Neobanks are now orchestrators for new propositions that revolve around customer-centricity and address unmet consumer needs in the latest market segments. The reason for neobanks winning in the market is the undying focus it has on solving customers’ pain points with tailored products. The absence of physical branches and a monolithic business model allows neobanks to operate with low-cost structures, empowered with disruptive technology stacks to scale banking solutions per the need of the customers.

The Asia Pacific neo banking market generated revenues exceeding USD 6.25 billion in 2020 by delivering frictionless experiences and customised solutions to their target market segments: millennials, rural localities, and SMEs. The strategic orientation of being customer-centric has led to a major growth spurt of a 250% increase in the number of neobanks in the Asia Pacific from 2015 to 2021. In order to sustain future success, neobanks must continuously aim for simple, unique, and flexible product propositions that invigorate customers to increase their product consumption.

Currently, customers consume one to two services, but in the next 10 years, the per capita consumption of services has an inclination to increase by 15 to 20 services. This potential rise creates a huge opportunity for neobanks to become orchestrators for ecosystems, marketplaces, and proprietary solutions to win in the future.

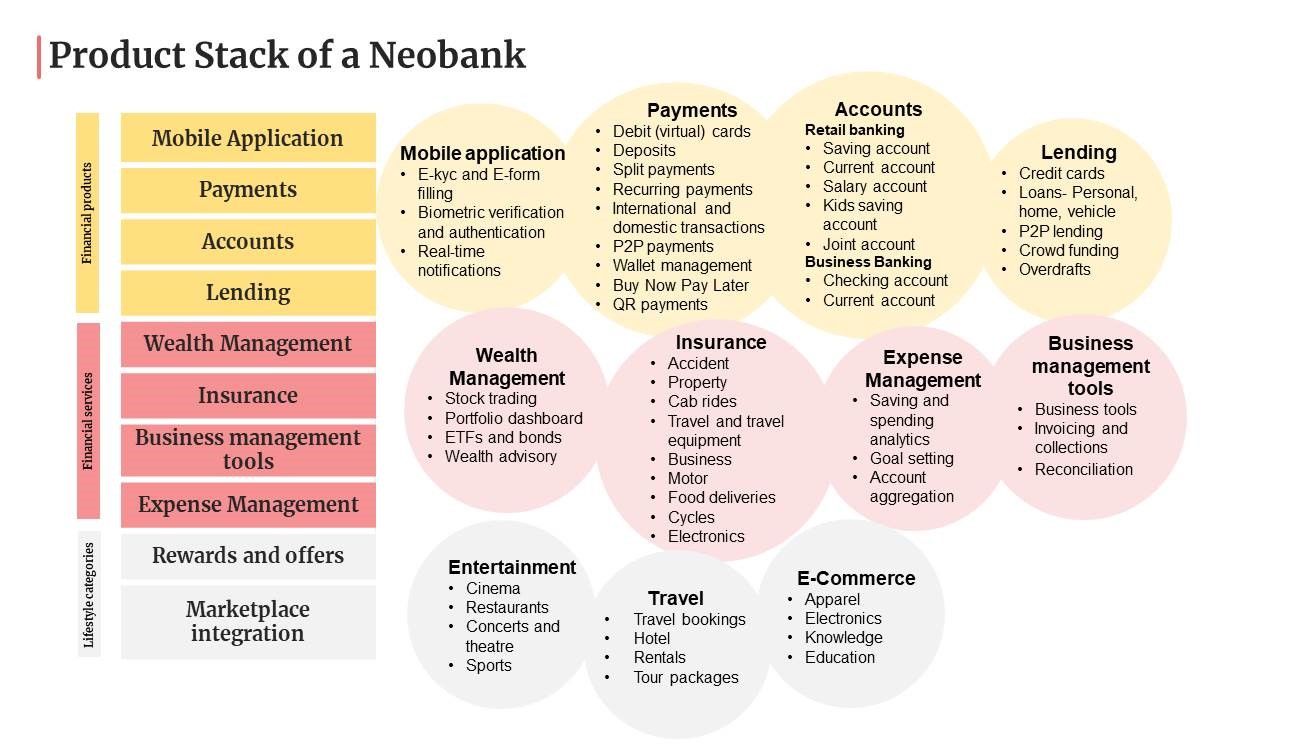

The Twimbit analyst team did a deep dive into the service offerings of the 62 Asia Pacific neobanks to understand the unique propositions. The service offerings, viz, the product stack of the neobanks is broadly classified in three buckets: Financial products, financial services, and lifestyle categories (see figure 1).

Figure 1: A comprehensive product stack to support the end-to-end customer journey

