The financial service industry is in transition right now. Due to increased competition, regulations and macroeconomic downturns, the banks’ profitability has been under pressure. The COVID-19 pandemic escalated the situation further by shrinking interest margins. Leaders across the banking sector now seek cost-transformation solutions beyond incremental improvements. Some streamline banking channels and increase operating and IT costs, while others opt to cut expenses by reducing manpower and redundant operations.

Cost control is not new. Hence, banks strive for top-line growth, finding new ways to turn growth investments into long-term profit. As a result, banks must restructure their cost bases.

Traditional cost-cutting techniques may not be as effective as they once were. Banks must also ensure those cost reductions do not come at the expense of growth. Banks should target efficiency rather than cost reduction by automating more operations, reducing redundant physical infrastructure, and establishing self-service channels. The future goal is to implement long-term, sustainable cost optimisation methods.

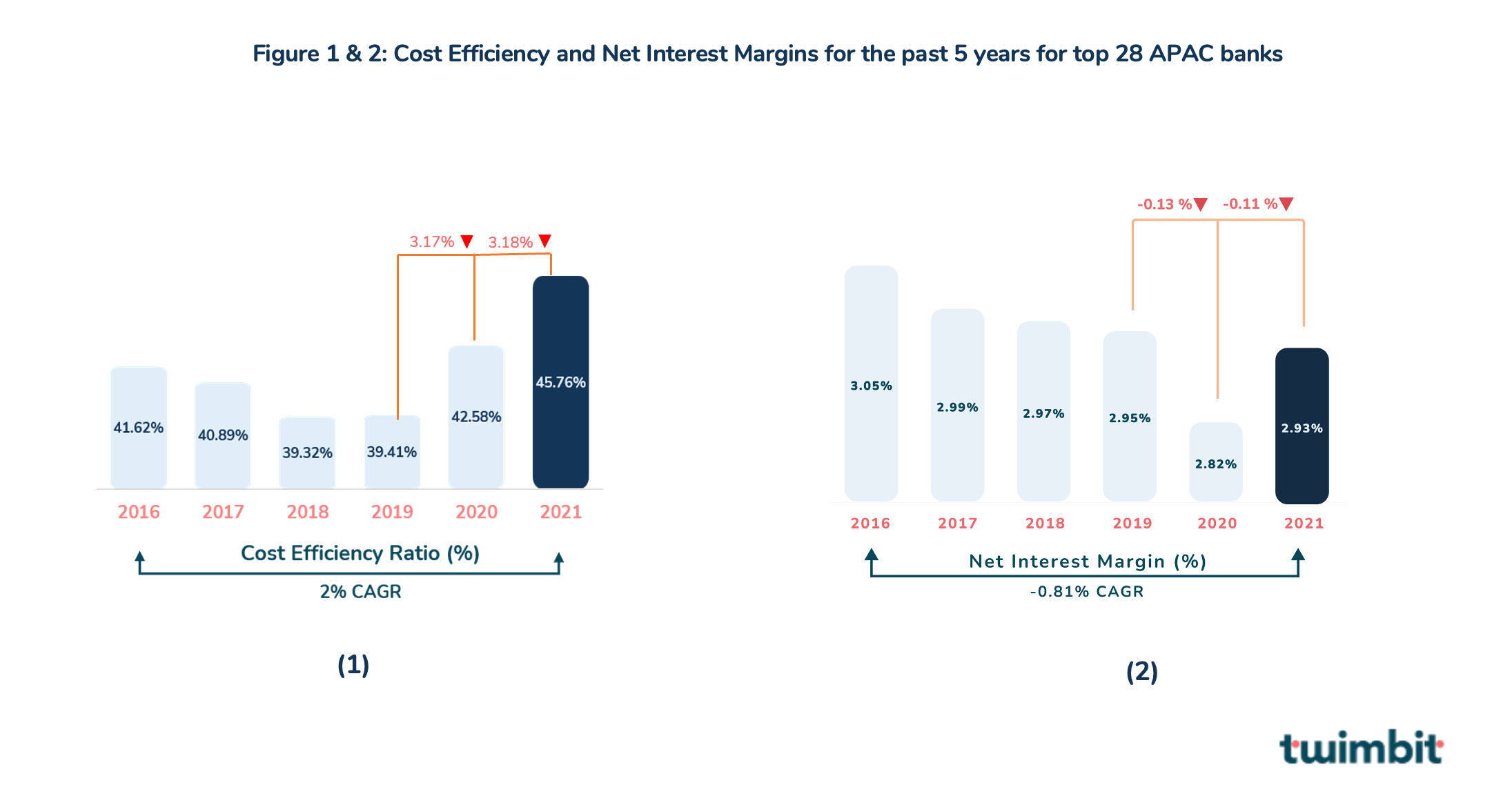

Digitisation, manpower reduction, and legacy IT transformation are essential to reduce costs following COVID-19. The cost efficiency (CE) levels of the top 28 APAC banks (Figure 1) signifies a downward hit on the cost structures, and it has significantly impacted profitability (Figure 2).

