1. Key highlights

A. Key takeaways

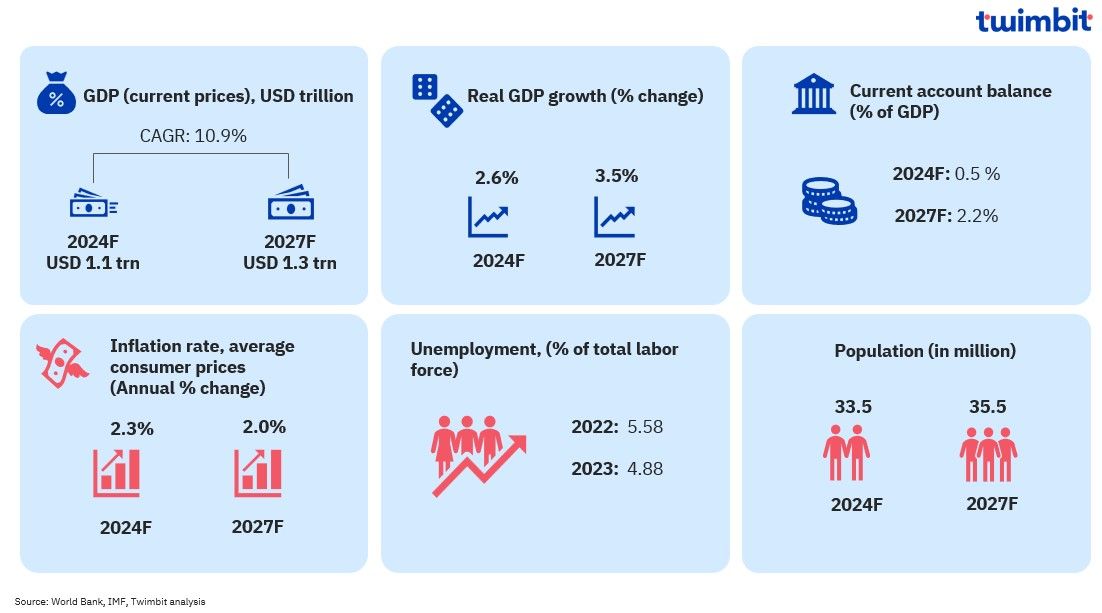

- As the economic leader of the Middle East, the KSA (Kingdom of Saudi Arabia) is projected to have a GDP (current prices) of USD 1.1 trillion in 2024. Fostering a thriving digital landscape, Saudi Arabia has emerged as a leader globally and within the Arab region.

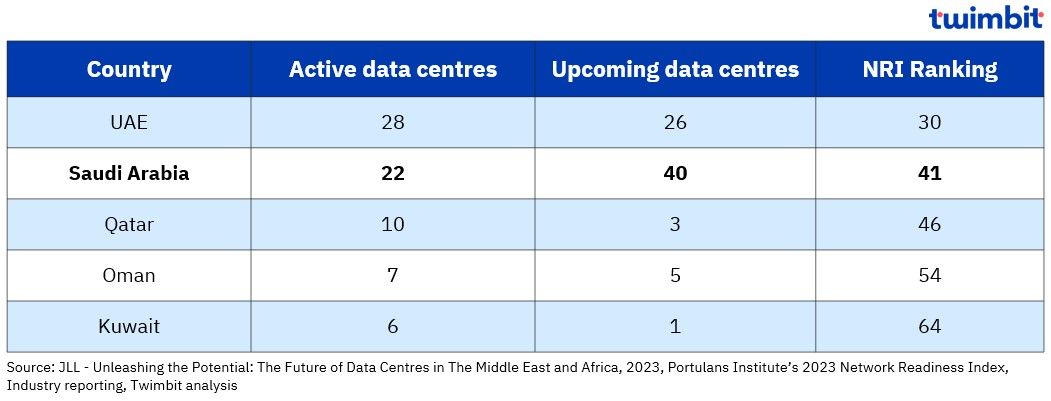

- According to the Portulans Institute’s 2023 Network Readiness Index, Saudi Arabia ranked 41st globally (out of 134) and 2nd in the Arab region (following the UAE at 30th).

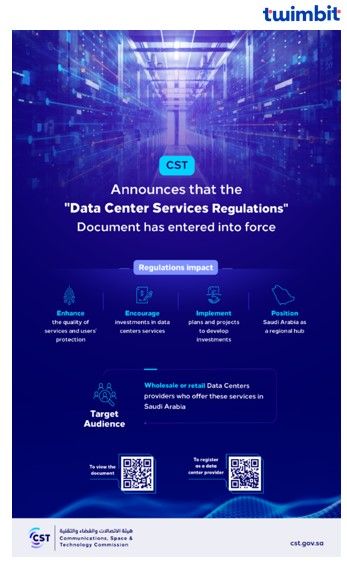

- Saudi Arabia’s CST (Communications, Space, and Technology) Commission implemented new regulations for wholesale and retail service providers in January 2024 for data centre growth alongwith stimulating investment, fostering competition, and optimizing IT infrastructure utilization.

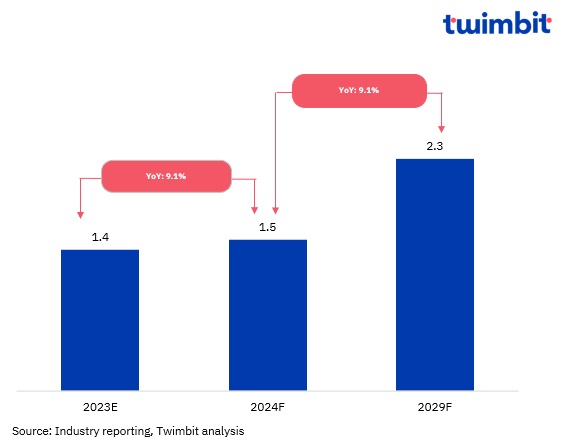

- As per industry estimates, the Saudi Arabian data centre market is expected to experience a robust compound annual growth rate (CAGR) of ~8.1% from FY-2024 to FY-2029, reaching a market size of USD 2.3 billion.

