Company Insights

twimbit Purpose Index

Source: Refer to the methodology in Appendix A below

RHB Bank (Group financials) – An overview as of 31st December 2020

| Bank name | RHB Banking Group |

| Headquarters | Kuala Lumpur, Malaysia |

| Operating income (31st December 2020) | USD973.9 million |

| Profit after taxation (31st December 2020) | USD501.8 million |

| Total Assets | USD66.9 billion |

| Employees | 14,000+ |

| Country of operation | 10 |

| Number of branches | 364 |

| Information and communication technology (ICT) spend (31st December 2020) | USD 67.13 million |

| Bank ranking in the particular country | 4th in Malaysia |

| Number of customers | Not available |

| Market capitalisation (31st December 2020) | USD 5.7 billion |

| Operating revenue CAGR growth (2016-2020) | 2.77% |

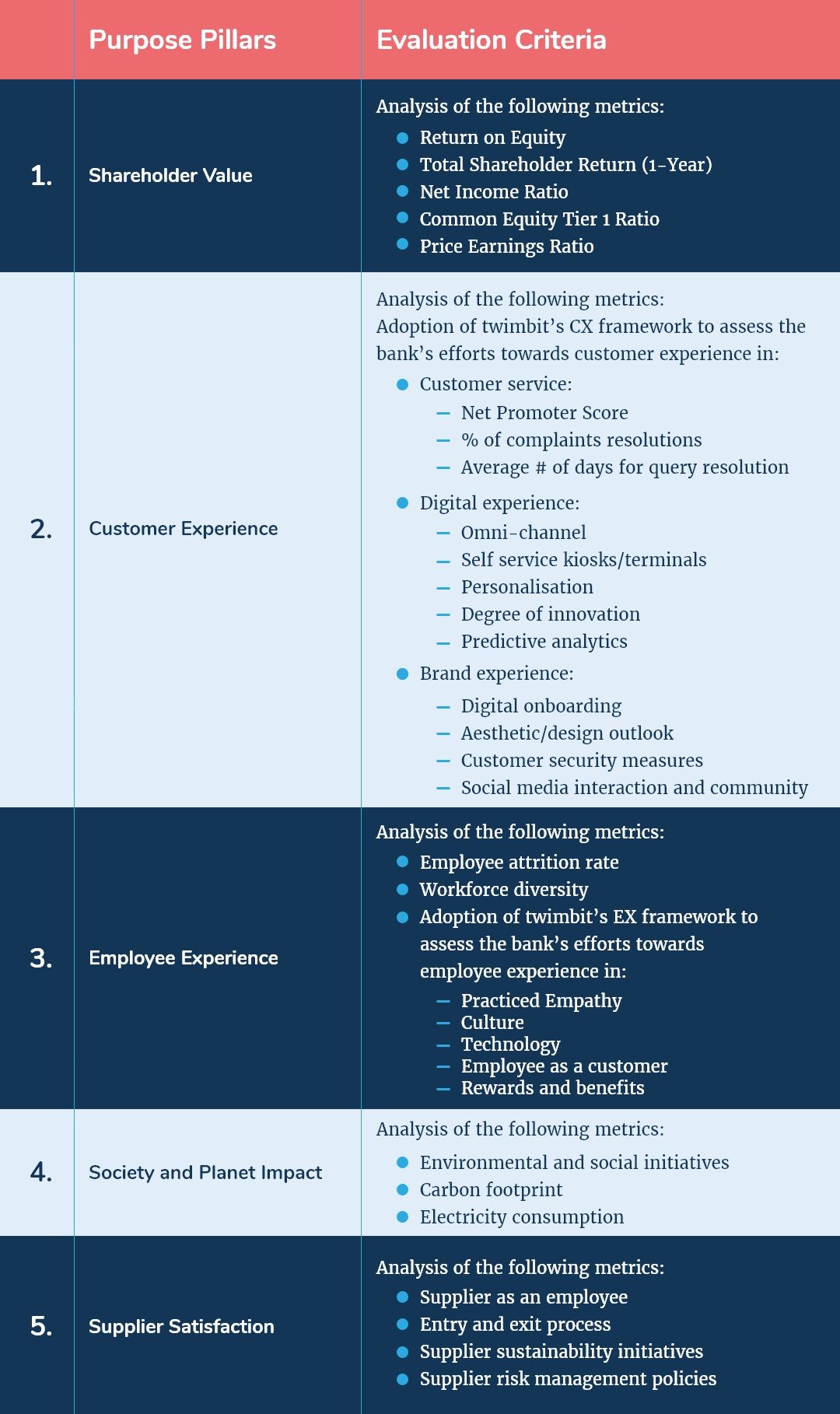

Shareholder value (31st December 2020)

| Return on Equity (31st December 2020) | 7.7% |

| Total Shareholder Return (1-Year) | -3.40% |

| Net Income Ratio | 35.04% |

| Common Equity Tier 1 Ratio | 16.18% |

| Price Earnings Ratio (31st December 2020) | 9.53 |

Awards

| 2020 | Best Retail Broker in Malaysia, 14th Annual Best Financial Institution Awards in Southeast Asia Green Deal of the Year, the Asian Banking & Finance Corporate & Investment Banking Awards 2020 Gold award from National Annual Corporate Reporting Awards 2020 (NACRA) |

