Competitive Overview

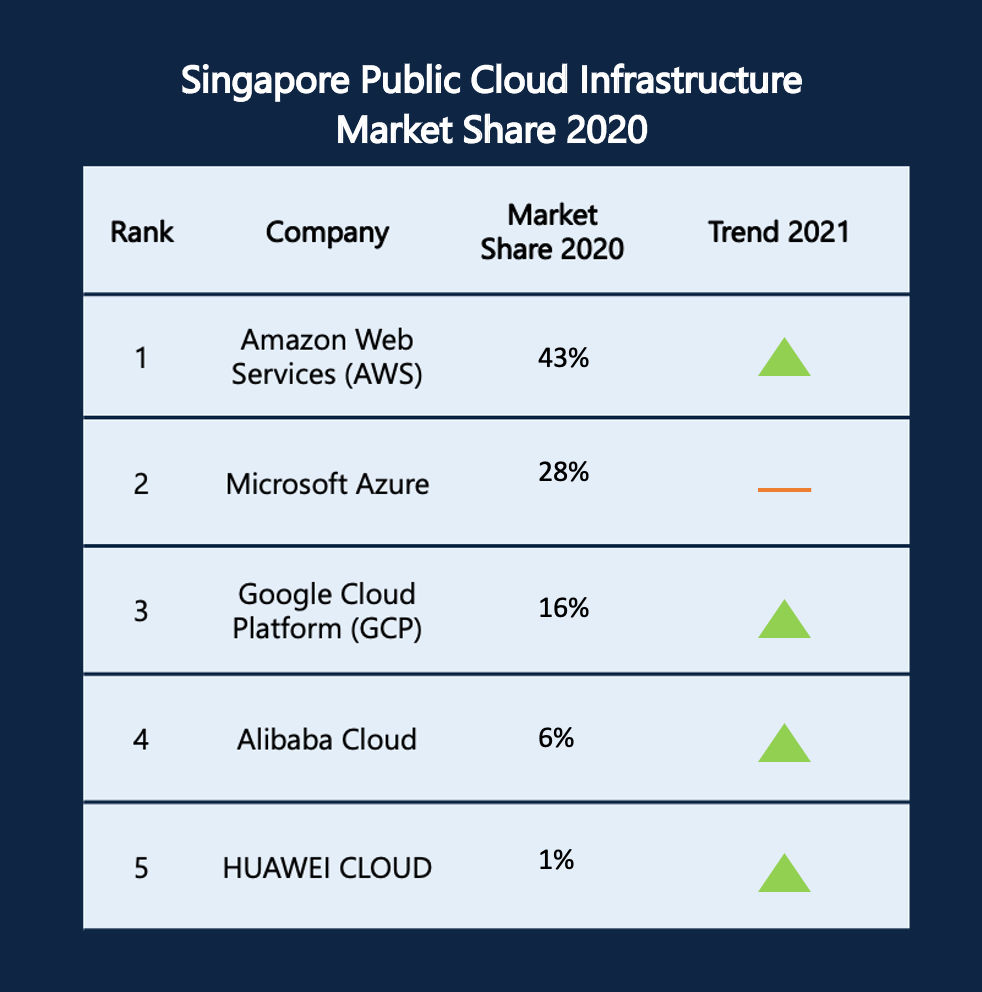

- Amazon Web Services (AWS), Microsoft Azure and Google Cloud Platform (GCP) collectively account for 87% of the Singapore public cloud IaaS market. This translates to a value of US$ 0.64 billion.

- AWS is the market leader with 48% of the IaaS market share, converting to a value of US$ 353.7 million. This is mainly due to their large enterprise accounts and solutions maturity in the compute segment.

- Microsoft Azure trails in next with 28% of the local IaaS market share. The company credits most contributions to their storage offerings, a stark difference from AWS. This is indirectly led by their SaaS applications. One such example is OneDrive, the usage for which has been accelerated by the pandemic.

- While GCP only holds 13% of the local IaaS market share, the company is gradually strengthening their presence in Singaporean market with renowned hires. This has opened doors to regional enterprises while establishing strategic solutions and partnerships simultaneously.