- A confluence of factors drives the Saudi Arabian data centre market:A stable expanding economy, strategic government initiatives and favourable environmental factors.

- A stable expanding economy, strategic government initiatives and favourable environmental factors.

- Ongoing digital transformation efforts paired with robust regional and global connectivity.

- Growing interest and investment from leading technology vendors.

- Competitive electricity tariffs, readily available raw materials, and a solid national digital infrastructure presence.

- Ongoing submarine cable deployments enhance Saudi Arabia’s robust and expanding connectivity infrastructure.

- Saudi Arabia boasts nearly 15 submarine cables, with an expected addition of 6 more cables by 2025.

- A diverse range of stakeholders characterise the Saudi Arabian data centre market. These include:

- Established local players

- Government entities actively participating in the market’s development

- Telecommunication companies leveraging their expertise

- A growing influx of new entrants

- Riyadh and Jeddah are the prominent data centre hubs, while Dammam and Neom represent promising emerging markets. Tier 3 and Tier 4 data centre categories dominate the Saudi Arabian market.

- Prominent trends driving the Saudi Arabian data centre market includes:

- 5G coverage expansion by telcos continue to drive demand for robust data centre infrastructure to support growing data needs

- Saudi Arabia’s Data centre market continues to grow, fuelled by Innovation and Investment be leading technology vendors

- Sustainable solutions for Saudi Arabia’s Data centre landscape gain traction, as its aims for net-zero by 2060

- Saudi Arabia data centre market tightens amidst strong regional demand

- Saudi Arabia shifts data centre investments from traditional hubs to emerging tech cities like Neom and Al Khobar.

B. Market opportunities

Vision 2030 positions Saudi Arabia for rapid growth. By fostering innovation-friendly regulations and attracting top global operators, Saudi Arabia is creating a robust environment for data centres. The growing AI and cloud sectors further boost demand for these services. Additionally, the region’s low energy costs provide a significant competitive advantage for data centre businesses.

The region’s growing AI and cloud sectors drive high demand for data centre services. Combined with the region’s low energy costs, this creates a strong competitive edge for data centre businesses.

1. Opportunities for Telcos

High mobile penetration rates of 130% limit growth in connectivity services, pushing telcos to diversify. B2B techno-services like cybersecurity, AI, cloud and data centres, and IoT offer new diversification opportunities.

Co-location partnerships, like the telecom tower model (where telcos offset their tower business), can create new revenue streams by offloading data centre workloads. This enables telcos to maximize their data centre assets and drive Saudi Arabia’s digital future.

2. Opportunities for Cloud Providers

Saudi Arabia’s digital transformation is driving rapid data centre expansion. Tech giants Google, Azure, and AWS are increasing their presence to improve service delivery and reduce latency. Cloud data centres offer businesses enhanced scalability, flexibility, and cost-efficiency. Growing cloud adoption is fueling demand for data centre capacity.

3. Opportunities for Data centre Providers

Growing digital consumption is increasing the environmental impact of data centres. To mitigate rising energy consumption and carbon emissions, industry must prioritize efficiency, energy reduction, and renewable energy adoption. Leading cloud providers, such as Apple and Google, have achieved carbon neutrality, while others have set ambitious targets. Sustainability is also a focus for colocation providers due to internal commitments and external regulatory pressures.

4. Opportunities for Telecom Vendors

The data centre market surge has created a strong interdependence between telecom vendors and telecom players. Leveraging their existing network infrastructure and expertise in data transmission, telecom companies can provide essential services such as high-performance connectivity, robust security, and edge computing for data centres. By fulfilling these critical needs, telecom vendors solidify their position as vital strategic partners for mutual success in the digital era.

5. Opportunities for IT Vendors

The data centre market expansion has accelerated IT vendor growth in Saudi Arabia, driving infrastructure expansion and new service offerings. Technology companies are better positioned to meet increasing data storage and processing requirements. The rapid expansion has also necessitated optimizations in data centre performance, scalability, compliance, and security.

Technology vendors are leading innovation, addressing customer needs through advanced solutions that enhance efficiency, security, and energy consumption. Their expertise in commissioning, consulting, and monitoring is crucial for digital transformation and global online service delivery.

2. Understanding the market

A. Macroeconomic insights

Increased hydrocarbon output and non-oil sector contributions (tourism, manufacturing, and logistics) aim to project a robust trajectory in Saudi Arabia’s economy through 2025-2028.

Exhibit 1: Saudi Arabia macro-economic indicators

In 2023, Saudi Arabia’s digital economy reached ~USD 123 billion, contributing nearly 14% to GDP. This growth reflects the widespread adoption of cloud computing services by approximately 48% of establishments.

Exhibit 2: Network Readiness Index (NRI) 2023 ranking – Arab countries

According to the Portulans Institute’s 2023 Network Readiness Index, Saudi Arabia ranked 41st out of 134 economies globally and 2nd in the Arab region (behind UAE, ranked 30th).

B. Regulatory landscape

Saudi Arabia’s regulatory environment for data centres has significantly improved following the implementation of the Data Centre Services Regulations by the Communications, Space, and Technology (CST) Commission on January 1, 2024. These new regulations have facilitated stronger partnerships between data centres, wholesale, and retail service providers.

Primary objectives of the regulations

- Conducive environment to the anticipated growth in the data centre sector.

- Promoting advanced and environmentally friendly data centres.

- Enhance development of Saudi’s IT infrastructure to create attractive environment for technology investments.

Obligations of registered service providers

- Must maintain valid registrations, certifications, and commercial registrations.

- Responsibilities include physical security, transparency in financial fees, SLAs, and quality standards.

- Liability provisions, customer notifications, and cooperation in case of data centre shutdown

Regulatory Mandates

- The registration holds a validity period of 3 years, with the provision for renewal. There are no fees for obtaining and renewing the registration, indicating a supportive regulatory environment.

- Tier 1: Registrations for Tier I data centres are under the limited category, restricted only to existing facilities and cannot be issued for new facilities.

