Key Takeaways

- The top five telecom vendors experienced a significant revenue increase in Q1 2023, with a combined YoY growth rate of 6.6 percent.

- The enterprise business experienced substantial growth for Ericsson and Nokia, driven by the increasing demand for 5G deployment.

- Vendors are investing significantly in research and development to stay at the forefront of innovation and maintain a competitive edge.

- Cisco’s research and development spending increased by 36.5 percent, reflecting their strategic decision to expand investment in ICT R&D internationally.

- Cisco achieved revenue growth across all geographic segments, reflecting its strong global performance.

- Ericsson overcame challenges in Europe and the Americas with significant gains in India, while Nokia offset a revenue decline in the Americas through substantial growth in India.

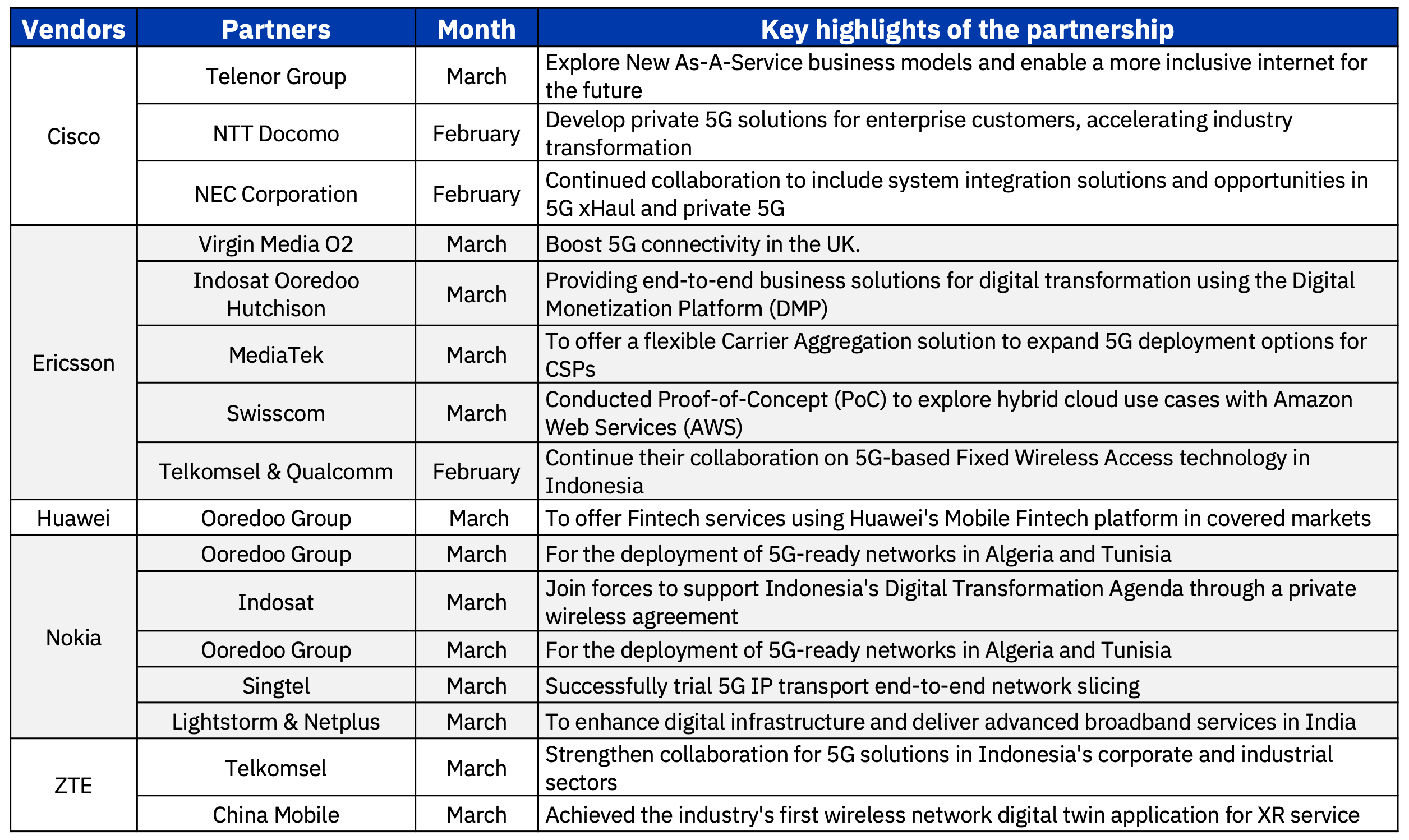

- Major partnerships in Q1 2023 included Ericsson with Virgin Media O2, Indosat Ooredoo Hutchison with Ericsson, Nokia with Lightstorm and Netplus, and Nokia with Indosat.