RHB Bank and its strategic focus areas

In FY2020, RHB Group took steps to adjust and adapt its strategies, given the unprecedented and lasting impact of the pandemic. Thus, the group revisited its FIT22 initiatives to incorporate a strong focus on driving business resilience, improving operational processes, and enhancing customer-centricity. In 2020-2021, the bank completed the third year of its five-year strategic road map. Defined by the bank as ‘FIT22’, the plan focuses on the following:

- Fund our Journey (F), a road map to enhance financial performance by targeting the right customer segment.

- Invest to win (I), a strategy to capitalise on the technologies available to ease banking operations.

- Transform the organisation (T), an agenda to enhance customer and employee experience.

- Business segment expansion

RHB Group plans to boost revenue from prioritised customer segments, as well as through optimising the use of capital by focusing on three key segments:

- Growing the high-net-worth clients with a continuously improving value proposition and product suite.

- Growing the retail segment through deposits and products by improving digital onboarding through ‘branchless services.’

- Accelerating growth in mortgage loans by continuing to build on the homeowner’s ecosystem.

- Enhancing SME loan growth by driving end-to-end banking solutions through online and digital channels for a better overall customer value proposition.

- Improving its penetration into large-cap and mid-cap commercial segments.

Key initiatives in FY 2020 to boost financial performance include:

- SME (Small and Medium Enterprises)

- Launched the first AI-powered SME financing mobile app in Malaysia. It automates the customer onboarding process and enables remote interaction with relationship managers.

- Started the RHB #JomSapot campaign, allowing SMEs to promote their products and services through a free online platform and connect with potential customers using social media.

- Mortgage

- Began the RHB MyHome website, in addition to its existing RHB MyHome App. Both platforms aim to deliver a seamless move-in experience, connecting homeowners with leading service providers through a single ecosystem.

- Partnered with a local fintech company to enable customers to receive instant in-principle approval of their online mortgage applications through the RHB MyHome App.

- Overall business growth

- RHB Group became the first bank in Malaysia to roll out real-time mobile e-ticketing services. It allows same-day appointments in 50 selected branches (as a pilot to nationwide deployment).

- Heightened loan growth by focusing on segments (Corporates, SMEs, Individuals) and driving end-to-end solutions instead of product-centric propositions.

- Increased retail deposit growth by becoming the main transaction account for customers, supported by more features in the new RHB Mobile Banking App.

- Intensified growth for Singapore by leveraging on the country as a regional hub and also for Cambodia by growing its SME segment and digital retail solutions.

- Consolidated select overseas investment banking businesses while building Singapore’s commercial bank as its regional hub.

- Partnered with Espírito Santo Investment Bank (ESIB) to distribute Malaysian equity research and investment banking products by RHB Investment Bank (RHBIB) in Europe. Collaborated with SinoPac Securities (SinoPac) to strengthen its internet banking (IB) operations in Malaysia.

- Customer experience

- Focusing on customer-centricity through better customer experience and treating customers fairly.

- The group intends to build a winning operating model that prioritises the customer journey, agility, analytics, and digital enablement. Steps include equipping the bank’s customer relationship managers with the vital skill sets to manage digital customer pathways. By driving service excellence through the RHB Way Service Culture initiative, RHB Group can excel in its overall customer experience. Streamlining the services at the customer contact centre and implementing an Interactive Voice Response (IVR) system to reduce the time taken by executives to resolve enquiries.

- Ensuring that the transition of the bank’s digital interfaces is seamless, thereby providing customers with enhanced convenience, connectivity, and speed.

- Delivering products and services in line with BNM’s (Bank Negara Malaysia – Central Bank of Malaysia) Fair Treatment of Financial Consumers (FTFC) Policy.

- Improving the turnaround time in both product application approval and the disbursement of credit cards, hire purchase, and loan portfolios to maintain a competitive position in the market.

Key initiatives to enhance customer experience in 2019-2020 include:

- Improved the net promoter scores (NPS) in Malaysia from 9 in 2019 to 11 in 2020

- Curated a dashboard on the RHB mobile application based on the banking activity of customers for a personalised banking experience

- Turnaround time for product application: Upon complete documentation received by the bank:

- Credit Card / Credit Card-i Application: Three working days, including the time taken to mail the card.

