Company Insights

twimbit Purpose Index

Public Bank (Group financials) – An overview as of 31st December 2020

| Bank name | Public Bank Group |

| Headquarters | Kuala Lumpur, Malaysia |

| Operating revenue (31st December 2020) | USD 5.01 billion |

| Net profit (31st December 2020) | USD 1.2 billion |

| Total Assets | USD 102.53 billion |

| Employees | 19,000+ |

| Country of operation | 7 |

| Number of branches (Global) | 406 |

| Information and communication technology (ICT) spend (31st December 2020) | USD 14.1 million* |

| Bank ranking in the particular country | 3rd in Malaysia |

| Number of customers | 9 million |

| Market capitalisation (31st December 2020) | USD 19.74 billion |

| Operating revenue CAGR growth (2016-2020) | 0.19% |

The conversion rate used 31 December 2020, 1 MYR = 0.24689 USD

Shareholder value (31st December 2020)

| Return on Equity (31st December 2020) | 11.2% |

| Total Shareholder Return (1-Year) | 19.5% |

| Net Income Ratio | 43% |

| Common Equity Tier 1 Ratio | 14% |

| Price Earnings Ratio (31st December 2020) | 15.93% |

Awards

| 2020 | Best e-Payment Bank at the Malaysian e-Payments Excellence Awards Best Customer Experience (FPX) at the Malaysian e-Payments Excellence Awards |

| 2019 | Forbes-Global 2000 World’s Best Employers Best Bank in Malaysia by Alpha Southeast Asia Best Bank for Corporate Governance by Global Banking & Finance Review |

Public Bank Group and its strategic focus areas

- Business segment

- The group is promoting special financing schemes initiated by the Government and Bank Negara Malaysia to assist SMEs in overcoming COVID-19 challenges. Underpinned by its proactive initiatives, the group approved more than USD0.83 billion for over 16,000 SME businesses under these special financing schemes.

- In addition, their non-interest income grew in 2020, majorly contributed by higher investment and stockbroking income, as well as higher income from its unit trust management business undertaken by Public Mutual, the group’s wholly-owned subsidiary. During the year, Public Mutual recorded profit growth of 10.5% and maintained its leading market position, with the highest market share of 33.4% in the retail private unit trust industry.

Wealth Management

The bank’s focus is to sustain the leading market position for the private unit trust business by:

- Offering superior services to customers and diversifying the product range through its Red Carpet Banking (RCB). It aims to serve emerging affluent customers by providing personalised wealth management services and attractive benefits through RCB-exclusive campaigns.

- Developing new insurance and investment products as part of managing customer wealth with AIA Group Ltd (“AIA”).

Transactional Services

- Public Bank Group also continues to explore and implement innovative digital solutions, particularly on advancing its e-payment capability to enhance operational resilience and customer experience.

Capital Market Operations

- Continue to focus on commercial foreign exchange revenue

- Continue to grow the existing corporate portfolios and acquire new, targeted corporate clients

- Continue to develop retail and institutional customer bases in the investment banking space

International Operations

- Increase contribution obtained from overseas operations in Hong Kong / People’s Republic of China and Indo-China through organic growth

Initiatives already taken by Public Bank Group to expand its business segment in 2020-2021:

- In 2020, new RCB customers grew by more than one-fold to over 24,500. The average product holding per RCB customer improved to 4.76 products from 4.17 products in 2019.

- In 2020, total deposits via RCB exclusive campaigns amounted to USD1.74 billion.

- Public Bank Group and AIA entered into its eighth year of strategic bancassurance partnership in 2020. The bancassurance business continues to be one of the main fee income generators for the bank. It promotes and provides customers with a comprehensive array of bancassurance products.

- Public Bank Group, in collaboration with AIA, launched the following products in 2020:

- PB Elite Signature: A new regular premium investment-linked product, targetting markets with emerging high-net-worth customers

- PB Smart Elite: A single premium investment-linked product, offering insurance coverage linked with two of the AIA Elite Funds series, suitable for investment-oriented customers

- PB Major Illness Care: Provides comprehensive major illness insurance coverage to customers

- AIA Strategic Fund Series: Provides customers with potentially higher returns through exposure to foreign markets

- The Public Bank enterprise corporate online banking platform is now enhanced to provide additional features that help businesses improve their cash management further. Features include frictionless e-payment transactions via Financial Process Exchange, virtual accounts for collection payment acceptance, uploading recurring payment instructions, requests for cheque books, and stop cheques.

- In recognition of the bank’s efforts and commitments in driving e-payment in Malaysia, Public Bank received eight awards under the Malaysian e-Payments Excellence Awards (MEEA) 2020 from PayNet.