This report comprehensively assesses the Q1 2023 performance of the leading global telecom vendors: Cisco, Ericsson, Huawei, Nokia, and ZTE. The report’s primary focus is to provide valuable insights into the benchmarking of their carrier and enterprise business operations. Please note that the Chinese equipment vendors do not disclose quarterly revenue for segments and geographic regions. The report encompasses the following areas:

- Financial Performance in Q1 2023

- R&D investment

- Region-wise performance

- Major partnership in Q1 2023

Financial Performance in Q1 2023

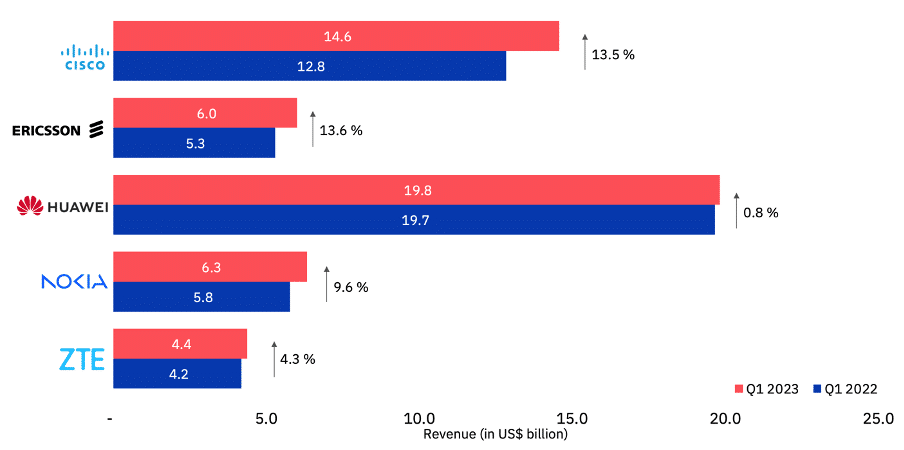

In Q1 2023, the top telecom vendors achieved positive revenue growth, demonstrating a combined YoY growth rate of 6.6 percent. The revenue growth performance of these vendors during this period is as follows:

- Cisco and Ericsson both experienced remarkable double-digit increases in their business, with growth rates of 13.5 percent and 13.6 percent respectively.

- Nokia achieved substantial growth with a growth rate of 9.6 percent.

- Chinese vendors Huawei and ZTE also witnessed growth, albeit at a slightly lower rate, with YoY growth rates of 0.8 percent and 4.3 percent respectively, including their consumer business revenue.

Exhibit 1

Total revenue and growth on a YoY basis

Note:

1. Huawei and ZTE don’t disclose segment and geographic wise revenue quarterly

2. Cisco’s financial performance is from February 2023 to April 2023

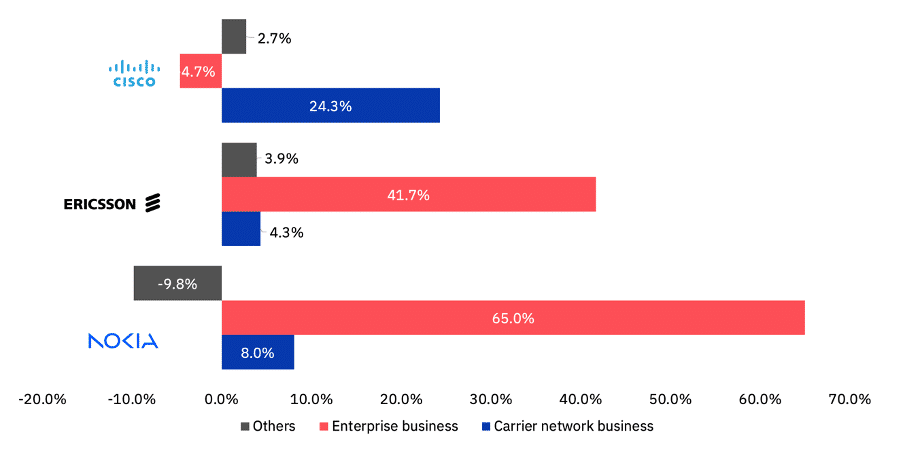

Ericsson and Nokia experience robust growth in their enterprise business, fueled by the rising demand for 5G deployment. However, Cisco relies on its carrier network business as a key revenue driver in Q1 2023, while its enterprise business witnesses a decline.

Exhibit 2

Revenue growth percent by customer type

Note:

1. Huawei and ZTE don’t disclose segment and geographic wise revenue quarterly

2. Cisco’s financial performance is from February 2023 to April 2023

Cisco

Cisco’s total revenue increased by 13.5 percent to reach $14.6 billion, with an increase in product revenue of 17 percent and an increase in service revenue of 2.7 percent.

