Siam Commercial Bank (SCB) is one of Thailand’s oldest and leading banks, operating in 8 countries with more than 700 branches. Its presence spans Cambodia, China, Hong Kong, Laos, Vietnam, Singapore, Myanmar and Thailand (home market).

Operational efficiency at SCB

Investment gains, wealth and bancassurance verticals significantly determined the direction of SCB’s income growth in 2021 (Figure 1). However, when combined with the bank’s initiatives in controlling costs, SCB quickly grew its operating profits, resulting in a 30.8% YoY (year-over-year) increase in its net profit for 2021.

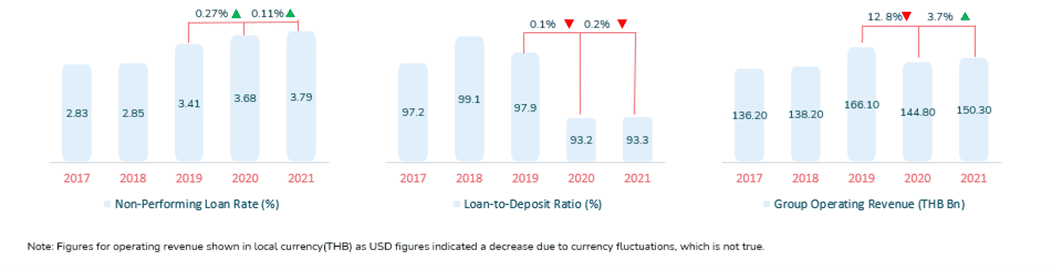

The NPL (Non-Performing Loans) ratio rose from 3.68% at the end of 2020 to 3.79% at the end of 2021 (Figure 1). This change happened primarily because the pandemic severely affected the qualitative loan downgrades of customers.

At the same time, the LDR (Loan-to-Deposit Ratio) saw an insignificant decline of 0.2% from 2020 to 2021. Ideally, the LDR should be between 80% – 90%. Instead, SCB charted at 93.3% in 2021 (Figure 1), registering itself above the threshold.

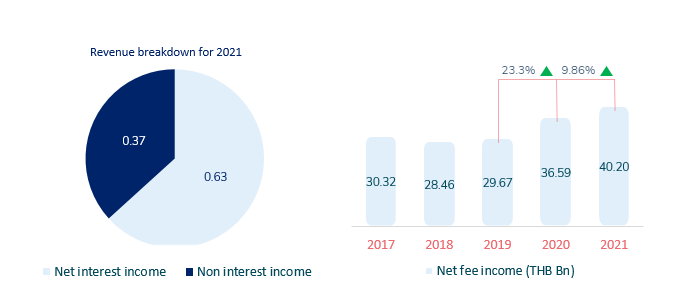

Regarding the revenue breakdown of SCB for 2021 (Figure 2), the net interest income decreased by 1.8% YoY, while the non-interest income increased by 15%. This increase in the non-interest income served as another critical factor to SCB experiencing its strong income growth.

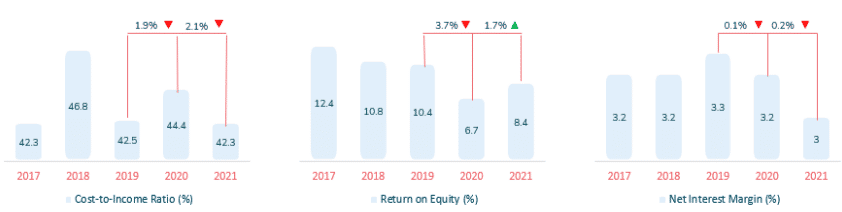

The decrease in net interest income seems to be a compression of the net interest margin (NIM) from 3.2 in 2020 to 3% in 2021 (Figure 3). The NIM decreased because of the low-interest environment rate and its deliberate focus on rolling out high-quality loans. Comprehensive debt restructuring is a factor for lower NIM as well.

The CIR (cost-to-income ratio) improved from 44.4% in 2020 to 42.3% in 2021 (Figure 3). The bank achieved this outcome due to the decline of 1.2% YoY in the bank’s operating expenses.

The bank’s CET1 (capital equity tier 1) ratio and ROE (Return on Equity) increased and stood at 17.6% and 8.4%, respectively (Figure 3). This increase worked favourably for SCB and its capital position.

