Key highlights

In Q3 2023, South Korea’s economic growth faltered due to rising borrowing expenses and sluggish export recovery, greatly affecting consumer spending.

- GDP grew by a marginal 0.5% QoQ (Quarter-on-Quarter) compared to the expected expansion of 1.1% in Q3 2023.

- The current policy rate in South Korea stands at a 15-year high of 3.5%.

- High borrowing costs for households have led to a decline in consumer sentiment.

- The loan portfolio of the top 5 banks grew by 4.09% from USD 1.1 trillion in Q3 2022 to USD 1142 billion in Q3 2023.

- Deposits grew slower at 3.04% from USD 1.26 trillion in Q3 2022 to USD 1.3 trillion in Q3 2023.

Revenue

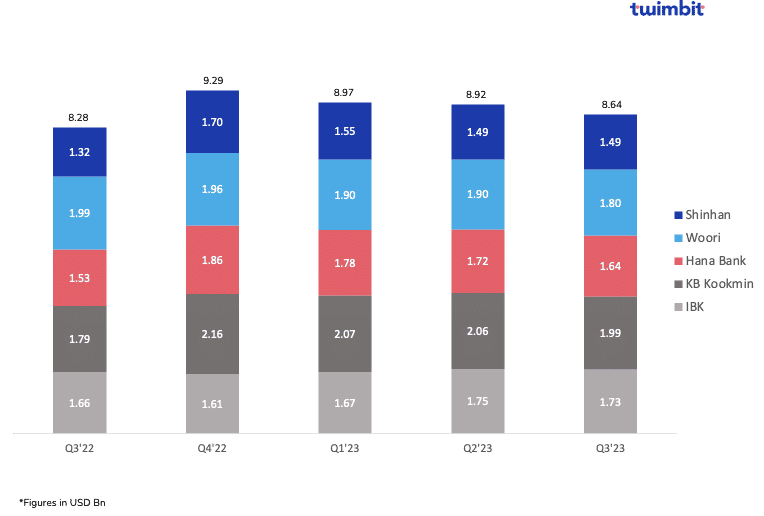

Net revenues for the Top 5 banks in South Korea grew by 4.35% YoY

The top 5 banks in South Korea increased from USD 8.28 billion in Q3 2022 to USD 8.64 billion in Q3 2023 (Exhibit 1). Average net revenues stood at USD 1.73 billion in Q3 2023.

- 7.81% increase in the net interest income from USD 7.63 billion to USD 8.23 billion.

- 34% increase in the non-interest income from USD 635 million to USD 851 million.

Exhibit 1: Net revenues of the top 5 South Korean Banks

Shinhan Bank

- 4% YoY increase in net revenues from USD 1.66 billion to USD 1.73 billion.

- 3.91% decline in fee income from USD 171 million to USD 165 million.

- 400% YoY increase in non-interest income from USD 17 million to USD 86 million.

- This was driven by a 513% increase in securities and forex trading income from USD 24 million to USD 149 million.

KB Kookmin Bank

- 11.10% increase in net revenues from USD 1.79 billion to USD 1.99 billion.

- 4.94% increase in net interest income from USD 1.85 billion to USD 1.94 billion.

- 3% decline in non-interest income from USD 213 million to USD 207 million.

Apart from Woori Financial Group, which reported a decline of 9.52% from USD 1.99 billion in Q3 2022 to USD 1.80 billion in Q3 2023, all banks reported an increase in their net revenues.

Profitability

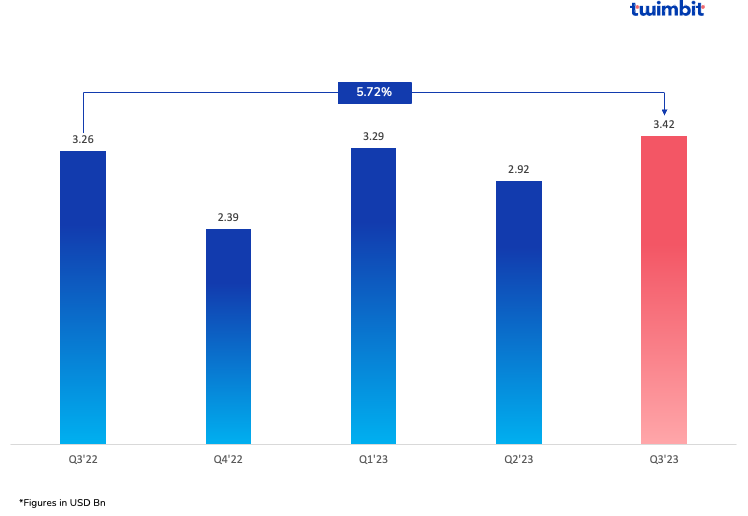

Net profit for the top 5 banks in South Korea grew by 5.03% YoY

Aggregated net profits increased from USD 3.24 billion in Q3 2022 to USD 3.42 billion in Q3 2023. Average net profits grew by 5.72% (Exhibit 2) from USD 647 million in Q3 2022 to USD 684 million in Q3 2023.