- Hire Purchase / Hire Purchase-i Application: Two working days.

- Mortgage Loan / Home Financing-i Application (individual): Five business days.

- Loan / Financing Application (Small and Medium Enterprise – SME): By Three weeks.

- Turnaround time for complaint resolution using phone banking:

- Where there no follow up is required – Immediate, such as a first call resolution.

- Where follow up is required – Within three working days from the date of the first call.

- Where an enquiry is complex, the bank will provide a reasonable timeframe and keep the customer updated accordingly.

- Continuously increased operational efficiency by improving turnaround time for trade bills processing from 40% in 2019 to 63% in 2020.

- Introduced post-resolution customer surveys to gauge customer feedback through the SMS platform and subjected the received feedback to the root-cause analysis of the customer query at hand.

- Relaunched SME e-solutions in May 2019 with the integration of Financio accounting solutions via API. This move has doubled the bank’s customer base to approximately 6,000 customers and delivered more than USD74.06 million of CASA under management.

- Initiated a financial benchmarking tool via iSmart for SME customers to improve advisory and engagement.

- RHB became the first bank to provide a real-time digital queue system for branches via mobile app, allowing customers to book their banking appointments ahead of time.

- Achieved ISO/IEC 27001 Information Security Management Systems re-certification of its core e-Banking and transaction systems.

- Provided automatic six-month moratorium, followed by further assistance through payment and targeted payment assistance programmes for individuals and SMEs that continue to be impacted by the pandemic.

- Implemented strict SOPs (Standard Operating Procedures) to ensure customer safety at branches, including limiting the number of customers it allows into the premises at any one time.

- Onboarded more than 370,000 customers on the RHB Mobile App in 2020, bringing the total number of onboarded customers to more than 679,000 (since post-launch of the banks’ new mobile app in April 2019).

- Employee experience

Through its Employee Value Proposition (EVP), RHB Group aims to drive and enhance its human capital. The bank’s end goal is to create a high-performing and inclusive workplace, one that empowers employees and leads them toward greater employee satisfaction and a higher retention rate. Here are some strategies the bank is taking:

- Re-skilling/upskilling employees through various development interventions, such as the RHB Managers Programme & Future Skills Programme.

- To ensure better preparedness in facing a future requiring the mastery of new skills in digitalisation, analytics, automation, customer preferences and risk management and compliance, RHB launched ‘Workforce of the Future Programme’. It aims to provide a structured approach to the upskilling of capabilities, thereby opening up new career progression opportunities within the group.

- RHB Group could strengthen its leadership pipeline through talent identification and assessment while accelerating the development of high-potential candidates to improve leadership bench strength.

- Managing human capital productivity through prudent headcount management, improving on its front office: back-office composition, and enhancing HR analytics and technology platform to increase productivity.

- Conducting roadshows to share its five-year strategic direction at RHB branches and via live updates on FB Workplace for continuous employee engagement.

- Conducting salary benchmarking exercises for comparison against the market and retention programmes.

- Conducting quarterly senior leadership forums and group-wide town halls. Such meetings aim to share the group’s strategic performance and achievements with senior leaders, as well as to provide ongoing information on key initiatives via live updates. Regularly communicating updates on COVID-19 pandemic-related matters to keep employees abreast of the latest developments in ensuring their health and safety.

- Enhance employee value proposition with high-impact initiatives including Health & Wellness, and drive engagement among the youth through the RHB Youth Council.

- Ensuring there strict adherence to Standard Operating Procedures (SOPs) within office and branch premises, allowing Work-From-Home (WFH) arrangements, implementing split operations for crucial functions, and allowing staff rotation at branches with shorter operating hours. RHB group and its employee engagement platforms:

- Intranet (My1Portal and MyLink2HR) and email

- The RHB Group internal social media channel, Workplace by Facebook and recognition via ThanksBot

- Social, sports, and recreational activities

- Engagement sessions during festive seasons

- Annual Employee Engagement Survey (EES) and Internal Customer Effectiveness Survey

- Formal and confidential grievance channel

- Formal meetings – GMD Chat Sessions and Townhalls conducted across the region

- Senior Leadership Forum

Key initiatives taken by RHB Group to enhance employee experience in FY 2020:

- Conducted an EES on an annual basis to gauge employees’ level of satisfaction and obtain feedback on areas for improvement. In 2020, the EES score improved from 90% to 92%.

- Implemented an enhanced Performance Management System (PMS) and improved the Group’s total rewards framework to be competitive in the market.

