OCBC is one of Singapore’s ‘Big 3’ banks, along with DBS and UOB. With more than 36 branches in Singapore, the bank offers customer service in 19 countries and regions. OCBC operates in six core markets: Singapore, Indonesia, Malaysia, China, Hong Kong, and Taiwan. The bank also has a presence in South Korea, the US, Australia, the UK, Luxembourg, UAE and Japan.

Financial highlights

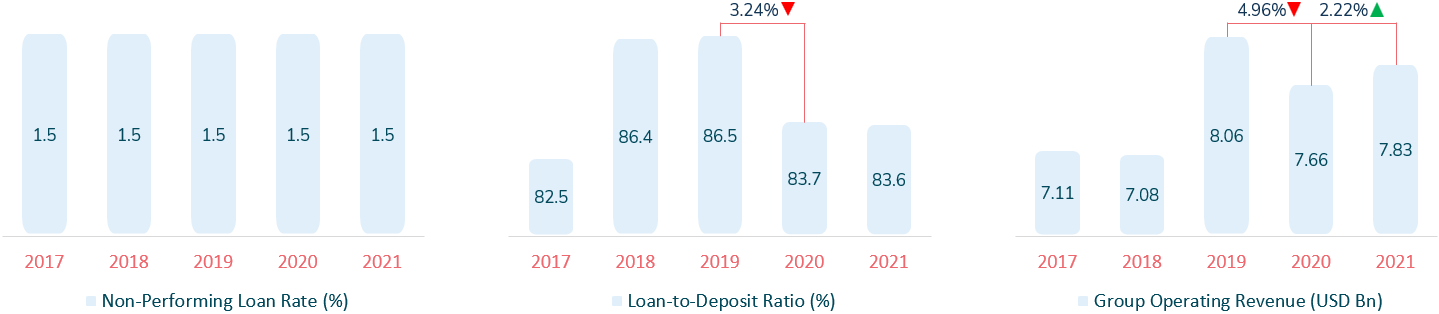

The NPL (Non-Performing Loan) rate at OCBC has remained constant despite the pandemic, signalling their loans are of quality. Similarly, the LDR (Loan-to-Deposit) ratio remained steady, even after it declined 3.24% the previous year.

Ideally, the LDR ratio should be between 80% to 90%. Currently, OCBC is on the lower end of the threshold and should strive to increase its loan disbursement to 90% or above. In addition, increasing the LDR ratio will also help OCBC improve its net interest margin, which has fallen almost 13% from its high of 1.77 in 2019 (Figure 2).

Singapore banks generally operate at high cost-to-income or cost efficiencies compared to banks in other regions in APAC. For example, Singapore banks reported a cost efficiency ratio of 57.96% in 2019.

In the case of OCBC, it reported a much lower cost efficiency ratio of 43% in the same year (Figure 2). However, since then, it has increased by 5.39%, with the bank operating at a cost efficiency of 45%. Still, indicators suggest that the bank is still able to operate efficiently.

Strategic focus areas

- #1 Geographic expansion

OCBC foresees growing trade, wealth and investment in Greater China as an excellent opportunity for expansion. And with a 20% (maximum allowed) share in the Bank of Ningbo of China, OCBC has used it to establish an enlarged footprint in the area. In addition, OCBC has ongoing strategic cooperation, creating an agreement with the bank to increase collaboration and interchange knowledge.

OCBC has signed multiple Memorandum of Understandings with the Bank of Shanghai and Guangfa Bank to strengthen collaboration and capture new opportunities. In October 2021, OCBC also partnered with Ping An Bank to maximise the newly state-approved cross-boundary investment scheme, which will allow residence of the Greater Bay Area. With this, OCBC can purchase approved schemes in China and vice versa.

This is forecasted to facilitate up to RMB 300 billion (SGD 63 billion) in total investment flows and generate about RMB 3.2 billion (SGD 670 million) in annual wealth fees.

