telcos recording double-digit EBITDA growth.

The YoY change in EBITDA rate was relatively higher for Iraq-based telcos owing to the cancellation of sales tax on telecom services starting December-2022.

Exhibit 2: EBITDA and EBITDA margin trends of telcos in the Middle East, 2023

Ooredoo – Qatar

EBITDA declined by 5.9% to USD 988.7 million (QAR 3.6 billion), due to higher comparison base and one-off impacts (FIFA World Cup) resulting in EBITDA margin reaching of 49.4% in FY-2023. Excluding these factors, EBITDA declined 1% YoY in FY-2023.

e& – UAE

EBITDA increased by 4.4% YoY to USD 4.5 billion (AED 16.5 billion), resulting in EBITDA margin of 47.3% in FY-2023. The YoY increase in EBITDA is owing to telcos’ intense focus on profitable revenue growth and continued cost-efficiency measures.

Telecom Egypt

EBITDA grew by 27.7% YoY to ~USD 726.5 million (EGP 22.3 billion) due to strong operational results and savings from the new national roaming agreement. These helped offset rising costs due to inflation. This strategic approach led to notable stability in its EBITDA margin of 39.3% in FY-2023.

Ooredoo – Iraq (Asiacell)

EBITDA grew by 23.6% YoY to ~USD 536 million (QAR 1.9 billion) due to higher revenue growth rates and data revenues, increasing EBITDA margin to 43.9% in FY-2023.

Omantel – Iraq

EBITDA grew by 20.4% YoY to USD 356.2 million (RO 137.1 million) due to higher net profits before interest and tax (EBIT) in FY-2023. Net profits grew by 112.9%, reaching USD 147.6 million (RO 56.8 million).

This resulted in a stable EBITDA margin level of 37% and strong YoY revenue growth of 21.2% in FY-2023.

Zain – Iraq

EBITDA grew by 19.9% YoY to USD 360.7 million (KWD 110.9 million) due to higher net profits before interest and tax (EBIT) in FY-2023. Net profits grew by 101.9%, reaching USD 156.5 million (KWD 48.1 million) in FY-2023.

This growth was supported by a USD 9 million increase from transferring 4,606 towers from TTI to TASC. Robust revenue growth of 20.7% YoY also resulted in a stable EBITDA margin of 37% in FY-2023.

Turkcell

EBITDA grew by 19.9% YoY to USD 1.9 billion (TL 43.9 billion) in FY-2023, primarily driven by Turkcell Türkiye, which reported a 24.1% YoY EBITDA growth to reach USD 1.8 billion (TL 40.7 billion), resulting in EBITDA margin reaching 44.2%.

Relatively lower energy expenses, interconnection expenses, and cost of goods sold as a percentage of revenues, resulted in EBITDA margin grow by 180ps YoY to reach 41.0% in FY-2023.

Omantel – Kuwait

EBITDA grew by 17.3% YoY to USD 485.6 million (RO 186.9 million) in FY-2023 due to higher net profits before interest and tax (EBIT) in FY-2023. EBIT grew by 35.6%, reaching USD 243.7 million (RO 93.9 million).

The telco completed the sale and leaseback of 101 telecom towers in Kuwait for USD 6.4 million (RO 2.4 million) in August 2023. The total gain from this transaction was USD 3.4 million (R0 1.3 million). This resulted in a significant growth in EBITDA margin, with a 410 bps increase from 37.8% in FY-2022 to 41.9% in FY-2023.

e& – Egypt

EBITDA declined by 34.3% YoY to USD 389.1 million (AED 1.4 billion) in FY-2023 due to stringent macroeconomic conditions. These include higher inflation rates and local currency devaluation.

However, in terms of local currency, EBITDA grew ~6% YoY to USD 0.4 billion (EGP 11.9 billion). Regardless, overall EBITDA margins declined from ~44% in FY-2022 to ~39% in FY-2023 due to inflation and loss in roaming revenue.