- Due to the COVID-19 pandemic, Public Bank Group, in collaboration with Western Union, launched the “Western Union 50% Service Fee Discount Promotion” from 30 April 2020 to 30 June 2020:

- The campaign offered a promotion code of 50% discount on service fees for customers who send money using Western Union via PBe.

- Customer experience

Public Bank Group plans to enhance customer experience by increasing the efficiency of its service delivery in every aspect of its business. The bank intends to develop innovative banking products and services that suit its changing customers’ needs:

Serving the customer

- Provide top-notch customer service, in line with the bank’s corporate tagline, “Excellence is Our Commitment”.

- Promote e-payment and other digital banking services to attract millennials.

- Customers can also interact through mobile applications or visit the website for their needs. These measures allow the bank to stay connected with customers without the need for physical interaction.

- For SME customers, they offer moratoriums and targeted assistance packages to help them get through any cash flow situation.

- Maintain effective partnerships with banking and non-banking partners to develop personalised banking products, while keeping in mind that the needs of the customer changes as they progress financially.

Channel Management (Omnichannel experience)

- Serves customers through a multi-channel network, comprising of branches, self-service terminals, and digital channels, which include mobile, internet and social media platforms.

- Customers can utilise the bank’s self-service terminals and have access to services such as loan applications, deposits, remittances, and card services at all times.

Product Innovation

Public Bank Group designed the Public Bank (PB) Journey Programme to assist and support customers from all groups, i.e., students, graduates, families, or retirees, among others. The design was to aid customers in riding through these testing times. The Journey Programme intends to support the financial needs of various groups of customers through:

PB Journey SME Assist, which supports SMEs that are adversely affected by the COVID-19 pandemic

PB Journey Golden Savers Campaign

- Targeted at senior citizens who depend on a fixed income for their daily needs

- Assisting the elderly customers by providing higher fixed deposit interest rates with monthly interest payments

- Offering cash rewards for elderly customers who register for PBe internet banking and perform online banking transactions

- Providing promotional fees for signing up Will and Wasiat Services

PB Journey Junior Savers Campaign

- Targets customers below the age of 18

- Aims to encourage parents to continue saving for their children by offering promotional interest rates for fixed deposit placements

- Offers cash rebates for the first year’s insurance premium for selected bancassurance products to assist parents in providing insurance protection for their children

PB Journey Wealth Builders Programme

- Offers higher bonus interest to inculcate a disciplined savings habit among fresh graduates and young professionals

- Offers cashback for retail purchases using Public Bank debit card for disciplined savings

- Provides attractive benefits for customers who apply for the PB Quantum Visa Credit Card

PB Journey Family Wealth Boosters Programme

- To encourage customers in a family to save together as a family by offering attractive cash rewards

PB Journey EzPay Home Financing, a home financing product with a lower initial financial commitment

Public Mutual

- Public Mutual Online (“PMO”), an investor platform, was improved to enable investors to get an overview of their investment portfolios based on fund categories, geographical regions, and schemes.

- The improved fund analytics feature provides investors with daily updates of the bank’s funds’ performances over various durations, including the year-to-date performance, fund details, and fund prices.

- Public Mutual also introduced the Pocket-PMO application, a mobile application that offers investors the ability to access their investment portfolio, perform transactions, and conduct fund analytics at their fingertips.

Initiatives already taken by Public Bank Group to enhance customer experience in 2020-2021:

- Public Bank Group has established a Queue Management System to monitor and manage the efficiency of its counter service. The bank strives towards 80% of its frontline customers served within two minutes for simple banking transactions.

- It developed Public Mutual Online (PMO), a one-stop online platform. PMO allows subscribers to update their profiles, invest, make transaction requests (such as the switching and redemption of units), and enquire about their investment accounts.

- In addition to the expanding branch network, which has reached a total of 264 domestic branches, the bank has opened two new Red Carpet Banking Centres to provide more personalised and tailored advice, specifically for high net-worth customers.

- Public Bank Group implemented a Business Continuity Plan (BCP) for uninterrupted customer service and product delivery.

- Risk management

With liquidity coverage ratio (LCR) and implementation of the Net Stable Funding Ratio, the bank chooses to focus on their core deposits’ growth. The Group’s gross impaired loans ratio stood at 0.4% at the end of 2020, compared to the banking industry’s gross impaired loans ratio of 1.6%The bank’s end goal is to safeguard the deposits market share while exercising prudence in their cash flows. The bank undertook an annual capital plan over the medium-term horizon of at least three years, taking into consideration the following factors:

- Internal Capital Targets for the bank and their entities are subject to stress tests that readjust the banks’ internal capital adequacy requirements beyond the prescribed legal limits.

- Recalibrating capital demand for business strategy and material risks based on the bank’s risk appetite and in compliance with Basel III liquidity standards.