A deep dive of 10 product/service categories prevalent in neobanks

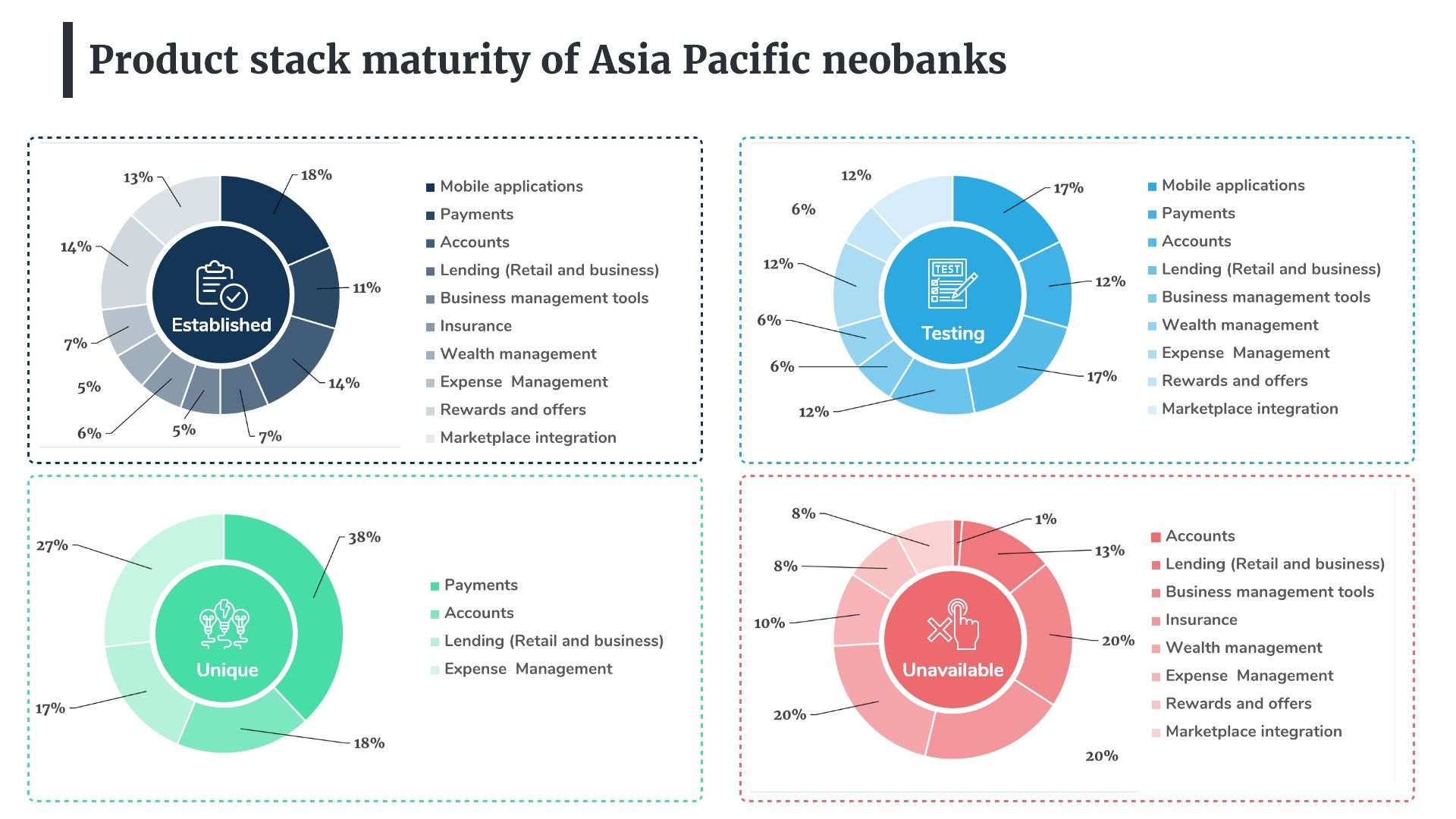

Ten sub-categories organise the innovative services in figure 1 (55 of them in total) for ease of analysis and understanding. One of the four stages of development classifies the current development state of the said services.

- Unavailable: Does not have the product/service type in its stack

- Testing: The product is currently in the pilot-testing phase and is not live to all customers

- Established: The product is a part of the neobank’s stack and is available to all customers for use

- Unique: A unique offering within the product type that is exclusive to all customers of the neobank

Based on the analysis, the analyst team benchmarked the 10 product/services categories across the four development stages to assess the product stack maturity of the 62 neobanks in the Asia Pacific

Figure 2: Product stack maturity of Asia Pacific neobanks

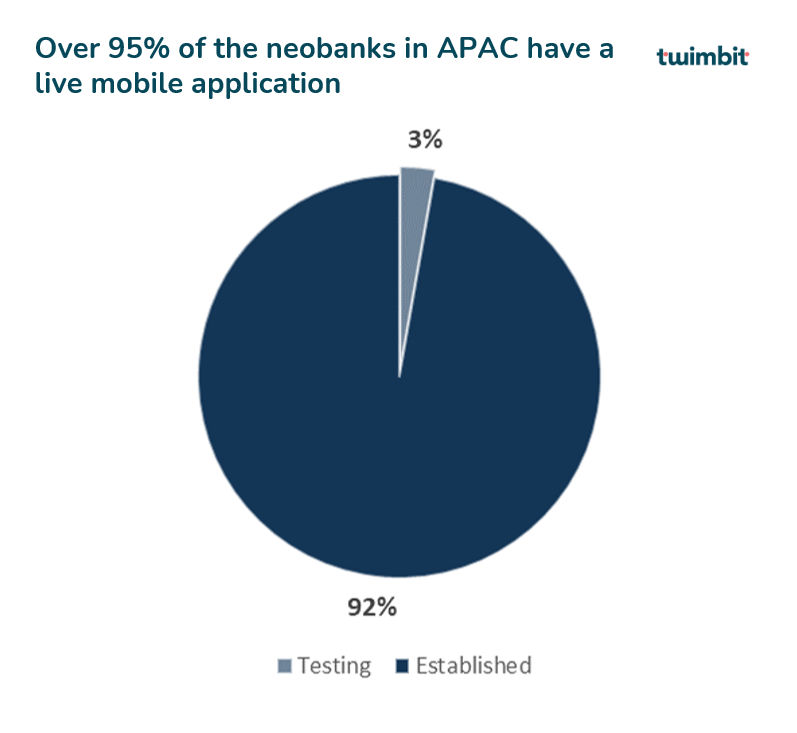

Mobile application:

A mobile application is the key to a neobank’s success, as it operates in a completely virtual environment. Hence, customer acquisition and retention are highly dependent on their appreciation of the banking application that enables banking to be ubiquitous, efficient, and flexible to deliver unique experiences. 95.59% of the neobanks in the Asia Pacific have an established mobile banking application (Figure 3). Meanwhile, 1.5% of the newly formed neobanks do not have a live application as they are in the testing phase. The newly formed neobanks are Fi, India; Robocash, The Philippines; and Parpera, Australia.

