A. Introduction

Dedicated enterprise private networks have been in existence since the evolution of telecommunications. Industries such as railways, defense, public safety, and mining are some of the top vertical segments that immediately come to mind when discussing large-scale private networks. The low latency and high bandwidth capabilities of 5G, and the ability to deploy it in a private manner, present a whole new gamut of applications that can transform enterprises. This report reviews the progress/implementations of private 5G and LTE networks globally. We cover:

- Challenges and drivers

- Private network spending by 2030

- Readiness of the ecosystem

- Key market trends and developments

- Market positioning of various private network suppliers (MNOs, OEMs, Hyperscalers, SIs)

- Recommendations for various stakeholders

B. Understanding private networks- What is a private network?

The three key aspects of a private network include:

- Coverage– A private network is a local area network dedicated to devices and applications authorised by an enterprise. They are more reliable, secure and offer better network control than legacy networks. Private networks are also critical for remote places (mines, agricultural lands) where public network availability either does not exist at all or is not sufficient for advanced use cases and applications.

- Spectrum– Spectrum availability is critical for building a private network, whether LTE or 5G. The regulators in the respective countries provide the spectrum and set reserves of the same for both public and private use (enterprises). If there is no such dedicated spectrum available for the enterprise (own spectrum or via MNOs), then this is a roadblock in building a private network.

- Assets- Assets refer to the components of a private network technology stack. Private networks are categorised into standalone and non-standalone private networks, and these are based on network architecture arrangement and the ownership of network equipment. An enterprise either buys or owns all the required network assets, which requires significant CAPEX investment. As opposed to this model, enterprises can opt for an OPEX-based model, where the network is provided as a managed service.

To know more about private networks, read our primer report on private 5G fundamentals

C. Key drivers

Enterprise digitisation – The rapid move towards industrial revolution 4.0 is creating a need to adopt new applications and use cases that are more business and mission-critical, for which the existing legacy network features are not adequate.

Private 5G networks enable better security– Features such as security, reliability, coverage, mobility, and low latencies can help enterprises accomplish their desired goals in terms of efficiencies and profitability.

According to the ‘the Economist’s Impact Survey conducted in 2021’, 69% of the executives surveyed indicated network security as one of the most significant pain points, especially in manufacturing industries such as pharmaceuticals, life sciences, and healthcare.

Lower deployment costs with emerging business models – Private 5G increasingly aligns with a NaaS model approach, simplifying consumption and ease of deployment (from months to days). This is an OPEX-based model which focuses on pay-as-you-use and is combating the high-cost fear associated with building private networks.

D. Key challenges

There are many benefits with 5G in comparison to existing wireless or wired networks. However, enterprises do not want to give up on their existing legacy networks completely. They have invested significantly in applications and they need to be ported over. Integrating private 5G networks with legacy systems and networks is one of the biggest roadblocks to adopting private 5G. Enterprises have heterogeneous connectivity needs. Thus, considering a private network as the only offering might not be the apt approach for all enterprises. Integration becomes essential to cover usage across a large number of enterprises.

Lack of in-house skills to deploy private networks (4G and 5G) is the second big challenge. The complex nature of these networks demands highly skilled people who have relevant expertise. Most enterprises have just started gearing up for it. Also, 5G networks are more driven towards softwarisation, making IT expertise significant.

Higher upfront costs are a major challenge of private network deployment compared to Wi-Fi. Only a limited number of enterprises with financial strength have the ability to deploy these networks. The pressure of cost could be comparatively less in an OPEX-based model compared to fully owned on-premise networks.

Non-availability of a dedicated/reserved spectrum from the regulator or MNOs is another challenge. As opposed to this, the availability of spectrum spurs private network activity. We will discuss how governments of various countries are introducing spectrum for local networks later in this report.