- Curated leadership, health, and wellness programs like- RHB Inspires, RHB Cares, RHB Progresses, among others, to promote workplace sustainability.

- Implemented FORWARD (Future-Oriented and Ready Workforce – Advancing, Reskilling and Developing) with a holistic look at the workforce of the future. It aims to enhance the professional standards and technical or functional competencies of employees.

- Introduced the RHB Wellness Programme for employees, aimed at promoting good health and mental wellbeing.

- In November 2020, RHB launched the RHB Wellness Hotline and Remote Therapy Programme to aid employees who needed help managing their stress levels and overall mental health.

- Organised mandatory IT security awareness training for employees and expanded the training programme to include Board members and third parties.

- Inaugurated RHB Digital Academy to provide digital-related foundational and upskilling training to more than 1300 RHB staff.

- Society and planet impact

- Risk Management

- The Group enhanced its risk management practices in 2020 by expanding on an Industry-specific ESG (Environment, Social and Governance) Risk Assessment (ERA) tool. It would include two more sectors – power or energy producers and cement manufacturing, besides the existing palm oil, oil & gas, as well as iron, steel and other metal manufacturing sectors.

- Collaborating and forging partnerships with non-profit organisations, associations or government organisations through the bank’s community engagement initiatives.

- Interacting and initiating discussions with related government bodies and Non-Governmental Organisations (NGOs).

- Encouraging proactive on-ground community engagement activities.

- Greenhouse gas emissions

- To manage its activities’ impact on the environment, the group expanded its Greenhouse Gas (GHG) emissions inventory and reporting coverage to include all main buildings and branches in West Malaysia.

- This step, along with various energy-saving initiatives, helped the group attain a 38% reduction in greenhouse gas emissions intensity per employee in 2020 compared to 2016.

- Green Financing

- The group aims to foster sustainable development whilst supporting its transition journey to a low-carbon economy.

- As of December 2020, the group had extended USD 0.76 billion in support of green activities through lending, investments as well as advisory and capital market activities.

- Value-Based Intermediation (VBI)

- Demonstrating its support of VBI principles, RHB Islamic Bank developed Malaysia and the Asia-Pacific’s first eco-friendly recycled plastic debit card. This move was to facilitate contributions that will aid the conservation of the marine ecosystem.

- This initiative was in line with UN SDG 14: Life Below Water and part of Ocean Harmoni, which also comes under the umbrella theme of RHB Harmoni. They initiate projects to conserve marine wildlife and habitats. As of December 2020, RHB Islamic Bank issued more than 20,500 cards.

Key initiatives taken by RHB to enhance society and planet impact in FY 2020:

- Rolled out the Money Ma$ter Programme, a structured financial literacy programme to educate students on managing their finances.

- Conducted online classes and educational sessions through social media for targeted B40 (Bottom 40% of the population based on income) students to ensure they could keep up during the pandemic.

- Nurtured and empowered children and youth from underprivileged segments through RHB X-Cel Academic Excellence and RHB X-Cel Star Scholarship programmes.

- Introduced the Payment Assistance Program in 2020. The Target Payment Assistant program, scheduled to be in place circa June 2021, will act as a follow-up plan.

- Committed to extend USD 1.23 billion by 2025, to support green activities and transition to a low-carbon and climate-resilient economy through either lending, advisory and investment activities.

- Facilitated the disbursement of relief funds for SMEs, such as the Special Relief Facility announced by Bank Negara Malaysia (BNM).

- Contributed funds through the Ministry of Health and Mercy Malaysia and various parties to assist front liners and vulnerable communities in Malaysia, Cambodia, and Laos.

- Reaffirmed its approach to sustainability and integration of ESG considerations through public disclosure (public documents, reports).

- Identified opportunities that will contribute to sustainable development and the transition to a low-carbon economy.

Digital Strategy

The group’s digital transformation journey aims to deliver convenience and create value for its customers. The group identifies opportunities and mitigates risks by investing in technology and channel improvements. It also delivers innovative products and services while encouraging digital consumption among customers.

- Fast-tracked the development of its digital payment platform solutions and digital enablement in RHB Group regional offices, particularly in Singapore and Cambodia.

- Enhanced compliance and security, including introducing the electronic Know-Your-Customer (e-KYC) process. This step will enable the bank to onboard customers through digital means quickly, efficiently, and safely.

- Invested in technological and digital initiatives that will differentiate the bank from its peers.

- Repurposed branch network while strategically expanding its overseas footprint.

- Trained more than 400 employees to be the digital leaders of the future.

Key initiatives in the year 2020 in lieu of the digital strategy include:

- Organisation-wide adoption and investment in analytics to enable customer-centric and cost-efficient banking products, solutions, and internal processes. RHB Group saw incremental benefits of USD 29.5 million from its analytics efforts:

- USD 25.8 million in revenue upliftment, due to increased cross-selling in retail and SME customers.