Disruptive technologies and architectures such as augmented artificial intelligence (AI), workloads in the cloud, virtual reality, cloud-native solutions and gamification will continue to transform banking experiences. As the competition rises, neobanks must focus on creating a future-proof platform strategy with a robust underlying technology stack that makes their apps intuitive and engaging for customers at all times.

Figure 3: Over 95% of the neobanks in the Asia Pacific have a live mobile application

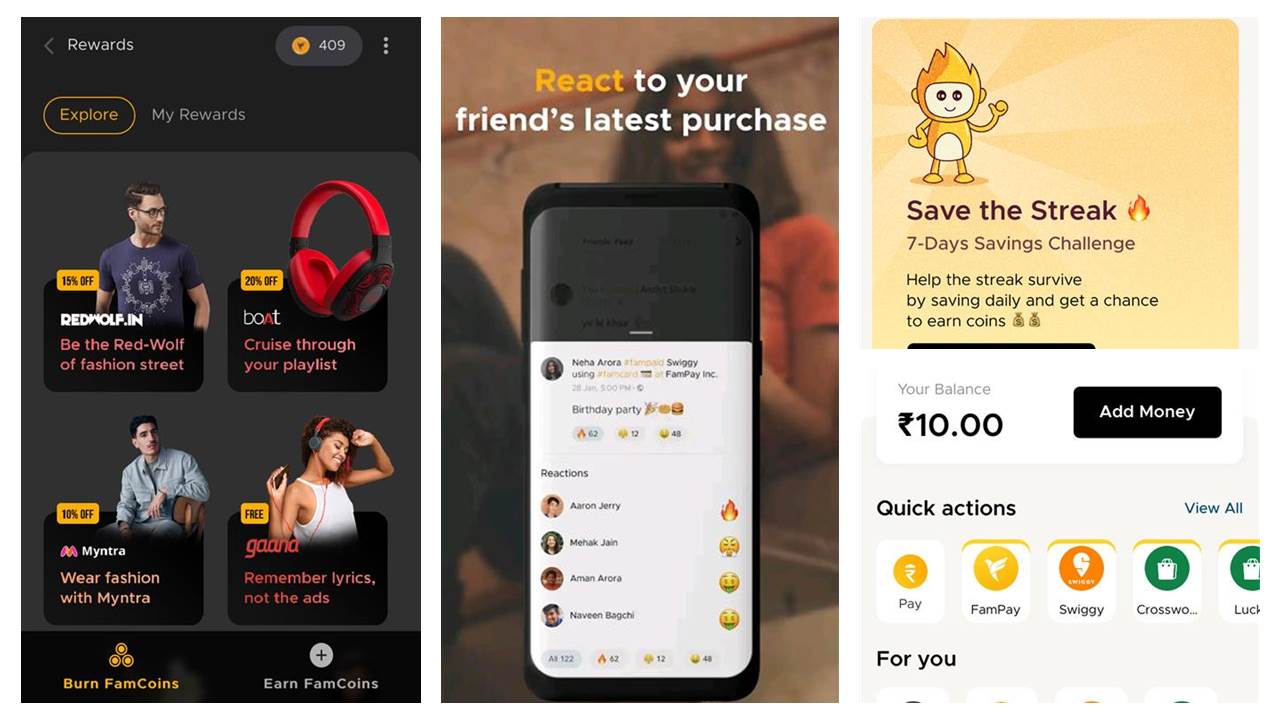

FamPay, India

- Fampay operates under the banking license of IDFC Bank India. It has built a banking platform exclusively for kids and teenagers. The app allows parents to open prepaid bank accounts for their kids to manage their savings and spending at a young age. A simple user interface, quick registration process and gamified money management tools within the platform help inculcate the habit of saving among kids.

Figure 4: FamPay offers an engaging banking platform for kids in India

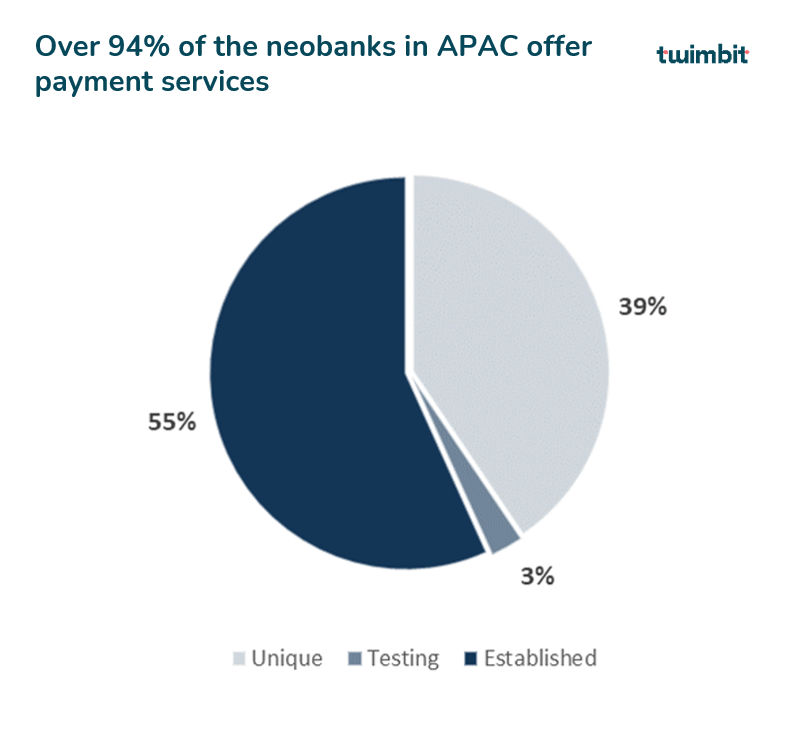

Payments

97.06% of the neobanks in the Asia Pacific have established or unique payment options (Figure 5) that traditional banks offer (domestic and international transfer, and debit cards), of which 47.06% offer a gamut of unique payments options, including:

- Virtual cards

- Biodegradable cards

- Peer-to-peer payments

- Automated recurring transactions

- Split payments

- QR payments

- Buy Now Pay Later (BNPL) option

For winning in the future, neobanks must ramp up their capabilities to enable payments through voice, touch, and gestures using multi-experience platforms that operate multiple modalities in a secured manner.

Figure 5: Over 94% of the banks in the Asia Pacific offer payments service

Jenius Bank, Indonesia

- Jenius by BTPN Bank in Indonesia is a millennial-centric neobank that offers a unique payment option, allowing its customers to split bills. This option help customers to divide any bill with their friends or families instantly. A notification in the app sends the bill to the customer. A few easy steps enable the bill payment via $Cashtag. This feature provides an alternative identity to each Jenius user to send and receive money within the Jenius community.

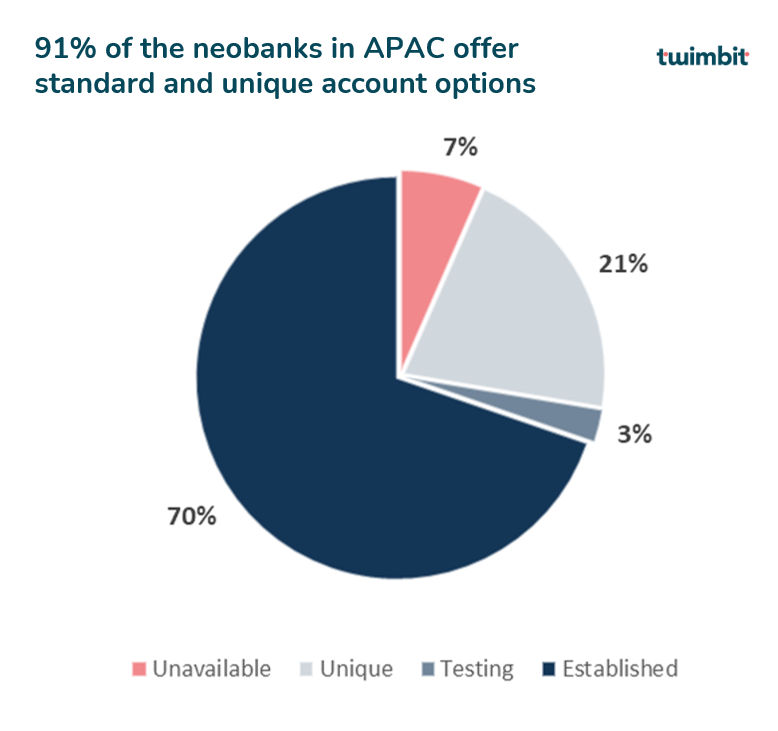

Accounts

73.53% of the neobanks in the Asia Pacific offer standard (established) personal and business accounts (Figure 6) that are standard in nature, while 23.53% of the neobanks offer unique account services such as:

- Joint account

- Teen and kid account

- Multicurrency account

Neobanks offer a virtual onboarding experience that enables instant electronic customer remediation rather than a long, tedious, and expensive verification process. Hence, neobanks do not face the cost impediments of physical infrastructures, personnel within branches, and bulky physical storage capacities. The cost efficiencies translate to offering high-interest rate savings accounts with minimal to zero balances at no cost.

Figure 6: 91% of the neobanks in the Asia Pacific offer standard (established) and unique account options