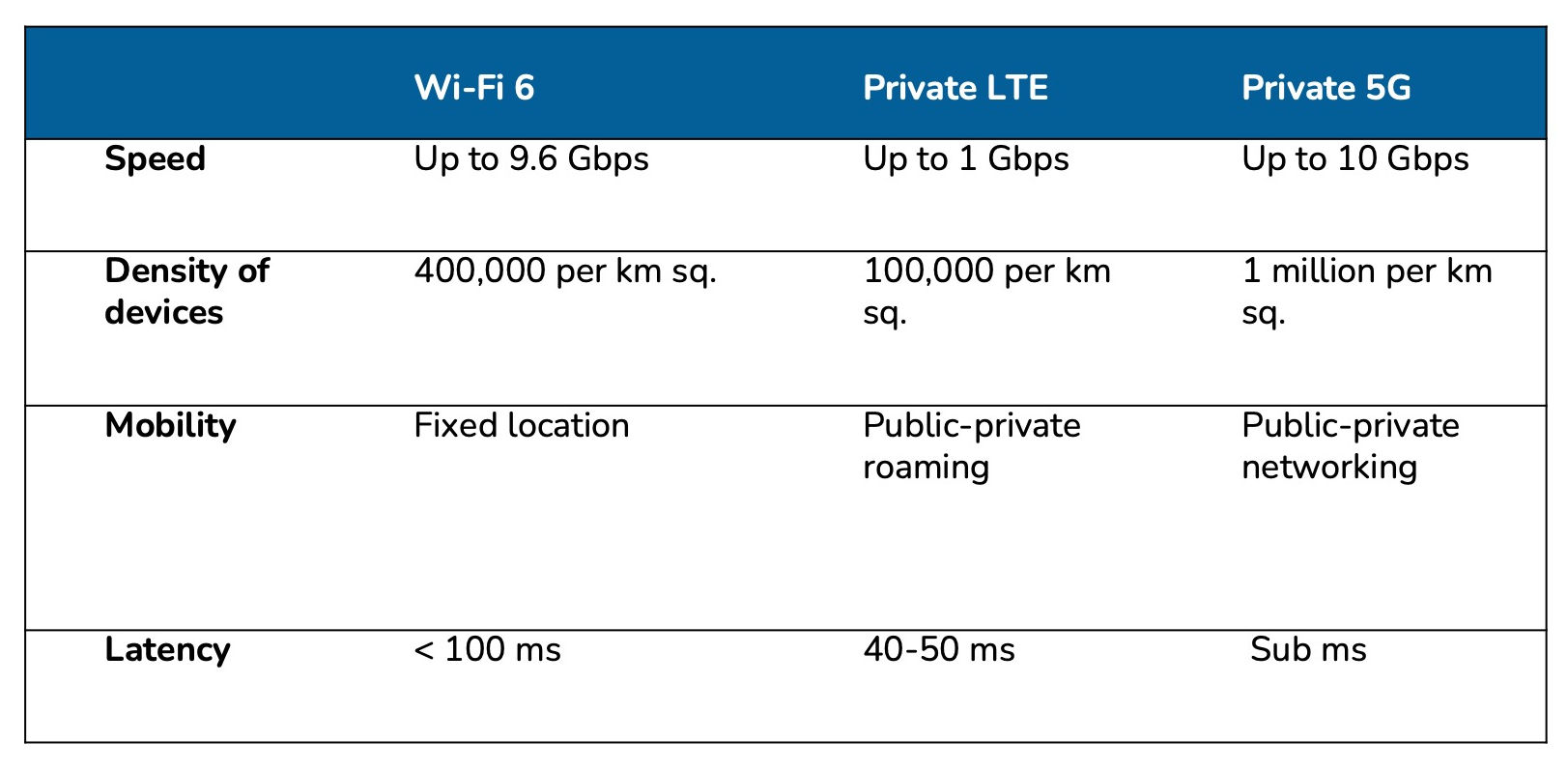

The emergence of Wi-Fi 6 and Wi-Fi 6E will limit some growth opportunities for private 5G /LTE deployments. For example, in the case of mostly indoor operations (communications are mostly internal), device density is not high, and applications are non-critical, Wi-Fi 6 would be sufficient. Therefore, deploying private networks is not a necessity but a good to have offering for these kinds of operations.

