Key takeaways

- APAC Banks generated USD 737 billion in net revenues in 2023, a 3.9% YoY increase from the previous USD 709.5 billion in 2022.

- Chinese banks are the most profitable, generating an average of USD 101.1 billion in net revenues.

- Revenue from Chinese banks comprises 54.9% of total net revenues generated in APAC in 2023.

- Excluding China, the net revenue growth stood at 13.5% YoY, up from 11.2% YoY in 2022.

- Net profits of APAC Banks increased from USD 261.8 billion in 2022 to USD 279 billion in 2023, signifying a 6.6% YoY growth.

- Chinese banks generated 61.5% of the total net profits in APAC.

- Net fee income grew by 2% from USD 100.1 billion in 2022 to USD 102.2 billion in 2023.

- China and Thailand reported declining fee incomes.

- Australia and South Korea reported modest growth of 0.7% and 2.2% respectively.

- Indian Banks reported strong YoY growth of 14.7% in fee income driven by product cross-selling, digital banking services and fintech partnerships.

- APAC’s average NIM (net interest margin) in APAC stood at 2.89% in 2023.

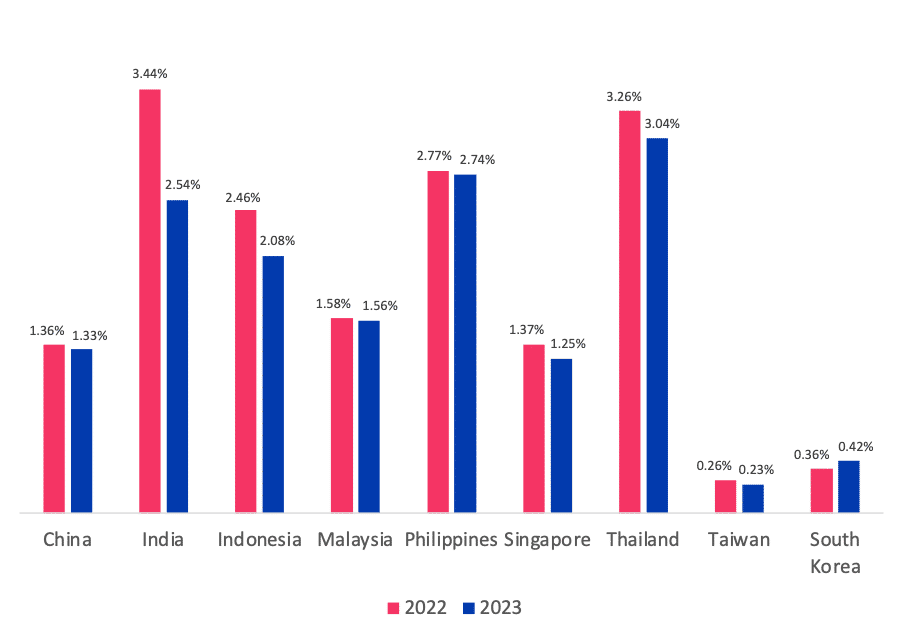

- Indonesian Banks have the highest NIMs at 6.08%, followed by Filipino Banks at 4.51%.

- Taiwanese, Chinese and South Korean Banks have the lowest NIMs at 1.14%, 1.63% and 1.68%, respectively.

- Low NIMs are due to low interest rates by the central banks and high non-performing loans (NPLs) in the country.

- The average NPL (non-performing loans) have significantly declined in the APAC region by 11.5%. The average NPL for the countries analysed is 1.74% (among the world’s lowest).

- The average cost efficiency of APAC banks declined by 43 basis points from 45.22% in 2022 to 45.65% in 2023.

- Singapore Banks’ average cost efficiency improved by 6.9% between 2022 and 2023.

- Taiwanese banks average cost efficiency declined by 11% during the same period.

- The average loan-to-deposit ratio (LDR) is 87.5%, within the ideal 80-90% range.

- Australian banks have the highest LDR in the APAC region at an average of 109.07%.

- Apart from the Philippines and Taiwan, all the regions that fall outside the ideal range only deviate by negligible points.