Strategic focus areas for SCB

- #1 Becoming a worldwide financial tech company

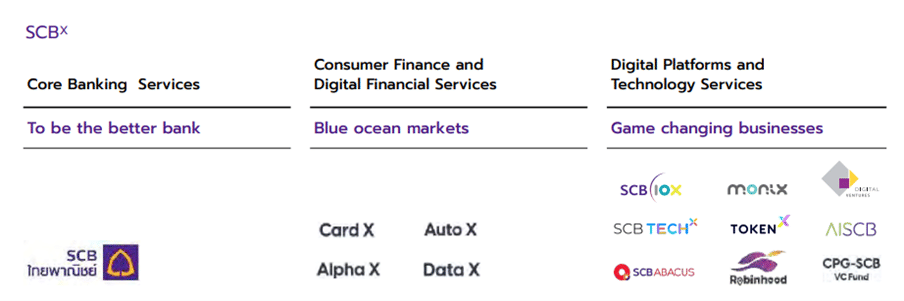

SCB has gone under massive restructuring and introduced SCBX.

The SCB Group has divided the SCBX business structure into three main segments: core banking services, consumer finance and digital financial services, and digital platforms and technology services (Figures 5 & 6) with the goals of:

- leveraging capital management efficiency,

- expanding ways to create long-term value,

- exploring new business gateways, and

- sharpening a new competitive edge by leveraging data

The reasons behind this transformation may be to:

- effectively deploy capital and boost its ROE

- maximise growth for its emerging businesses (consumer finance and digital platform services)

- defend its market share in core banking services against both banks and non-banks

- #2 Digital measures of success

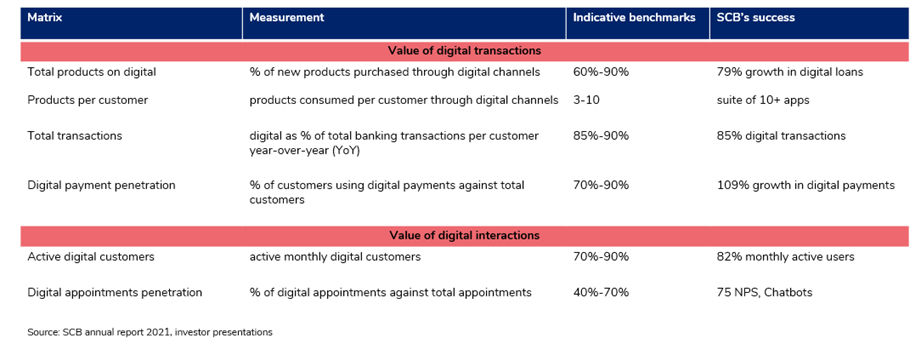

SCB has deployed seamless payment solutions, implemented chatbots, introduced robust digital product stacks and upscaled business capabilities to provide a holistic digital experience to its customers. As a result, the bank has excelled in each digital measure of success (Figure 7):

- #3 Sustainability and ESG integration

SCB ranked 3rd on the World Index and the Emerging Markets Index of the Dow Jones Sustainability Indices (DJSI). The bank implements sustainability initiatives under 3 key pillars:

- Sustainable finance – SCB SME Academy

- A community for developing and sharing business know-how, aiming to holistically uplift the capabilities of SMEs to thrive in the digital era.

- Social impact – Robinhood

- A food delivery mobile application under a social enterprise model that operates by eliminating the gross profit fee imposed by other platforms.

- Robinhood helps small restaurants expand their online sales opportunities, creating job and wage gains for delivery personnel.

- Environmental future

- Reduced greenhouse gas emissions of over 960,000 million tons (20%) of carbon dioxide equivalent per annum

- Reduced energy and water consumption by 19% and 33%, respectively.

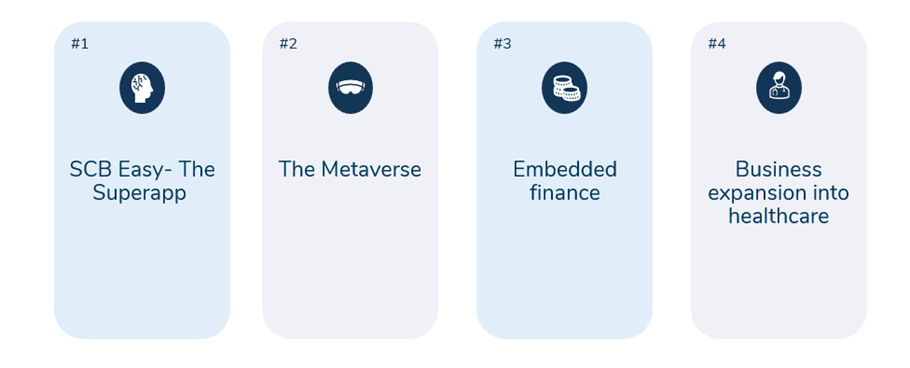

Top 4 growth opportunities for SCB

- #1 SCB Easy – The Superapp

Understanding the need for enhancing its digital experience, SCB Easy provides a plethora of services from;

- investments,

- insurance,

- checks,

- card services,

- and other financial services ranging from transfers to bill payments

The bank can now take it a notch higher and consolidate all its consumer services onto one platform instead of having different apps (Connect, Protect, Robinhood), leading to an ecosystem of banking facilities for the consumers.

