Why is customer-centricity imperative for a neobank’s success?

The Amazon Effect dramatically changed the way we shopped since 1994 – it introduced us to an almost frictionless shopping process with near-immediate results. In addition, Amazon has played an influential role in raising customer expectations.

The customers of today expect similar disruptions within the banking and services industry, transcending banks to build customer-centric solutions rather than the standard traditional product approach.

As neobanks operate as platform companies, their DNA are far more compatible with today’s fast-paced customer mindset than their incumbents. Customers relish the seamless journey they have with neobanks that have mastered the art of delivering integrated, frictionless customer experiences (CX).

In this report, the twimbit analyst team helps Chief Executive Officers (CEO), Chief Product Officers (CPO) and business unit leaders of existing and upcoming neobanks understand the importance of building a neobank on the principles of customer-centricity. Our team also outlines the best practices from the top 10 neobanks in APAC who ace customer-centricity and become the bank of choice for their customers.

Figure 1: With over a billion dollars in funding in 2020, there is a significant growth opportunity for neobanks

Methodology

Step 1: We analysed 58 retail neobanks across 13 countries in APAC.

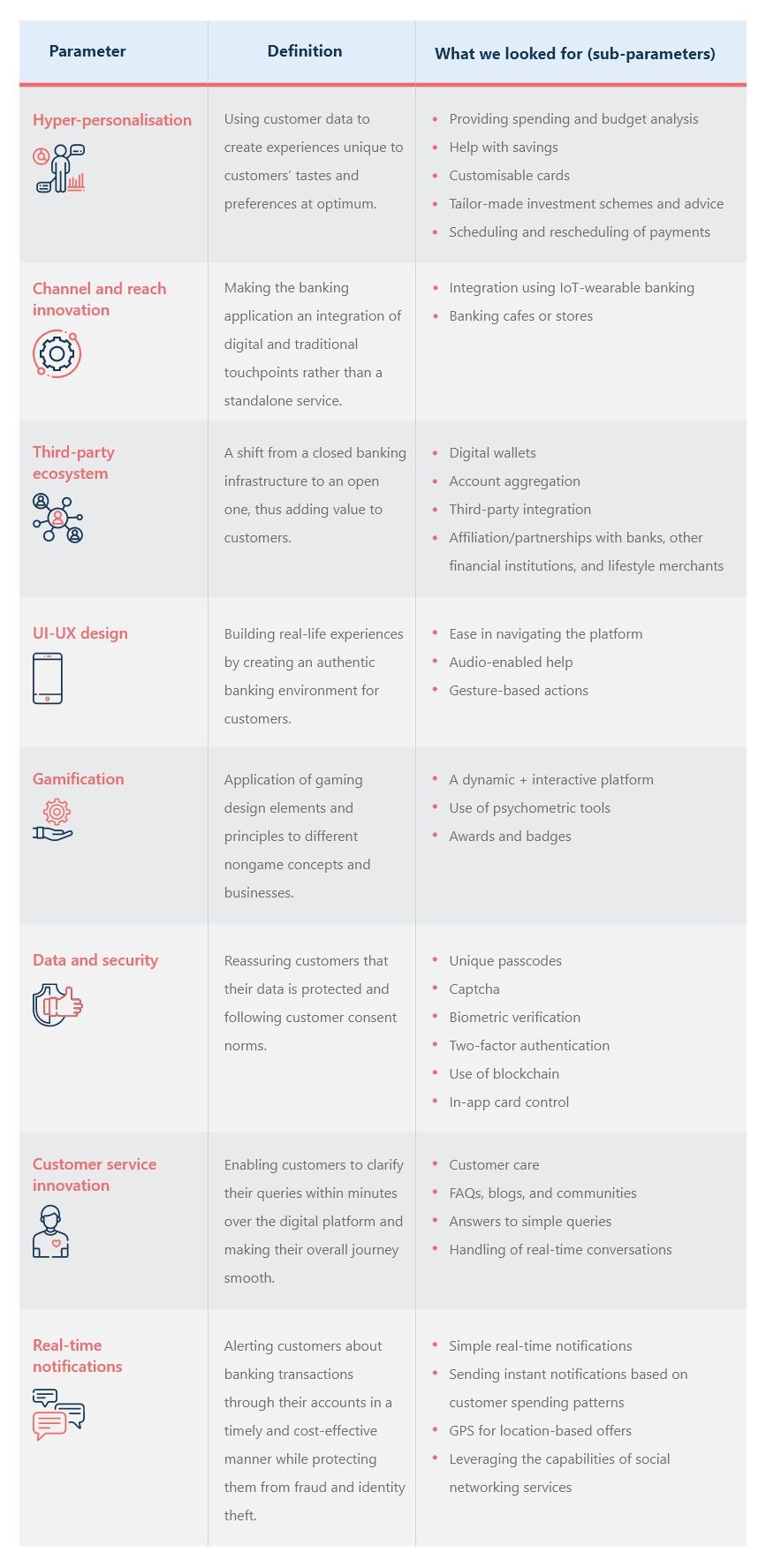

Step 2: We developed an eight-point framework to help set the customer-experience standard for neobanks across APAC. At the same time, we developed informed perspectives through company annual reports, company websites, and published anecdotes.

Step 3: We evaluated our neobanks across 8 parameters and 31 sub-parameters (Table 1) on a scale of 1 to 10, measuring their responsiveness to increasing customer expectations.

Table 1: twimbit’s customer-experience framework