Turk Telekom

EBITDA declined by 7.9% YoY to USD 1.5 billion (TL 33.5 billion) in FY-2023 due to EBITDA decline in both mobile and fixed line segment. Fixed line EBITDA declined by 27.2% YoY to USD 739.5 million (TL 17.1 billion), Mobile EBITDA increased by ~26% YoY to USD 714.2 million billion (TL 16.5 billion)

Despite the increase in mobile EBITDA, it could not offset the overall decline in fixed-line EBITDA. This resulted in the EBITDA margin declining by 640 bps to 33.5% in FY-2023.

Ooredoo – Oman

EBITDA declined by 5.9% YoY to USD 317.4 million (QAR 1.1 billion) due to lower gross margins, which resulted from the higher cost of sales and operating costs. As a result, EBITDA margin declined by 510 bps to 47.1% in FY-2023.

CAPEX analysis of Middle East telcos: 2023

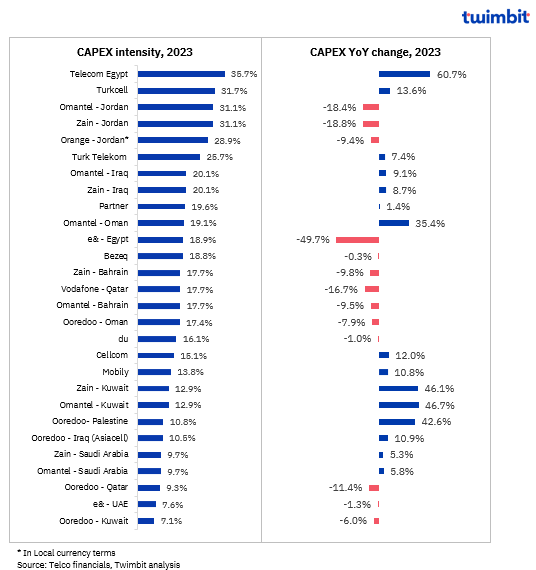

CAPEX spending declined to ~18% of overall revenue for telcos in the Middle East as telcos curtail spending on new deployments and network expansion

One third of the telcos reported a decline in CAPEX spending in FY-2023 as compared to FY-2022. The CAPEX spending is likely to stabilise as telcos near the completion of 4G/5G network deployment.

Exhibit 3: CAPEX and CAPEX intensity trends of telcos in the Middle East, 2023

Telecom Egypt

In-service CAPEX increased by 60.7% YoY to USD 661.3 million (EGP 20.3 billion) in FY-2023, owing to increased procurement and upfront settlement of obligations.

Cash CAPEX (including license fees) reached USD 861.6 million (EGP 26.4 billion). These investments ranged from ~USD 65.3 million (~EGP 2 billion) for NUCA, Hayat Karima and several digitisation projects, which is also financed by the Government.

This increased the CAPEX intensity from 28.5% in FY-2022 to 35.7% in FY-2023.

Omantel – Kuwait

CAPEX increased by 46.7% YoY to reach ~USD 149 million (RO 57.4 million), resulting in a CAPEX intensity growing by 360 bps to reach 12.9% YoY in FY-2023.

Ooredoo – Palestine

CAPEX increased by 42.6% YoY to USD 11.9 million (QAR 42.8 million) in FY-2023. One-off building land CAPEX and ongoing spending in digitalisation initiatives impacted this increase. This increased the CAPEX intensity from 7.1% in FY-2022 to 10.8% in FY-2023.

Omantel – Oman

CAPEX increased by 35.4% YoY to USD 300.8 million (RO 115.8 million) due to the 5G rollout and 4G network expansion. This increased the CAPEX intensity from 15.1% in FY-2022 to 19.1% in FY-2023.

e& – Egypt

CAPEX declined by 49.7% YoY to USD 188.2 million (AED 691 billion) in FY-2023 due to reduced spending on 4G deployment and network capacity expansion. This decreased the CAPEX intensity from 28% in FY-2022 to 18.9% in FY-2023.

Omantel – Jordan

CAPEX declined by 18.4% YoY to USD 161million (RO 62.0 million), decreasing CAPEX intensity from 39.4% in FY-2022 to 31.1% in FY-2023.