ICBC has the lowest CE ratio in 2021, focusing more on digitisation and transforming legacy IT infrastructure into an agile cloud environment. The bank has also increased its use of AI and blockchain technology to enhance internal processes and improve customer-facing applications. Meanwhile, BOQ had the highest CE ratio due to heavy investments in risk and security mechanisms.

Although banks have tactical and incremental cost reduction strategies in their arsenal, now is the time to take a step back and envision a future enterprise-wide business strategy. The cost structure must be highly efficient, adaptable, and scalable, redefining the measures of success.

New cost measures to build a resilient profitability model for the banks

To lock in a sustainable cost optimisation strategy, banks must reimagine their operating model. This reimagination involves augmenting the agility, resilience, and digital transformation they deployed in their initial pandemic measures. The major focus of the cost strategy must be to revamp and own customer journeys. Two sensible approaches to reducing costs would be to target operations that provide value to the customers and simplify and automate current revenue-related activities. These activities can include payroll, KYC, loan processing, AML, etc.

Winning banks will develop strategies based on a solid grasp of their competencies and infrastructure, including the markets and customer segments they cater to. Banks will need to strike a balance between innovation and utility to implement these strategies successfully.

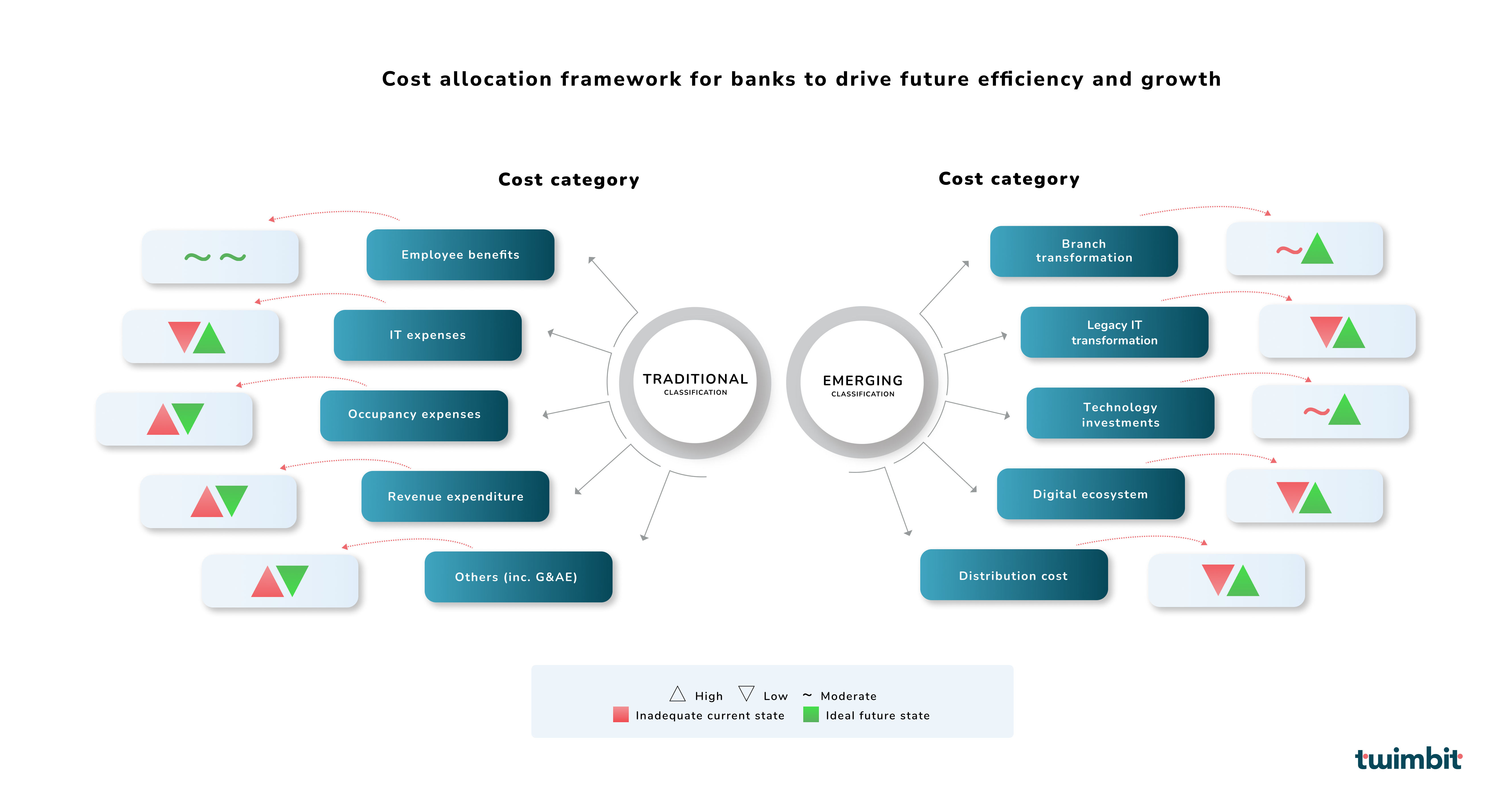

At twimbit, we have studied top APAC banks and observed these new, emerging costs that have become a part of the cost structure for banks.

Many banks have made substantial efforts toward digital transformation and have thus adopted the new cost structure. Hence, let us talk about the five emerging cost categories for banks:

- #1 Branch transformation:

A consistent customer experience across all physical and digital channels is increasingly becoming the norm. To boot, many institutions have already made significant expenditures in this direction. However, bridging the physical and digital divide is unlikely easy or quick, leaving many banks concerned about the process. As it is, they are already dealing with a myriad of other issues — greater regulation, sluggish loan growth, and new competitors. Thus, the oldest and most expensive banking channels are under severe pressure. Moreover, as customers progressively shift to digital channels, these banks must adapt to the reality of lower foot traffic and transaction volumes, resulting in greater transaction costs.

Branch banking must evolve, yet there are difficulties along the way. For instance, while closing an underperforming branch is common, many banks make these decisions in the dark, relying on obsolete branch performance models. So, how should branch performance be judged in the digital age? We believe banks must redefine their profit, revenue and cost centres.