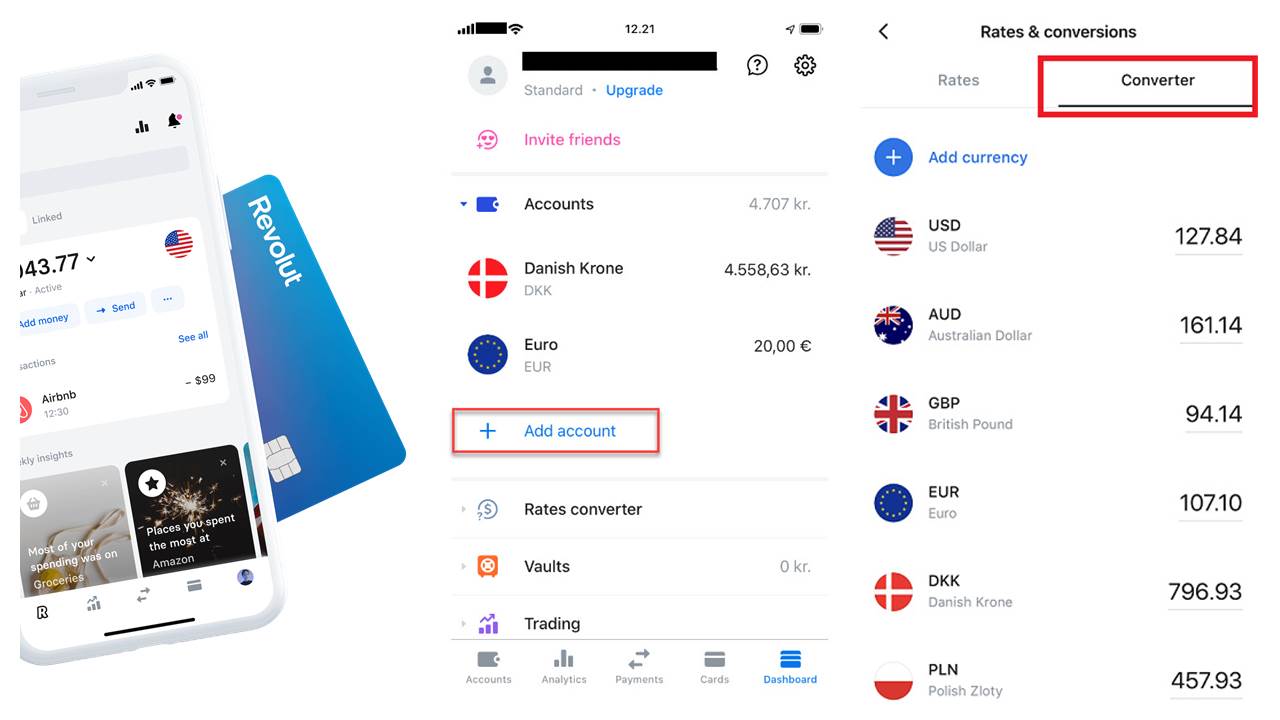

Revolut, Global

- Revolut operates in 7 countries, including Australia, Singapore, and Japan in the Asia Pacific. The neobank allows its customers to open multiple unlimited multi-currency accounts to manage their business with no hidden charges. It supports over 30 different currencies. Revolut also allows its customers to view and track all their internationals transactions in real-time from different accounts in a single dashboard. Moreover, customers are in full control of what their team members can see and do.

Figure 7: The Revolut multi-currency account supports over 30 different currencies

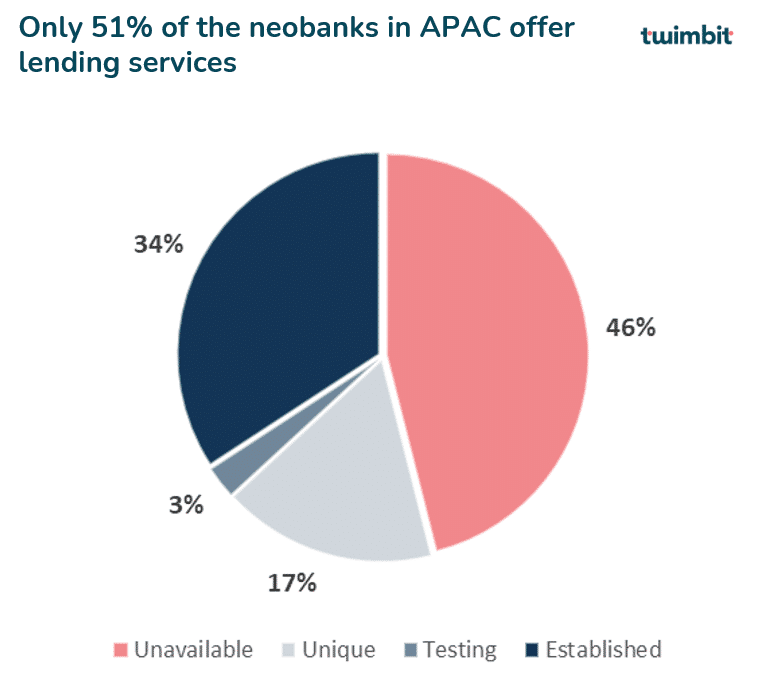

Lending (Retail and business)

In addition to multiple visits to the banks and unwanted costs, it generally takes two to four weeks to get a loan sanctioned from a traditional bank. Neobanks are transforming the loan market by assessing the creditworthiness of a customer and disbursing loans within minutes. With the advent of open banking, neobanks synchronise data from various sources to create comprehensive credit profiles of their customers. The democratisation of data also empowers neobanks to offer loans to individuals or businesses who are either first-time borrowers or have struggled to gain credit from incumbents.

However, the Asia Pacific still represents an untapped market for lending, with 88.23% of neobanks offering standard and unique lending services (Figure 8) such as SME loans, personal loans, credit cards, and business overdrafts.

Figure 8: 51% of the neobanks in the Asia Pacific offer lending services

MYBank, China

- MYBank, with its 3-1-0 loan model, has revolutionised the lending market in China and acquired unicorn status globally. The neobank institutes a robust risk management system that uses real-time payment data, social media interaction, and lifestyle choices to analyse more than 3000 variables for customer verification and risk profiling. It takes a customer about 3 minutes to apply for the loan and1 second for approval with zero human involvement. MYBank has catered to over 16 million SMEs in China.