Step 4: Based on their relevance, we used the weighted average method to assign each pillar a weightage for the overall analysis.

In addition to this, sub-attributes have pre-defined scaling for better distinction between a neobank’s services.

Step 5: Based on our analysis of 58 neobanks on our customer-centricity framework, we finalised the top 10 retail neobanks that ace customer experience in Asia-Pacific. (Table 2).

Table 2: twimbit’s top 10 neobanks to ace customer experience

Research caveat: Limited to secondary sources and publicly declared information by the companies.

Debunking customer experience benchmarks

#1 Hyper personalisation

- Personalised tips for budgeting and saving

- RoboAdvisory

- Offering a suite of unique products and services, such as personalised credit card recommendations and loan and insurance offers

- Customised Dashboards

- Customisable cards

#2 Channel and reach innovation

- Integration with Apple Watch and Siri

- Offline bank stores

#3 Thirdparty ecosystem

- Robust open banking system supporting TPPs

- Personalised cashback

- Browser extension for cashback and discounts

#4 UI-UX Design

- Voice-based assistance

- Gesture-based actions

- Multilingual app support

- Animations and videos: a dynamic and interactive website

#5 Gamification

- 2-player banking

- Gamification with predictive analysis

- Gamification to help with savings

#6 Data and security

- Unicard

- Single-use virtual cards

- Location based security

#7 Customer service innovation

- Using social media platforms to send notifications

- Virtual assistants and chatbots

- Active blog and community

#8 Real-time notifications

- Real-time expenditure warnings

- Instant notifications

- Elements of Augmented Reality

Our recommendations

We believe that these four growth opportunities will define the way neobanks incorporate a customer-centric approach to neo banking and significantly improve customer experience:

- Invisible banking

- Create an ecosystem

- Data and security

- Channel and reach innovation

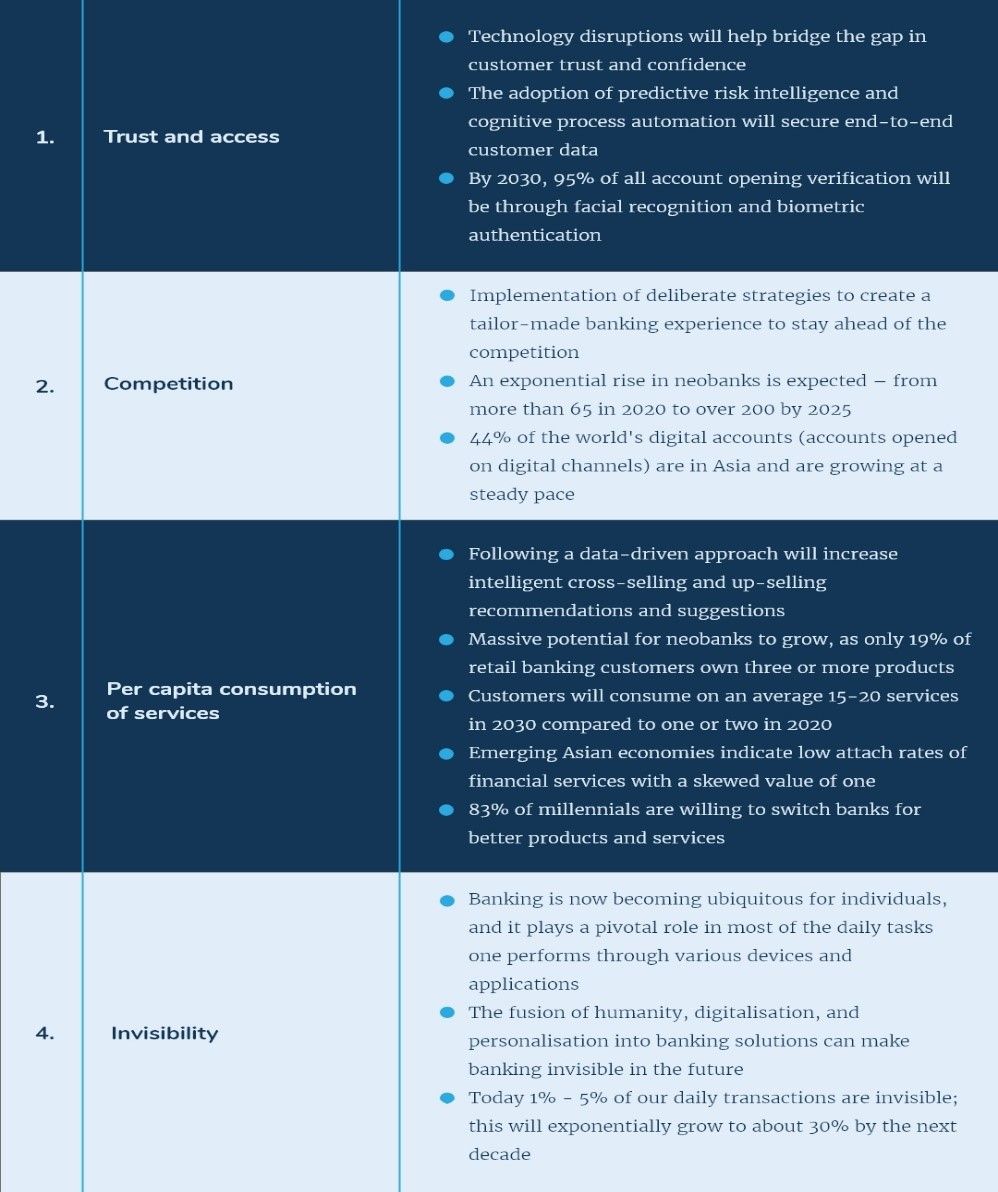

#1 Invisible banking

Invisible banking allows the integration of banking products and services with day-to-day digital customer touchpoints. The main idea is to make the customer journey as smooth as possible. For example, a customer can tap to make a payment or tell you they are saving to buy a new car in 5 years, and you can automatically move money from their checking account to a vault labelled “car” at appropriate intervals.

Banking that is invisible is about being behind the scenes and embedding your neobank into the customer’s daily life. At present, 1% – 5% of our daily transactions are invisible. This figure will grow exponentially to about 30% in the next decade.

How can you incorporate invisible banking into your customer experience?

Targeted value proposition:

As a by-product of advancements in other industries,people now expect banks to deliver more and more hyper-personalised products and services. Investing in tools that can enable this will help your bank engage with your customers better. You will then be able to deliver the right products at the right time.

Gamification:

Gamification is the application of gaming design elements and principles to different nongame concepts and businesses. The banking industry has advanced a lot compared to the early 2010s, which awarded users with badges and stickers to now, where we see the gamification of money management tools and interactivity. Gamification is essentially about customer centricity: you help your customers set and achieve their financial goals in an exciting and fun way. Game techniques make banking more interactive and appealing.