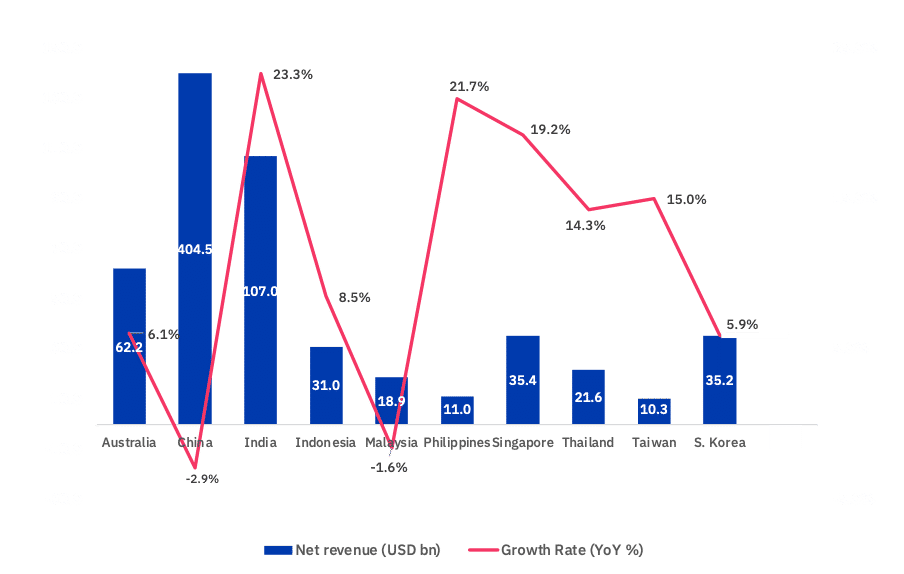

Exhibit 1: APAC Banks net revenue and growth trends (YoY basis), 2023

Financial Performance

APAC Banks surpassed USD 737 billion in net revenues in 2023

In 2023, APAC Banks recorded a net revenue growth of 3.9% YoY with an average net revenue of USD 13.4 billion. The total net revenue of the 55 banks analysed stood at USD 737 billion, up from USD 709.5 billion in 2022.

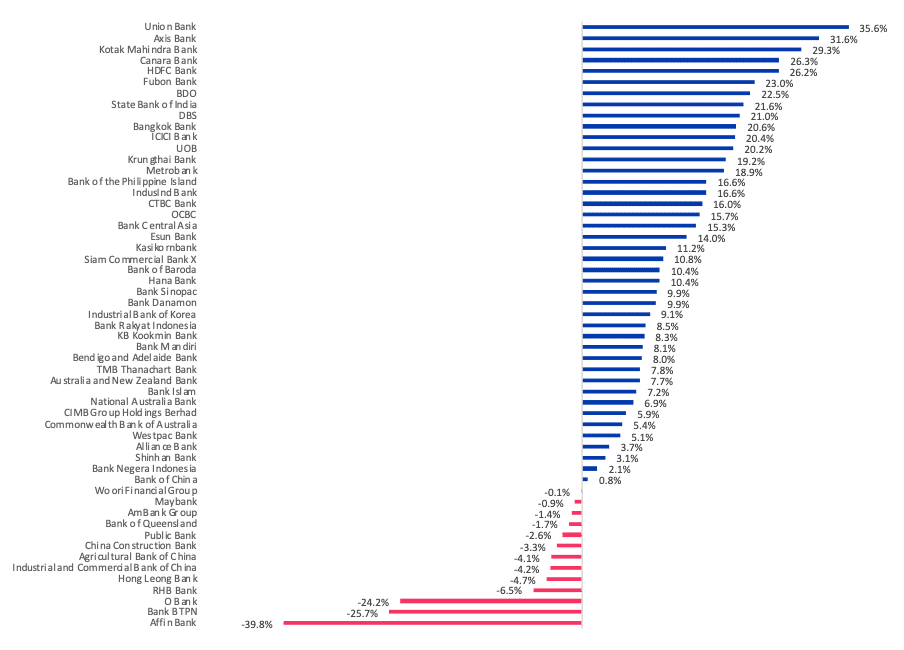

- 24 of 55 banks recorded double-digit growth in net revenues.

- 76% recorded a positive change.

- 24% recorded a negative change.

All the regions analysed reported a growth in their net revenues, with only China and Malaysia reporting a decline of 2.9% and 1.6% respectively.

Exhibit 2: Net revenue growth change between 2022 and 2023 in %

- Union Bank of the Philippines

- Union Bank recorded the highest net revenue growth at 35.6% (USD 1.28 billion).

- Net interest income grew by 33.7% from USD 700 million in 2022 to USD 935 million in 2023.

- Non-interest income grew by 41.4% from USD 239 million to USD 338 million, driven by:

- 48.5% increase in fees from parent customer transactions

- 38.5% increase in fees generated through trust, wealth management and bancassurance

- Fee income grew from USD 210.4 million in 2022 to USD 282.3 million in 2023, accounting for 83% of the bank’s total non-interest income.

- The bank’s loan book expanded by 10.1%, from USD 8.5 billion to USD 9.4 billion.

- Affin Bank

- Affin Bank recorded the highest net revenue decline at 39.8% (USD 436 million).

- Net interest income declined by 19.5% to USD 302.6 million in 2023.