Table 1 shows the comparison of Wi-Fi 6 with private LTE and private 5G:

E. The market opportunity for private networks

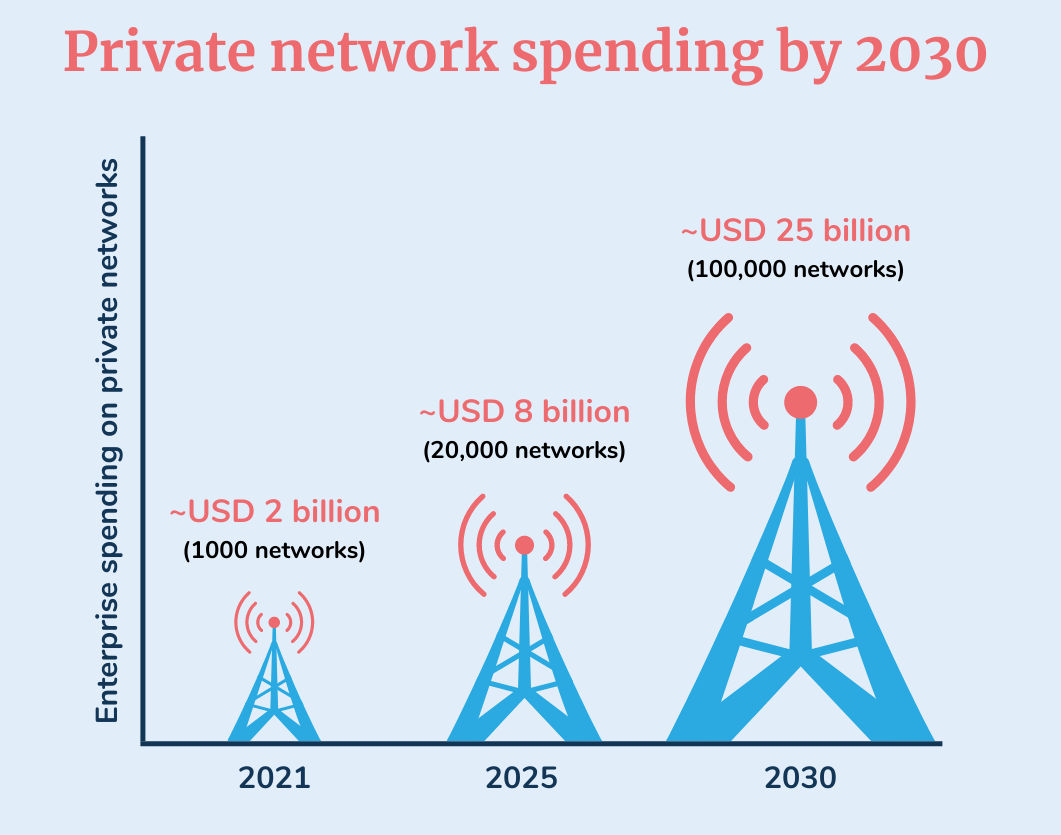

Figure 1 below shows the total spending by enterprises on deploying and running private networks:

- Between 2021 and 2025, enterprise spending on private networks will increase by an estimated 280%. During the last five years of this decade, the spending will jump at least 3X from 2025, leading to an estimated private network market of approximately USD 25 billion by 2030.