Chatbots, virtual assistance and voice banking

You no longer have to be held up in phone queues or read through long pages of FAQs; chatbots and virtual assistances are drastically changing the way neobanks interact with customers. Virtual assistance in banking brings convenience, speed, reduced friction, and powered accessibility to customers. The fascinating thing about it is perhaps the ubiquity and ease that it brings. Banking assistants can be available 24×7 and across multiple channels such as WhatsApp, Facebook Messenger, and emails.

Investments in virtual assistance will be a top customer-centric priority for the next five years. Essentially, as we move forward, advancements in technology will enable bots to do everything, from answering account-related queries to giving personalised advice to customers. However, to maintain a personal touch, neobanks should integrate AI-ML algorithms and text-to-speech techniques with sentimental analysis such as Natural Language Processing (NLP) and Named Entity Recognition (NER).

In addition to this, you can introduce voice-enabled virtual assistance that can carry out repetitive tasks such as money transfers and payments, password resets, and alerts and reminders to customers for bills and payments.

We believe that neobanks of the future should also forge strategic partnerships with leading social media and internet giants to strengthen their chatbot capabilities. These partnerships will subsequently boost customer engagement and loyalty.

Enhanced User Interface-User Experience

The shift has begun for banking UIs from using fewer graphic tools to building real-life experiences. Under this enhancement, three main trends are noticeable:

- Virtual Reality (VR)

- Augmented Reality (AR)

- Holographic technology

These three tools can help you create an authentic and real-life banking environment for your customers.

The banking industry is still at a nascent stage for adopting these next-generation technologies. However, we do believe that they have tremendous potential to change the banking experience for users completely.

The importance of UX comes from the fact that it determines the viewpoint of the customer on the bank’s actual workability. It is about making an impression on the user in one go. At the same time, the bank has to make sure that it provides the user with a seamless and intuitive banking experience. The primary purpose of an enhanced user interface, after all, is to eliminate friction and improve on the customer’s digital journey.

Few ways in which the introduction of these tools can change the user experience completely include:

Table 3: Incorporating invisible banking into your customer experience

| Feature | Innovative ideas |

| Targeted value proposition | 1. AI robo-advisors 2. Omni-channel interaction 3. On-demand customer service 4. Recommendation engines 5. Customisable cards |

| Gamification | 1. Virtual currencies 2. Introduce mascots and guides 3. Referral programs, contests, and rewards 4. Use of Augmented Reality 5. Use of psychometric tools to analyse customer thought process and behaviour |

| Chatbots, virtual assistance and voice banking | 1. Integrate AI-ML technologies with sentimental analysis such as NLP and NER 2. Forge strategic partnerships with leading social media and internet giants 3. Voice-enabled virtual assistance 4. Give insights and suggestions to improve financial health |

| Enhance UI-UX | For UI, 1. Introduce visuals and animations 2. Introduce Virtual and Augmented Reality 3. Incorporating wearable banking For UX, 1. Auditory tools for GPS tracking near ATMs and shops 2. Offering customers personalised spending-based and location-based offers 3. Using VR and AR tools to assist differently abled and blind customers to a seamless experience from the comfort of their homes. |

#2 Create an ecosystem

The advancements in technology have taken user experience to a whole new level. For banking, one of the biggest challenges is creating and developing a banking ecosystem that organically presents numerous products and services in a flow. In fact, we believe that the future goal should be enabling banks to act as platforms instead of service providers. The idea is to embed multiple add-ons to the banking platform to serve the needs of the customer.

Open banking has enabled neobanks to gain customer data and availed a wide range of opportunities to provide additional services and products, resulting in added value to the customer. The most striking of all the newly emerged software is the Application Programming Interface (API) which developers use to get third-party data and services into their applications. The main goal is to improve customer satisfaction and engagement. When customers engage with the neobank in innovative ways- be it in the form of an embedded tax filing platform or choosing which loans to buy and doing a comparative analysis- it increases brand loyalty and customer retention.