- Reassessing the availability and composition of different capital components by taking into account the market’s evaluation of bond yields, rating agencies’ assessment of financial health and creditworthiness, as well as the country’s level of accessibility for any debt issuance.

Initiatives already taken by Public Bank Group to improve its risk management practices:

- Introduced Regular Investment Authorisation (RIA), which allows investors to spread out risks associated with a single large investment. RIA happens by switching a pre-determined number of units from the bond/sukuk/fixed income/money market funds into equity/mixed-asset/balanced funds at pre-selected intervals.

- To facilitate a more objective credit assessment, the bank has an internal statistical-based credit scoring system that enables credit officers to quantify the risk involved better, hence helping to determine the creditworthiness of loan applicants.

- Regional expansion and integration

In recent years, Public Bank Group has been actively expanding its business in the Indo-China region, particularly in Vietnam, capitalising on the favourable economic environment in the region. Whilst its Indo-China operations registered strong performance, the Hong Kong operations were affected by unabated social unrest. Public Bank Group could:

- Focus on commercial foreign exchange revenue to improve the bank’s share in the international arena

- Continue to grow their corporate portfolio and acquire new clients, and grow the retail and commercial customer base in the investment sector

- Enhance contribution from overseas operations in Hong Kong/People’s Republic of China and Indo-China through organic growth

- Society and planet impact

The bank plans to embed the environmental consideration into its banking by quantifying their energy consumption, waste disposal and atmospheric emissions, thereby measuring their environmental footprint and gauging the impact of their efforts. Public Bank Group has:

- Proactively encouraged the migration to electronic payment using digital reports and documents to avoid unnecessary paper consumption and waste generation.

- Installed solar energy in the building and harvested total solar energy of 55,600 kWh, which helped them reduce their electricity consumption.

Climate Change

The Public Bank Group adopts the BNM (Bank Negara Malaysia) Climate Change and Principle-based Taxonomy guideline to facilitate the identification and classification of the Group’s business activities, based on their impact on the wider ecosystem.

ESG Lending Exclusion List

The Public Bank Group issued its ESG Lending Exclusion List, which consists of activities that the Group shall refrain from financing. The list is to strengthen the Group’s lending practice further and promote a sustainable environment and future for the wellbeing of the broader economy.

Value-based intermediation (VBI)

Advocated by BNM, VBI aims to align Islamic finance business models towards realising the objective of Shariah in generating a positive and sustainable impact on the economy, community and environment. In its product development process, PIBB considers not only customers’ needs but also embeds VBI values that bring positive impact to the wellbeing of customers, society, and the environment as a whole.

Investing in green energy

In line with Malaysia’s National Green Technology Policy, the Public Bank Group is supportive of the Government’s Green Technology Financing Scheme (GTFS). This scheme is available to domestic companies and entrepreneurs involved in green technology projects. Combining GTFS and GTFS 2.0, the Group has approved more than USD4.19 million to companies investing in green resources and technology.

Some initiatives already taken by the bank to foster environmental sustainability:

- Appointed e-waste vendors licensed by the Department of Environment and certified with relevant ISO standards in Environmental Management System to manage its e-waste.

- In Cambodia, the replacement of lighting with LED bulbs in their building helped reduce its electricity consumption by almost 50%.

- Energy Efficient Vehicles (EEVs) Campaign – In April 2020, PIBB rolled out a campaign offering exclusive financing rates, which were as low as 2.20% per annum with tenure up to nine years, to purchase selected energy-efficient vehicles.

- Solar Plus BAE Personal Financing-i – In November 2020, PIBB launched the Solar Plus BAE Personal Financing-i, which offers attractive financing packages for households looking into installing a rooftop solar panel.

- Campu Bank (Cambodian Public Bank), a subsidiary of Public Bank Group, offers financing to private water and electricity producers to expand their power grid and water supply. Campu Bank also refrains from extending loans to borrowers involved in sand dredging and timber logging. For its overseas operations, Campu Bank achieved 50% lower electricity consumption in its headquarters located in Campu Bank Building, Phnom Penh, following the complete replacement of all lighting with LED lights.

- Employee experience

The bank continued to initiate steps to ensure the relevance and competency of staff as required of their job scope and their readiness for future challenges:

- Inculcate a conducive, inclusive, and dynamic workplace where their employees are valued, respected, and empowered.

- Promote good staff morale through proper staff training, development, and the provision of opportunities for career advancement

- Promote their staff’s well-being through attractive remuneration and fringe benefits

- Push forward for an inclusive and diverse workplace

- Upskill employees through enhancement programs and initiatives to widen their knowledge and skillsets

- Offer sponsorships to encourage employees to take up self-learning courses

Initiatives taken by Public Bank Group to upskill their staff:

- In 2019, Public Bank Group had once again recorded the highest number of graduates for the banking qualifications offered by the Asian Institute of Chartered Bankers.