- This decline is due to the low-interest rate environment and the bank’s efforts to reduce reliance on high-cost deposits.

- Non-interest income declined from USD 348 million to USD 133 million.

- 41.4% decline in net fee and commission income from USD 93.8 million to USD 55 million.

- 82.8% decline in other income from USD 240.6 million to USD 41.4 million.

- This was partially offset by a 170.3% increase in net gains on financial instruments from USD 13.7 million to USD 36.9 million.

- BTPN

- BTPN reported the second-highest decline in net revenues at 25.7%, despite a 2.6% increase in net interest income and a 5% increase in non-interest income.

- Net revenues declined by 25.7% YoY from USD 305.9 million to USD 227.3 million

- The decline was due to a 5.6% increase in the bank’s operating expenses

- 10.4% increase in personnel expenses from USD 223.5 million to USD 246.7 million

- 65.7% increase in provision for impairment losses from USD 120.8 million to USD 200.3 million

APAC Banks report USD 279 billion in net profits in 2023

APAC Banks recorded a 6.6% YoY increase in net profits from USD 261.8 billion in 2022 to USD 279 billion in 2023. The average net profits increased from USD 4.8 billion to USD 5.1 billion.

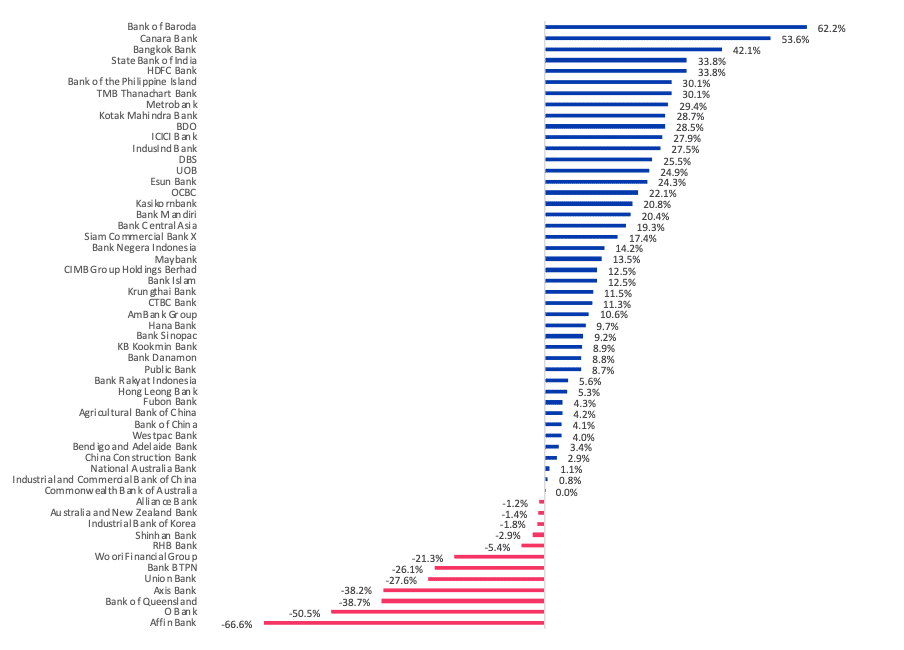

- 43 of 55 banks recorded an increase in net profits.

- 27 of 55 banks reported double-digit growth in their net profits.

- 12 of 55 banks recorded a decline in their net profits.

- 7 of 55 banks reported a double-digit decline in their net profits.

Exhibit 3: Net profit growth change between 2022 and 2023 in %

- Bank of Baroda

- BOB recorded the highest net profit growth at 62.2% (USD 2.2 billion).

- The growth was driven by a 15.6% increase in net interest income from USD 4.7 billion to USD 5.4 billion and a 51.6% increase in non-interest income from USD 1.1 billion to USD 1.7 billion.

- Affin Bank

- Affin Bank recorded the highest net profit decline at 66.6% (USD 88.3 million).

- The decline was due to a 39.8% decline in the net income from USD 698.3 million to USD 420.5 million.

- Net interest income declined by 19.5% from USD 376 million to USD 302.6 million in 2023.

- Non-interest income declined by 61.7% from USD 348 million to USD 133 million.

APAC Banks recorded USD 102.2 billion in net fee income in 2023

APAC Banks recorded a 2% YoY growth in fee incomes from USD 100.1 billion in 2022 to USD 102.2 billion in 2023. The average fee income grew from USD 1.8 billion to USD 1.9 billion.