Exhibit 2: Consolidated net profits of the top 5 South Korean Banks

- Shinhan Bank: 1% net profit growth

- KB Kookmin Bank: 20.95% net profit growth

- Hana Bank: 6.57% net profit growth

- Woori Financial Group: 1.71% net profit decline

- Industrial Bank of Korea: 1.40% net profit decline

KB Kookmin Bank reported a 20.95% growth in its net profits from USD 634 million in Q3 2022 to USD 766 million in Q3 2023. This was driven by:

- 5% YoY growth in the net interest income from USD 1.85 billion in Q3 2022 to USD 1.94 billion in Q3 2023.

- 2.37% YoY growth in the loan portfolio from USD 253 billion in Q3 2022 to USD 259 billion in Q3 2023.

Fee-based income

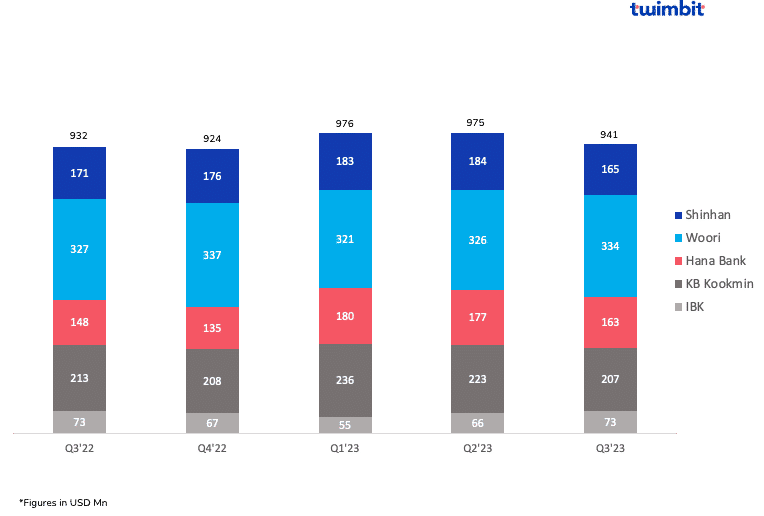

Fee income for the top 5 banks in South Korea grew by 0.96%

Fee income grew from USD 932 million in Q3 2022 to USD 941 million in Q3 2023 (Exhibit 3).

Exhibit 3: Fee income of the top 5 South Korean Banks

Hana Bank

- 10% increase in fee income from USD 148 million to USD 163 million

- Strong performance in fee items related to loans, trusts, pensions and operating leases

Woori Financial Group

- 2.35% increase in fee income from USD 327 million to USD 334 million

All other banks reported declining fee incomes.

- Shinhan Bank reported a decline of 3.91% from USD 171 million to USD 165 million.

- KB Kookmin reported a decline of 3% from USD 213 million to USD 207 million.

- Industrial Bank of Korea reported a decline of 0.63% from USD 73 million to USD 72.6 million.

Fee income (a part of the bank’s non-interest income) is low in South Korea compared to peers in other regions due to tighter rules and consumer behaviours. This is because banks in South Korea are not allowed to impose account-related fees due to the consumer backlash and government pressure against such practices. These charges include monthly charges for failing to maintain the minimum required balance and commission fees on consumer transactions and banking services.

Net interest margins (NIM)

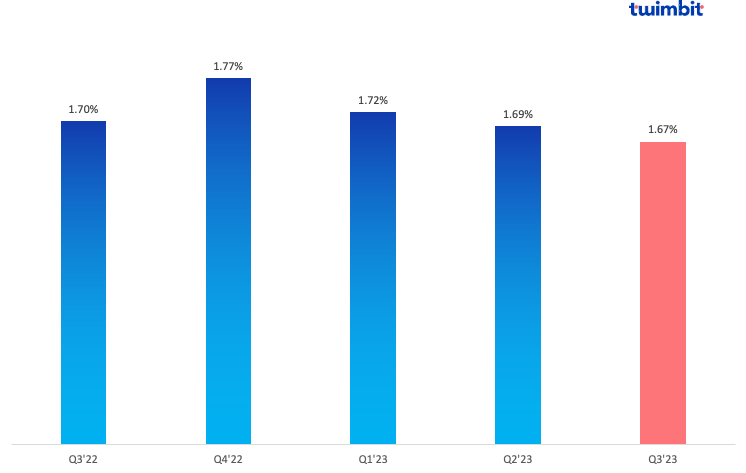

NIM for the top 5 banks in South Korea declined by 3 basis points

The average NIM declined from 1.70% in Q3 2022 to 1.67% in Q3 2023 (Exhibit 4). Apart from KB Koookmin, all the banks reported a decline in their NIMs.