- In 2019, the group undertook a bank-wide skills gap analysis to assess staff competency and identify their skills gap. The assessment had facilitated the formulation of more effective training plans with the target to develop and enhance specific skill needs of staff.

Digital Strategy

Public Bank Group is mindful of staying relevant amidst the fast-changing environment. The bank developed a three-year digital roadmap as a subset of the group’s long-term strategic plan to respond to changing customer needs. The three-year roadmap focuses on the following areas:

- Adopting new technologies & industry standards such as Open API (Application programme interface), Artificial Intelligence and Machine Learning, industry standards for governance, business alignment, software development and security.

- Seeking technology partnerships for specialising in expertise or advanced technology unavailable in-house via smart partnerships with fintech, bank, and non-bank players.

- Training and developing staff to prepare them for Industry 4.0 through classroom training and mobile learning on-the-go, as well as professional certifications.

Initiatives already taken:

- Launched the PBe QR, Malaysia’s first universal QR payment acceptance riding on DuitNow QR, which provides businesses with the convenience of displaying just one QR code to receive payment from their customers through mobile applications.

- Launched Ask Sara, a virtual assistant with more than 700 questions for easier onboarding of customers by sales staff.

- Launched the updated PB engage mobile banking application with new features, such as device binding, face identification, and future-dated financial transactions.

- Launched PB Direct, an online insurance application.

- In 2019, Public Mutual launched a new digital initiative, Digital Onboarding, which enables new investors to onboard almost instantly and unit trust consultants (UTCs) to service a more extensive investor base. It reduces the hassle of submitting physical forms.

- Upgraded the security infrastructure to provide additional defence against the growing risk of cyber threats with the increase in adoption, as well as the usage of online and internet banking services.

IT Strategy

Public Bank Group is aware of the changing atmosphere in the banking needs of their customers. The group invested USD 148 million in IT-related capital expenditure and USD 22.2 million in fintech-related initiatives as a part of their 3-year digital roadmap. They have implemented some of these measures as a part of their IT strategy:

- Staying cyber resilient by designing a resilient cyber framework, security-by-design principles, constant upgrades to the ICT infrastructure, and strategies for rapid breach detection & recovery.

- Prioritising internal software development, in-house technology ownership, internal capabilities for innovation & service differentiation and adopting mobile-first design strategy and agile development methodology. These prioritisations increase business agility and corporate standards for governance.

- Observing ICT cost optimisation by investing in private cloud infrastructure, robotic process automation, and software customisation to optimise ICT resources.

Initiatives already taken by Public Bank Group to develop a resilient ICT infrastructure:

- Pilot launched fintech microsite, revamped with an Open Application Programming Interfaces (API) testbed environment. It enables third parties to connect with the Group’s open data, allowing for speedier system integration.

- In June 2019, the Public Bank Group piloted UnionPay International (UPI) QR Code Payment acceptance and became the first such acquirer in Malaysia.

- To further drive sales and increase e-Commerce acceptance platforms, Public Bank Group launched the CyberSource e-Commerce Payment Gateway Services in November 2019. This payment management platform facilitates and streamlines payments for online transactions.

- Revamped the hire purchase delivery system using the latest Agile Development to improve the user interface.

10 Growth and Innovation Opportunities

- #1 Cost to serve

- Public Bank Group had a cost to income ratio of 34.6%. Although well below the industry average of 44.7%, the bank’s cost-to-income ratio has been increasing at a compounded annual growth rate of 1.59% from 2018 to 2020.

- The bank’s personnel cost, which accounts for 34% of their total income, is 27% higher than its regional competitors. The bank can control its personnel cost by:

- Optimising iterative back-end tasks by using cognitive-process automation to save man-hours and increase efficiency.

- Automating front-desk customer query handling by upgrading virtual assistant capabilities to accommodate a broader range of customer complaints

- The bank suffered significantly on the operational front due to poor net interest margins, OPR (overnight policy rate) reductions, and a one-off net modification loss of USD 122 million to provide aids and assistance to individuals and businesses.

- A 1.6% growth of operating profit to USD 1.82 billion in 2020 from USD 1.8 billion in 2019 was adversely affected by higher ECL (estimated credit losses) provisions set aside to account for increased impairment charges due to the COVID-19 pandemic.

- The bank can optimise its operational model by focussing on the following areas:

- Expanding its data analytics capabilities to incorporate real-time risk monitoring of repayment risks.

- Continuing to leverage on its non-interest income and loan and deposit growth to balance out the negative effect of poor net interest margins and OPR reduction.