The definition of what a branch is, what it does, and how it functions is evolving — branches are not disappearing anytime soon. Branch-related costs often account for one-third or more of a bank’s operational costs. They’re also where relationships form and business gets done. Because of the importance of branches, banks must look past the hype and carefully plan their strategy and service delivery methods while enabling their technology. They must adapt to a phygital (physical + digital) model.

The phygital model gives incumbents a competitive edge since they can use their physical network to create customer trust, while the digital side is convenient and fast in meeting demands. The marriage between physical and digital gives them an advantage over new-age digital-only banks.

But customers’ acceptance and adaptation to the new phygital model are critical to the success of a branch transformation initiative. So these are the two questions that any bank should ask:

- How do my customers currently bank with us?

- How do I want future customers to bank with us?

- #2 Legacy IT transformation:

A digital-first, customer-centric bank must modernise its business, operating models and core banking platforms. Such banks must continue to invest in the future by updating their key platforms and preparing their infrastructure to keep up with the fast pace of change and competition. All of this is to enable agility and innovation. Nowadays, any organisation with the technical ability to grow, manage, and transport consumer money is competing for wallet share. Nonbanks and fintechs aggressively pursue traditional banking customers at a time when switching becomes costless. Many new competitors do not bear the same economic and technical debt as banks. It is no surprise that consumers prefer to interact with enterprises ahead in their digital transformation journey. Hence, banks have ample chance to respond to this challenge by revamping their basic infrastructure, allowing them to prosper as future-ready, customer-centric institutions.

Banks have been hesitant to update their systems for a long time, and with good reason. Instead, they use contemporary systems, a product of continuous innovation, to address instant consumer needs. However, this has resulted in adopting separate systems for transactions, savings, investments, and loan accounts. This method is incompatible with the digital age, especially when banks face competition from technology-based fintech businesses.

We believe the highest cost incurred lies in the end-to-end digitisation of the middle and back office, where wasteful manual processes are still prevalent. Therefore, while modernising an entire bank in one go is difficult, starting with the fundamentals is a good step.

Through core modernisation, product innovation, speed-to-delivery methods, real-time processing, and other critical customer needs, components can be unlocked. However, only modernising technology is not the goal. In fact, the goal is to ease out business concepts and operating models. The goal is to ensure that the front, middle, and back offices are all working together to create consistent customer experiences, thus positively impacting the entire organisation, from strategy to people to culture.

