Key Highlights

- The total number of branches in APAC (Asia-Pacific) has increased by 1.03% YoY.

- Indian banks reported the highest increase at 4.57% YoY.

- Australian Banks saw a decline of 9.01% YoY.

- The median average branch expense-to-revenue ratio has decreased to 14.46% YoY.

- Indonesian banks had the highest increase at 16.37% YoY, rising from 4.5% to 5.24%.

- Australian banks saw a decline at 14.46% YoY, decreasing from 3.06% to 2.62%.

- The total number of customers served per branch monthly have increased by 12.92% YoY.

- Philippine Banks had the highest increase at 70.53% YoY.

- Indian Banks reported a decline of 0.42 % YoY.

- APAC banks are modernising core systems, upgrading network infrastructure with 5G, and ensuring 24/7 operations.

- Indian banks have a dual approach of expanding physical branches while embracing digital banking due to trust factors.

- Australia’s big banks are closing branches due to a shift towards digital channels but risk alienation of regional communities.

- Malaysia’s digital-only banks are disrupting traditional banks with superior customer experience.

- Philippines’ branches are revamping from transactional roles to advisory services driven by digital growth.

- Thailand’s hybrid model combines physical branches with an increased focus on advisory services supported by technological investments.

- South Korean banks are focusing on self-service by deploying AI-based STMs and self-service kiosks while reducing branch networks.

- Chinese banks are expanding rurally using smart/mobile branches and rural finance platforms for better reach.

Operational performance indicators

Branch network

The impact of increased revenue on branch numbers varies significantly by country and is influenced by local market conditions and digital trends. With net revenue growing by 10.7% YoY, some regions are seeing banks expand their branch networks to capitalize on revenue growth and enhance customer service, reflecting a strategic focus on market penetration and accessibility. Conversely, in other countries, banks are reducing branch numbers as they shift towards digital channels and streamline operations. This includes closing less profitable branches and investing in technology to meet the rising demand for online and mobile banking services.

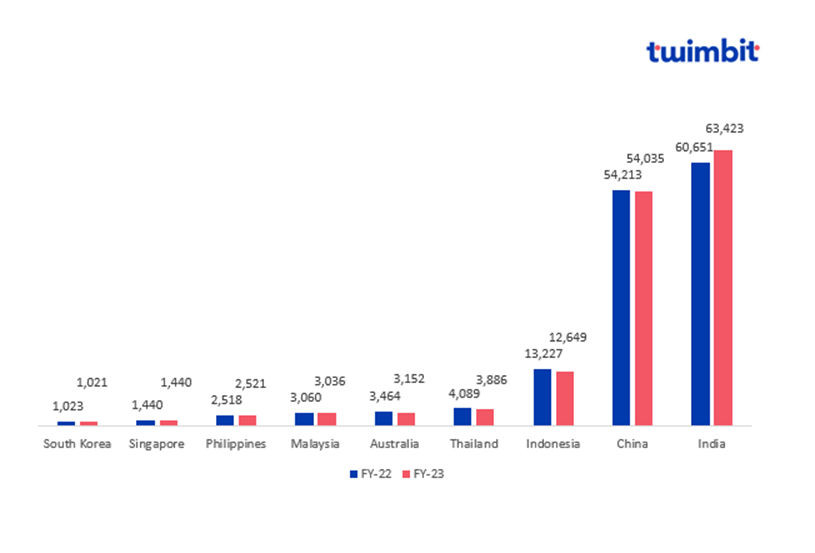

The branch network of APAC banks has increased by 1.03% YoY, from 143.7 thousand in FY-22 to 145.1 thousand in FY-23.

Source: Bank financials, Twimbit analysis

- Indian banks have reported the highest increase in their number of branches, achieving a 4.57% YoY growth. This expansion is indicative of strategic efforts to enhance market penetration and accessibility.

- Conversely, Australian banks have experienced a decline in their number of branches by 9.01% YoY. This reduction reflects a strategic shift towards digital banking channels and an optimization of physical branch networks.

Branch expense-to-revenue ratio

A low branch expense-to-revenue ratio signifies effective cost management and operational efficiency, whereas a higher ratio indicates potential inefficiencies. The slight increase from 44.38% in FY-22 to 44.44% in FY-23 underscores ongoing inefficiencies and suggests a need for further improvements in cost management. This ratio is critical in assessing a branch’s ability to manage costs relative to income, with fluctuations offering valuable insights into operational effectiveness and informing strategic decisions to enhance financial performance.