- Solidifying and expanding its Islamic banking business, which represents 11.6% of the bank’s total net income in 2020, and continue to be one of the main drivers of its net income.

- #2 Transformation of the branch and its branch networks

- The bank infrastructure cost contributes 18% to the total operating costs, mainly from the upkeep and setting up of 406 branches and 2000 self-terminals. The bank has significant room to streamline its physical footprint and go for a robust digital branch outlook in line with their 3-year digital roadmap.

- By restructuring the branch model, Public Bank Group can attract the young and growing millennial population, who are tech-savvy and enjoy gamification to transact with the bank. The restructure will also help the bank strengthen their red-carpet banking centres, which provide tailored advice and services to its high net-worth customers.

- The bank should focus on the following branch transformation themes to optimise its overall operational model:

- Building an omnichannel banking platform by migrating sales and transactions to digital channels and offering personalised and face-to-face customer advice on complex financial products at their retail outlets.

- Employing interactive teller machines (ITMs) with multi-language support in remote locations instead of building flagship retail branches, thereby optimising their physical footprint and maximising customer reach.

- Introducing self-service and community spaces (for example: cafes, lounges, etc.) within existing branches, hence reducing reliance on front desk channels of customer interaction and engagement.

- #3 Customer experience

- As a part of enhancing their customer service delivery quality, the bank should focus on developing its omnichannel experience by creating a phygital (physical + digital) customer interaction environment through:

- Improving its digital banking application, PB Engage, by integrating customer analytics capabilities:

- This improvement enables the bank to contextualise insights on the customers’ interests and preferences from continuously monitoring their saving and spending patterns.

- Developing a virtual assistant who can handle front-end customer grievances and is capable of handling using the region’s local language.

- Gamifying money management tools to build an immersive customer experience.

- Introducing virtual cards to improve customers’ buying abilities without compromising on transactional security and customer trust

- To develop and launch targeted financial products, the bank should:

- Form strategic partnerships with fintechs to collectively develop ‘pay as you use’ products to give their customers a more flexible choice to switch between a myriad of product ranges.

- Offering byte-sized loan and investment products to make the customer journey towards their financial goals more seamless.

- #4 Business segment expansion

- The small and medium enterprises (SME) sector continue to remain challenging, mainly due to uncertainties in the business environment from the protracted United States of America (US) and China trade war, contributing to weak consumer and business sentiment. There is an expectation that the demand for working capital by SMEs will increase amidst the COVID-19 recovery stage for business growth. To further enhance the SME financing strategies, the bank can:

- Develop business advisory and management tools that will allow SMEs to make smart investment and banking decisions over digital platforms.

- Collaborate with e-commerce websites to extend credit to small vendors who wish to enter the Malaysian market.

- Invest in digital-only banking services for SMEs to reduce the issue of outreach and inadequate distribution infrastructure.

- Reduce the in-merchant interchange reimbursement fee, and roll out tactical card acquisition and usage campaigns, including offering low merchant discount rates.

- #5 Employee experience and productivity

- Public Bank Group should try directing its employee-centric efforts to build a more productivity conducive work culture. It should focus on both practised empathy and technological advancements to ensure maximum employee satisfaction:

- As a part of its employee training and development initiative in terms of digital awareness, the bank can further streamline its employee development programme by:

- Using people analytics to understand the varying levels of experience, knowledge and future aspirations of the employees and design the training modules based on the data insights generated.

- Transforming their existing training delivery channels and breaking them down into byte-sized and easy-to-consume modules. Employees can then learn at their own pace and convenience.

- Training not only its ICT personnel but also all front-end and back-end employees in analytical-driven activities. The training will make them ready to transition into artificial intelligence and machine learning.

- As one of the top 3 best employers1 in the banking industry, the bank should continue to adopt best practices for employee well-being by focusing on things such as:

- Sponsoring volunteer ship programmes to build a more empathetic and ethical workforce.

- Financing 100% of the education loans of its employees to attract and retain the fresh graduates they hire.

- Furthering the use of AI to develop a comprehensive compensation mechanism to account for unconscious bias and ensure equitable distribution of rewards and benefits.

- A liaison for mental health and meditative programs.

- #6 Migration of workload to the cloud

- As a part of their digital strategy, the bank aims to develop a private cloud infrastructure to manage its IT infrastructure. However, to make its operational data sets more portable and ultimately migrate its operational workload to dedicated cloud storage, the bank should go for a hybrid cloud platform.

- The bank should spread its data across multiple IaaS (Information-as-a-service) and integrate its local servers with third-party, public cloud servers such as Amazon Web Services (AWS), Google Cloud, and Microsoft Azure.