Most importantly, SCB also integrated a single source of truth capability into the app to gather customer data and help manage their budgets and finances. With that in mind, SCB should maximise all the customer data available to unlock new journey-based services for each customer.

- #2 The Metaverse

Looking to be a part of the buzz in the banking sphere, which is the Metaverse, the bank established SCB 10X HQ – a virtual headquarters in The Sandbox. Following JP Morgan’s foray into the virtual medium, SCB has become the second major financial institution to establish a virtual headquarters. The HQ features three zones:

- Virtual hub – A space for events and sharing knowledge through immersive experiences

- Virtual land – A space for business partners to collaborate on activities and project development in the future

- A hub to support and promote local artists in the global market through a non-fungible token (NFT)marketplace, NFT gallery, virtual concerts and more

If the bank decides to enhance its metaverse capabilities and offerings further, it should aim to do the following:

- Establish a dedicated virtual bank for users to save, spend or invest their virtual currency within the Metaverse.

- Install virtual branches and ATMs in popular regions within the Metaverse to provide virtual users with the same level of convenience that a physical customer usually attains.

- Create loyalty programs for its customers with NFTs within the Metaverse

- Partner with content and intellectual property franchises to add their financial services expertise in co-designing economic and financial interoperability between multiple Metaverses and the physical world. For instance, SCB could utilise this aspect and closely emulate the interoperability that exists in other mediums, such as gaming universes, where developers design in-game economies to manage supply and demand patterns.

- #3 Embedded finance

SCB became Thailand’s first bank to launch an open API (application programming interface) in 2019. It is complete with a developer portal, which enables third parties to build apps connected to SCB services and products through APIs. The portal also acts as a sandbox environment for developers, allowing them to instantly conduct tests covering all scenarios in an open and pre-meditative environment.

The portal has APIs for the following:

- Mae Manee merchant

- SCB payment gateway direct debit

- SCB Easy app payment

- Customer information

- Authentication

- QR code payments

- Slip verification

SCB can thus further expand its embedded finance offerings through:

- Expanding the API suite

The bank should enhance its API suite by including the following:

- Core banking APIs to create savings accounts and perform cash deposits

- Lending APIs

- Card Issuance APIs

- KYC APIs

- Establish marketplaces

- SCB can analyse transactional data from its large customer data pool to;

- identify costs

- offer tailored products and discounts through their own marketplaces

- For example, the bank has plans to expand the scope of services for Robinhood to provide all-in-one travel services such as bookings for airlines, hotels, activities, car rentals and travel insurance in one platform.

- SCB can replicate this model with products, such as insurance and home loans, to establish the insurance marketplace and property marketplace.

- SCB can also expand into the property marketplace by partnering with home retail stores, such as Homepro and other utility providers, to satisfy the end-to-end utility needs of customers.

- #4 Business expansion into healthcare

SCB has partnered with Mahidol University and Good Doctor Technology to breach the health-tech market in Thailand. Together, they have combined technological capabilities with sports and nutritional science to create health experiences for their customers through their “SPRING UP” mobile app.

SPRING UP integrates three important features in its digital health platform:

- Food: Nutrition facts and alerts for users recommended by Mahidol University experts.

- Fitness: Personalised exercise plans recommended by Mahidol University experts to enable users to achieve their exercise goals

- Telemedicine: Chats with doctors and home-delivery of medications through Good Doctor Technology

The bank can further expand into the healthcare sector by:

- Enhancing SPRING UP

SCB can further enhance the application through the following:

- Video consultation with healthcare professionals

- Bookings for in-person consultations

- Provision and renewal of health insurance

- Listing the medical history of users along with insurance data

- Collaborating with healthcare giant BDMS

The partnership will benefit both parties, with SCB being able to launch smart hospitals and lifestyle and wellness centres, growing its expansion into the healthcare sector.

Conclusion

Fully leveraging its tech stack across new business verticals, SCB is on the path to becoming a regional financial technology group that could compete with digital natives in terms of customer-centricity and operational efficiency. Moreover, the increase in the bank’s digital app adoption further indicates that this strategy is helping the bank increase customer loyalty and draw in new customers. One thing is clear – SCB is truly changing the game in this digital transformation era.

Read more such reports, here.