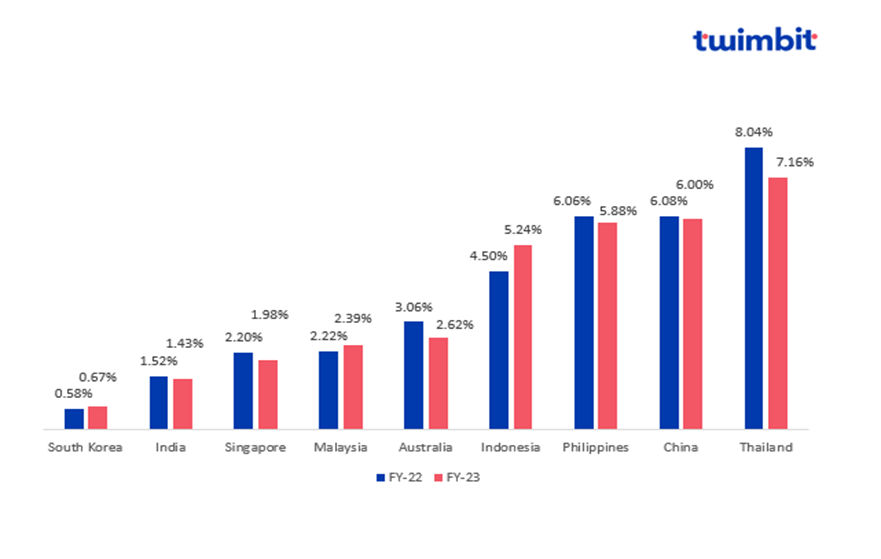

The median average branch expense-to-revenue ratio has decreased by 14.46% YoY, from 3.06% in FY-22 to 2.62% in FY-23.

*The expenses of Shinhan Bank, ABC, and BOC were estimated by Twimbit

Source: Bank financials, Twimbit analysis

Indonesian Banks have reported the highest increase in expense-to-revenue ratio at 16.37%, increasing from 4.5% in FY-2022 to 5.24% in FY-2023. This can be attributed to:

- Increase in salaries, wages, and allowances elevate a branch’s expense-to-revenue ratio by raising operating costs.

Australian Banks have reported a notable decline of 14.46% with figures dropping from 3.06% in FY-2022 to 2.62% in FY-2023. This downturn can be attributed to two primary factors:

- There is a marked shift among customers towards digital banking solutions, reducing reliance on traditional branch-based services.

- The reduced foot traffic within physical branches has led to a decrease in the volume of in-branch transactions.

An increase in the expense-to-revenue ratio typically occurs when there is a significant rise in salaries, wages, and allowances, while revenue growth remains sluggish. This imbalance arises because higher labour costs consume a larger portion of the revenue when income does not scale at a commensurate rate.

Customer-to-branch ratio

The customer-to-branch ratio serves as a critical indicator of how effectively banks are managing their physical locations. There has been a notable shift in the balance between maintaining a physical branch presence and driving digital innovation. While some regions excel in optimising branch efficiency through modern strategies, others face challenges in expanding their reach and enhancing branch performance. This dynamic underscore varying approaches banks are following to adapt to evolving market demands and technological advancements.

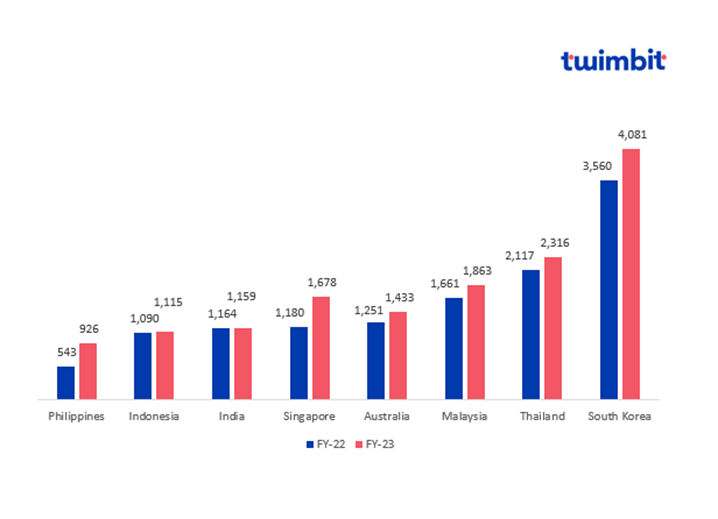

The total number of customers served per branch monthly has increased by 12.92% YoY, from 16.16 thousand in FY-22 to 18.25 thousand in FY-23.

Source: Bank financials, Twimbit analysis

Philippine banks have reported the highest growth in the customer-to-branch ratio, achieving a remarkable 70.53% YoY. Despite having the lowest customer-to-branch ratio compared to other regions, this surge reflects the effectiveness of several strategic initiatives.

- Implementation of automation and optimized processes has significantly improved operational efficiency.

- Prioritising personalised service and support has enhanced the overall customer experience.

In contrast, Indian banks have experienced a slight decline of 0.42% YoY in their customer-to-branch ratio due to specific challenges:

- Opening branches in areas with lower population densities has resulted in reduced demand for services.