Initiatives that banks can do:

- Use cloud service models to transition from a capital-intensive approach to a more flexible business model with lower operational costs. The key to success is choosing the correct cloud service model to fit the requirements. Using offshore hybrid cloud environments reduces a high upfront capital investment into a smaller, recurring operating cost. Furthermore, the unique nature of the cloud allows banks to ‘pay-as-they-go’ for the services they require.

- In order to facilitate agility in a technological ecosystem, each component must function independently within a given input. However, building such an ecosystem requires support from a horizontally linked team rather than a different chain of tasks, from chains such as design, development, testing, and security to operations. Therefore, banks must build a team to form an integrated technological ecosystem.

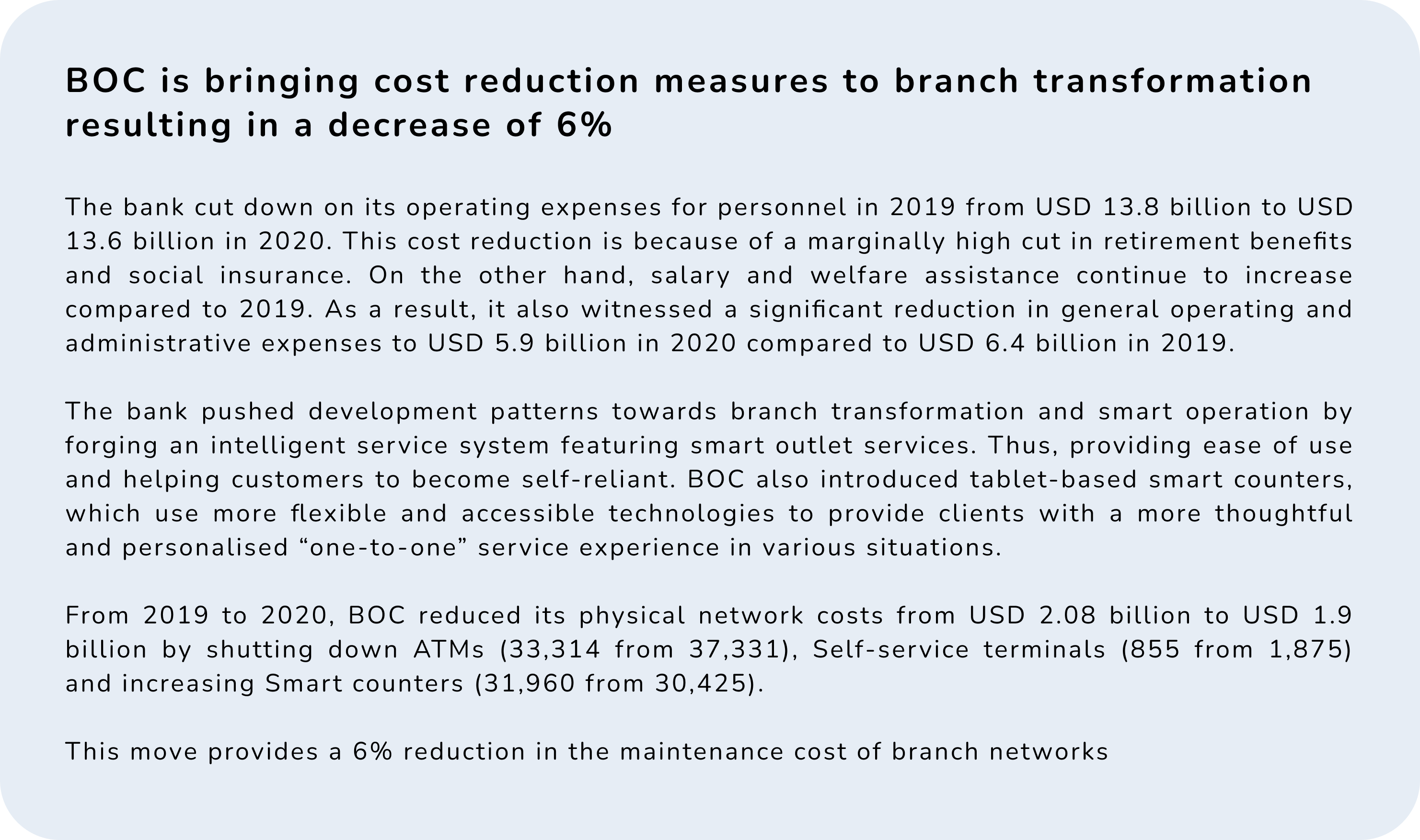

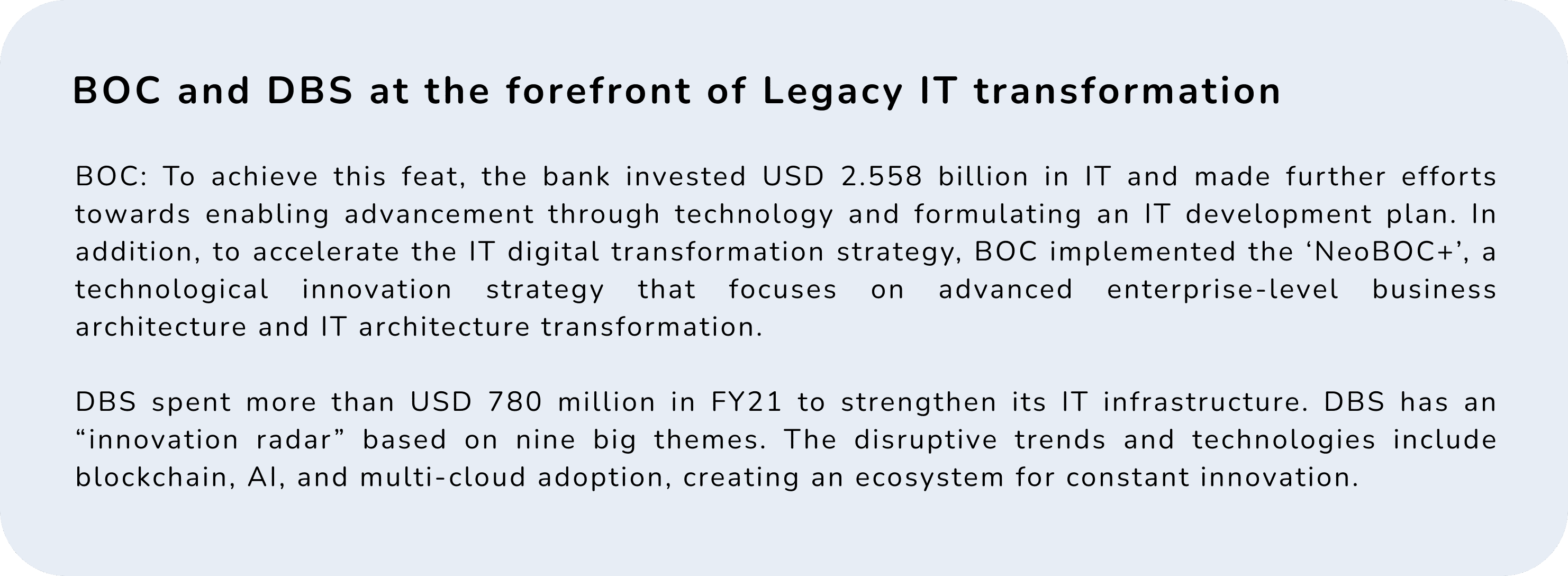

Some instances where banks were successful in modernising their infrastructure include:

- #3 Technology Investments:

These projects use cutting-edge technologies to ensure a customer-centric approach rather than a traditional product-centric approach. They also use real-time intelligent data integration rather than post-hoc analysis and an open platform foundation.

Banks must become leaner and more effective in choosing their technology strategy to manage their costs. The rapid expansion of cloud-based software, remote access via personal devices, and the handling of enormous volumes of data and documents across a complex technology environment are significant enablers. Still, they also introduce a vastly unsecured surface. As a result, it’s no surprise that the most crucial investment in the new reality should be security and privacy. Other technologies that banks should prioritise are:

- Cloud for corporate services and IT.

- Corporate SaaS, particularly cloud-based enterprise resource planning (ERP), modernises the front, middle, and back-office divisions, driving more effective and smarter operations.

- Intelligent automation, artificial intelligence (AI), and machine learning (ML), where AI and ML should combine with the Internet of Things to improve efficiency, productivity, and quality.

- Banking software and platforms to build sustainable digital banking channels.

- #4 Insourcing over outsourcing digital ecosystem:

By offering the same products and services to the same customers with the same level of delivery, banks cannot grow market share or achieve sustainable revenue and earnings growth. The bar for innovation in new thinking, value propositions and delivery mechanisms have been reaching new highs, barring the largest organisations. The internal capacity for technology and new business model development has outpaced external resources for the smaller organisations. As a result, complex fintech ecosystems must be partnered with and invested in to ” insource ” innovation and broaden possible market reach. Such collaborations significantly reduce the customer acquisition cost (CAC) as fintechs are more agile in technology than banks, thus acquiring customers much faster. Connecting with fintechs at scale is a huge operational challenge that requires banks to rethink traditional business development strategies.