- USD 3.7 million in compliance cost avoidance due to improved compliance and risk management.

- Launched RHB Live FX @ Reflex, a digital foreign exchange (FX) service that offers real-time executed FX rates and seamless processing of spot and forward transactions.

- Rolled out the RHB SME ecosystem, integrating banking, HR, accounting, and payment activities on a single platform.

- Launched Malaysia’s first multi-currency debit card and a dynamic CVV code for credit cards.

IT Strategy

RHB Group refined its IT strategy to accelerate the digital innovation and modernisation of its IT infrastructure. Focus was centred on improving customer journeys and moving the bank’s digital channels from a transactional focus towards engagement and acquisition. To promote eco-efficient practices and manage natural resource consumption, there was an increase in the cost to adopt more modern and efficient technology in the group’s operations.

- The digitalisation and investment in the modernisation of its IT systems.

- Multiple rounds of investments in artificial intelligence, big data and robotic process automation to accelerate the speed of banking operations.

- Leverageing cloud technology by deploying new tools and collaborating with partners who leverage similar technology.

- Enhancing frameworks and policies relating to technology risks, including cyber risk management and IT security controls. The group also considered the new norms and the constantly evolving regulatory compliances for technology use.

- Subscribing to third-party IT security risk rating services as part of the bank’s third-party due diligence process.

IT initiatives for FY 2020 include:

Incorporated analytics-based systems that enabled the identification of potential mule accounts for anti-money laundering purposes

RHB Bank and its ICT contracts

- Sourced Group, to lead a cloud transformation journey.

- SOGO, to provide a convenient and seamless online platform for financing and payment solutions.

8 Growth and Innovation Opportunities

- #1 Cost to serve

- Malaysia’s economic growth in 2020 contracted alongside global economies, largely due to the impact of movement control orders imposed to contain the spread of the pandemic. The disruptions to economic and business activities, together with subdued consumer sentiment and border closures, led to Malaysia’s gross domestic product contracting by 5.6% compared to the 4.3% growth recorded in 2019. This change in macro-economic factors severely impacted the group’s bottom line with an 18.1% decline in its net profit of USD 501.8 million for the FYE 31 December 2020, from last year.

- The effect on the profits was mainly due to the impact of net modification loss and higher allowances for credit losses, including additional provisions set aside for potential COVID-19 impact. Consequently, profit for most business segments declined in the financial year under review.

- The group had a relatively stable cost-to-income ratio of 47.1% compared to 48% in the previous year. This percentage is 7% higher than the industrial average and 29.4% higher as compared to its regional competitors.

- The bank also increased its ECL provisions to absorb potential deterioration in asset quality due to the COVID-19 pandemic. Moreover, Net Interest Margins (NIM) also stood low at 2.12% because of the impact of OPR (Overnight Policy Reduction) cuts.

- The bank can optimise its operational model to increase profitability by focusing on the following areas:

- Expanding its data analytics capabilities to incorporate real-time monitoring of loan repayment risks

- Continuing to leverage its non-fund income and CASA deposit growth to balance out the negative effect of poor net interest margins and OPR reduction.

#2 Transformation of the branch and its branch networks

- RHB operates 364 branches and 1,744 self-service terminals in Malaysia. These include ATMs, cash deposit machines, cheque deposit machines, EPF kiosks, cash recycler machines, and coin deposit machines. The bank’s establishment costs including water, electricity, repair, maintenance, and rental of equipment and premises amounts to approximately USD 41 million, i.e., 4.2% of the bank’s total income.

- RHB needs to move from a traditional branch layout to a much more interactive, modern, and customer-friendly form. Compared to banks like OCBC and UOB that have built conducive customer branches (especially for the younger generation), RHB needs to reimagine its current branch strategy.

- To systematically optimise establishment costs and build a unique branch outlook for its customers, RHB Group needs to focus on the following areas:

- Revamp the entire branch outlook and make it more community-centric by introducing cafes or community centres. Customers can, therefore, easily identify various customer touchpoints and freely socialise with other customers within the branch.

- Expand the scope of self-service kiosks by introducing holistic ITMs (Interactive teller machines) that can handle routine customer queries initially answered through physical branch channels. This step saves time for customers and removes the effort needed to visit a branch physically.

- Build a hybrid omnichannel banking strategy to provide a personalised and immersive customer experience. The bank can start with its insurance and retail segment and later expand to other segments.