- The emphasis on Micro, Small, and Medium Enterprises (MSME) loans narrows the customer base and creates service overlap.

Key developments in the APAC region

Each region in the APAC presents different characteristics in terms of branch structure. As such, banking institutions must carefully consider which key developments are essential for maximum benefit. Key developments include the following:

- Banks are beginning to prioritise a higher form of community-oriented experience with a personalised touch supported by extensive infrastructure capabilities.

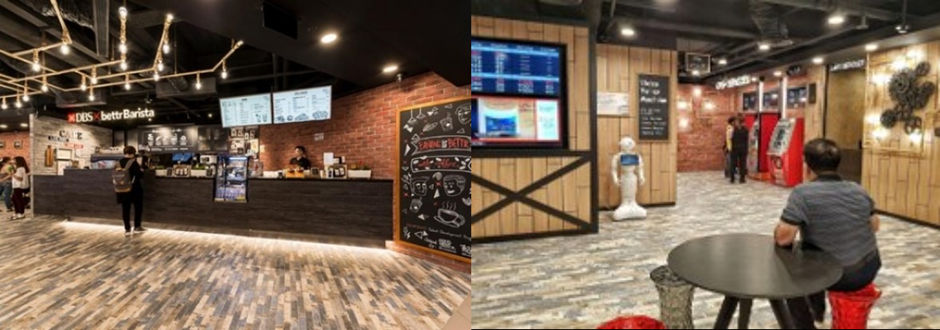

DBS’s “cafe and branch concept” – This unique approach ensures the branch is designed with an open floor plan and a relaxed atmosphere. The easy accessibility of a coffee shop within the bank branch further accentuates this atmosphere. Customers can grab a coffee while they wait or discuss their banking needs.

2. Banks face pressure to reduce the size of their branch facilities to optimise floor space and enhance control over customer interactions, a common challenge in larger branches.

ICICI Bank’s “branch rationalisation” strategy – By consolidating smaller branches and opening new, smaller branches in high-traffic areas, ICICI Bank in India can seek to optimise its footprint and cater to the growing digital banking population.

3. Despite experimenting with different branch types, most banks continue to emphasise the one-stop-shop model of retail, family, and lifestyle branch concepts.

The “OCBC Future Smart Branch” by OCBC bank in Singapore – This one-stop-shop model integrates banking with lifestyle elements. This model also includes a family-friendly environment with play areas for children and digital advisory services for adults.

4. Leading banks are entering a critical phase of branch evolution, transitioning from a ‘processing factory’ and liability-driven model (common in emerging markets) to an advisory and asset-based model.

ICICI Bank in India is shifting its focus from traditional transaction-based services to offering more advisory and wealth management services, positioning its branches as financial advisory centres.

5. To maximize branch value, the best-in-class banks have begun to adopt an integrated approach. They connect branches with electronics, other network points, and the surrounding micro-market. Internally, they align with strategic priorities, back-end infrastructure, and staff/branch management.

CBA has invested over USD 39.51 million in branch upgrades for the 2024 financial year including USD 11.19 million for the June quarter. From April to June 2024, eight branches received significant renovations, following a USD 29.63 million investment in 20 branches between July 2023 to March 2024. The upgrades feature self-service banking technology, private meeting areas, and improved accessibility with Braille signage and hearing loops.

6. Retail banking executives highlight that there is room for improvement in their plans, processes, and technologies in place. Expressing overall dissatisfaction with the results, most banks have identified the need to acquire better hiring, training & frontline tactics and turn their staff into customer champions.

CBA’s “Branch Transformation Program” – This program emphasises that branch staff are “financial problem solvers” rather than just product sellers. Here, the staff are trained to understand customer needs holistically and recommend solutions across various financial products. This multi-skilled approach enables them to serve customers more effectively.

7. Branch managers are shifting from a business line focus to a market-oriented focus, leading to the rise of owner-entrepreneurs and multi-skilled frontline staff.

BPI’s “Community Branching” initiative aims to empower branch managers to build relationships with local businesses and community leaders. This allows them to identify specific financial needs within their market and develop targeted products or services, fostering a more entrepreneurial approach.

Top APAC banking trends in 2024

In 2024, the APAC banks are having a pivotal transformation, driven by cutting-edge technological advancements, shifting customer demands, and strategic operational realignments.

- #1 Core system modernisation

To stay competitive and agile, banks in the APAC region are modernising their legacy infrastructure. This modernisation is crucial to enhance efficiency and customer experience. Banks can achieve this through:

- Orchestrating customer journeys

- Centralised data management – The systems can ingest and integrate data from various accounts, products, and interactions, creating a single source of truth for a holistic customer view.

- Streamlined omnichannel experiences – A modernised core simplifies integration and streamlines product development, creating more consistent and frictionless customer experiences across all touchpoints.