To capture more market value, banks are encouraged for an ecosystem approach to address the customers’ needs. An ecosystem approach entails bundling services outside of banking to provide customers with a frictionless and comprehensive solution.

These service bundles could target several parts of people’s lives, including housing, retail, mobility, retail and wellbeing, and financial health. Various players deliver their products and services as part of an ecosystem offering, integrated into a single digital platform aimed at the customer. By increasing the number of locations of access to their financial goods, banks may address a larger percentage of total wallets.

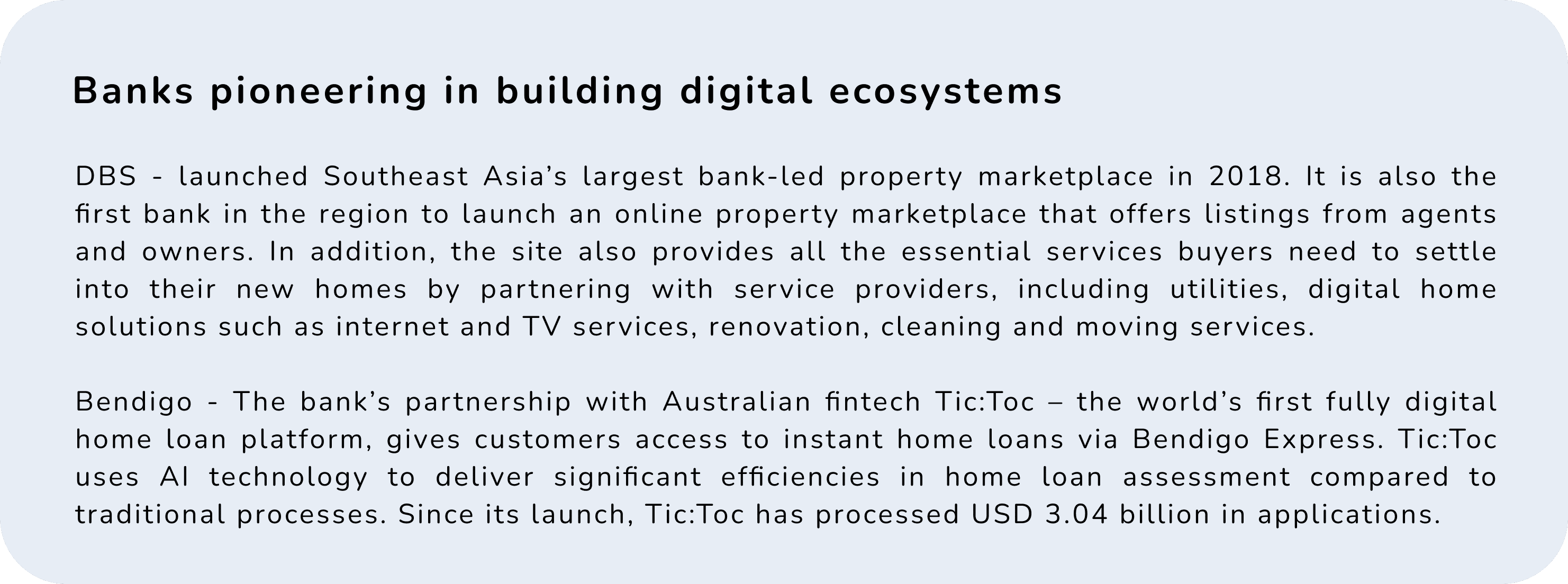

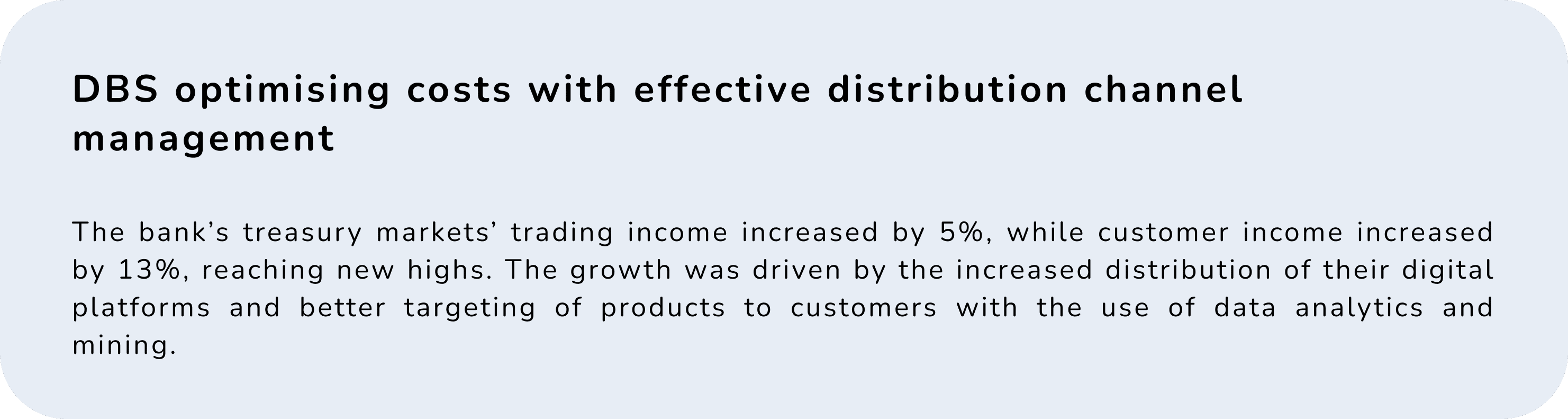

Insourcing its digital ecosystem will cut costs and improve its strategic positioning by offering non-financial services that clients will pay for. A few instances of banks taking this approach include:

Other initiatives that banks can take are to:

- Set up investment funds and build in-house fintech accelerators

- Build design labs for testing prototypes of new offerings

- Invest in robust and real-time third-party risk management capabilities

- Spend on API infrastructure to enable quick and open architectural partnership models

- #5 Digital distribution cost:

All financial institutions spend a large amount of money on digital marketing, and the rivalry for new consumers is fiercer than ever, resulting in high expectations for customer acquisition.