- #3 Customer experience

- With the intent of building the most optimum operating model that focuses on the customer journey, the bank should revisit its current customer-centricity strategy by laying special emphasis on agility, analytics and digital enablement,

- The bank has already witnessed the benefits of increased customer-centric analytical capabilities by virtue of USD 25.8 million in revenue upliftment. It should upscale its customer analytical capacities by focusing on:

- Understanding the customers’ behavioural patterns, life journey needs, and spending areas through AI and machine learning (ML) tools to build unique persona-based product portfolios.

- Introducing virtual assistants and real-time chatbots who can handle front-end customer grievances and come equipped with handling complaints in the region’s local language. This move will also help RHB Group reduce the turnaround time for complaint resolution to less than 24 hours, irrespective of follow-ups and query complexity.

- Gamifying customer touchpoints by incorporating animated dashboards to make the user experience more interactive and immersive.

- Increasing the use of predictive analytics and algorithms to show customers relevant products based on their preferences and saving or investing habits.

- Investing in building an intelligent credit application tool using natural language processing and big data analytics. This feature will help conduct a preliminary analysis of a customer’s creditworthiness using their past credit history, financial statements, and non-financial variables. The bank can reduce its credit card application process from 3 working days to immediate approval. It will also reduce the SME short-term loan, and overdraft financing needs processing from 3 weeks to less than one working day. RHB Group can use the credit application tool to support mortgage loan and home financing applications, along with digital document uploads and e-document signature to fast-track application turnaround from 5 working days to 1-2 working days.

- #4 Employee experience and productivity

- The bank should move beyond employee engagement scores to measure employee satisfaction. It could inculcate and practice employee empathy to create an employee-friendly culture and a holistic employee wellbeing framework. Furthermore, RHB Group should use suitable technologies for its employee upskilling and development programs.

- RHB Digital Academy, a vital component of the bank’s digital transformation journey, aims to expose and educate participants on the knowledge and skillsets that are critical to support this transformation. The bank has a lot of potential in terms of improving its employee training and development strategy. It could:

- Prepare its employees for future roles by incorporating comprehensive design thinking into existing training modules.

- Revisiting its existing pedagogy and introduce virtual learning using augmented data insights on the learner’s existing knowledge and experience. By doing so, RHB Group can provide personalised learning modules according to a learner’s capabilities.

- Break down existing training modules into easily consumable content forms (like podcasts, short videos, etc.) so that employees can learn at their convenience, pace and time.

- Develop a comprehensive recognition mechanism for the equitable distribution of rewards, benefits and promotions.

- To enhance employee wellbeing, the bank can do more than its existing system of rewards and benefits, which includes performance link pay to personal, housing and motor loans. Options include:

- Sponsoring volunteer ship programmes to build a more empathetic and ethical workforce.

- Sponsoring 100% of the education loans of its employees to attract and retain the fresh graduates the bank hires, thereby controlling the employee attrition rate.

- Roll out special maternity and paternity leave for employees with children, as well as financial support for single parents and parents of children with special needs.

- Appoint a liaison for mental health and meditative programs with targeted mental, emotional, spiritual, and physical wellbeing.

- #5 Migration of workload to the cloud

The bank’s cloud strategy is to partner with third-party vendors for infrastructure-as-a-service (AWS cloud). This step will allow the migration of workloads and software-as-as-service solutions (e.g., Sourced Group) to build, test, and deploy customer solutions. To complement their existing cloud strategy and build a robust cloud framework, RHB Group needs to incorporate the following:

- Apart from cloud solutions in specific regional markets, the bank needs a well-defined and multi-dimensional hybrid cloud strategy. It should aim towards building cloud-native solutions for its entire ASEAN network by creating efficiency in credit approvals, foreign exchange management, and customer query and complaint management.

- The bank should leverage its virtual private cloud infrastructure to optimise data-driven activities across compliance, auditing, and pan-organisation communication channels.

- The bank can capitalise on success from cloud-native product/solution hackathons (Construct on, Cambodia 2021) in other regional operating locations.

- #6 Neo banking

- The current RHB mobile banking app provides basic facilities of fund transfers and bill payments along with slightly advanced features. These include RHB Pay Anyone (which allows customers to transfer funds almost instantly to anyone via mobile phone, email or Facebook) and RHB Now Secure Plus (which ensures transactional security).

- With customers moving to neo banking and the lack of proficient digital-only platforms in Malaysia targeting the growing millennial and GenZ population, the banks need a definitive neo banking strategy that should be separate from its current digital banking app and platform. To do so, RHB Group needs to focus on the following:

- Aiming to create a separate neo banking brand name, which can be done by partnering with a suitable fintech firm, to position itself strategically among the millennials and Gen Z.

- Introducing byte-sized loan and investment products which gives customers increased flexibility to navigate through different product options.