- Personalised offerings – The seamless integration of advanced analytics tools and open APIs has enabled banks to segment customer bases, leverage insights, and integrate third-party solutions. This empowers banks to provide personalised product recommendations and tailored financial solutions.

- New customer relationships

- Modular architecture – Modern core systems are built on microservices, allowing for independent development and deployment of new features, making it faster to experiment, test, and iterate on new products and marketing campaigns.

- Advanced analytics tools can help banks identify trends, predict customer behaviour, and uncover hidden opportunities for innovation. This data-driven approach can guide the development of new products and services that meet specific customer needs.

- Embedded experiences

- Open API ecosystem – Modern cores offer open APIs and integration capabilities that allow seamless connection with third-party applications and services, facilitating the embedding of financial functionalities into customers’ daily lives, like automatic bill payments from IoT devices or goal-based savings within budgeting apps.

- Strategic partnerships – Partnering with fintechs, e-commerce giants, travel companies, and other established players allows banks to access new markets, expertise, and technologies. This can accelerate the development and implementation of embedded banking solutions, providing a faster time-to-market advantage.

- Hyper-personalisation

- AI and analytics – The use of AI and analytics to clean real-time customer data from transactions, spending patterns, and other interactions empower the banks to offer personalised financial advice, proactive alerts, and tailored product recommendations, going beyond reactive solutions.

- Gamification – Gamification elements are not just fun and flashy; they generate valuable data on user behaviour, preferences, and financial goals. Banks can design challenges that cater to users’ specific financial situations and aspirations.

- #2 Upgrading network infrastructure and 5G

APAC banks are actively upgrading their network infrastructure and leveraging 5G technology to enhance their services and operational efficiency. This transformation is driven by the need to improve digital banking experiences, support emerging technologies, and cater to the growing demand for mobile and internet-based financial services.

- Upgrading network infrastructure

- Enhanced connectivity and speed – Many banks in the APAC region are investing in high-speed network infrastructure to support faster and more reliable internet connections. This is crucial for enabling seamless digital banking services, such as mobile banking apps, online transactions, and remote customer support.

- DBS – The bank has focused on enhancing its connectivity and speed by upgrading its IT infrastructure. This includes adopting high-speed broadband and improving network reliability to support its extensive range of digital banking services.

- Use of cloud services – Banks are adopting cloud computing to ensure scalability, flexibility, and cost-efficiency. Cloud infrastructure allows banks to handle large volumes of transactions and data with improved security and compliance.

- ANZ – The bank has partnered with leading cloud service providers like Amazon Web Services (AWS) to transition its core banking applications to the cloud. This move is aimed at improving scalability, reducing costs, and enhancing the bank’s ability to innovate rapidly.

- Leveraging 5G

- 5G Deployment – The adoption of 5G technology is set to revolutionise the banking sector in APAC. By 2030, 5G is expected to account for over 40% of mobile connections in the region. Countries like Australia, Japan, Singapore, and South Korea are leading in 5G deployment, enhancing the speed and reliability of mobile banking services.

- KB Kookmin Bank – The bank is leveraging South Korea’s advanced 5G network to enhance its mobile banking services. The bank uses 5G technology to provide high-speed, real-time financial services, including video consultations and remote customer support.

- Improved mobile banking – With 5G, banks can offer enhanced mobile banking experiences, including faster transaction processing, high-definition video consultations, and augmented reality (AR) and virtual reality (VR) applications for customer engagement and support.

- Bank of China – The bank is using 5G technology to improve its mobile banking services, enabling features like biometric authentication and high-speed financial transactions, which enhance the overall customer experience.

- Smart branches and ATMs – 5G enables the development of smart branches and ATMs that can offer personalised services, biometric authentication, and advanced security features. These branches can also utilize Internet of Things (IoT) devices to monitor and manage branch operations more efficiently.

- HSBC (Hong Kong) – The bank has implemented smart ATMs and branches that use 5G technology to offer a range of services, from personalised banking advice to secure and swift transactions. These smart branches are designed to improve customer engagement and operational efficiency.

- #3 24/7 operations

APAC banks are implementing various strategies and technological advancements to support 24/7 operation infrastructure requirements. These efforts are aimed at ensuring uninterrupted banking services, enhancing customer experience, and maintaining high levels of operational efficiency. Some of the key initiatives are:

- Cloud computing

- Standard Chartered Bank – The bank has moved a significant portion of its infrastructure to the cloud. This move ensures scalability and reliability, allowing the bank to maintain operations around the clock. The cloud infrastructure provides robust disaster recovery and high availability, critical for supporting 24/7 operations

- DBS – The bank has adopted a cloud-first strategy, leveraging cloud services to ensure continuous availability and scalability of its digital banking services. This approach helps the bank manage high volumes of transactions without downtime, crucial for supporting a 24/7 banking environment.