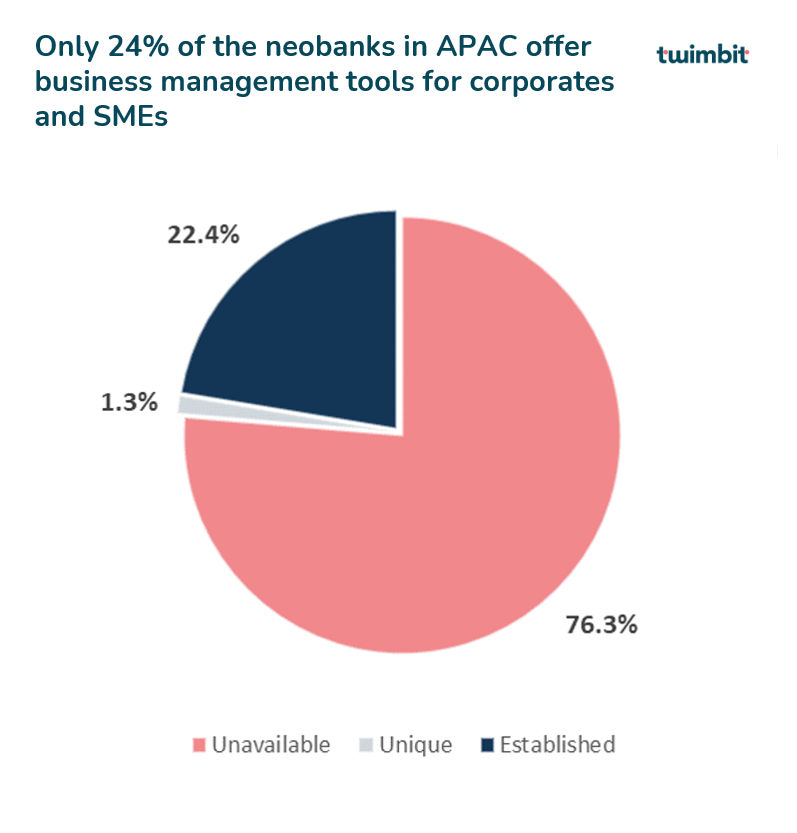

Business management tools

In the Asia Pacific, only 23.53% of neobanks offer business management tools (figure 9). Coupled with the rapid growth of SMEs in the region, this is a largely untapped turf for neobanks to generate new revenue streams and increase customer stickiness. Business management tools enable neobanks to serve SME needs in a constructive and targeted manner.

They can offer activities automation, such as cash flow management, payroll assessment and disbursement, and account reconciliation to take the non-core workload off SME owners. These tools also help neobanks understand business functioning to predict cash flows inflexions, credit needs, and sales revenue in the future. Neobanks can build credit financing models based on the day-to-day information collected from SME operations, and in turn, help business owners access an expanded line of credit.

Figure 9: Only 24% of the neobanks in the Asia Pacific offer business management tools for corporates and SMEs

Aspire, Singapore and Thailand

- Aspire is a neobank that specifically caters to the SME segment. The neobank currently operates in Singapore and Thailand. To enable SMEs to manage their cashflows easily and efficiently, Aspire is launching an invoice management feature in its application. This feature will allow SMEs to create and customise invoices, get intelligent cashflow insights on invoices and reconcile all incoming payments by integrating all business accounts to one unified dashboard. Moreover, the neobank also sends automatic reminders and updates about payment timelines.

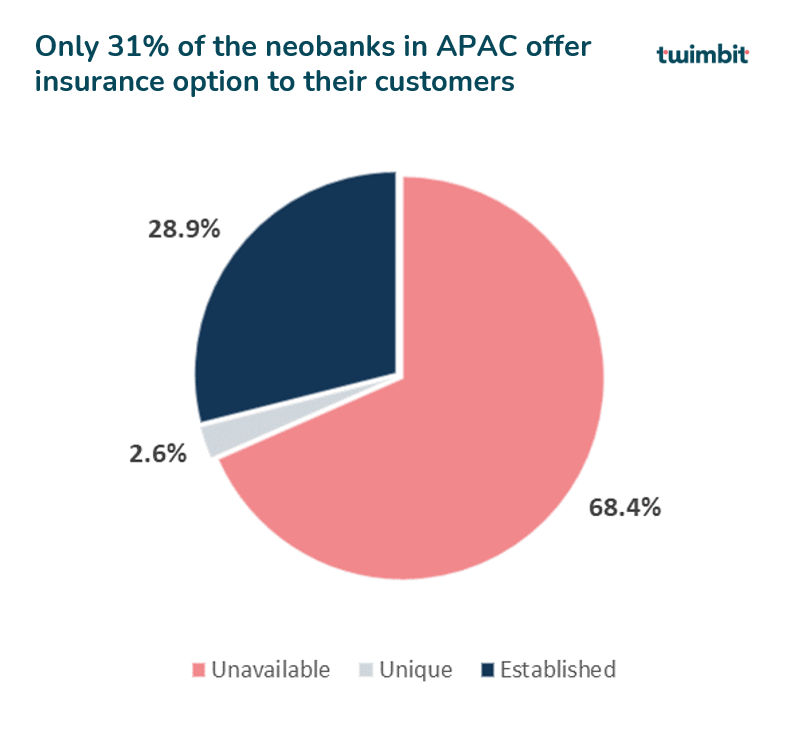

Insurance

Neobanks increase revenue streams through cross-selling products on their platforms. One of the most attractive products is byte-size insurances alongside its standard insurance products. However, the market is still at the nascent stage. 79.41% of the neobanks (figure 10) in the region have partnerships with leading bancassurance service providers to offer insurance solutions to consumers and businesses exclusively through their mobile applications.

Figure 10: 31% of the neobanks in the Asia Pacific offer insurance options to their customers

Airtel Payments Bank, India

- India’s leading payments bank, Airtel Payments Bank, offers its customers a variety of insurance options, including insurance for travel, accident, mobile, and home. It allows customers to pay their insurance premium with their online payment service anytime and anywhere, along with the choice to avail of any insurance benefits or rewards.