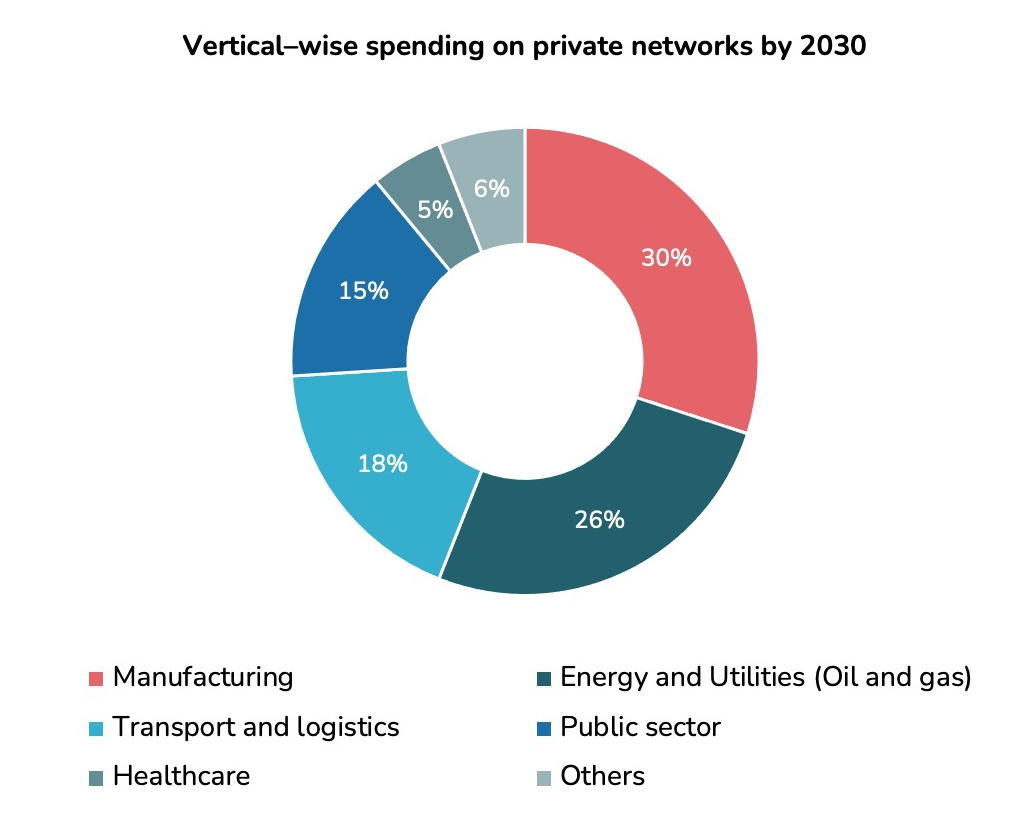

- Manufacturing, energy & utilities, and transport & logistics will be the leading vertical industries, accounting for 74% of the total enterprise spending on private networks by 2030.

- The number of private networks globally will also grow multifold from a few thousand in 2021 to over 20,000 by 2025 and approximately 100,000 in 2030. China will account for the bulk of these deployments.

- This increase is mainly due to the reduction in upfront costs of deploying private networks as more as-a-service business models will emerge to encourage the adoption of private networks with small and medium enterprises (SMEs).