- Artificial intelligence and automation

- OCBC – The bank has implemented AI-driven systems to automate routine tasks and enhance operational efficiency. These systems include chatbots for customer service, automated fraud detection, and predictive maintenance for IT infrastructure, all contributing to a seamless 24/7 operation.

- CIMB – The bank utilizes AI and machine learning to monitor and optimize its IT infrastructure. Automated systems predict and resolve potential issues before they impact services, ensuring uninterrupted operations and improving overall reliability.

- KB Kookmin Bank – The bank launched multiple AI services such as voice phishing monitoring, an automated corporate lending review system (ML Bics), KB AI Financial Assistant, an AI financial consulting system, and the KB AI Translator.

- Network and data centre upgrades

- CBA – The bank has invested heavily in upgrading its network infrastructure and data centres. The bank uses redundant systems and advanced data centre technologies to ensure high availability and disaster recovery capabilities, which are essential for 24/7 operations.

- ANZ – The bank has enhanced its data centres with state-of-the-art technologies, including advanced cooling systems, redundant power supplies, and robust cybersecurity measures. These upgrades ensure that the bank’s critical systems always remain operational, supporting continuous service availability.

- Cybersecurity enhancements

- HSBC (Hong Kong) – The bank has implemented advanced cybersecurity measures to protect its infrastructure from cyber threats. This includes real-time monitoring, threat detection, and automated response systems that operate 24/7 to safeguard customer data and ensure uninterrupted services.

- NAB – The bank uses a combination of AI, machine learning, and big data analytics to enhance its cybersecurity posture. These technologies help detect and mitigate threats in real-time, ensuring the bank’s operations are not disrupted by cyber incidents.

- Digital platforms and mobile banking

- UOB – The bank has developed robust digital platforms and mobile banking applications that provide customers with 24/7 access to banking services. These platforms are built on scalable and resilient architectures to manage high transaction volumes without downtime.

- BOC – The bank offers comprehensive mobile banking services that allow customers to perform a wide range of banking activities anytime, anywhere. The bank’s digital platforms are designed to be highly available and secure, supporting continuous operations.

- BOQ – Following its acquisition of ME Bank, BOQ is integrating a new digital platform to enhance the customer experience for ME Bank clients. This strategic initiative aims to deliver a superior digital experience across transaction accounts and mortgages, streamline operations, and reduce duplication.

- Continuous monitoring and support

- KB Kookmin Bank – The bank employs continuous monitoring tools and dedicated support teams to ensure its IT infrastructure is always operational. These teams use real-time analytics to detect and address issues proactively, maintaining high service availability.

- Maybank – The bank has implemented round-the-clock monitoring and support systems to manage its IT infrastructure. These systems use AI and machine learning to predict and prevent potential failures, ensuring seamless 24/7 operations.

Key drivers of branch transformation

Branch transformation is being driven by critical factors such as heightened competition in the banking sector and evolving customer expectations.

- Changing customer expectations

Banks should continuously seek new ways to simplify their services, adapting to modern banking preferences. While addressing customer expectations remains a challenge, banks must prioritise making banking easy and flexible, whether in person or online, to meet customer needs effectively.

- People want banking to fit their personal needs. They want to switch between going to a bank and using apps seamlessly while seeking fast information, intuitive interfaces, and quick service.

- Updating bank branches with digital tools can help. Queue management software allows customers to save their spots. This results in shorter and smoother queues, increasing everyone’s satisfaction.

- Convenient self-service options like online banking, mobile deposits, and remote account management via kiosks empower customers to control their transactions.

- Personalised assistance and 24/7 support for customers through AI and chatbots.

- Real-time transaction monitoring and automation to speed up services and enhance the overall customer experience.

- Increasing competition in the banking sector

Fintech companies and digital banks pressure traditional banks to shake up their services and work harder to stand out. There are several methods that today’s banks can employ to keep up with the increasing competition for customer retention.

- Updating bank branches is crucial for banks to keep up and keep customers happy. Banks should make their branches different to fight competition while making branches digital-friendly.

- Offering WhatsApp appointments is another unique approach banks can use to ensure higher customer retention. By providing a modern way to connect with customers, banks can ensure that the customer remains their operation’s top priority.

The enduring allure of brick-and-mortar: Why Indian banks embrace physical branches in the digital age?

India’s banking sector is experiencing a fascinating duality. While the nation continues to embrace and explore full-fledged digital banking, it simultaneously recognises the enduring value of physical branches.

This paradoxical trend stems from the importance of trust in banking, especially in developing regions. Despite the rise of fintech, the traditional reality remains. While digitalisation remains a key strategy for growth, Indian banks (particularly private ones) are defying expectations by expanding their branch networks.

Leading institutions like HDFC Bank and ICICI Bank have significantly increased their physical presence, challenging the notion that digital dominance renders brick-and-mortar obsolete. This focus on physical infrastructure can be attributed to the fundamental nature of banking – it’s built on trust. While digital platforms offer convenience, face-to-face interactions with bank representatives remain crucial for building trust, especially in rural and semi-rural areas.