Wealth management

Only 29.41% of the neobanks (Figure 11) in the Asia Pacific offer wealth management services to their customers. A key reason for the unpopularity of wealth management products in neobanks are in the nascent stage of their operations. Therefore, wealth management products are a significant growth opportunity for neobanks. They enable customers to make byte-size investments through their platform with the assistance to manage portfolios.

Moreover, neobanks can conduct regular surveys and release video-ask campaigns to understand their customers’ long-term goals and make them financially literate. In order to add a personalised touch and make customers feel secure, the neobank can assist its customers through live virtual interactions, thus providing personalised investment advice based on a customer’s age, income and financial needs.

Figure 11: Only 29.41% of the neobanks in the Asia Pacific offer wealth management tools

The wealth management offerings may not necessarily be a proprietary solution for the neobank. Such capabilities, however, can be integrated from third-party providers who offer innovative solutions for investments. Marketplace integration will further strengthen revenue propositions for the neobank as it operates in a low-margin environment.

Digibank by DBS

- Digibank currently operates in Singapore, India, and Indonesia. The neobank recommends 5-star rated mutual funds with over 250 options to choose from, based on a customer’s budget and an agreed risk level. Customers can compare between mutual funds and buy or sell them at the drop of a hat. Digibank does not charge any transaction fees on investments and offers a lifetime free investment account with a 24×7 secured and encrypted communication interface.

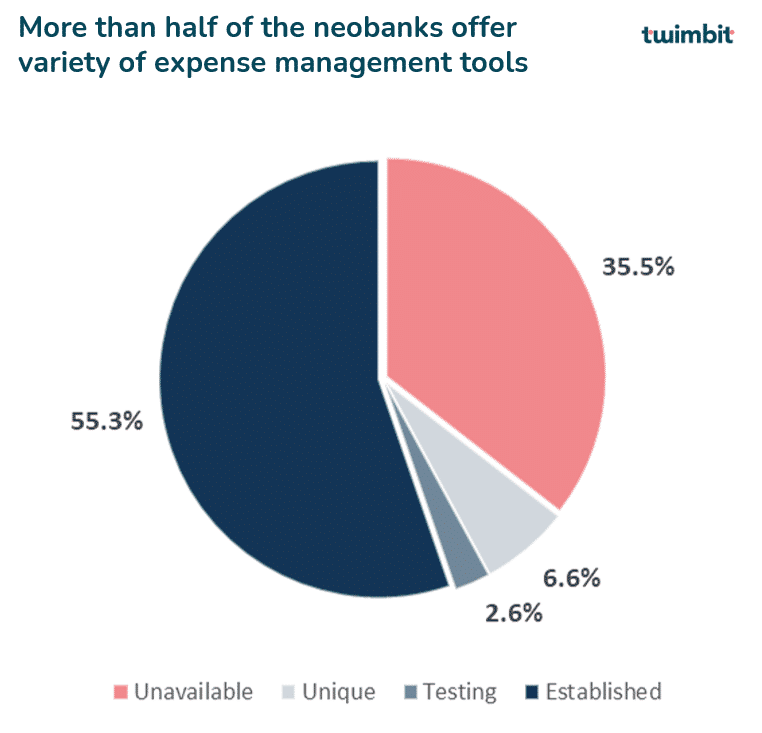

Expense management

Neobanks use AI and machine learning technologies to integrate and analyse real-time data in the bank’s back-end infrastructure to deliver practical insights on its customers’ spending and budgeting patterns. 73% of the neobanks (Figure 12) in the region offer various expense management solutions to their customers. The neobanks also allow customers to set a specific goal to spend and save, inculcating a mindful way of managing one’s own money in their daily transactions. As a way to incentivise the customers in achieving their goals, neobanks offer rewards, conduct challenges, and create live in-app games.

Figure 12: More than half of the neobanks in the Asia Pacific offer a variety of expense management tools

Up Bank, Australia

- Up Bank is a digital spin-off launched by Bendigo and Adelaide Bank in Australia. The neobank has come up with an innovative solution to boost a customer’s savings. In addition to the bank’s expense management dashboard, it gives customers an option of rounding up their transactions to the nearest dollar and contribute the rounded-up amount towards savings. For example, when a customer purchases a book for AUD 10.60c, then 40c would be automatically rounded up and accounted to the customer’s savings account.

Video 1: UP Bank offers a unique option of rounding up transactions to boost savings