- Recreating the design outlook of its digital banking app and platform by making the design theme more unique and intuitive and inculcating interactive dashboards.

- Customising its product stack and personalising it for the customer based on their life journey – student, executive, pursuing marriage, or planning a family, among others.

- #7 Artificial Intelligence (AI) in everything

To build analytics-based systems, RHB needs to optimally leverage AI and ML, starting with automating non-core functions and then incrementally moving towards core business functions. In order to create a comprehensive AI footprint, the bank needs to focus on the following areas:

- Automating labour-intensive backend and iterative daily tasks, like customer on-boarding, document collation, book-keeping, sales recording, etc., through robotic process automation (RPA).

- Incorporating predictive threat monitoring and risk detection mechanisms for fraud and money laundering, insider threat, and cyber risks.

- Using natural language processing (NLP) for digital biometric customer verification for customer profiling to acquisition strategies. The bank can further use NLP in deploying chatbot and automating customer application approval and processing.

- #8 Cybersecurity

RHB aims to enhance its technology and cyber risk management frameworks and continue strengthening its IT security controls to keep up with the constantly evolving technology landscape. In line with the initiatives already taken by RHB, it should focus on the following measures to strengthen the group’s security footprint:

- Automating regular security functions such as threat monitoring, identity access management, controlling and reporting mechanisms to make the overall security framework more transparent and smoother.

- Regular screening of data silos using AI-ML to check for the misconfiguration of firewalls, data leakage and data manipulation. These steps will help ensure that there is data integrity at all points in time.

- Incubate new and advanced security tools and cloud-based security instruments by testing in a safe sandbox environment, locating operational and security fallouts in the current security framework.

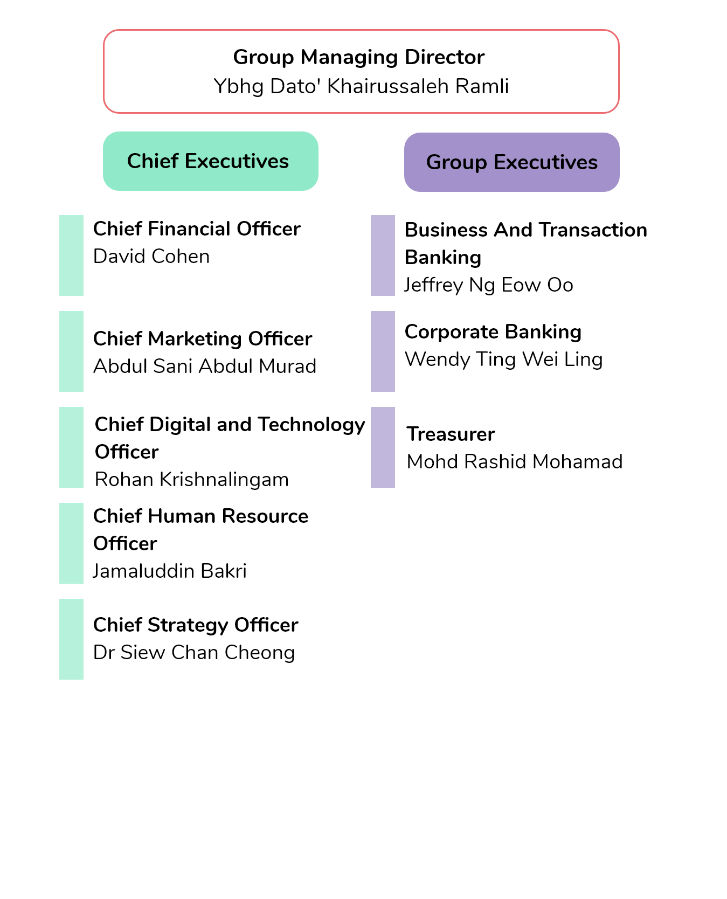

Organisation structure: Leadership

Executive Profile

Tan Sri Ahmad Badri Mohd Zahir

Chairman

Tan Sri Ahmad Badri Mohd Zahir (“Tan Sri Ahmad Badri”) started his career as a Senior Valuation Executive at C.H. Williams, Talhar & Wong Sdn Bhd. Followed by the appointment as the Assistant Secretary in the Finance Division of the Ministry of Finance in 1989. He served with the Ministry of Finance for nearly 30 years in various capacities, the last being the Secretary-General of Treasury.

Tan Sri Ahmad Badri held the position of the Chairman of the Employees Provident Fund starting 1 May 2020. He sat on the EPF Investment Panel since 2014 and has vast experience in the fields of strategic investment, loan management, financial market and actuarial science.

Tan Sri Ahmad Badri previously served on the Boards of Bank Negara Malaysia, Kumpulan Wang Persaraan (Diperbadankan), Permodalan Nasional Berhad and Tenaga Nasional Berhad, among others.