- #2 Deliver differentiated and integrated CX

With customer experience at the core of OCBC, the bank has established a dedicated data department to provide customers with automated and personalised financial recommendations. This feature aims to help customers make better informed financial decisions.

Moreover, customers can view personal “insights” in their mobile banking app. For instance, someone with excess cash will be prompted to repay their loan to save on interest or deposit the excess into an interest-bearing account.

OCBC also launched “One Group” to drive customer experience, boost efficiency, extract synergies, and manage risks prudently and more effectively. The “One Group” program aims to promote collaboration within different geographies regarding banking, wealth management and insurance.

- #3 Becoming a technology company

OCBC Digital (the main mobile banking app), OCBC Pay Anyone™ (the lifestyle-oriented payment app), and OCBC’s online banking portal function to accelerate digital transformation. These platforms can be used independently or simultaneously and undergo regular updates are all updated regularly for a safe and competitive experience.

OCBC also dedicated its efforts to building ‘FRANK by OCBC’, a digital-first banking initiative that transforms traditional banking into an online experience. Customers interested in FRANK can apply for an account from the website and immediately start.

To learn more about FRANK by OCBC, check out this article.

On another note, cybersecurity is another avenue where OCBC has its full attention locked. Today, user protection and security is necessary to avoid scams and fraud. OCBC frequently conduct webinars to raise fraud awareness in the minds of their customers. In fact, OCBC prepared for the worst-case scenario – a kill switch. The kill switch works alongside a dedicated ‘fraud hotline’ for customers to freeze all their assets in the bank immediately in case of an unfortunate incident.

- #4 Shaping a climate-aligned future

OCBC is the first Singaporean bank to introduce the sustainability-linked structured deposit – an investment plan focused on sustainable development. In addition, with the introduction of ‘Eco-Care’ car, home, renovation loans and solar panels loans to encourage a sustainable lifestyle, OCBC proactively supports customers’ transition to a low-carbon economy. In 2021, it disbursed more than SGD 34 billion in sustainable financing and is targeted to grow the portfolio to SGD 50 billion by 2025.

OCBC is also actively reducing its environmental footprint. Currently, it is on track to achieve net-zero operational carbon emissions across the bank in 2022. It aims to achieve this by retrofitting properties with energy-efficient technology, such as LED lights and energy-efficient cooling systems.

OCBC also donated SGD 3.2 million for various social causes and helped deliver the government’s loan relief programs to individuals, SMEs and corporate customers during the pandemic.

- #5 Employee experience

As important as the customer is in business, OCBC also believes in treating their employees with the same level of care and attention. To demonstrate, OCBC developed the OCBC Future Smart Programme to equip employees with digital skills.

OCBC also regards employee welfare with a high level of care and attention to detail, with the bank providing vaccination support for the employee. The support encompasses transport, additional medical leave and work-from-home arrangements. OCBC also introduced a holistic wellness programme to better look after employees’ physical, mental, social and financial wellbeing.

On top of that, OCBC cares about the future state of the employees and their personal growth, establishing various internship and training programs for graduates to participate in and grow. A few examples are OCBC FRANKpreneurship for future bankers, OCBC Ignite for IT students and OCBC Regional Scholarship, a complete scholarship program.

To learn more about OCBC’s EX, check out this article.