- Tier 2 & 3: Tier II (Standard) and Tier III (Advanced) data centres are to be Carrier Neutral, and the service providers must furnish energy management and sustainability plans.

3. Opportunities in the Saudi Arabia Data Centre Market

A. Saudi Arabia Data Centre Market Size and Forecast, 2023 – 2029F

Over the next 2-3 years, the influx of capital from established and emerging market players is expected to drive robust data centre investments in Saudi Arabia.

Exhibit 3: Saudi Arabia Data Centre Market Size in USD Billion from 2023 – 2029

The Saudi Arabian data centre market is projected to reach USD 1.5 billion in FY-2024, reflecting a year-over-year (YoY) growth of 9.1%. This robust trajectory is underpinned by a coming together of multiple factors including a stable prevailing macroeconomy, government-led digital initiatives, enterprise digital transformation endeavors, and the nation’s ongoing investment in digital infrastructure (FTTH and 5G).

The market is anticipated to sustain a compound annual growth rate (CAGR) of approximately 8.1% over FY2024-2029, culminating in a market valuation of USD 2.3 billion.

Riyadh and Jeddah have emerged as primary data centre hubs in Saudi Arabia, with Dammam and Neom demonstrating significant growth potential.

The region’s focus on wholesale colocation has attracted major cloud providers such as Google, Alibaba, Oracle, and Huawei. This influx of cloud services will support the evolving needs of both public and private sector organizations.

B. Key Drivers of the Saudi Arabia Data Centre Market

1. Stable and growing Saudi Arabia’s economy is expected to outperform most Arab nations by 2027

Saudi Arabia is the 16th largest economy globally among G20 nations and maintains its leadership position in the Middle East. This economic dominance is projected to strengthen, with GDP expected to grow from USD 1.1 trillion in FY-2024 to USD 1.3 trillion by FY-2027.

Concurrently, other factors indicate immense potency for Saudi Arabia to outperform most Arab nations. These factors include:

- Anticipated decline in average consumer price inflation from 2.4% in FY-2024 to 2% by FY-2027

- A forecast in accelerated real GDP growth from 2.6% in FY-2024 to 3.5% in FY-2027

This GDP growth is expected to rank 2nd only to the UAE’s projected 4.5% growth rate among the leading Arab economies (UAE, Qatar, Oman, Bahrain, Kuwait, and Jordan).

2. Strategic and favourable Government initiatives favour sustained data centre market growth

Saudi Arabia is rapidly expanding its renewable energy sector. The King Salman Renewable Energy Initiative and the National Renewable Energy Program aim to power over half the country with clean energy by 2030.

To achieve this, the Government is combining renewable energy with data centre growth. Special Economic Zones, Free Trade Zones, and smart cities will be developed to support this strategy. Riyadh will remain the primary data centre hub, while cities like Jeddah, Dammam, and Neom will attract significant investment.

A new Cloud Computing Special Economic Zone will accelerate data centre development through tax breaks, reduced fees, and lower energy costs. Additionally, a USD 18 billion initiative will create large-scale data centres across the country, targeting 1.3 gigawatts of capacity.

This initiative will help accommodate sectors to the ever-expanding investment landscape. For instance, while Riyadh, Jeddah, and Dammam have traditionally been data centre hotspots, Neom’s planned USD 500 billion digital infrastructure investment is poised to reshape the sector.

3. Digital transformation across enterprises propels data centre demand

Saudi Arabia’s IT landscape is undergoing a transformative evolution, underpinned by strategic initiatives such as Vision 2030, the National Transformation Program, and the Saudi Data and Artificial Intelligence Authority. These frameworks have been instrumental in shaping the Kingdom’s technological trajectory.

The Saudi Data and Artificial Intelligence Authority is at the forefront of accelerating AI adoption through substantial investments. Its mandate extends to bridging the chasm between government agencies and the private sector, fostering a collaborative ecosystem for AI innovation.

Concurrently, cloud computing is emerging as a key driver of data centre expansion within the Kingdom. The cloud’s inherent attributes of flexibility, scalability, and cost-efficiency are compelling enterprises to migrate their IT infrastructure. Consequently, the demand for robust data centre facilities is surging to support the growing cloud ecosystem.

4. Presence of strong regional global connectivity

Saudi Arabia possesses robust terrestrial connectivity to key regions encompassing APAC, Europe, and the Middle East. The nation currently leverages a network of approximately fifteen submarine cables and is strategically expanding its subsea infrastructure with an additional six cables slated for completion by 2025. Jeddah serves as the primary landing station for these cables, complemented by additional landing points in Al Khobar, Duba, Haql, and Yanbu.

5. Growing interest from leading technology vendors, including hyperscalers

Saudi Arabian data centre continues its line of initiatives to improve and enhance itself. These include:

- Substantial investments from local, government and telecom entities.

- Transitioning established players such as Center3 (stc), Mobily, and Gulf Data Hub into prominent co-location operators.

- Ensuring opportunities for new entrants like EDGNEX Data Centres, Quantum SwitchTamasuk and Agility to expand their global footprint.

The growth trajectory is further bolstered by the strategic interest of global hyperscalers like Oracle Cloud, Google Cloud, and Microsoft which view the nation as a lucrative market for cloud service expansion and a regional investment hub. Recent prime investment in Saudi Arabia includes opening of data centre by AWS in 2026 and Google’s announcement to launch a new Dammam Cloud region.

6. Competitive electricity tariffs provide a cost advantage

Abundant fossil fuel reserves in KSA have contributed significantly to lower electricity costs, making it an attractive destination for data centre investors.