- #7 Neo banking

- Public Bank Group aims to partner with fintechs by providing guidance on regulatory compliance and a secured sandbox environment for testing, research and development to forge meaningful fintech partnerships.

- With the growth of neobanks across the ASEAN region (TMRW by UOB and FRANK by OCBC), the bank needs more than just partnering with fintechs. It needs to carve out a GenZ/millennial-focused brand name which functions differently from the legacy channels of product delivery and customer interaction.

- Public Bank Group can roll out a digital spinoff with a specific target audience in mind and introduce digital-only customer journeys.

- The bank can address the different customer pain points by:

- Aiming for hyper-personalisation of its products to address the unspoken and latent needs of customers.

- Recreating the design outlook of existing products by introducing things like trendy ATM card designs, virtual cards, animated banking app interface

- Gamify various customer touchpoints like awarding badges with increased use of products, giving discount coupons to its loyal customers, leaderboard between friends and colleagues based on product purchases and highlighting trending products

- #8 Artificial Intelligence (AI) in everything

- Public Bank Group is already making efforts towards building a strong digital framework by focusing on API banking, AI, and machine learning in their operational segments.

- As a part of its pan-company digitisation journey, the bank should prioritise its AI framework in a layered approach by firstly focusing on:

- Automating iterative back-end jobs such as keeping sales records, book-keeping, loan application processing, etc.

- Filtering and enhancing data silos to make them conducive to analytics and algorithmic forecasting, which would further help them get insights into their operational inefficiencies.

- Using a comprehensive AI-enabled compliance system to standardise operational activities against pre-defined process benchmarks

- #9 Cybersecurity

- Public Bank Group has dedicated risk committees and overarching compliance committees that regularly test existing security standards and disaster preparedness. The bank should integrate technology into its traditional security practices by:

- Incorporating Cognitive process automation (CPA) to develop and test new security strategies and to determine appropriate response mechanisms to account for the dynamic and varied nature of security threats.

- Using predictive analytics in their cybersecurity strategies to identify risk trends and streamline its operational model to pre-empt and find the locus of inadvertent risks.

- Automating regular security functions to threat monitoring, identity access management, internal benchmark compliance, controlling and reporting mechanisms to make the overall security framework more transparent and smoother.

- Regular screening of data silos by using AI-ML to check for the misconfiguration of firewalls, data leakage and data manipulation to ensure that there is data integrity at all points in time.

- #10 Society and planet contribution

- The bank has a comprehensive sustainable outlook in bringing about a tangible impact in societal outlook strategy. To streamline its commitment to combat climate change, the bank should:

- Build on-site solar facilities and sign renewable agreements to add new wind and solar electricity to the grid. It should also focus on paperless transactions by investing in the digitalisation of services.

- To compensate for unavoidable emissions, Public Bank Group can launch supporting projects in impoverished areas that help preserve biodiversity, drive reforestation, and further local economic mobility.