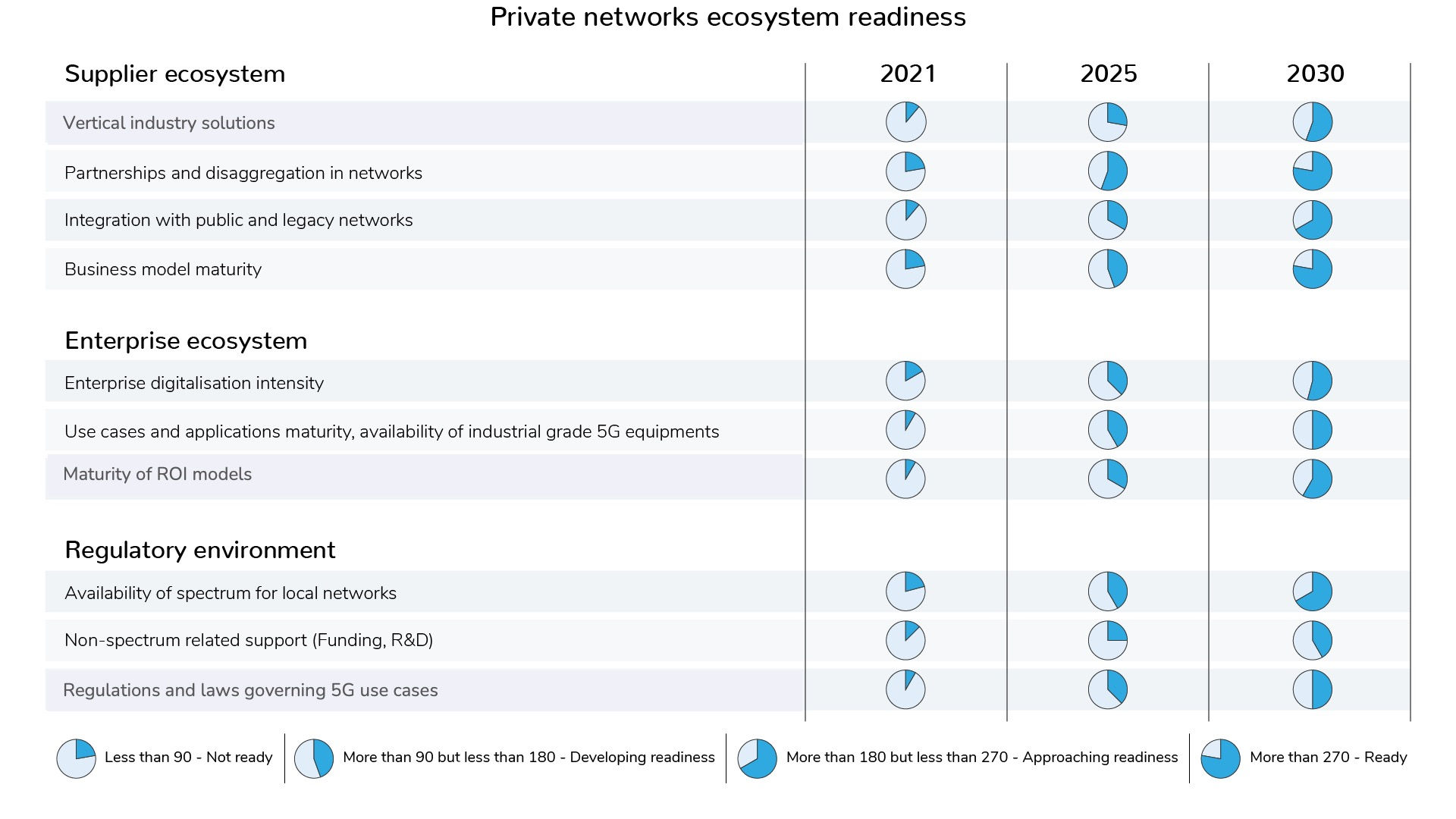

F. Private networks ecosystem readiness

The mature supplier ecosystem, improved buyer confidence, and supporting regulations will determine the adoption of private networks among enterprises. Figure 2 shows how these three drivers would shape the private network opportunity going forward

1. Supplier ecosystem

Vendors and MNOs have begun to acknowledge the need for developing bespoke industry-specific solutions to drive a wide-scale deployment of private networks. These bespoke solutions are largely built based on the nature of applications in a particular industry vertical. For example, a private 5G solution customised for ports might not be applicable for manufacturing or any other vertical. A one-size-fits-all approach would not exist since every enterprise will require certain customisations to meet its specific needs.

Disaggregation in networks is another aspect that makes the supplier ecosystem robust in the ability to provide cost benefits and flexibility. NaaS providers like AWS are into partnerships with equipment vendors to leverage Cloud RAN and Open RAN technology in developing these solutions. Open RAN, for instance, will also be highly embraced by large enterprises.

Private networks today lack interworking with the existing networks and public networks. Only a few suppliers have claimed the interworking of their private network solution with Wi-Fi. Ideally, private networks should co-exist with Wi-Fi 6, which might be the likely scenario as the technology matures going forward. However, the network-as-a-service model is yet to win the confidence of enterprises in terms of control, data privacy, security, reliability, SLAs, and other compliance matters.

2. Enterprise ecosystem

The enterprise ecosystem for 5G is still evolving. There is a limited development in the number of use cases with high economic value. Decisions for the deployment of private networks require clear business case and the demonstration of ROI for the investment. As the technology and business models mature, the ROI mechanism will be clearer. There is also limited availability of industrial-grade 5G equipment which is slowing adoption.

3. Regulatory environment

The availability of spectrum to build private networks is the most critical factor in terms of regulator support. How government perceives 5G for different enterprise verticals as a means to drive economic impact for the nation is an important metric and driver for the growth of the industry.

The availability of government support in terms of R&D and the formation of regulations for use cases (such as for autonomous vehicles) is also essential. Further, it is more likely that countries, where manufacturing and transport are the major contributors to the GDP, will see government support coming their way.