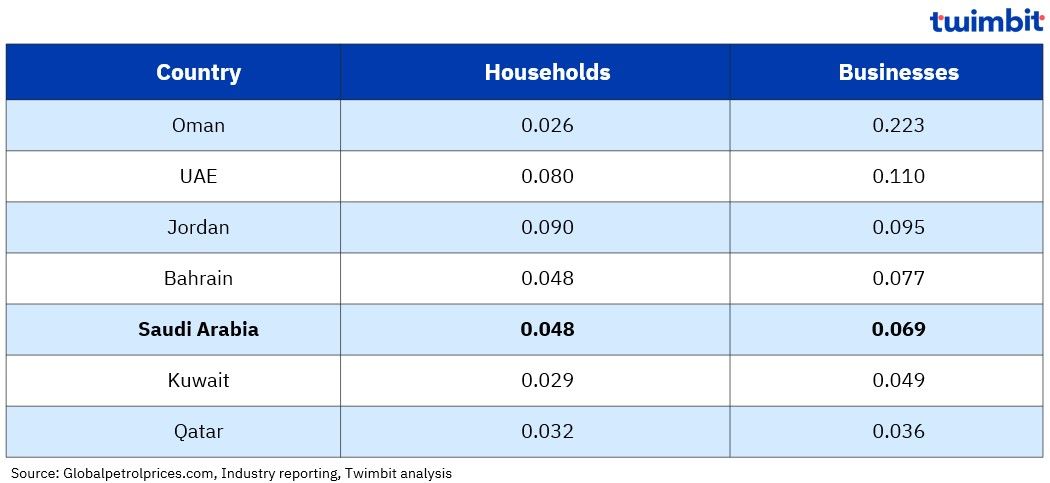

Exhibit 4: Electricity prices across key Arab countries in USD/kWh, Dec-2023

Saudi Arabia ranked 4th among its competitors, with a residential rate of SAR 0.180/ kWh (USD 0.048/kWh) and a commercial rate of SAR 0.257/kWh (USD 0.069/kWh).

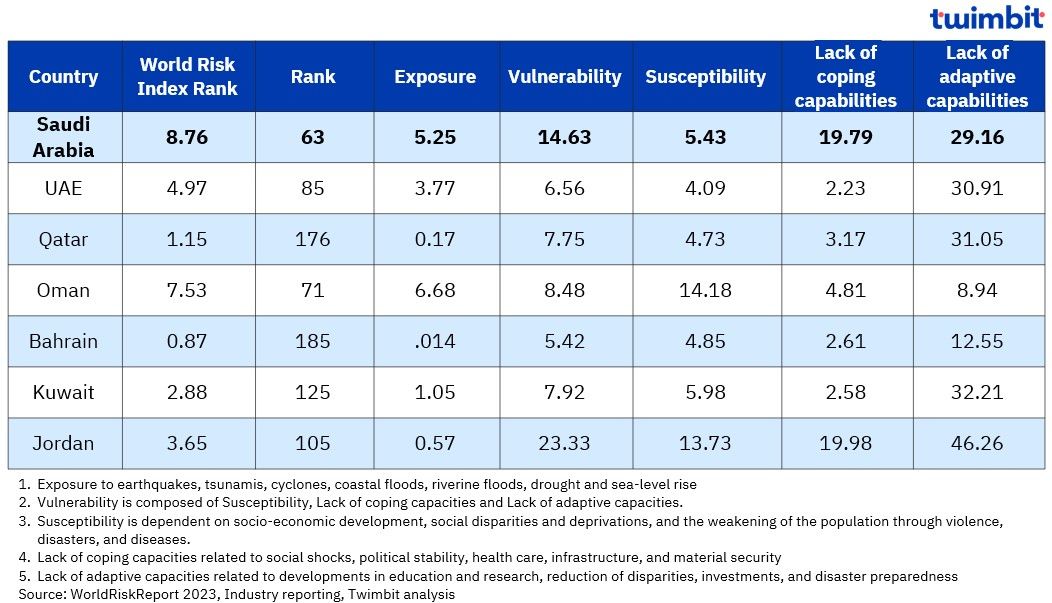

7. Favourable environmental factors offer operational advantages

Thought not too prone to natural disasters, Saudi Arabia is still prone to other environmental factors such as water contamination and increased nitrogen oxide emissions. It was ranked 63rd globally, with an index of 8.76 as World Risk Report 2023.

Exhibit 5: World Risk Index of Arab Countries, 2023

8. Presence of raw materials mitigates construction costs

Real estate developers capitalise on the growing data centre market by providing essential infrastructure like physical space, power, and connectivity.

This symbiotic relationship offers significant growth opportunities – increased investments, job creation, and urban development.

Additionally, Saudi Arabia’s abundant raw material resources have helped overcome the high construction costs of new data centre projects.

9. Nationwide digital infrastructure boost driven by tech-savvy population and government support that fuels data centre growth

The proliferation of digital devices, social media platforms, e-commerce marketplaces, and IoT applications has necessitated the emergence of robust data centre infrastructure capable of efficiently storing, processing, and analysing vast datasets. This surge in demand is underpinned by

- Burgeoning tech-savvy population

- Surge in the smartphone and internet penetration rates

- Meteoric rise of social media and e-commerce platforms within Saudi Arabia.

These factors collectively present a lucrative opportunity for data centre providers to capitalize on the exponential growth of data.

Moreover, the Saudi Arabian government’s strategic focus on attracting foreign investment and economic diversification has created a conducive environment for international data centre players. The influx of global expertise and advanced technologies is poised to significantly enhance the domestic data centre landscape.

C. Key Challenges of Saudi Arabia Data Centre Market

1. Lack of skilled workforce poses data centre growth challenges

Saudi Arabia’s data centre market is undergoing exponential growth, aligned with the ambitious objectives outlined in Vision 2030. However, the realization of this potential is impeded by a pronounced dearth of critical talent. The industry is grappling with a significant shortage of qualified personnel adept in data centre operations and management, which is adversely impacting facility efficiency.

Some of the key factors which contribute to this talent scarcity includes

- The domestic talent pool possessing requisite data centre management experience is limited, creating a substantial gap between supply and industry demand.

- Additionally, the prevalence of English as the lingua franca within the data centre domain poses challenges for Saudi Arabian professionals.

- The unique operational environment and potential relocation requirements inherent to data centre roles may also deter a segment of the workforce.