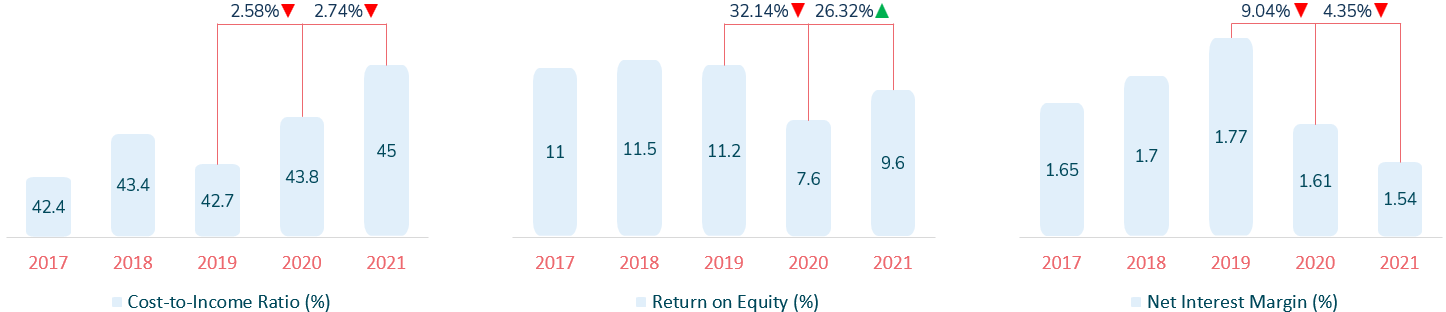

OCBC digital strategy

OCBC plans to deliver its digital strategy through the following (Figure 4).

OCBC technology innovation

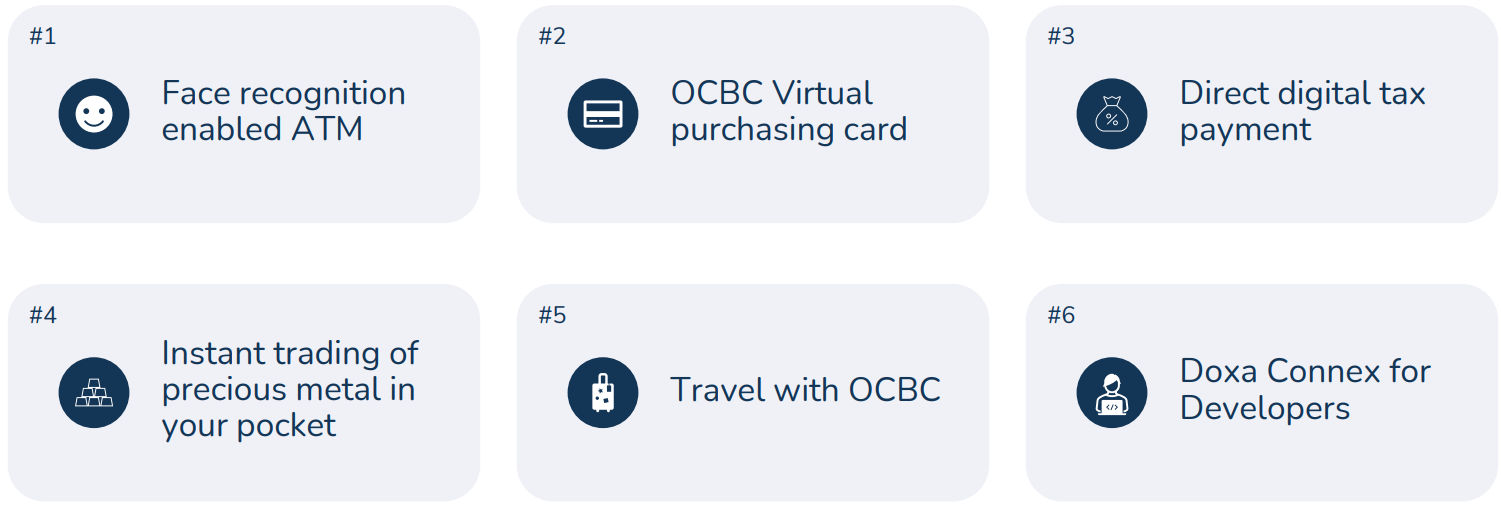

- #1 Face recognition enabled ATM

This initiative increases the security of the money withdrawal process while keeping the process convenient for the customer, ensuring customers would no longer need to carry their ATM cards.

- #2 OCBC Virtual purchasing card

OCBC virtual purchasing card powered by Visa Commercial Pay Mobile allows customers to generate multiple virtual cards for single-use or multiple-use purposes. The customers will receive their virtual Visa credit or debit within minutes by simply applying for one online. In addition, the virtual card will be available for usage via Apple Pay once the setup process is completed.