Vodafone – Qatar

CAPEX declined by 16.7% YoY to reach USD 150.9 million (QAR 550 million), decreasing CAPEX intensity from 21.5% in FY-2022 to 17.7% in FY-2023. A key reason for the decline might be higher CAPEX spend ~USD 181.1 million (QAR 660 million) in FY-2022, which would have fulfilled most of its immediate infrastructure needs.

Ooredoo – Qatar

CAPEX declined by 11.4% YoY to USD 185.2 million (QAR 674.7 million) in FY-2023 due to higher spending for the FIFA World Cup & completion of data centres in FY-2022. This decreased the CAPEX intensity by 30bps to 9.3% in FY-2023.

Omantel – Bahrain

CAPEX declined by 9.5% YoY to USD 33.5 million (RO 12.9 million), decreasing CAPEX intensity from 21.1% in FY-2022 to 17.7% in FY-2023.

Orange – Jordan

CAPEX declined by 9.4% YoY to USD 146.8 million (JD 104.1 million) in FY-2023 due to network stabilisation post the 5G launch in July 2023. This decreased CAPEX intensity from 33.1% in FY-2022 to 28.9% in FY-2023.

ARPU analysis of Middle East telcos: 2023

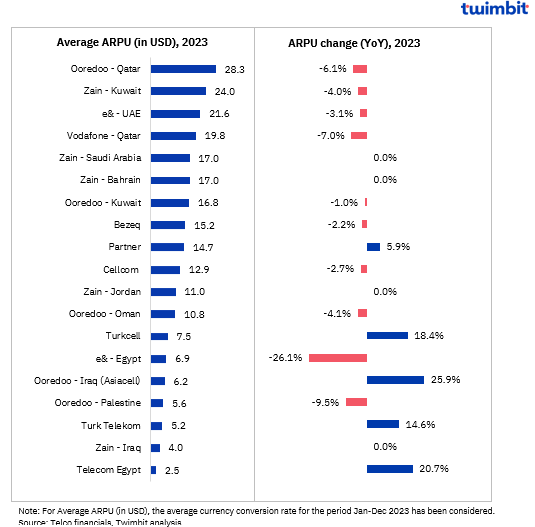

Competitive intensity and a challenging macroeconomic environment stalls ARPU growth rate despite data & subscriber growth

The ARPU analysis for the telcos is as follows:

- Nearly 74% of the telcos in Middle East reported stagnant or decline in ARPU growth rates in FY-2023 than in FY-2022

- Additionally, ~38% of the 19 telcos such as Cellcom, Bezeq, Zain – Jordan, Ooredoo – Kuwait, Zain – Bahrain etc, reported stable ARPU levels in FY-2023, with YoY changes ranging from -3% to 3%.Exhibit 4: ARPU trends of telcos in the Middle East, 2023

Exhibit 4: ARPU trends of telcos in the Middle East, 2023

Ooredoo – Iraq (Asiacell)

ARPU increased by 25.7% YoY to reach USD 6.2 (QAR 22.5) in FY-2023, driven by the increase in data consumption and an expanded digital portfolio, which includes:

- Check Your Offer

- Free social media data

- Sales contests across many channels

Telecom Egypt

ARPU increased by 20.7% YoY to reach USD 2.5 (EGP 75.4) in FY-2023, driven by growth in mobile data and USD subscribers.

- Mobile data traffic subscribers increased by 11% YoY (76.7 million) and USB subscribers by 2.1% YoY (2.5 million).

Turkcell

ARPU increased by 18.4% YoY to reach USD 7.5 (TL 174) in FY-2023, driven by increased smartphone penetration of 250 bps to 90%.

- Average data consumption per user increased 10.8% YoY to 17.4GB in Q4-2023

- Users without 4.5G reported a data consumption increase of 5% to 6.3GB

- Users with 4.5G reported a data consumption increase of 9.5% to 18.5GB

Turk Telekom

ARPU increased by 14.6% YoY to reach USD 5.2 (TL 118.8) in FY-2023, driven by ARPU growth in prepaid and postpaid segments.