Despite the growth in digital adoption, traditional banking services have not been fully replaced. This is because physical branches offer one hallmark that digital banks lack – a sense of security and a familiar touchpoint, aspects that are highly valued by customers in smaller towns.

Hence, while Indian banks are continuously expanding their branch network to serve the population, there is pressure on them to innovate within their branches.

- Digital banking units (DBUs)

DBUs are specialised bank branches by the Reserve Bank of India (RBI) to bridge the gap between traditional banking and digital access. As of June 2024, there are 84 DBUs operational across India, set up by a mix of public and private sector banks.

- Promote financial inclusion – Bridge the gap for people who may not have access to traditional banking or lack the confidence to use digital banking services independently.

- Increase digital literacy – Educate people in rural and semi-urban areas about the benefits and security of digital banking.

- Expand banking reach – Provide essential banking services in areas where traditional branches may not be feasible.

Australian banks are in danger of estranging regional communities as they reduce their branch networks

Australia’s big four banks (CBA, ANZ, Westpac and NAB) have sped up branch closures due to increased customer preference for digital channels. In 2023, they shut down 375 branches, marking a 56% increase from 239 closures in 2022 and 337 closures in 2021. Since 2018, these banks have collectively closed 1,446 branches.

Many have expressed concern against this trend, with the risks of alienating rural communities reliant on physical branches. Banks justified the closure of branches in response to shifting customer preferences favouring digital services over traditional banking. However, ongoing scrutiny of these closures in a public hearing has highlighted the adverse impact on communities left without nearby branches.

- Digital focus

- CBA invests USD 0.69 billion annually in its branch network. However, most of its customer base conducts transactions through its CommBank app. Transactions through the app surpassed USD 12.59 billion, marking a 64% increase within the last two years.

- The value of mobile wallet transactions surged from USD 558.53 million in 2018 to USD 67.47 billion in 2022, further signified by how 98.9% of interactions in Australia have occurred online.

- Customer trust

- Branch closures pose additional challenges for remote communities that continue to depend on in-person interactions with banks.

- The closure of branches significantly impacts regional communities, as residents in these areas are compelled to travel considerable distances to reach their banks, resulting in additional financial burdens.

Malaysia shifts focus on digital-only banks

Neobanks have been disrupting traditional banks with superior customer experience, ease of use, and popularity among the younger generation, attracting a large customer base at lower acquisition and service delivery costs. Malaysia’s nascent neobank sector presents a significant opportunity for local banks to leverage, with a CAGR growth of 14.24% in transaction value between 2023 and 2027.

Bank Negara Malaysia (BNM) introduced a licensing framework for digital banks, aiming to enhance financial inclusion and serve the underserved population. This initiative aligns with Malaysia’s Shared Prosperity Vision (SPV) 2030, encouraging digital banks to innovate and offer targeted, personalised services.

In April 2022, BNM announced five digital banking licenses approved by the Ministry of Finance Malaysia. The licenses have been split into two categories and are given to the following consortiums:

- Financial Services Act 2013 (FSA):

- Boost Holding and RHB Bank Consortium

- GXS Bank and Kuok Brothers consortium

- Sea Group and YTL Digital Capital consortium

- Islamic Financial Services Act 2013 (IFSA):

- AEON Financial Service Co., Ltd., and AEON Credit Service (M) Berhad Consortium

- KAF Investment Bank Consortium

Out of the five, three have started their operations:

- Boost holding’s consortium released an embedded digital bank app to address financial inclusion gaps for the underserved and unserved.

2. GX Bank was launched as the first digital bank in Malaysia, and it currently offers a savings account and a debit card.

3. AEON financial services consortium is the first Islamic digital bank in Malaysia.

Philippines banks are revamping branches driven by digital growth and changing customer preferences

Despite the global trend of reducing physical branches, banks in the Philippines continue to expand their physical presence to reach underserved areas. However, the role of these branches has evolved, shifting from the traditional role of transaction processing, deposit-centric and inward-focused deals with what comes through the door to sales & service, product-neutral and outwardly looking acquisition-focused.

- Shift from transactional to advisory services

Digital banking has led to a drastic increase in online transactions, thereby reducing the need for physical branch visits.Hence, these branches are now focusing more on advisory services.

- Advisory focus

Includes managing financial planning, investment advice, mortgage consultations, and complex financial products. The face-to-face interaction in branches provides an opportunity to build stronger customer relationships and offer personalised services that are difficult to replicate digitally.

- Metrobank’s private wealth division provides comprehensive financial advice to high-net-worth individuals. They offer investment planning, estate planning, and wealth management strategies.

- BPI wealth offers personalised financial planning services to clients with investable assets. They focus on helping clients achieve their long-term financial goals.