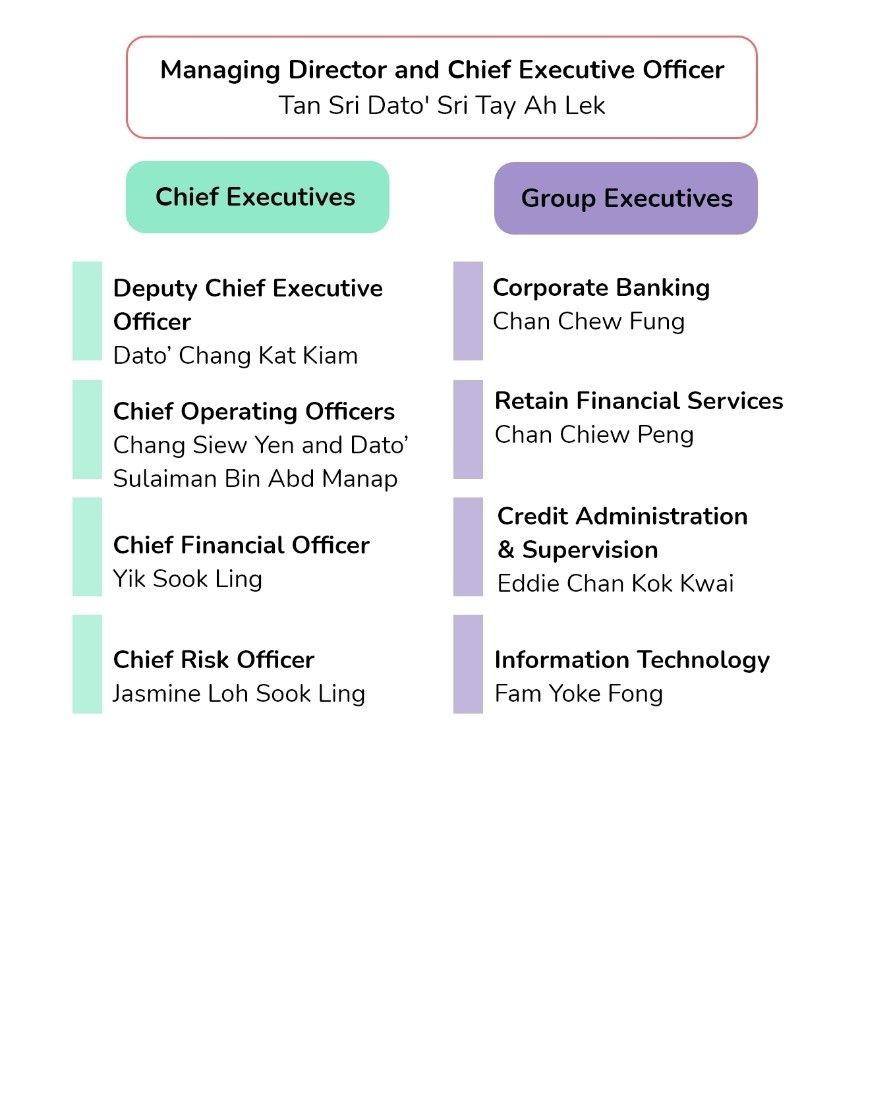

Organisation structure: Leadership

Executive Profile

Tan Sri Dato’ Sri Tay Ah Lek

Managing Director and Chief Executive Officer

Tan Sri Dato’ Sri Tay Ah Lek holds a certificate of Chartered Banker of the Chartered Banker Institute (CBI), United Kingdom and a Master in Business Administration (Finance) from the University of Hull, United Kingdom. With a rich 59 years of experience in the banking and finance industry, Tan Sri Dato’ Sri Tay Ah Lek currently serves as the Managing Director and Chief Executive Officer of Public Bank.

Quotes

Notwithstanding its long record of stable financial performance, the Public Bank Group is mindful that staying relevant amid the fast-changing environment is crucial.(30 April 2020)

- Future of Public Bank Group, Annual Report 2020

Amid this challenging environment, the Public Bank Group will continue to focus on sustaining its fundamental strengths. The Group’s time-tested strategies will enable the organisation to remain stable and resilient against challenges. The Group will also continue to explore new strengths to compete more effectively in this competitive banking landscape. (30 April 2020)

- Staff development, Annual Report 2020

Given the evolving banking environment arising from the more stringent regulatory requirement, and the changing dynamics of customer expectations and banking trend, the Group continued to initiate steps to ensure the relevance and competency of staff as required of their job scope, as well as their readiness for future challenges. (30 April 2020)

- Digitalisation, Annual Report 2020

The key goals and focus would be to enable business agility, offer competitive digital banking products and services, maintain resilient ICT infrastructure, advance data analytics, strengthen cyber resilience and improve governance and compliance.(The Edge, 30 April 2020)

Chang Siew Yen

Senior Chief Operating Officer

Chang completed her Bachelor’s degree in Accounting (Hons) from the University of Malaya, post which she went on to complete the Chartered Accountant of the Malaysian Institute of Accountants certification (MIA), Certified Public Accountant of the Malaysian Institute of Certified Public Accountants (MICPA) and Chartered Banker of the Chartered Banker Institute (CBI), United Kingdom. She was promoted from her previous post of Chief Operating Officer to Senior Chief Operating Officer in January 2020. Chang over26 years of experience in the auditing, banking and finance industry. She currently oversees the bank’s finance, corporate planning, strategy & economics, information technology, and property.

Dato’ Sulaiman bin Abd Manap

Senior Chief Operating Officer

Dato’ Sulaiman was promoted from his previous post of Chief Operating Officer to Senior Chief Operating Officer in January 2020. He got his Bachelor’s degree in Chemistry from the University of Malaya. He completed his Master’s in Business Administration (Finance) from the University of Hull, United Kingdom. Dato’ Sulaiman presently oversees Knowledge & Learning, Banking Operations, Credit Administration & Supervision, HP Credit Control, as well as Compliance and Loan Rehabilitation or Credit Review for Corporate Banking.