The problem is that digital financial services marketing is too slow to respond to market changes. Other issues include a lack of transparency in the end-to-end acquisition experience and a lack of accountability between marketing and digital product owners. As a result, the digital distribution costs go high. On average, the CAC is USD 100 per customer, which banks need to reduce by 70% to USD 30 to see a significant impact in cost transformation. Therefore, banks need to manage their distribution channels effectively.

When the strategy applied optimises internal and customer benefits, that is when effective distribution channel management takes place. Some of the ways that banks can optimise these benefits include:

- Reduced call demands;

- Migrating tasks to lower-cost channels;

- Optimising the workload and required employees to reshape customer interactions and improve the omni-channel experience

Banks should examine the answer to these questions when building a cost-effective distribution channel strategy:

- Should banks leverage different distribution strategies to reach specific consumer demographics?

- How can banks maintain the rise of digital adoption resulting from the COVID-19 pandemic?

- What is the channels’ CE each?

- Could banks make their digital user experience more seamless and intuitive for customers?

- How can banks persuade customers to switch to more CE channels?

- What are the banks’ options for dealing with critical failure demand in their branches and call centres?

Its distribution channel strategy influences the cost-efficiency of a bank. If the bank cannot fulfil a customer’s needs via a phone call, the cost of a branch visit rises. Similarly, there are additional expenditures if a consumer lacks confidence in digital channels and prefers to speak with someone in person or over the phone. If incomplete data on the internet necessitates manual intervention before the bank can process a consumer request, costs rise again. Consequently, this increases the CAC.