- Prepaid ARPU increased by 25.5% to ~USD 4 (TL 92.1)

- Postpaid ARPU increased by 9.5% to USD 5.6 (TL 128.5)

Partner

ARPU for the Israel based telco increased by 5.9% YoY in FY-2023 to reach USD 14.7 (NIS 54). This was driven by a change in the counting method, resulting in the removal of M2M subscribers (SIM cards designated for use in machines) in Q4-2022.

- 189,000 subscribers were removed from the postpaid cellular subscriber list

- 94,000 subscribers were removed from the prepaid cellular subscriber list

e& – Egypt

ARPU declined by 26.1% YoY to USD 6.9 (AED 25.4) in FY-2023. Despite the growth in mobile subscribers by 12.7% to reach 33.9 million, revenues declined by 18.2% during the same period.

Ooredoo – Palestine

ARPU declined by 9.5% YoY to USD 5.6 (QAR 20.3) in FY-2023 due to the challenging macroeconomic environment.

Vodafone – Qatar

ARPU declined by ~7% YoY to USD 19.8 (QAR 72.0) in FY-2023, owing to decline in revenue from both prepaid and postpaid segment.

Ooredoo – Qatar

ARPU declined by 6.1% YoY to USD 28.3 (QAR 103.2) in FY-2023, due to decline in both prepaid and postpaid ARPU

- Prepaid ARPU declined by ~15% YoY to USD 9.2 (QAR 33.7) in FY-2023

- Postpaid ARPU declined by ~6.6% YoY to USD 71.8 (QAR 261.7) in FY-2023

Ooredoo – Oman

ARPU declined by 4.1% YoY to USD 10.8 (QAR 39.5) in FY-2023

- Prepaid ARPU declined by 9.1% to USD 5.8 (QAR 21) in FY-2023

- Postpaid ARPU declined by 4.6% to USD 25.6 (QAR 93.1) in FY-2023

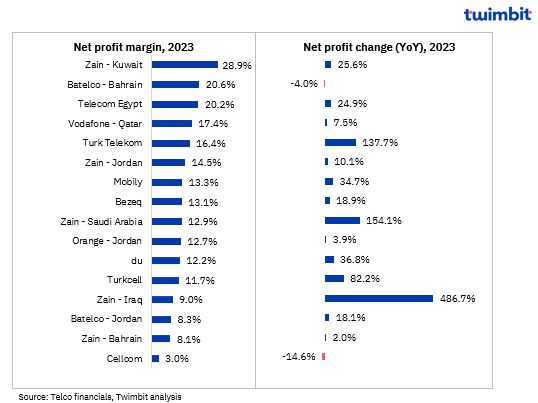

Profitability analysis of Middle East telcos: 2023

Profitability increases for telcos in Middle East, on account of revenue growth and cost containment measures

~88% of the 16 telcos reported net profit growth, excluding Batelco – Bahrain and Israel’s Cellcom. Favorable market conditions also impacted an increase in positive revenue growth rate. These include:

- Local currency appreciation against USD (Iraq)

- Gain from sales of assets (Saudi Arabia)

- Government support in the cancellation of taxes (Iraq), which facilitated net profit growth

Exhibit 5: Net profit trends for telcos in the Middle East, 2023

Zain – Iraq

Net profit surged exponentially to reach USD 88 million in FY-2023, driven by:

- Favourable market dynamics, such as the 20% sales tax cancellation fee on telecom services starting December 2022

- Appreciation of the Iraqi Dinar against USD

The net profit margin grew from 1.9% in FY-2022 to ~9% in FY-2023.

Zain – Saudi Arabia

Net profit grew by 154.1% YoY to reach USD 338 million in FY-2023, driven by:

- Substantial gains from the sale and leaseback of towers for operations

- Fintech entity (Tamam) reported 112% growth in net profitability

The net profit margin grew from 5.5% in FY-2022 to 12.9% in FY-2023.