G. Key market trends and developments

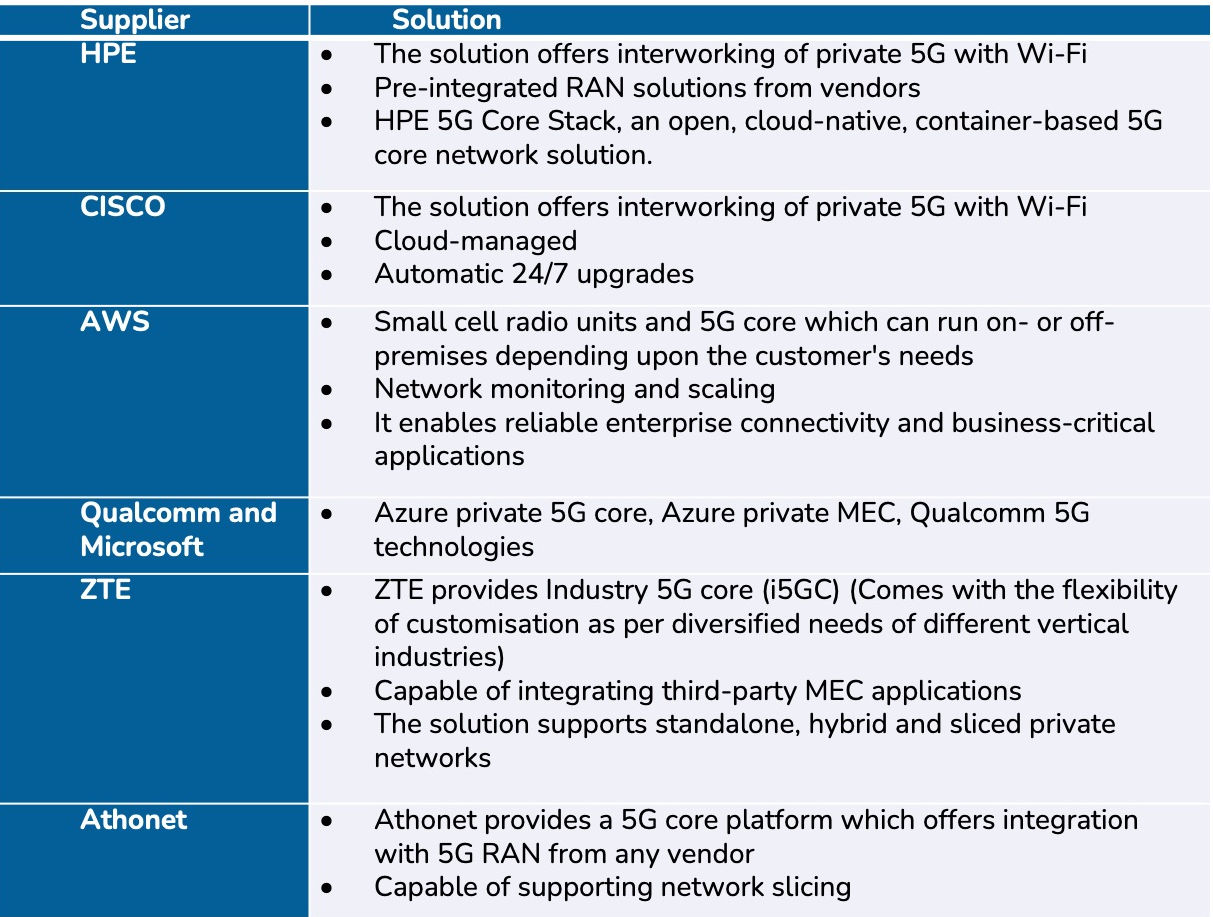

1. Suppliers are investing in building cloud-managed services solutions (NaaS) to ease the deployment of complex-natured private networks

- The network-as-a-service model of private 5G simplifies the procurement and deployment process, which allows customers to deploy private networks within days instead of months. They can also rapidly scale up and down the number of connected devices and benefit from a familiar on-demand cloud pricing model (pay-as-you-go). Customers only pay for the total network capacity and throughput they request for and are not charged per-device costs.

- With NaaS in place, the ecosystem of players in the private network space has broadened, especially for the non-traditional vendors. For example, in the US, telcos AT&T and Verizon partnered with Celona.