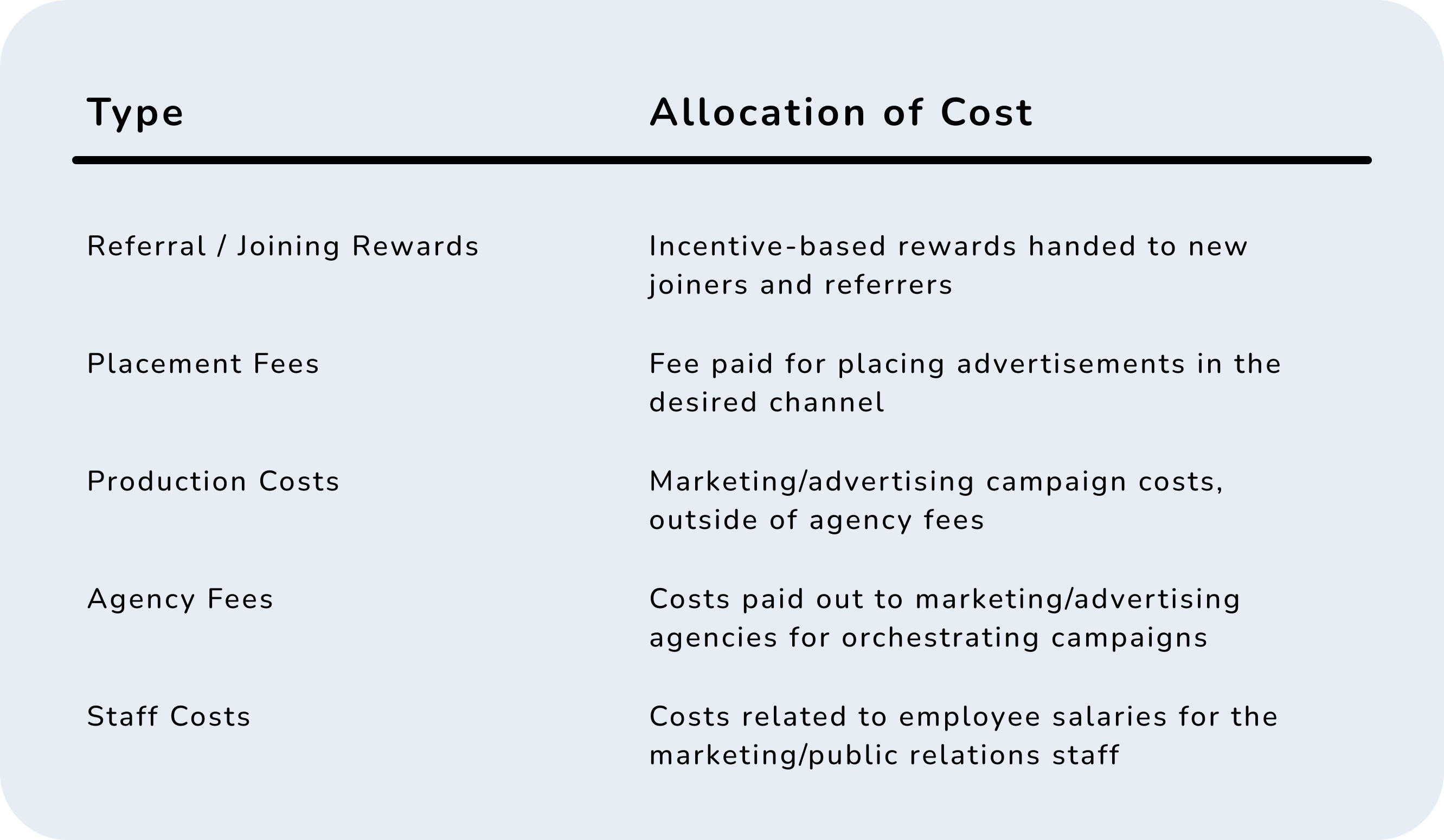

There are quite a few hidden costs on customer acquisition:

To optimise these costs, the banks should focus on AI-powered technologies that can analyse complex data from relevant sources — such as marketing and offline onboarding data — and make suggestions to optimise spending depending on the acquisition of the right customer.

Conclusion

Cost control is a top concern for banks all around the world, and the majority have reached remarkable levels of operational efficiency. Despite their best efforts, however, far too many mid-tier banks struggle.

To get to the next level, they will need to heavily focus on strategic cost reductions and implement more breakthrough technologies like automation, cognitive/AI, and business intelligence. These digital technologies have the potential to deliver the significant cost savings required to fund and implement business changes that are not only for growth but also for business model transformation.

Refocusing attention on IT and operations creates cost-cutting initiatives, such as enhanced automation and better customer service, while generating direct revenue. Likewise, increased data and analytics engines can have a similar, double impact, providing richer insights into banks’ customers and businesses. Altogether, this allows for developing more customer-centric products and services, driving more targeted business outcomes with the potential to generate more profit.

Banks must aim for low distribution costs. Therefore, accurately analysing performance by distribution channel provides insights into the potential for increased profitability by moving toward more effective channels and streamlined incentives.

Banks with clear business models, a stronger focus on their differentiators, streamlined product portfolios, and simpler, more transparent processes and systems will be more successful than their competitors. In addition, they need to focus on being their customer’s life partner. The end goal should be to make banking “invisible” to consumers. This will be possible by building ecosystems that immerse financial services into different customer life events. Insourcing their digital ecosystem will cut costs, allowing them to improve their strategic positioning by offering non-financial services that customers will pay for.