Exhibit 4: Consolidated net interest margins of the top 5 South Korean Banks

South Korean banks have low-interest margins due to:

- Low-interest rates – Maintaining low-interest rates to spur economic growth has posed challenges for banks in generating interest income from loans, thereby exerting pressure on their profit margins.

- High reliance on retail banking – The heavy dependence on retail banking (which generally yields lower profits) has contributed to the diminished interest margins of Korean banks.

Credit growth in South Korea has been slow, with an average growth of 6.34% to USD 1142 billion in Q3 2023.

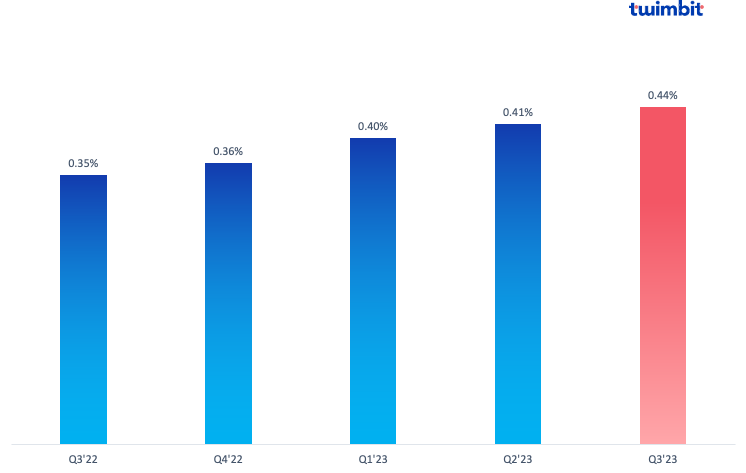

Non-performing loans (NPL)

NPL for the top 5 banks in South Korea increased by 9 basis points

South Korean banks have the lowest NPLs among APAC regions. The average NPL increased from 0.35% in Q3 2022 to 0.44% in Q3 2023 (Exhibit 5).

All banks reported an increase in NPL, with 3 of 5 reporting double-digit growths.

Exhibit 5: Consolidated non-performing loans of the top 5 South Korean banks

Reason for low NPL among South Korean banks:

- Strict lending standards – The stringent lending standards prevent loan extension to borrowers with doubtful repayment capabilities.

- Conservative provisioning – The mandate for South Korea’s banks to allocate substantial provisions for potential loan losses helps ensure that funds are set aside to mitigate the risk of non-repayment. This conservative strategy contributes to maintaining low Non-Performing Loan (NPL) ratios, even amid economic downturns.

- Effective debt collection – To implement more effective processes, South Korean banks leveraged the support of the country’s robust legal system to recover loans that have not been repaid promptly.

Reasons for rising NPL among South Korean banks:

- The economic slowdown led to an increase in bankruptcies and loan defaults.

- Rising interest rates to combat inflation have made it difficult for businesses and individuals to repay their loans.

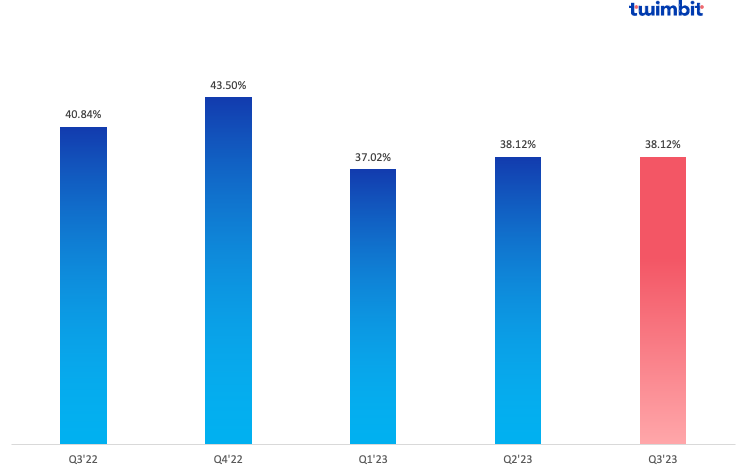

Cost efficiency (CE)

CE for the top 5 banks in South Korea improved by 272 basis points

Cost efficiency stood at 38.12% in Q3 2023, slightly improving from the average cost efficiency of 40.84% in Q2 2023 (Exhibit 6).