Furthermore, while the nation’s commendable nationalization initiatives aim to enhance Saudi participation, they concurrently present hurdles for organizations. Identifying and nurturing a domestic talent pipeline within the specialized domain of data centre operations has emerged as a formidable challenge.

2. Elevated capital expenditures and operational expenses pose significant barriers to data centre development

In 2023, premium construction costs averaged ~USD10 million per MW in the KSA. This represents a substantial premium of nearly 20% compared to regional counterparts such as the UAE. Moreover, the acquisition of suitable land parcels has led to increased upfront investments.

The power grid infrastructure in certain regions also required upgradation. This can deter operators from pursuing hyperscale data centre projects. As a result, they would need to invest heavily in UPS systems and generators.

3. Cybersecurity threats necessitate the requirement of robust security protocols to safeguard critical information

Data centres bear inherent vulnerability due to the storage of sensitive data. Hence, robust security protocols are necessary to safeguard critical information.

Increasing cyber-attacks have also prompted data centres to implement the latest and most advanced security measures, ranging from firewalls and encryptions to intrusion detection systems.

Recent research from Tenable highlights that nearly 40% of cyberattacks against Saudi Arabia during 2022 and 2023 were successful. 62% of respondents also identified cloud infrastructure as a high-risk area within their organisations.

4. Saudi Arabia’s data centre industry faces significant environmental and operational hurdles

Saudi Arabia ranked higher than its Middle Eastern counterparts in exposure and vulnerability (World Risk Report 2023). This is because the arid climate, water scarcity and extreme temperatures have hindered Saudi Arabia’s efforts to achieve eco-friendly operations and efficient cooling.

Other hurdles include the corrosive nature of sandstorms that can accelerate the deterioration of cooling and mechanical systems. As a result, this can lead to increased operational expenses and reduced equipment lifespan in data centre infrastructure.

Hence, data centre operators need to focus on energy-efficient cooling solutions and environmentally responsible practices. However, the lack of advanced cooling technologies currently adds difficulties in Saudi Arabia’s pursuit for environmental sustainability.

D. Global submarine connectivity

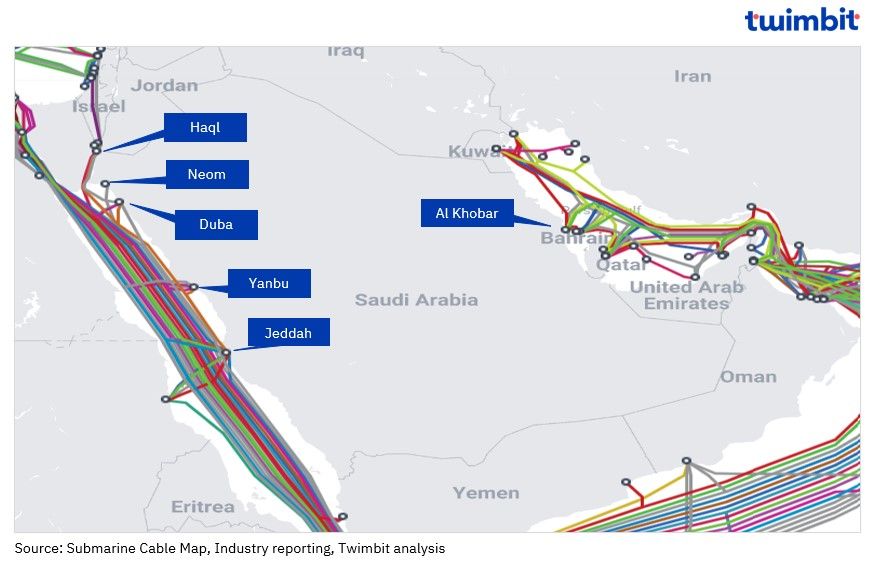

Saudi Arabia stands as a leading data centre market in the Middle East, characterised by robust and expanding connectivity facilitated by ongoing submarine cable deployments. The nation’s strategic geographic position between Asia, Africa, and Europe grants it privileged access to the numerous subsea cables traversing the Red Sea and the Persian Gulf.

Exhibit 6: Saudi Arabia global submarine cable connectivity, Q2-2024

Saudi Arabia is connected to nearly 15 submarine cables as of date, with most of the landing points in Jeddah in addition to Al Khobar and Duba.