Turk Telekom

Net profit grew by 137.7% YoY to reach USD 712.1 million (TL 16.4 billion) in FY-2023, driven by:

- Inflation on sizable, deferred tax income, resulting from the indirect impact of applying inflation accounting on statutory accounts for the first time

The net profit margin grew by 880 bps to 16.4% in FY-2023.

Turkcell

Net profits grew by 82.2% YoY to reach USD 543.5 million (TL 12.5 billion), driven by:

- Strong performance at the revenue and EBITDA levels

- Positive impact of deferred income tax expense

The net profit margin grew from 7.4% in FY-2022 to 11.7% in FY-2023.

Cellcom

Net profits declined by 14.7% YoY to USD 36.4 million (NIS 134 million) primarily due to ~7% YoY increase in selling and marketing expenses, which reached USD 188.9 million (NIS 695 million).

The net profit margin declined by 70 bps to 3% in FY-2023.

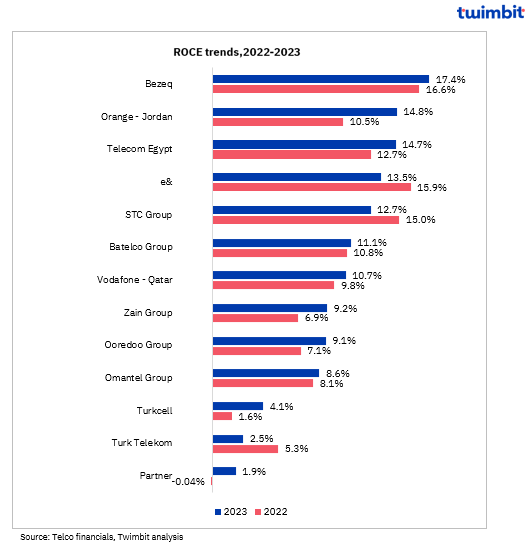

Return on capital employed (ROCE) analysis of Middle East telcos: 2023

ROCE improves for the majority of telcos in Middle East in FY-2023, indicating better capital utilisation

ROCE increased for ~77% of the telcos (including group conglomerates) in FY-2023

- Growth in revenue alongwith increased profitability (due to a reduction in expenses) resulted in positive ROCE growth for the majority of the telcos

Exhibit 6: ROCE trends for telcos in the Middle East, 2022-2023

Bezeq

ROCE increased by ~90 bps to 17.4% in FY-2023, the highest among the Middle East telcos analysed. This is driven by the higher profits and improved business results in most of Bezeq’s activities.

Orange – Jordan

ROCE increased by 430 bps to 14.8% in FY-2023, driven by a decrease in total capital employed by ~10%.

Turkcell

ROCE increased 250 bps to 4.1% in FY-2023, driven by:

- Higher revenues earned in FY-2023

- Margin decline in cost incurred resulted in higher Earnings Before Interest and Tax (EBIT)

Zain

ROCE increased 230 bps to 9.2% in FY-2023, driven by:

- Gain on sale of telecom towers

- Higher contributions from interest and investment income, resulting in higher Earnings Before Interest and Tax (EBIT)

Turk Telekom

ROCE declined 280bps YoY to 2.5% in FY-2023, driven by relatively higher costs incurred owing to increased:

- Cost of sales

- General administrative expenses

- Marketing, sales and distribution expenses

- Finance costs

Key suggestions and recommendations

A rising tech-adept population and positive economic indicators signal a pivotal shift in the telecommunications landscape in the Middle East. The region presents several strategic opportunities for telcos.

1. AI adoption is high on the board room agenda, offering opportunities for operational efficiency in the near term

As part of their digital transformation initiatives, telcos in the Middle East strategically integrate Artificial Intelligence (AI) to enhance operational efficiency and boost profitability.

- STC – Bahrain embraces AI to improve network processes and enhance its customer experience.

- Adopted Nokia’s Self-Organizing Network (SON) software with an AI-powered Energy Savings Management module

- Launched a mobile SIM activation service in March 2024 which uses AI-powered facial recognition technology

- Mobily leverages AI to manage the rise in connected devices linked to Saudi Arabia’s ‘Vision 2030’ program.