Leaders of Singapore Public Cloud Infrastructure Market

The 3 cloud titans of Singapore

Dominating nearly half of the local public cloud infrastructure market share, AWS remains the flagship cloud provider in Singapore. This company serves virtually every organization and every industry imaginable. AWS leads the market with key accounts like Grab, DBS, and Singapore Government, where each commit at least US$ 10 million every year. In 2020, AWS continues to be the backbone of various digital transformation initiatives such as Smart Nation and Start Digital while continuing to expand their acquisition of DNBs, as more flock into the country year-on-year. With these well-rounded go-to-market strategies, AWS pushes ahead of all its competitors in a digital-first country like Singapore.

On the other hand, Microsoft Azure’s reliance on partners for customer acquisition. This has awarded them with a substantial share of the market. An approximate 94% of their revenue comes from their established Microsoft Partnership Network (MPN), with leading partners such as Avepoint and Ingram by their side. Apart from its comprehensive partner programs, runner-up position is driven by its solutions’ ability to address the public sector and large enterprises’ demands. For instance, financial services customers are drawn to the new Azure architecture, which reflects the Zero Trust model, adding an additional layer of security to sensitive data. As an outcome, Azure won the country’s leading insurance company, AIA Singapore.

GCP may have the smallest share of the market compared to the other two CSPs but has quickly gained traction for its Google Workspace offerings. This has in turn drove adoption for Google Cloud’s solutions. The platform’s accelerated growth in Singapore was led by hiring top talents. This successively helped open doors to leading enterprises across the country and the region. Some of its successes include the acquisition of NTUC and FWD and was chosen as the cloud provider for Go-Jek expansion in Southeast Asia. GCP also holds a strong track record for catering to the Singapore Government. For instance, as of December 2020, GCP was one of the cloud service providers selected by GovTech to work with Singapore’s government agencies. The cloud provider assisted in moving majority of the nation’s system onto the cloud.

Smaller market players

Some remainder of the infrastructure market shares are held by regional cloud players such as Alibaba Cloud and Huawei Cloud. Alibaba Cloud has a unique strategy by targeting the growth of start-ups in the country. This is to ensure their success and potentially converting them into their customers. The company has partnered with the Singapore University of Social Sciences (SUSS) to launch their Entrepreneurship Program, aimed to develop the start-up landscape in the country. On top of seeding startups, they are assisting the government’s ongoing efforts in digitally transforming the SME sector. Alibaba Cloud also has a keen eye in gaining e-commerce accounts and has used Lazada as a successful example of their expertise in handling e-commerce companies. It is of no doubt that Alibaba Cloud has ensured that their presence in the Singapore market is noticed.

Another cloud service provider to note is HUAWEI, who is currently in the stages of expanding their partner network and building their brand awareness. Having entered the Singapore cloud market in 2019, the company plans to develop the Singapore into one of its largest regions outside of China. Some of HUAWEI’s notable partners include Infosys and Bespin Global. Alibaba and HUAWEI are prioritising similar strategies by showcasing themselves as the best choices of CSPs for the government’s initiative to digitalize SMEs in Singapore. SMEs are the spine of Singapore’s economy, making up 99% of all domestic companies and contributing almost half (49%) of the national GDP.

Twimbit Takeaways

- As SMEs are the heart of Singapore’s economy, this sector has high potential for cloud adoption. Over 80% of these businesses are embracing digital solutions to ensure revenue improvement and business continuity.

- Enterprises in Singapore are beginning to embrace multi-cloud strategies for bolstered resilience and lower latency. For example, DBS Bank has adopted Azure and AWS, whereas Allianz is currently using Azure and GCP. This trend is expected to continue amongst large enterprises and digital startups.

- CSPs in Singapore have carved their own niche according to their expertise, resulting in enhanced customer relationships. Newer market entrants would need to compete with these strategies and the highly competitive pricing if they want to gain customers. Entering the cloud market in Singapore without addressing a gap and a unique target market could prove futile.

Click here to read about Singapore’s public cloud market performance in 2021