Cisco’s carrier network business achieved a significant growth rate of 24.3 percent, primarily driven by strong performance in product revenue, which was led by growth in Secure, Agile Networks, which increased by 28.6 percent and Internet for the Future segment which increased by 5.1 percent.

Ericsson

Ericsson earned US$ 6 billion, including US$ 0.3 billion from Vonage, a 14 percent increase. Due to the network’s business restructuring, the IoT business was moved from enterprise to other segments, lowering the gross profit margin to 39.8 percent in Q1 2023. Enterprise Wireless Solutions and Vonage consolidation raised operating expenses.

Southeast Asia and India boosted network sales by 4 percent while other markets slipped. Networks sales dropped 600 basis points to 68 percent in Q1 2023. Enterprise organic sales (without Vonage) gained 19 percent. However, including Vonage revenue, enterprise revenue increased by 41.7 percent YoY. Cloud software and services recorded positivity in Q1 2023 with an 11 percent increase and are expected to be somewhat less than normal in upcoming quarters.

Huawei

Huawei generated revenue of US$ 19.8 billion, an increase of 0.8 percent YoY, and a net profit margin of 2.2 percent. The overall business results were consistent with projections. Huawei has increased R&D spending once more to continue innovating for the future, create new value for its customers, partners, and global communities, and promote quality development.

Nokia

Nokia’s reported a substantial increase of 9 percent with growth across all business groups except Nokia Technologies. Gross profit margin fell 310 basis points to 37.5 percent from 40.6 percent. Network infrastructure grew 14 percent YoY, with IP networks expanding by 13 percent and optical networks by 45 percent. Fixed networks declined by 5 percent, offsetting this rise. Normalised supply chains boosted growth in Q1 2023, but comparisons will make future quarters harder.

Nokia’s order book fueled 65 percent YoY enterprise revenue growth. In Q1 2023, Nokia added 73 Enterprise clients, bringing the total to over 595 customers. Nokia Technologies’ revenue fell 21 percent due to a long-term licence that was exercised in Q4 2022 and no longer contributes to licencing revenue.

ZTE

ZTE reported strong financial results for the first quarter of 2023, with revenues of $24.3 billion, an increase of 4.3 percent YoY. ZTE’s net profit has increased by 19.2 percent. The financial results for the first quarter of 2023 for ZTE demonstrate the company’s resilience and adaptability in the face of ongoing global challenges. ZTE has achieved impressive growth and further cemented its position as a global leader in the ICT industry by employing a methodical and pragmatist approach to business operations.

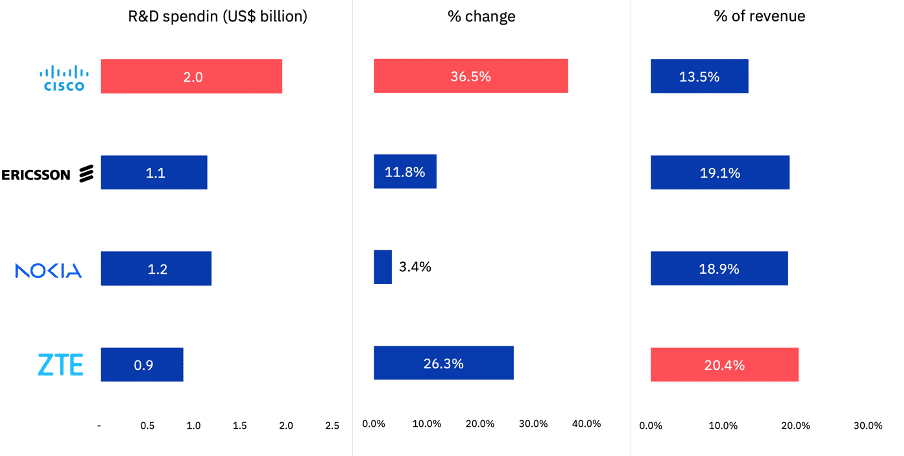

Cisco bets on innovation with increased R&D spending

Exhibit 3

R&D spending by vendors, Q1 2023

Note:

1. Huawei don’t disclose segment revenue quarterly

2. Consumer business revenue included for ZTE

3. Cisco’s financial performance is from February 2023 to April 2023

Cisco

Cisco’s research and development spending increased by 36.5 percent YoY, reaching US$ 2 billion. This expansion was fueled by the company’s strategic choice to increase its investment in ICT R&D internationally.