- Deployed Ericsson’s AI-based network solution to proactively manage network challenges and enable predictive and automated network management

- e& introduced ‘EASE’, the world’s first autonomous telecom store experience powered by AI.

- Leverages AI, machine learning, facial recognition, robotics, and smart technology to enable seamless product and service purchases

Telcos can utilise AI to improve sales and marketing, customer service, network operations, information technology, and support services.

2. Strategically target the Enterprise (B2B) segment with “Beyond Connectivity” offerings as an alternate revenue stream

Repositioning as one-stop shops, telcos cater to the full spectrum of their customers’ digital service requirements. This approach enables telcos to offer enhanced customer satisfaction, unlock new revenue streams and solidify their position in the evolving digital landscape as “Digital Service Providers”.

- e&’s recent success in its enterprise division is underscored by its diversified digital service offerings.

- Achieved a 32% YoY revenue growth to reach USD 720 million (AED 2.7 billion)

- Growth was driven by strong annual performance in key areas like digital infrastructure (32%), Help AG (36%), IoT (56%) and engage (56%).

- Mobily leverages strategic partnerships with government clients to launch AI-powered cybersecurity solutions and enhance overall customer connectivity.

- Yielded a notable B2B revenue increase of ~21% YoY to USD 963.1 million (SAR 3.6 billion)

- Du partnered with Microsoft in October 2023 to combine its network capabilities with Microsoft Azure’s cloud computing power.

- Aims to fuel business innovation, drive digital transformation, and deliver cutting-edge solutions in AI, sustainability, and cybersecurity

“Beyond Connectivity” offerings can also encompass key areas like cloud solutions, cybersecurity offerings, data analytics, AI, and other cutting-edge technologies. By fostering a digital offering ecosystem, telcos can cater to the growing demand for integrated solutions.

3. Selective acquisitions and strategic partnerships by telcos enhance their revenue mix

This strategic shift allows telcos to both monetise their existing infrastructure investments and cater to the evolving needs of their customers

- STC Group partnered with Hyundai E&C and KT Corp in November 2023 to leverage their combined expertise in smart city development.

- Focuses on constructing data centers and establishing IT infrastructure for a smart city in Saudi Arabia

- Aligns with Saudi Arabia’s ‘Vision 2030’ program to emphasise smart infrastructure and digital transformation

- Zain spearheaded the establishment of the Sustainability Innovation Hub in December 2023 in collaboration with GCC Telco Alliance members.

- Key collaborations would enable Zain to address climate change issues and expand access towards affordable and reliable energy

- e& acquired a majority stake in Careem Technologies (Careem Everything App) in December 2023 to strengthen its ambition of becoming a global technology group.

- Diversified its existing consumer digital offerings, signifying a broader telco shift beyond traditional connectivity services

By strategically integrating new technologies and forging partnerships, telcos can unlock new revenue streams and solidify their positions in the evolving digital landscape.

4. Aligning business focus on emerging adjacent products and applications

The established infrastructure and multi-product service portfolio of Middle East telcos incentivises a deeper exploration into the burgeoning metaverse landscape.

- Augmented reality (AR)/ Virtual reality (VR) adoption bears strong potential

- UAE stands out as the one of the most advanced market in region and is actively promoting the integration of advanced technologies across industries to enhance efficiency

- AR/VR contribution to UAE’s economy is projected to be ~USD 4.1 billion by 2030

- Metaverse presents a more substantial opportunity for telcos to expand beyond individual technologies.

- The potential annual contribution of the metaverse to the economies of the Gulf Cooperation Council (GCC) is estimated to reach USD 15 billion by 2030

- Saudi Arabia and the UAE poised to capture significant shares of ~USD 7 billion and ~USD 3.3 billion, respectively

While the AR/VR potential is undeniable, hurdles exist regarding widespread adoption. Hence, it is necessary to ensure continuous investments such as enhancing resolution, expanding field of view, and minimising latency for a more immersive user experience.