Table 3 shows private network (NaaS) offerings by various suppliers:

2. Manufacturing is leading the early adoption of private networks

- GSA noted a 117% increase in the private networks (pilots or deployments) in the manufacturing sector as of February 2022 compared to the beginning of 2021. Automotive companies looking to drive factory automation to dominate the private LTE/5G deployments in manufacturing. Factories are keen on private 5G due to its high-security feature.

- Manufacturing is in the lead, followed by the transport (ports), and utilities (mining, oil, and gas) sectors

- German regulator have issued a total of 120+ 5G spectrum licenses for private 5G campus networks, which is one of the key drivers for growth. Germany accounts for 5.3% of the global manufacturing GDP.

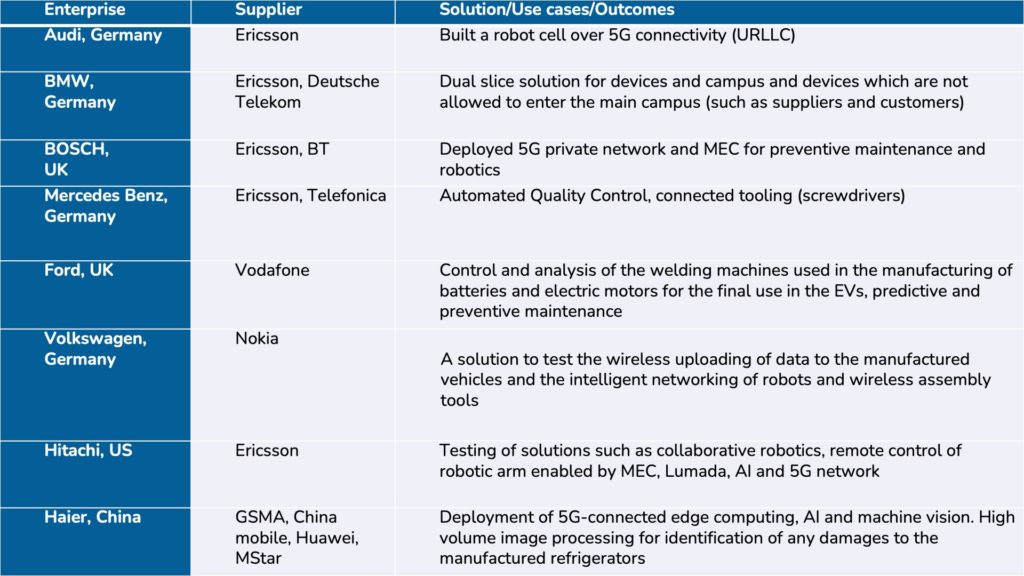

Table 4 shows some of the private network deployments in the manufacturing sector:

3. A few enterprises (manufacturers) are building their own network gear

- Siemens and Foxconn are examples of enterprises building their private network gears without traditional network equipment vendors. Siemens has built LTE private network in its factory in Wisconsin using its own evolved packet core alongside Air-span small cells. Foxconn has also built its own 5G small cells (in partnership with Yageo Group).

- A year ago, Siemens announced building a private 5G in its plants using its independently developed network products and solutions.

4. Industrial spectrum, a key component to spur the adoption of private networks

As discussed before, the non-availability of spectrum for local network usage could be a serious issue for enterprises aiming to have control over the network. Countries that have taken steps to allocate spectrum for industrial use have seen growing interest to think, pilot, and deploy private networks for their operations. Below are some notable examples of countries where the industrial spectrum is made available by the respective regulatory authorities:

- Germany

The German regulator allocated spectrum in the 3.7-3.8 GHz category. It charges fees to ensure the optimal utilisation of the spectrum. The fee amount depends on the bandwidth and the size of the area covered.

Large industrial enterprises, airports, trade fair organisers, universities, and research institutes have shown the most interest, while only a small number of telcos applied for the local licenses.

- France

The government of France provided a spectrum in the 3.8-4.0 GHz category. Besides spectrum allocation, the government of France is also taking other steps such as inviting expression of interest in specialist 5G industry zones. In a joint effort with Germany, the government of France will also invite industries that have identified use cases.