We believe running an active blog that is engaging and consistent will be a key differentiator in the coming time. Digital content needs to be more than functional; it must make people act. Without this, neobanks jeopardise opportunities that could drive engagement and, in turn, increase their customer base.

Building communities is essential for any neobank looking to build new relationships with potential customers and nurture existing ones. For starters, today’s customers use social media to research a product they want to buy — they check out recommendations, reviews, and so on. Therefore, it is vital to leverage these capabilities of networks and drive target engagement. But, most importantly, this initial engagement needs to be followed up by seamless onboarding and customer consultations that remain personalised.

Table 4: Key innovations for creating an ecosystem

| Account aggregation |

| TPPs and marketplace integration |

| Integration of IoT and wearable banking |

| Creating quality content and engaging customers |

| Building communities and an omni-channel presence |

#3 Data and security

Predominantly, we see neobanks face significant challenges such as digital identity theft, transaction theft, malware contamination, and data ownership.

The increased integration of systems in the financial services sector has created malware propagation prospects. Cross-platform malware contamination is when the malware or viruses infect and propagate from one platform to another without any notice.

Partnerships between fintechs and various software providers are on the rise. This increase comes with a motive– for neobanks to gain a competitive advantage and provide exceptional customer experience. The most critical thing to seek in such partnerships is seamless data sharing, where confidential data move in and out of systems. Data ownership poses a big problem. Neobanks must find a way to seek out customer consent for data sharing while also ensuring that the data is not misused nor exploited in the grey market.

What can you do as a neobank to build trust?

As the banking environment continues to evolve and explore move computing power avenues for its users via mobile apps, there is an urgency to revisit, remodel and revise traditional security models. For any user, security is a crucial part of the applications they use, and the onus falls on the providers to come through. We believe that as neobanks move ahead, data security and privacy will play a pivoting role in winning their customer’s trust and loyalty.

To build trust with your customers, you can:

- Organise awareness campaigns

- Take on a proactive approach

- Expand the deployment of technologies that have greater security protocols, such as machine learning and AI

- Partner with fraud prevention solutions

- Find the right balance between capabilities and security

The authentication model

- Biometric authentication framework

- Biometric cards

- Mobile Know Your Customer (mKYC)

- Adaptive authentications

- Pick-and-choose authentications

Table 5: Key innovations for data and security

| New KYC solutions Biometric authentication | – With in-app fingerprint authorisation – Face ID feature – Eye-scanning technologies The future is to move towards a single authentication hub that supports multi-factor and multi-modal authentication |

| Augmented identity solutions | – Biometric cards – Adaptive authentication |

| RegTech | – Regulatory technology to improve reporting, compliance, and regulatory tracking |

| Intelligent payment fraud detection | – Using algorithms for real-time abnormal behaviour/rogue trading/market abuse detection in multiple accounts |

| Blockchain | Internal banking technologies supported by immutable ledgers that can be applicable for: – Innovations in transaction banking – Peer-to-peer (P2P) lending – KYC solutions Blockchain directly affects the efficiency of banks too by potentially saving costs on compliance, business operations and many more Most importantly, blockchain comes with the highest degree of transparency in financial transactions |

#4 Channel and reach innovation

The era of hyperconnectivity is here. Customers are increasingly oscillating between apps, devices, and platforms. As a result, banking no longer applies to just physical branches, mobile devices, and desktops. Instead, customers may want to identify and use a less distractive way of conducting transactions through solutions like smartwatches, gesture-based actions, and virtual reality devices. Wearable banking brings ultra-convivence to customers, especially for:

- Conducting payments through Near field communication (NFC) technology enabled point-of-sale devices

- Receiving real-time notifications

- Making immediate and urgent inquiries and transactions

- Finding nearby ATMs or branches through geo-location tracking capabilities

Another major shift is visible in the perception of a bank branch that goes beyond a traditional structure to a casual hangout destination, fulfilling your financial needs. Banking is moving towards making the customer self-reliant with interactive kiosks, fully automated walk-in bank cafés, and humanoid driven branches.

Hence, it becomes imperative for neobanks to invest in multi-channel customer support that enables customers to interact with their neobank across various modalities.