5. Monetise 5G infrastructure with innovative service offerings

The deployment of 5G technology continues to signify promising future opportunities for telecom service providers to leverage this transformative technology. Countries such as the United Arab Emirates (UAE), Bahrain, and Saudi Arabia have swiftly launched 5G networks and introduced competitive mobile packages to consumers, incentivising them to upgrade to 5G device.

- Pelephone leads Israel’s 5G revolution, boasting over 1.1 million 5G users (45% of its total subscriber base).

- Retail internet ARPU has increased by 16% over 2021-2023 to reach USD 33.4 (NIS 123)

- Cellular ARPU (Pelephone) has grown from ~USD 10.9 (NIS 40) in FY-2021 to ~USD 12 (NIS 44) in FY-2023

- Zain – Kuwait seeks to enhance user experiences through network improvements and 5G technologies.

- Successfully launched a trial run of the 5GNC (5G New Calling) technology in December 2023

- Achieved speeds of 10 Gbps through a 5.5G trial run, which occurred in November 2023

- STC – Kuwait successfully piloted 5GNC technology in November 2023, offering an enriching calling experience between customers.

- Enhances existing calling features with interactive HD video communication to further expand the value proposition of its 5G services

The robust GCC economy, digitalisation programs and the surge in smart city projects also create significant demand for 5G capabilities. From network slicing to API exposure, these capabilities are key for telcos to move forward and unlock new revenue streams. Industry sources project a promising future for 5G subscriptions in the region, with annual growth anticipated at 19% over the forecast period. By 2029, over 90% of all subscriptions are expected to be 5G, reflecting the rapid pace of adoption in the Middle East.

6. Telcos prioritise cybersecurity implementations to address vulnerabilities arising from rapid 5G rollout

The rapid rollout of 5G creates a complex security landscape due to its interconnected nature and increased reliance on virtualisation. Owing to the above complexities, telcos are faced with multiple challenges including insecure integrations, virtualisation risks and DDoS.

As per IBM’s Cost of a Data Breach Report 2023, the average total cost of data breach in the Middle East increased 8.2% YoY from USD 7.46 million in 2022 to USD 8.07 million in 2023. Telcos in the region were targeted by malware family named as “HTTPSnoop” in 2023.

- Zain: ZAINTECH established ICT hub in Dubai Internet City in December-2023 and would host Network Operation Centre (NOC), Security Operating Centre (SOC) and an Experience Centre

- e&: Collaborated with UAE Cybersecurity Council to launch Mobile Security Operation Centre (MSOC) in March-2023, to provide business customers with real-time protection services to safeguard mobile phones from malicious attacks

Telecommunications companies typically control a vast number of critical infrastructure assets, making them high-priority targets for adversaries looking to cause significant impact. Hence, telcos must focus on adopting stronger encryption tools, prioritising application layer security to prevent data breaches and containerisation of VMs to isolate threats compromising physical network resources.

Research Methodology and Assumptions

- “Middle East telcos performance benchmarks – Winter 2024” report provides key findings regarding performance of telcos for key financial metrics including Revenue, EBITDA, CAPEX, ARPU, Net Profit and ROCE for the period January-December 2023.

- This report leverages data acquired from telecommunications companies and extensive secondary research. Twimbit adopted a calendar year approach for data analysis, where FY signifies the January-December period.

- To ensure consistency and facilitate accurate comparisons, a constant currency conversion rate has been applied throughout the report. This rate represents the average USD exchange rate for the entire calendar year 2023 (January-December 2023).

- The report presents a comprehensive assessment of Revenue and EBITDA for 34 and 28 telecommunication companies, respectively. Additionally, CAPEX and ARPU analyses encompass data from 28 and 19 telcos, respectively. Net profitability and ROCE analysis is based on 16 and 13 telcos respectively.

- Blended mobile ARPU has been incorporated wherever relevant for a more holistic view.

- ROCE has been calculated at overall Group level for select telcos, owing to non-availability of the data at country level for the respective telcos. Formula for calculating Return on Capital Employed (ROCE)=EBIT / Total Assets – Total Current Liabilities)