Ericsson

Ericsson’s R&D expenses increased by 12 percent YoY, primarily in the Enterprise segment due to the acquisition of Vonage and investments in expanding its Enterprise Wireless Solutions portfolio, even though R&D spending as a share of total revenue decreased by 30 basis points to 19.1 percent.

Nokia

Nokia experienced a growth of 3 percent YoY while it faces a decline of 9 percent on a QoQ basis. The increase in R&D expenses was part of long-term R&D investment for Radio Frequency Systems (RFS).

ZTE

ZTE’s commitment to innovation has enabled it to remain competitive globally. The company continues to invest in research and development, focusing on key technologies such as 5G, 6G, artificial intelligence, and the Internet of Things (IoT). ZTE’s R&D spending grew by 26.3 percent YoY. This dedication to innovation is evident in its growing patent portfolio, which has enabled ZTE to maintain a leading position in the ICT industry.

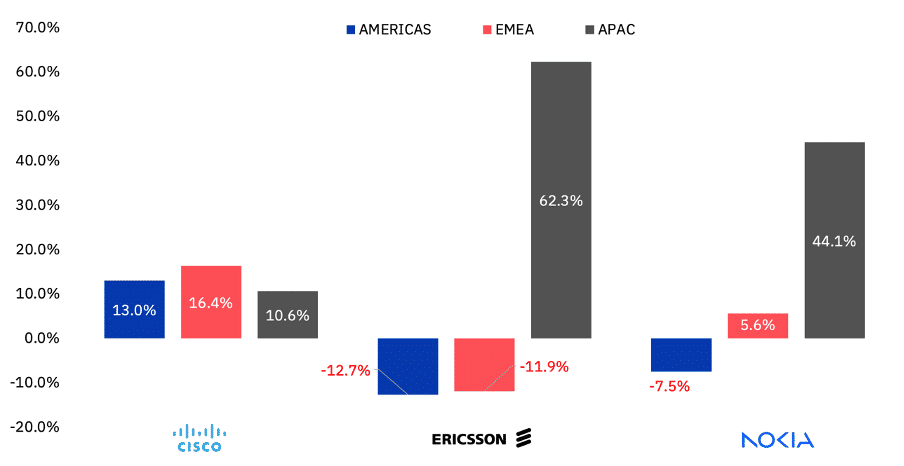

India’s 5G rollout fuels strong growth for vendors

Exhibit 4

Revenue growth in different regions

Note:

1. Huawei and ZTE don’t disclose segment revenue quarterly

2. Cisco’s financial performance is from February 2023 to April 2023

Cisco

Cisco reported double-digit increases across every region. There was a growth of 13 percent in the Americas, 16 percent in EMEA, and 11 percent in APAC. Growth in the Americas was driven by an increase in service revenue, while the growth in the APJC was driven primarily by partnerships with telcos in India for the rollout of 5G.

Ericsson

Ericsson encountered challenges in the Americas and EMEA region, but these were successfully offset by a remarkable 62.3 percent increase in the APAC region. Particularly noteworthy was the exceptional revenue growth of 138 percent in Southeast Asia, Oceania, and India, driven by our significant market share gains in the 5G sector in India and the timely achievement of project milestones in the Philippines and Malaysia. While Northeast Asia, North America, and Europe experienced a decline in revenue by 20 percent, 18 percent, and 16 percent respectively, it is important to acknowledge that these regions had already made substantial investments in 5G in 2022. On a positive note, Latin America showcased a commendable 6 percent revenue growth, propelled by successful 5G deployments in the region.

Nokia

Asia Pacific’s performance (excluding India and China) declined by 9 percent due to the decline in Mobile Networks and Cloud and Network Services, particularly in Japan. This was partly offset by broader growth in Network Infrastructure. Greater China reported a decline of 14 percent, majorly impacted by Mobile Networks. However, the growth in India was enough to offset the decline for Nokia in APAC. The growth in India was fuelled by strong demand for Mobile Networks due to the ramp-up of 5G deployments in India.

Middle East & Africa growth was driven by growth in all business groups, whereas Europe reported double-digit growth across all business verticals, which was able to offset the negative impact of Nokia Technologies caused by a long-term licensee in its Europe business.

Latin America’s growth was stable, with slight growth in Network Infrastructure mostly offset by Mobile Networks and Cloud and Network Services, which was not sufficient to offset the decline of 9 percent in North America due to a double-digit decline in Mobile Networks combined with some customer inventory depletion in Q1 2023. However, this was somewhat offset by growth in Cloud and Network Services and Network Infrastructure.

Vendors accelerate growth with partnerships

Thank you for reading! Reach out to us for any feedback

You might also like:

Benchmarking the performance of the top 5 telecom equipment vendors in 2022

Cloud Stories Q1 2023: Insights into the performance of AWS, MIC, GCP and Oracle Cloud