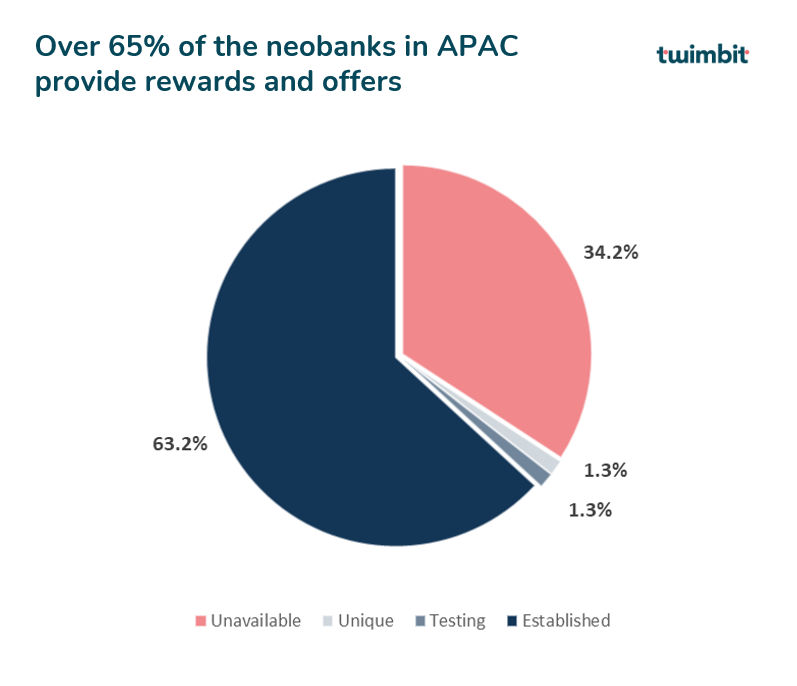

Rewards and offers

63.33% of neobanks (Figure 13) reward their customers in versatile ways to keep them engaged and vested with the bank. In order to acquire and retain customers, neobanks capitalise on hyper-personalised rewards and cashback. These incentives are based on the information the bank collects by continuously monitoring its customers’ transactions and spend categories. The banks are beginning to are embed GPS, Wi-Fi, and cellular tracking to provide rewards that are dependent on the customer’s location.

Figure 13: Over 65% of banks offering rewards and offers in the Asia Pacific

FRANK, Singapore

- FRANK by OCBC targets millennials and the Gen Z population of Singapore. It has differentiated product offerings for students and executives. The bank offers over ten different cards with different reward plans. Customers can choose a personalised debit or credit card that best suits their spending pattern. For example, the OCBC 365 Credit Card is best suited for individuals who dine often, while OCBC Titanium Rewards Card is best suited for travellers.

Marketplace integration

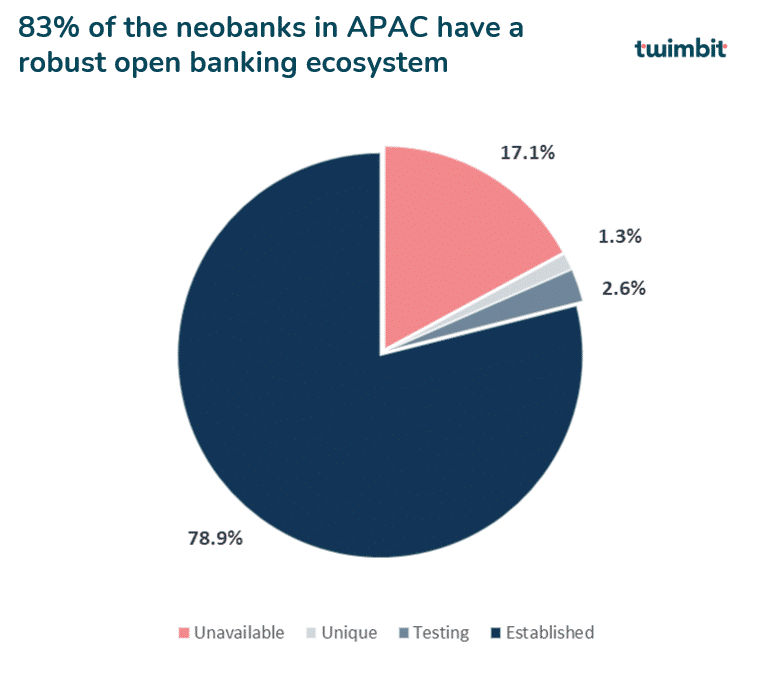

Over 95.59% of neobanks (Figure 14) in the Asia Pacific have an established open banking infrastructure. However, it is still in its infancy. Countries in the Asia Pacific are slowly adopting a structured and regulated open banking system. The open banking ecosystem allows platform-based banks to establish a marketplace for multiple third-party players to integrate their services at a one-stop location. This ecosystem empowers customers to consume more services on a single platform than juggle between multiple applications for their financial needs.

One noteworthy example comes from Australia. The Australian Competition and Consumer Commission launched the first phase of its open banking initiatives through the Consumer Data Right (CDR) in 2020. Under this system, consumers consent to transfer data from banks to an accredited data recipient who will use the information collected to create personalised products and services.

An initiative like this opens the greater potential for neobanks to understand their customers’ spending patterns, financial health, and investment goals for tailoring solutions to suit specific needs. Additional products and services best suited to satisfy the customers’ needs can match to the basic services by partnering with third-party players, thereby increasing revenue opportunities for the neobanks.

Following a holistic data-driven approach with feature-rich API platforms will allow neobanks to stay ahead of their competitors. Data security and fraud prevention are also key success measures for neobanks.

Figure 14: 83% of the neobanks in the Asia Pacific have a robust open banking ecosystem

InstantPay, India

- One of India’s oldest and largest neobank, InstantPay, has its inbuilt open banking platform called InstantPay API. The platform is super scalable, and it auto-scales from zero to a million transactions every day. Businesses can integrate this platform with their business applications or accounting systems. InstantPay installs several layers of verification to maximise security and ensure data protection.

How can neobanks unleash their full potential by hiding in plain sight in the future?

For them to win in the future, neobanks will operate from behind the curtain and embed themselves in the customers’ daily lives without the preamble of defined product offerings. Neobanks will provide financial services that automatically respond to the date and day of a particular month, its customers’ location, life stages and events. These banks will emphasise on improving the quality of its customer’s life by optimally channelising the ability of augmented insights, quantum computing, and predictive modelling.

As invisible banking becomes more evident in the coming decade, it will not necessarily take away the underlying neo banking platform. The product stack of neobanks will float per the customers’ needs and do not have to be carried out through the proprietary platform explicitly.

Endnotes:

Banking consumer study: Making digital banking more human

Welcome to the Invisible Bank and the Era of Frictionless Connectivity (citibank.com)

Akshita Maurthavanan, Research Intern, contributed to the research in conducting preliminary literature review, building data library, writing, and conceptualising the article.