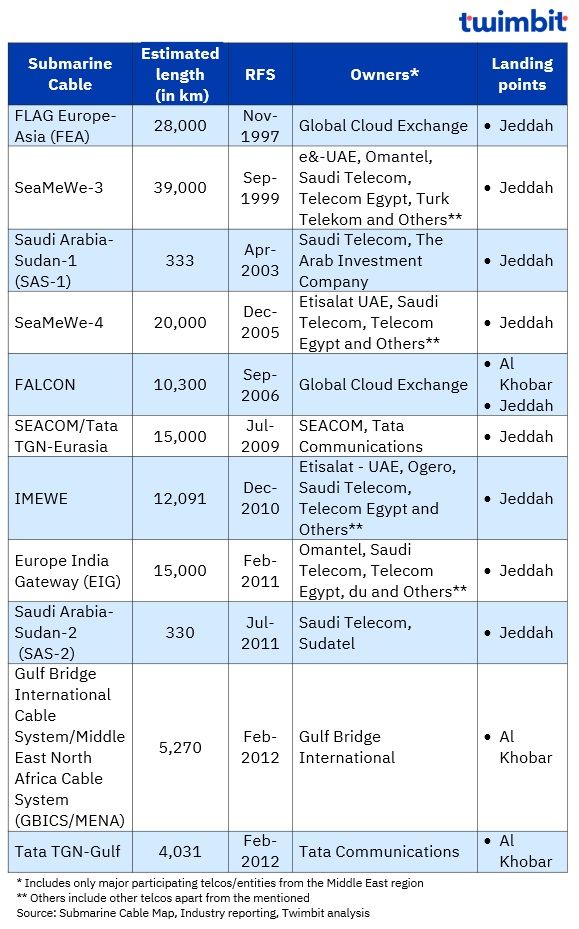

Exhibit 7: List of Submarine cables connecting Saudi Arabia, Q2-2024

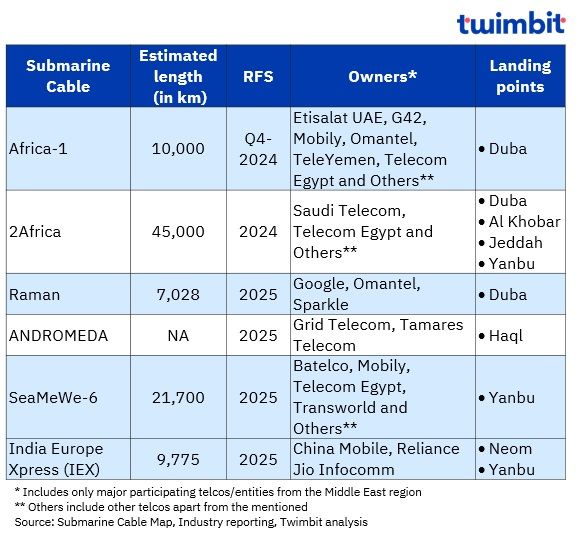

There are 6 upcoming submarine cables expected by 2025, with landing points expected in Duba, Haql, Yanbu and Neom. This will help enhance the country’s submarine cable connectivity of the country with other external geographies.

Exhibit 8: List of upcoming Submarine cables connecting Saudi Arabia, Q2-2024

4. Competitive landscape

Saudi Arabia’s data centre market thrives with Vision 2030, with global and local providers enhancing competitive intensity.

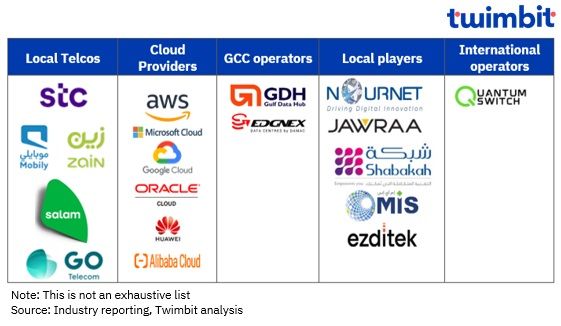

Established co-location operators such as Saudi Telecom Company (stc), Mobily, Gulf Data Hub, NourNet, and GO Telecom (Etihad Atheeb Telecom) maintain a strong market presence. The growth is further supported by global giants. Google’s recent partnership with Aramco to establish a cloud and data centre region exemplifies this trend.

The sector is further invigorated by the influx of new entrants, actively developing data centre facilities or announcing their imminent entry. EDGNEX Data Centres by DAMAC, Quantum Switch Tamasuk, and Agility represent some of the prominent newcomers poised to shape the market landscape.

Exhibit 9: Key players in the Saudi Arabian Data Centre market, Q2-2024

The market anticipates a surge in hyperscale data centres. A prime example is Quantum Switch Tamasuk’s (QST) ambitious project. It aims to develop six facilities across key cities like Jeddah and Riyadh, with a combined power capacity of 300 MW by 2026.

The rise of edge computing and AI will also necessitate localised data processing, creating opportunities for smaller, specialised data centres. With its strategic location and government backing, Saudi Arabia is poised to become a regional data centre powerhouse, attracting both domestic and international players.

Riyadh and Jeddah lead in terms of the number of data centres present. Tier 3 and Tier 4 data centre categories dominates the Saudi Arabian market, with data centre providers predominantly operating/owing nearly 60% of the data centres.

Exhibit 10: List of Data centres in Saudi Arabia, Q2-2024

5. Key strategic developments

A. Key partnerships in Saudi Arabia Data centre market

- Several key partnerships are propelling Saudi Arabia’s data centre market forward. Collaborations between domestic and international companies are establishing a robust cloud infrastructure, fostering innovation in areas like gaming and construction, and enhancing data centre capabilities.

- This growth is fueled by select major partnerships involving major players like Oracle, Google Cloud, and Tencent, solidifying Saudi Arabia’s position as a regional technology leader.