- UK

Ofcom will charge an average annual license fee of £320 (approx. USD 337), based on a 40MHz holding. It calculates £80 per 10 MHz in all bands, except 1800 MHz, which will be available at £80 for 2 x 3.3 MHz. The licenses will be valid for three years, as default, and may be revoked if not in use with one month’s notice. Spectrum is provided in 3.8-4.2 GHz 2.6 GHz, 28 GHz bands.

- Japan

The MIC allocated these bands to private and public organisations, including Fujitsu and Toyko University. The spectrum band categories offered include 4.6-4.8 GHz 28.2-29.1 GHz.

- South Korea

An announcement was made regarding additional spectrum allocation to both telcos and non-telcos in Sub-6 GHz and 28 GHz bands. This move is in alignment with South Korea’s 5G plus strategy.

- US

CBRS spectrum is available to enterprises for incumbents (government agencies, satellite services) and enables them priority access license (private networks for enterprises), and general authorised access caters to public devices. CBRS is available in the 3.5-3.7 GHz category

H. Key roles and core strength areas of various suppliers of private networks

- MNOs- Private networks, when combined with edge computing, can offer a range of benefits to customers. Some mobile network operators are focusing on integrating and co-creating edge solutions with hyperscalers. Partnerships are necessary to help provide integrated solutions which are an important pre-requisite for private 5G solutions, which is more than just the conventional connectivity. Verizon, AT&T, Telefonica are some telcos that have collaborated with hyperscalers. The role of MNOs becomes limited if an enterprise directly owns a spectrum from the regulator and doesn’t have to depend on a service provider. Therefore, tapping into such solutions and partnership strategies is essential for telcos.

- Network equipment vendors- Network equipment providers lead the private 5G ecosystem by being the main contractors in private network deals. Vendors are part of a majority of the deals. They deploy and sell private solutions both with or without network service providers. Vendors like Nokia use service providers as one of their key distribution channels to sell their solutions to enterprises.

- Hyperscalers- Hyperscalers have come up as disruptors in the private networks space with their cloud-managed network as a service solution. These offerings promise to overcome the top two challenges of deploying private networks viz; high upfront cost (CAPEX) and the complexity in deploying networks which require a highly-skilled workforce that can both deploy and manage these networks. Hyperscalers are also focusing on building vertical-specific solutions. Computing capabilities are their core strength, which they are leveraging to build private 5G network solutions.

- System integrators – With multiple entities such as CSPs, vendors, and SaaS companies playing their different roles in private deployments, there is a need for a single entity that can bring together the capabilities of all of these entities. System integrators are responsible for service level agreements (SLAs) between the enterprise and entities deploying a private network. Their core strength is the ecosystem of diverse partnerships.

I. Recommendations

Solution providers

- Developing a strong industry-specific value proposition is key to success. Partnerships with companies across the value chain are important to help serve the client’s needs.

- There is a need to demonstrate use-cases, build client confidence, and help enterprises build the business case.

- Flexibility in the choice of business models will be needed for customers. They could opt for outright purchase, managed service or build-operate-transfer models.

- Addressing inter-operability will support the scalability of initiatives. Large enterprises will require solution providers to leverage existing investments and migrate to new networks over a period of time. They will need to port existing applications over to the private 5G environment.

- Security should be an integral part of the offer as it is an area of great concern and limited knowledge for most companies when transitioning to 5G.

Buyers

- Define business objectives (bringing innovation, improving efficiency, or shift in business model) and use cases to make a better choice between Wi-Fi, private LTE, or Private 5G.

- Give due attention to cyber security when deploying private 5G networks which are based on software-defined digital routing. This leads to more vulnerable threat points. Enterprises should consider solution providers offering security solutions built into the network layers themselves more favourably over others. The vendor providing products and services for managing security risks associated with deploying 5G as a value add is also advantageous to the enterprise.

- Deciding between private LTE and 5G is a tough choice for many. The right choice of network technology is not necessarily the latest technology. Despite this, one must keep itself prepared for the transition to 5G to meet its future needs.

- Focus on building a competent workforce to have better control over private networks. It will reduce the dependence on the channel partners or suppliers.