- Enhanced customer experience

- Customer engagement hubs – Branches are being redesigned to serve as customer engagement hubs rather than mere transaction points. This involves creating welcoming spaces where customers can learn about new financial products and services, attend financial literacy workshops, and receive tailored financial advice.

- Union Bank of the Philippines is advancing customer experience through its Customer Experience Centre of Excellence (CX CoE). This initiative focuses on optimizing customer interactions and ensuring a seamless banking experience by leveraging technology and innovative practices.

- Community engagement – Branches are increasingly viewed as integral parts of their local communities. They host events, provide financial education, and engage with local businesses and community groups. These branches aim to strengthen their role and presence in the community.

- BPI foundation is dedicated to community development projects in education, healthcare, and environmental protection.

- Metrobank foundation focuses on education and youth development programs, including scholarships, livelihood training, and disaster response initiatives.

- Technological integration

- Smart branches – By equipping the latest technology, banks aim to streamline operations and enhance the customer experience. This includes self-service kiosks, digital displays, and AI-powered customer service tools. These innovations help reduce wait times and improve service efficiency.

- Metrobank introduced “digital onboarding centres” in some branches, enabling faster account opening and loan application processes.

- Omnichannel experience – The integration of branch services with digital channels ensures a seamless customer experience. For instance, customers can start a transaction online and complete it in a branch, or vice versa. This approach is crucial for meeting the expectations of tech-savvy customers.

- BDO launched “omni-channels” within branches, allowing customers to seamlessly switch between online banking and in-person assistance.

- BDO has integrated digital banking solutions with its branch network, providing mobile access, in-branch self-service stations, and universal machines. This approach aims to enhance customer experience by blending advanced technology with human interaction.

- Smart branches – By equipping the latest technology, banks aim to streamline operations and enhance the customer experience. This includes self-service kiosks, digital displays, and AI-powered customer service tools. These innovations help reduce wait times and improve service efficiency.

Thai banks are transforming how branches operate and serve customers

Thai banks are revolutionising their branch operations and customer service by embracing advanced technologies. This shift includes adopting hybrid service models that blend digital and in-person interactions, optimizing branch designs, and using data-driven insights to tailor customer experiences.

- Increased digital adoption

There has been a substantial increase in mobile and online banking services in Thailand. Digital payments have surged. Platforms like PromptPay have quadrupled their daily transactions from an average of 7 million per day in 2020 to 28 million per day in 2023.

- Hybrid banking models

Thai banks are moving towards a hybrid model that combines physical branches with digital services. Branches are becoming more focused on providing advisory and complex services while routine transactions are handled digitally.

- SCB has adopted a hybrid model by integrating digital services with physical branches. Their branches now offer more advisory and complex services, while routine transactions are handled online or via mobile apps.

- Branch design and experience

Many banks are redesigning their branches to be more customer-centric, offering a more engaging and interactive experience. This includes open layouts, self-service kiosks, and spaces for digital consultations.

- Kasikorn Bank – New branch designs feature open layouts with self-service kiosks and digital consultation spaces. This transformation aims to make branches more welcoming and efficient, allowing customers to handle simple transactions quickly while still having access to in-person advice for more complex needs

- Technological investments

Thai banks are increasing investments in machine learning, big data, and blockchain technologies to enhance their digital capabilities and improve operational efficiency.

- Krungthai Bank has been a frontrunner in adopting new technologies such as AI and big data. They use machine learning algorithms to analyse customer data, provide personalised financial advice and improve operational efficiency. This technology investment helps the bank stay competitive in a rapidly changing financial landscape.

- SCB has partnered with Sunline to modernize its IT infrastructure and core banking system, this upgrade will significantly enhance the bank’s transaction processing performance, including deposits and loans, by improving efficiency, security, and scalability

- Cloud computing

The strong push towards cloud-first strategies allows banks to be more agile and scalable in their operations.

- Bangkok Bank has adopted a cloud-first strateg7, moving many of its services to the cloud. This transition allows the bank to scale its operations more efficiently and provide better customer service. The cloud infrastructure supports the rapid deployment of new services and enhances the bank’s innovation ability.

South Korean banks building self-service capabilities for their customers

South Korean banks are significantly enhancing customer experience by investing in self-service capabilities. Emphasizing automation and user-friendly technologies, these banks are deploying advanced self-service solutions such as interactive kiosks, automated teller machines (ATMs), and digital platforms.

- Technological innovation

South Korean banks leverage AI, biometrics, and remote monitoring to personalise customer interactions, enhance security and minimise maintenance downtime. For instance, KB Kookmin Bank has launched 2 AI-based services to help modernise their branches.

- KB Kookmin Bank Smart Teller Machines (STMs) – An AI-based digital branch that can perform over 90% of the services traditionally handled by human tellers. These services include account opening, debit card issuance, and various transactions.

2. Liiv M – An AI-based mobile banking service that provides personalised financial advice and services through a conversational interface, further reducing the need for physical branches.