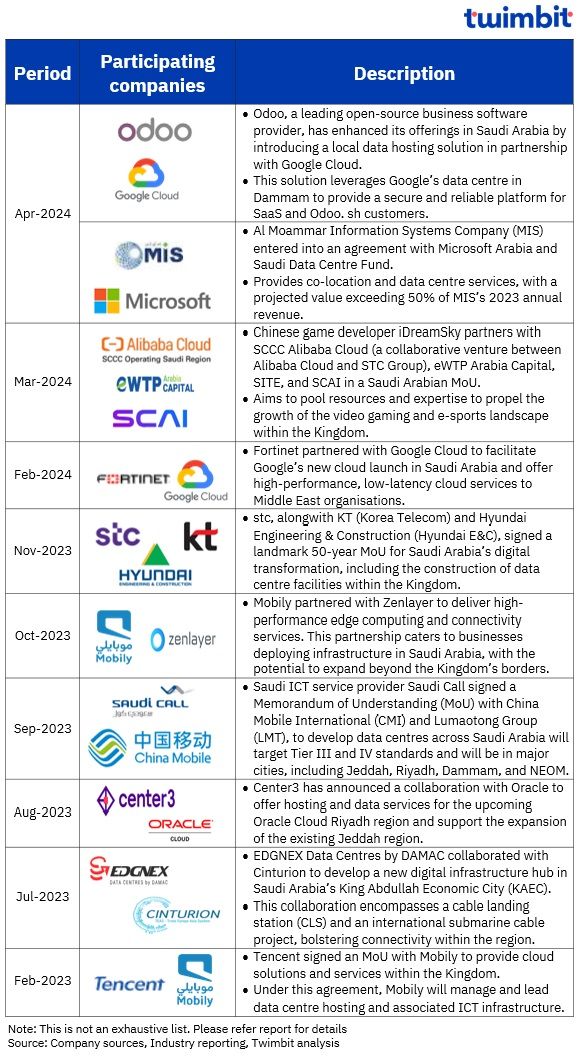

Exhibit 11: Key partnerships in Saudi Arabia Data centre market

B. Key contracts in the Saudi Arabia Data centre market

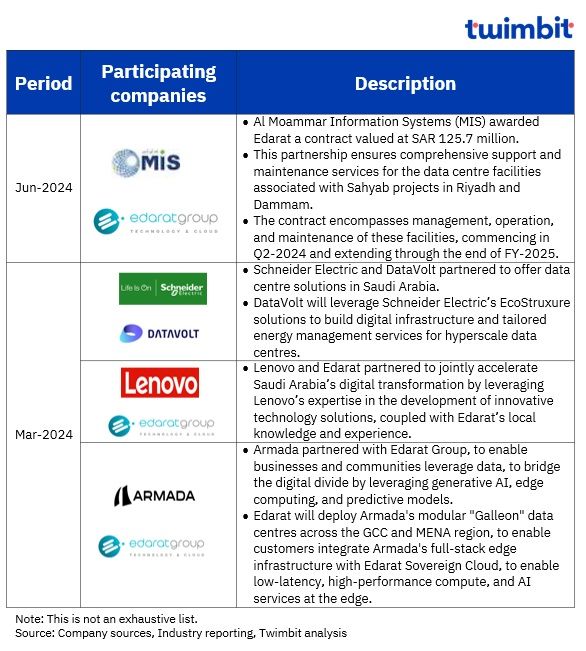

- Some of the major data centre contracts propelling advancements in Saudi Arabia’s data centre landscape are driven by companies like Al Moammar Information System, DataVolt and Edarat.

- These initiatives underscore the focus on enhanced efficiency, scalability, and data accessibility within the Kingdom.

Exhibit 12: Key contracts in Saudi Arabia Data centre market

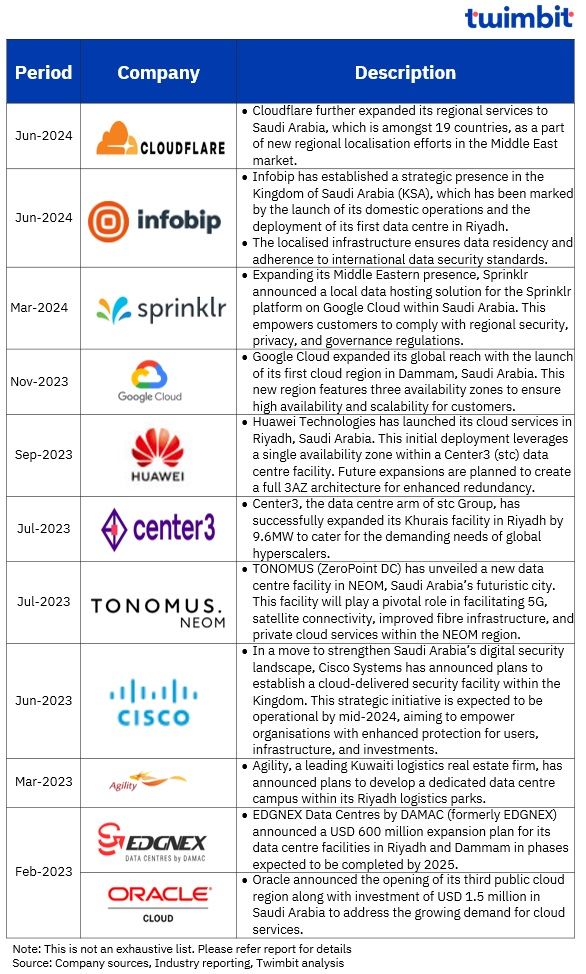

C. Key Data centre launches and initiatives in Saudi Arabia

- The Kingdom of Saudi Arabia is experiencing a surge in data centre investments and cloud service deployments. Major players like Google Cloud, Oracle, Huawei, and Cisco are establishing a presence, while local providers like stc and TONOMUS are expanding their facilities.

- This growth strengthens Saudi Arabia’s digital security posture and empowers businesses with secure, localised data storage solutions.

Exhibit 13: Key Data centre launches and initiatives in Saudi Arabia

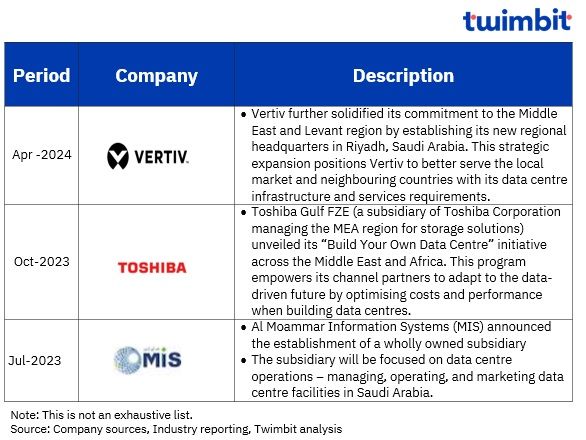

D. Other key developments in Saudi Arabia data centre market

Leading technology firms, Vertiv and Toshiba Gulf FZE, are strengthening their presence in the Middle East by establishing regional headquarters and data centre solutions initiatives in Saudi Arabia. This strategic move caters to the Kingdom’s flourishing tech sector and positions them to serve the broader region.

Exhibit 14: Key Data centre launches and initiatives in Saudi Arabia

6. Key trends in Saudi Arabia Data centre market

A. 5G coverage expansion by telcos continue to drive demand for robust data centre infrastructure to support growing data needs

Saudi Arabia’s telecommunications landscape is characterized by the robust presence of key players, including Saudi Telecom Company (stc), Mobily, and Zain KSA. Recognizing the transformative potential of 5G technology, these telecommunications giants have been at the forefront of deploying 5G services nationwide.

The Kingdom’s 5G journey commenced in October 2019, with stc spearheading the initiative. Underscoring its commitment, stc unveiled a substantial network expansion plan in October 2023, targeting coverage across 75 cities and governorates. As of Q1 2024, Zain KSA demonstrated impressive network penetration, achieving 99% population coverage, including 94% for 4G and 65% for 5G. Mobily has also made significant strides, with its 5G network encompassing 52 major cities and leveraging over 5,900 sites, thereby providing 5G accessibility to over 84% of the population in the Kingdom’s seven largest urban centres.