Exhibit 6: Consolidated cost-efficiency ratio of the top 5 South Korean Banks

- Shinhan and Woori Financial Group reported a decline in cost efficiency by 150 bps and 20 bps, respectively.

- All banks have their cost efficiency ratio below the threshold value of 50%.

Initiatives by the top banks in South Korea

- Hana Bank

Hana x BitGo

This collaboration will enter the Digital Asset Custody (DAC) sector as BitGo establishes its presence in South Korea. It also aims to explore joint ventures, further capitalizing on strengths in security solutions, DAC technology, and Hana Bank’s financial services.

- Hana Bank aims to enhance trust and customer protection in the domestic digital asset market by promoting the DAC sector with global partners.

- BitGo will assist Hana Bank in developing custody services in the second half of 2024.

- Woori Bank

Global expansion

Woori Bank has announced plans to achieve up to 25% of its net profits from global sales by 2030. As it stands, overseas net profits accounted for 15.4% of total net profits in 2022. To achieve its goals moving forward, the bank plans to implement numerous initiatives, mergers and acquisitions.

- Focus on nurturing its business units in Indonesia, Vietnam, and Cambodia

These central Southeast Asian units accounted for 43% of overseas net profits in the region in 2022. Hence, Woori Bank intends to invest USD 200 million each in Indonesia and Vietnam and USD 100 million in Cambodia in H1 2024.

The bank also plans to expand its operation in Poland by converting its local office into a full-fledged branch to serve the financial service demands of Korena companies in Poland.

Foster a strategic partnership with USD real estate platform BuildBlock

The partnership would be beneficial for both parties because of the following:

- BuildBlock offers a wide range of real estate services, which encompass:

- Residential and commercial real estate brokerage

- Maintenance

- Post-sale payment recovery

- Tax support

- DinoLab (Woori Bank’s incubation initiative) aims to connect Woori Bank’s clientele with BuildBlock to streamline foreign real estate acquisitions and associated foreign exchange processes.

According to a Woori Bank official’s statement, the partnership can further enhance global property investments and facilitate easy entry for customers into overseas real estate investments.

- Shinhan Bank

Business agreement with BC Card

Shinhan Bank’s Vietnamese branch entered a business agreement with BC Card to jointly advance the card acceptance business in Vietnam. Here, BC Card’s Vietnam and Indonesian branches will collaborate with Shinhan Bank to:

- Establish a card acceptance system

- Expand and manage the merchant network

- Develop card terminals and POS systems

The bank aims to activate the credit card payment market in Vietnam, contributing to the Vietnamese government’s goal of achieving a cashless society by 2025.

- KB Kookmin

AI Banker

The initiative in collaboration with DeepBrain is a first in the country. The proposition is a virtual human capable of real-time interactive communication directly with users using a fusion of speech synthesis, video synthesis, natural language processing and speech recognition.

- AI Banker greets customers at the kiosk and answers queries using KB-STA, a bank-developed financial language model.

- Answers are delivered through AI Banker’s video and voice interface, powered by DeepBrain’s AI human technology.

- It guides customers on using devices, such as Smart Automated Machines and ATMs, introduces financial products, and directs them to kiosk installation points.

- Provides information on financial topics, daily weather, and nearby facilities.

- In idle mode, the AI Banker exhibits gestures, recognizes customers, and bids farewell with a Thank You when they leave.

Increasing competition from Kakao Bank

Besides China, South Korea is the only other Asian country where digital banks have reached profitability. Kakao Bank is by far the country’s best and most profitable digital bank, benefitting from its super app, Kakao Talk. Since its launch, the bank has gained over 21 million users. The bank generated revenues totalling USD 823 million in FY2022 which is higher than some traditional banks in the country. To compete with Kakao Bank in a landscape shaped by innovation and customer expectations, traditional banks need to dedicate themselves to digital transformation, customer-centricity and strategic partnerships from traditional banks. They can do this by:

- Leverage the APIs of social media giants or create in-house instant messaging banking capabilities within your banking application to simplify your customers’ banking journey.

- Adopt gamification practices to make your customers’ banking, budgeting, and savings experiences fun and engaging.

- Extend your product offerings by taking an ecosystem approach to drive more diversified revenue streams.

Outlook for 2023

Rising borrowing expenses suggest a challenging outlook for the final months of 2023. Looking ahead, prospects for a significant enhancement in private consumption growth seem unlikely. Instead, economic growth is expected to be primarily driven by net exports and business investments.

To learn about how the leading Indian banks performed in Q3 2023, click here.

To learn about how the top 3 Singapore banks performed in Q3 2023, click here.

To learn about how the top 5 Indonesian banks performed in Q3 2023, click here.

To learn about how the leading banks in the Philippines performed in Q3 2023, click here.