Appendix A

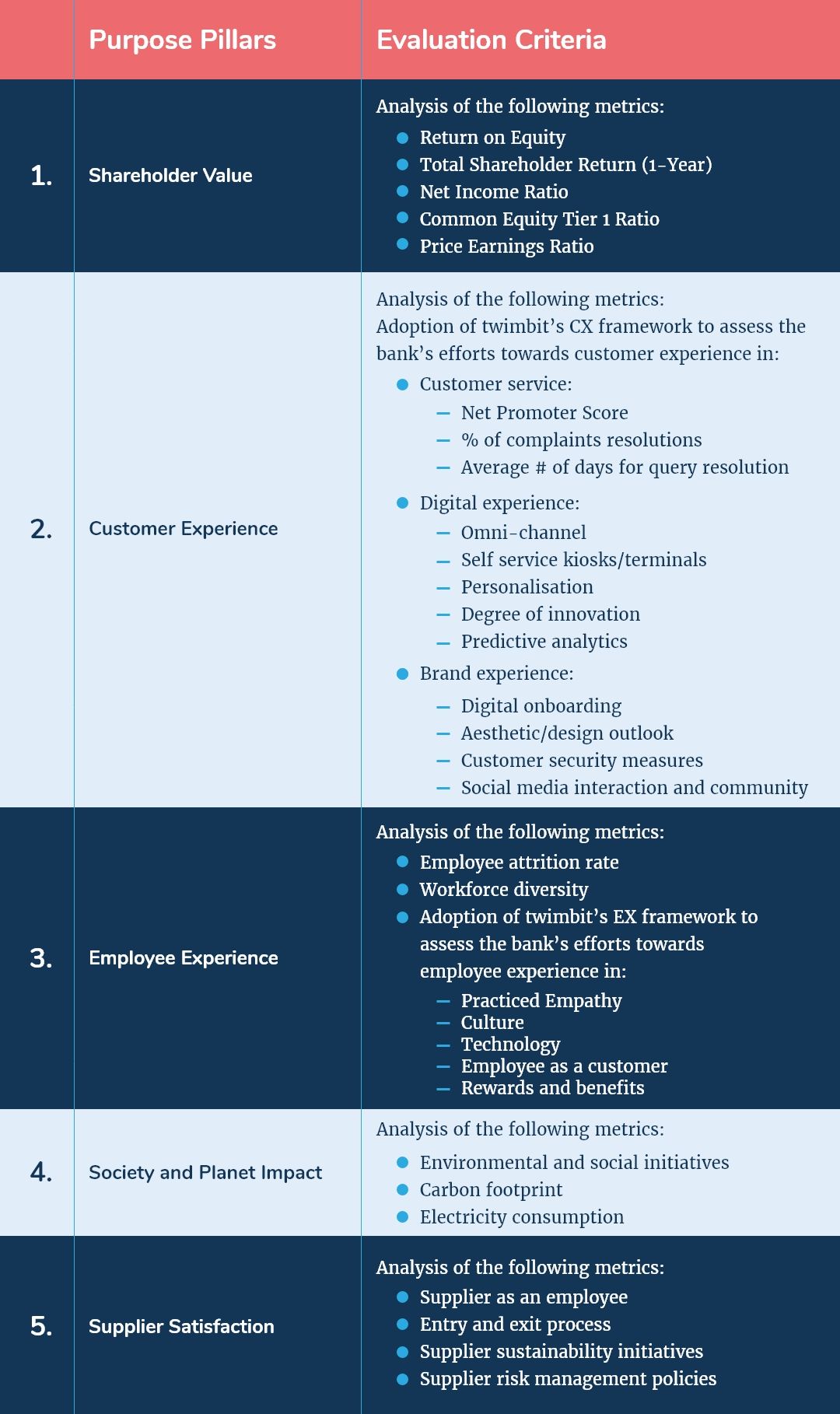

- twimbit Purpose Index

We evaluate Asia Pacific’s top banks to understand whether their strategic objectives, market positioning, and operational efficiency align with continued sustainability and profitability. In evaluating the respective bank’s focus areas and performance, we base our analysis on 5 purpose pillars and score each bank on them.

Endnotes

Top 10 Best Companies to Work For.(2012, August 22). The Richest.

https://www.therichest.com/salary/best-companies-to-work-for/

Adeline Paul Raj.(2018, October 30).Public Bank shows its digital hand. The Edge Malaysia.

https://www.theedgemarkets.com/article/public-bank-shows-its-digital-hand

Public Bank Group.(31st December 2019). Annual Report 2019.

https://www.publicbankgroup.com/CMSPages/GetFile.aspx?guid=fcfffb0b-ac32-4537-8640-938f9eae894f

Public Bank Group.(31st December 2019). Investor Presentation 2020.

https://www.publicbankgroup.com/PDF/Investor-Relations/Investor-presentation/2020/PBB_Sep2020.aspx

Public Bank Group.(31st December 2019). Quarterly Report 2020.

https://www.publicbankgroup.com/PDF/Investor-Relations/QF-Results/2020/4thQ-2020/PBB4Q2020.aspx

Vinayak Gandhi, Research Intern, contributed to the research in conducting preliminary literature review and conceptualising the article.