Ybhg Dato’ Khairussaleh Ramli

Managing Director

Dato’ Khairussaleh Ramli (“Dato’ Khairussaleh”) was appointed as Managing Director of RHB Bank Berhad and Deputy Group Managing Director of RHB Banking Group on 13 December 2013. His next appointment was the Group Managing Director/Group Chief Executive Officer of RHB Banking Group on 5 May 2015.

Dato’ Khairussaleh sets the Group’s vision and strategic direction while defining and shaping the bank’s corporate culture and brand values. He leads the Group in managing its businesses and operations to achieve set targets and goals and maximise the Group’s return on capital invested.

Dato’ Khairussaleh has more than 25 years of experience in the financial services and capital markets industry, where he held senior positions in well-established regional financial institutions.

Syed Ahmad Taufik Albar

Chief Financial Officer

Syed Ahmad Taufik Albar was appointed as the Group Chief Financial Officer on 1 December 2016. Taufik leads Group Finance and ensures the effectiveness of the various finance functions across the Group. Tasks include budgeting, reporting, capital and balance sheet management, taxation, procurement and recovery.

Taufik has more than 2 decades of experience as an accountant and a finance professional with domestic and international exposures. The said exposure includes oil & gas, mobile telecommunications and infrastructure, as well as property development and construction. He began his career in finance with Shell and worked in various Shell offices in Malaysia, Australia and the Netherlands. Prior to joining RHB, he was the Group Chief Financial Officer of UEM Group Berhad and Chief Financial Officer of Smart Axiata (Cambodia).

Rohan Krishnalingam

Chief Digital & Technology Officer

Rohan Krishnalingam has been the Group Chief Digital and Technology Officer since 1st August 2019. Krishnalingam is responsible for providing accurate and timely technology and back-office operations and services support for the relevant business and functional units. He has also helped develop the IT and Digital Strategy towards driving the implementation of Digital and IT transformation, led the efforts on digitisation of RHB Banking Group, and driven the adoption of Agile@Scale as part of RHB Group’s strategic focus to create a successful operating model.

Jamaluddin Bakri

Chief Human Resource Officer

Jamaluddin Bakri was appointed as the Group Chief Human Resource Officer on 1 July 2013. In his current role, he is responsible for developing and executing long-term Human Resources (HR) strategies as well as build HR capability that will be able to support the Group’s long-term strategic goals. He is also responsible for managing various HR functions across the Group. Tasks include strategic planning and also organisational development, human capital development, succession planning, rewards as well as performance management that will align with the group’s Business Strategies.

Jamaluddin brings more than 20 years of solid track record in HR functions, having over 15 years overseas. He gained experience working with different nationalities, as well as its diverse cultures and working styles. Bakri has also partnered with business leaders of multinational and local organisations in driving various HR strategies globally and locally.

Dr Siew Chan Cheong

Group Chief Strategy Officer

Dr Siew Chan Cheong was appointed as Group Chief Strategy Officer on 2 May 2019. He is responsible for driving the strategic priorities of RHB Group. Achievements include supporting strategy teams within each business unit in the development of business-specific strategies to drive improvement in financial and strategic outcomes. He develops and refines value-based portfolio management of the Group, drives top-down change initiatives (FIT22 Strategy Execution) and spearheads the Group’s annual business planning.

Dr Siew has more than 19 years of experience developing strategy and implementing large-scale transformation programmes, especially for financial services providers across Europe and Asia. He has also developed and implemented strategies for large global and regional banks and insurance firms, covering business growth, operational improvement, talent and technology strategies. Before this appointment, he was the Senior Director for Financial Services with Strategy & (formerly Booz & Company), which is part of the PwC network, serving financial services clients across South East Asia.

Appendix A

twimbit Purpose Index

We evaluate Asia Pacific’s top banks to understand whether their strategic objectives, market positioning, and operational efficiency align with continued sustainability and profitability. In evaluating the respective bank’s focus areas and performance, we base our analysis on five purpose pillars and score each bank on them.

Endnotes

RHB Banking Group Limited, (2020, December 31), Annual Report.

https://www.rhbgroup.com/~/media/files/malaysia/investor-relations/annual-reports/rhb-ir20-final-pdf.ashx

RHB Banking Group Limited, (2020, December 31), Financial Statements.

https://www.rhbgroup.com/~/media/files/malaysia/investor-relations/annual-reports/rhb-integrated-report-2020-financial-statements.ashx

RHB Banking Group Limited, (2020, December 31), Investor Presentation.

https://www.rhbgroup.com/~/media/files/malaysia/investor-relations/annual-reports/rhb-ir20-interactive-pdf.ashx