To optimize network costs and enhance user experience, the strategic deployment of edge data centres is gaining prominence. This decentralized approach involves establishing numerous edge facilities connected to a central, high capacity hyperscale data centre. As 5G technology proliferates and data generation accelerates, the demand for robust data centre infrastructure is poised to escalate in tandem, necessitating substantial investments to accommodate the expanding data landscape.

B. Saudi Arabia’s Data centre market continues to grow, fuelled by Innovation and Investment be leading technology vendors

Government initiatives aimed at digital transformation and a burgeoning demand for digital services are creating fertile ground for investment. The LEAP 2024 conference served as a powerful testament to this trend, witnessing announcement of numerous launches and investments exceeding USD 1.5 billion and total cumulative investment during this edition reached a staggering USD 13.4 billion.

Several prominent industry players have announced substantial investments over the past year and a half, illustrating the sector’s growing appeal:

- AWS: In Mar-2024, AWS pledged a commitment exceeding USD 5.3 billion to be invested by 2026 for the establishment of data centres planned to be operational by that same year.

- Datavolt: This Saudi Arabian data centre provider announced a USD 5 billion investment plan in Mar-2024, earmarked for the construction of data centres with a combined capacity exceeding 300 MW.

- ServiceNow: Announced a direct investment of USD 500 million in Mar-2024, encompassing the creation of two dedicated data centres within the Kingdom. This initiative aims to facilitate business transformation, job creation, and the development of crucial digital skills.

- Huawei: In Feb-2024 marked the announcement of Huawei’s USD 400 million investment plan, to be directed towards the development of the Saudi Arabian cloud region over the period 2023-2027.

C. Sustainable solutions for Saudi Arabia’s Data centre landscape gain traction, as its aims for net-zero by 2060

Saudi Arabia has embarked on an ambitious sustainability journey, with a resolute commitment to achieving net-zero carbon emissions by 2060. The Saudi & Middle East Green Initiatives are at the forefront of this endeavor, targeting a substantial 278 mtpa reduction in carbon emissions by 2030. A cornerstone of this strategy is the accelerated transition to renewable energy sources, with an aspirational goal of deriving 50% of the nation’s power from renewable energy by 2030.

Recognizing the unique challenges posed by the region’s arid climate and water scarcity, data centre operators and vendors are prioritizing sustainability in their operations. Minimizing heat generation and optimizing cooling systems to conserve water have become paramount. The abundance of solar energy in the region offers a compelling solution, promising both cost-efficiency and environmental benefits.

As the data centre landscape in Saudi Arabia expands, sustainable power consumption has emerged as a critical imperative. Operators are actively exploring renewable energy integration to reduce their carbon footprint. A pivotal development was the October 2023 Memorandum of Understanding between Aurum Equity Partners and Al Nowais Group to construct a 50MW data centre featuring cutting-edge technology, a sustainable design, and robust security measures. Similarly, agility, a Kuwaiti logistics real estate firm, announced plans in March 2023 to develop a 25MW data centre in Saudi Arabia, with over 10MW of power generated from solar energy.

The NEOM Green Hydrogen Project stands as a testament to Saudi Arabia’s commitment to a green future. This groundbreaking initiative aims to produce large-scale green hydrogen in the visionary city of NEOM, positioning the region as a global hub for innovation and sustainability.

To optimize data centre operations and ensure long-term sustainability, a multifaceted approach is essential. Upgrading cooling systems with energy-efficient technologies is paramount. Integrating renewable energy sources, such as solar and wind power, is crucial to reducing carbon emissions. Deploying edge computing solutions closer to data sources can enhance network performance and efficiency. Finally, adopting modular and scalable data centre designs provides the flexibility to adapt to evolving business needs and optimize resource utilization.

D. Saudi Arabia data centre market tightens amidst strong regional demand

Data centre availability in Saudi Arabia is experiencing a significant decline, as evidenced by falling vacancy rates. A Q3-2023 report from Knight Frank indicates a substantial decrease in vacancy, reaching just over 30% in Q3-2023, compared to approximately 38% two years prior.

This trend is projected to continue due to robust regional demand from hyperscale cloud providers and burgeoning domestic service providers within Saudi Arabia.

E. Saudi Arabia shifts data center investments from traditional hubs to emerging tech cities like Neom and Al Khobar.

Historically, data centre investments within the Kingdom of Saudi Arabia have exhibited a centralised focus, with Riyadh, Jeddah, and Dammam attracting most of the capital pre-2023. However, a discernible shift is underway. The geographic landscape of investment is expanding to encompass emerging technology hubs. Notably, significant future investment is anticipated in Neom, the nation’s futuristic smart city project, alongside the growing metropolis of Al Khobar.

Research Methodology and Assumptions

- The “Saudi Arabia Data centre market insight – 2024” report provides an overview of the data centre market in Saudi Arabia including Macroeconomic overview, Regulatory landscape, Market opportunity, Competitive landscape, key Drivers and Challenges and major trends prevailing.

- Key aspects covered in the report offers insights related to different ecosystem players in the Saudi Arabian data centre market.

- The report involves exclusive secondary research and primarily leverages company websites and publicly disclosed information from major cloud service providers.

- To maintain consistency and enable accurate comparisons, the report applies a constant currency conversion rate (wherever applicable), reflecting the average USD exchange rate for January – December 2023.

- The data presented in this report is based on the most current information available at the time of compilation. As such, it may not reflect subsequent developments. This report is intended for informational purposes only and should not be relied upon as a substitute for independent research.

Click here for more contents on telecom

Recommended by Twimbit:

Saudi Arabia telcos performance benchmarks – July 2024

Middle East telcos performance benchmarks – Spring 2024 (Q1 2024 edition)

Global telcos performance benchmarks – Spring 2024 (Q1 2024 edition)