3. KB Kookmin Bank – The Bank has introduced the nation’s first kiosk-type “AI Banker,” developed in partnership with DeepBrain AI. This innovative solution leverages real-time interactive communication with AI technology to offer customers contactless service and personalised assistance providing information on banking services, financial products, and local conveniences, delivering a responsive and engaging user experience through video and voice synthesis.

- Self-service kiosks

To maintain customer service levels while reducing operational costs, banks in South Korea are increasingly deploying self-service kiosks. These kiosks provide various banking services such as cash transactions, account inquiries, fund transfers, and account opening processes.

- Shinhan Bank implemented “Digital Kiosks” to facilitate self-service banking. These services include loan applications, credit card issuance, and other banking transactions.

2. Woori Bank deployed “Smart Branches” equipped with ATMs that support contactless transactions and biometric authentication. Using QR codes and NFC technology, customers can perform transactions without touching the machines.

3. Hana Bank upgraded its ATM network with “Smart ATMs” that enhance functionalities. These include remote customer service assistance via video calls, diminishing the need for branch visits.

- Branch closures and digital shift

Many South Korean banks have closed branches and transitioned to digital platforms. This shift to being digital-first has led banks to optimise their branch networks and enhance their digital service capabilities.

- Hana Bank has been reducing its physical branch network, closing less profitable locations while upgrading remaining branches to serve more complex customer needs. They have also launched the “Hana 1Q” mobile platform to offer comprehensive digital banking services.

- NongHyup Bank is transforming its branches into community centres, where customers can access banking services and various community activities and educational programs. These branches are equipped with digital kiosks and offer workshops on digital banking to help customers transition to online services.

- The “Branch in Branch” concept – Digital kiosks and remote consultation services are provided within existing branches. This model enables customers to perform transactions and seek assistance without direct human interaction.

Chinese banks expand their rural reach with digital inclusion and deployment of mobile banking units

Chinese banks are transforming rural banking by adopting advanced technologies and innovative service models. Through smart branches, mobile banking units, and digital platforms, they are enhancing financial inclusion and revolutionising access to services in remote areas.

- Industrial and Commercial Bank of China (ICBC)

- Smart branches – ICBC has been rolling out smart branches equipped with advanced technologies like AI, big data, and facial recognition. These branches offer a variety of self-service options, reducing the need for traditional teller services.

2. Mobile branches – ICBC has introduced mobile banking units that travel to remote areas, providing essential banking services to customers who may not have easy access to physical branches.

3. Rural finance platforms – The bank is developing digital platforms tailored for rural customers, offering them a range of financial products, from basic savings accounts to agricultural loans.

- China Construction Bank (CCB)

- Village banks – CCB has established village banks in rural areas to provide localized banking services. These branches are equipped with self-service machines and digital platforms to facilitate banking activities.

- Digital finance – The bank is leveraging its digital finance platform to offer microloans and other financial products to rural entrepreneurs and farmers.

- Financial literacy programs – CCB runs educational programs to improve financial literacy in rural areas, helping residents understand and utilize banking services effectively.

- Agricultural Bank of China (ABC)

- Smart counters – ABC has deployed smart counters that can handle a wide range of banking services. These counters are designed to be user-friendly and efficient, cutting down on waiting times.

2. Rural branches – The bank is focusing on transforming its rural branches by introducing mobile banking units and enhancing digital infrastructure to serve remote areas better.

3. Rural financial service stations – ABC has set up numerous rural financial service stations that act as mini-branches, offering a range of banking services. These stations are often equipped with advanced technology to support digital transactions.

4. Mobile banking units – The bank uses mobile banking units to reach underserved rural communities, providing them with necessary banking services on the go.

- Bank of China (BOC)

- Smart outlets – BOC has been upgrading its branches to smart outlets, incorporating AI, blockchain, and other technologies to streamline processes and enhance security.

- Virtual banking – The bank is developing virtual banking services that allow customers to access banking services through virtual reality (VR) and augmented reality (AR) platforms.

- E-commerce platforms – The bank collaborates with e-commerce platforms to provide financial services to rural merchants and consumers, facilitating online transactions and payments.

Conclusion

The APAC banks are undergoing a significant transformation driven by technological advancements, evolving customer expectations, and strategic operational realignments. Banks are increasingly adopting digital solutions, modernising branch networks, and enhancing customer experiences to stay competitive. The future of banking will likely see a continued blend of digital and physical services, with branches evolving into advisory and community-centric hubs, supported by advanced technologies and personalised service models.

Research methodology and assumptions

- Data collection has been done based on secondary research about the information provided by the respective banks through their annual reports.

- For fair representation and analysis, we have considered a constant currency rate for conversion from local currency to USD value.

- The report analyses customer-to-branch, branch expense to revenue, and the number of branches for APAC banks.