This feature would allow scenarios such as a company generating a temporary purchasing card for an employee or a parent generating a temporary card for their child.

- #3 Direct payment of taxes via digital banking

OCBC customers in Singapore can directly pay their income taxes either in an instalment basis or on a one-time basis via the OCBC Digital platform. This would allow customers to conveniently pay their taxes, check their tax-related information and even integrate tax planning into OCBC’s wealth management services.

- #4 Instant trading of precious metal in your pocket

Instant buy/sell precious metals with the OCBC Digital mobile app, where customers can open an account and directly trade precious metals without having to visit a physical branch. This feature is both convenient for customers and comes with no sales charge or custody fees.

- #5 Travel with OCBC

Travel with OCBC is an online hotel booking and travel platform that allow customers to find and compare hotel, taxi and airline services. OCBC 90°N Mastercard holders can also enjoy further rewards when booking on the platform.

- #6 Doxa Connex for Developers

Doxa Connex for Developers is a platform co-developed by OCBC, Guocoland and Doxa to provide the built environment with the first-to-market digital workflow solution. This platform aims to automate the procurement and payment workflow by connecting property developers with banks, consultants, suppliers and contractors. The platform would automatically handle data entry, invoicing, and cash flow management while unlocking new efficiencies and reducing errors in the process.

4 growth opportunities for OCBC

- #1 Open banking

OCBC currently has 41 Application Programming Interfaces (APIs) for developers to integrate into their applications. In 2016, OCBC was the first bank in Southeast Asia to launch a dedicated portal for APIs.

OCBC is one of the top leaders in Southeast Asia for open banking, with significant efforts in this initiative. Therefore, OCBC should continue to issue regular improvements and updates to the APIs while adding new APIs wherever suitable. Another recommendation from OCBC’s API forum is to improve the APIs by increasing the number of API call requests.

- #2 Buy Now Pay Later (BNPL)

OCBC has launched the ‘PayLite’ program for its credit card holders. With ‘PayLite’ being available exclusively to credit card users, this allows for flexible instalment repayment periods with no interest charge.

The next step for the bank is to expand the scope of the program to its current account holders. To help with the expansion, the bank should also reduce the substantial processing fee to increase its competitiveness in the BNPL market.

- #3 Banking Ecosystem

As of date, OCBC integrates its money management, wealth management, lifestyle and particular loan application platforms into its online portal. However, it is unknown if the data is shared across these businesses since there are no offerings or indicators. Regardless, OCBC’s diverse interest in multiple financial sectors, such as banking, wealth management and insurance, highlight the strong potential OCBC possesses with a banking ecosystem.

To begin, OCBC should focus on developing a super-app where customers can interact with all their financial products under OCBC Group that is simple and consistent in design. OCBC should also coalesce the customer data collected from the different business segments and use it to form one big data point to provide more accurate customer insights. These insights can be utilised to better serve the customer.

- #4 Smart contracts powered by blockchain

Currently, OCBC is developing a blockchain-based trade finance smart contract system that would reduce the reliance on paper-based documents. Going a step further, OCBC can expand their research and explore the use cases of smart contracts for more use cases, such as when dealing with internal documents, household consumers, and suppliers.

Conclusion

OCBC looks to be on top of sustainable growth by displaying significant efforts and investments. This level of assuredness is evident in their sustainable financing portfolio of over SGD 34 billion in 2021 and is targeted to further grow till 2025. Moreover, OCBC’s constant strive to advance, digitize and innovate its technology is evident in its 6 first-to-market initiatives, marking just how much OCBC understands the importance of technology to grow. Even so, there is still room for OCBC to flourish by improving its current open banking platform and BNPL offerings as well as creating a banking ecosystem. As OCBC advances, the bank should gaze its attention to speeding up the development and widening the use cases of smart contracts.