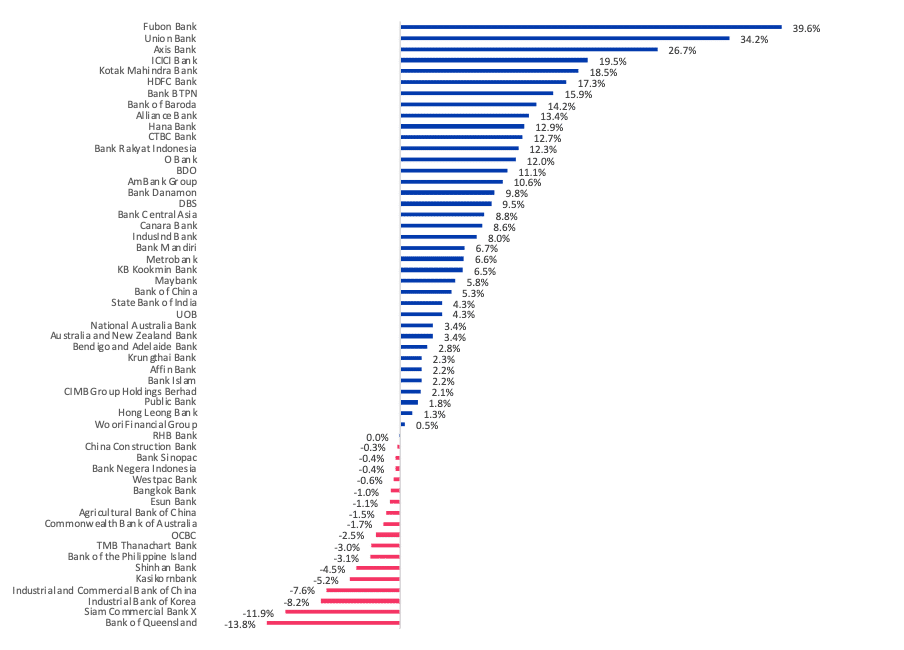

- 38 of 55 banks recorded an increase in net fee income.

- 15 banks reported double-digit growth in their net fee income.

- 17 of 55 banks recorded a decline in net fee income.

Of all the regions analysed, only China and Thailand reported declining net fee incomes. In contrast, India and Taiwan reported double-digit growth in their net fee income.

Exhibit 4: Net fee income growth change between 2022 and 2023 in %

- Fubon Bank

- Fubon Bank reported the highest growth in net fee income at 39.6%, from USD 330.4 million to USD 461.4 million.

- The growth in fee income was primarily driven by the following:

- 30% growth in wealth management fees from USD 296.8 million in 2022 to USD 385.9 million in 2023.

- Growth in credit card income from USD 0.2 million to USD 43.8 million

- The substantial growth was due to increased active cards and card spending and some adjustments in marketing expenses.

- Union Bank of the Philippines

- Union Bank recorded the second-highest fee income increase at 34.2%, from USD 210.4 million in 2022 to USD 282.3 million in 2023.

- This increase in fee income was due to customer transactions, which accounted for ~64% or USD 181.6 million of the income generated.

- Fee income through trust, wealth management and bancassurance also grew by 38.5%.

- Post-COVID-19, the Philippines experienced rising inflation, which has led to higher prices. This is offset by using credit cards, which extend the consumer’s purchasing power, leading to an exponential growth in credit card transactions in the economy.

- The rise in credit card usage attracts transaction fees, leading to higher non-interest income growth among banks, especially for Union Bank.

- Bank of Queensland

- Bank of Queensland reported the highest decline in its fee income at 13.8%, from USD 99.8 million in 2022 to USD 86.1 million in 2023.

- This decline was driven by a 26% decline in other income for the bank, from USD 50 million to USD 36.8 million. This decrease was driven by:

- One-off revenue items in 2022 relating to updated card service arrangements and an insurance termination fee

- The decrease also reflects lower gains from the sale of leasing equipment.

- Siam Commercial Bank

- Siam Commercial Bank reported the second-highest decline in fee income at 11.9%, from USD 1.1 billion in 2022 to USD 942 million in 2023.

- The decline in fee income was mainly due to the following:

- Bancassurance fees declined by 23.8% from USD 434 million to USD 331 million

- Wealth management revenue declined by 2.6% from USD 224 million to USD 219 million

- Transactional banking fees declined by 10.2% from USD 394 million to USD 354 million

APAC Banks recorded an average net interest margin of 2.89% in 2023

- The average NIM (net interest margin) achieved by the 55 banks analysed in APAC stood at 2.89% in 2023 compared to 2.85% in 2022.

- 25 out of the 55 banks analysed reported a decline in their NIM.

Exhibit 5: Change in average NIM between 2022 and 2023 in %

- China

- Chinese banks witnessed the highest NIM decline at 14.4%.

- Some of the drivers of the declining NIMs in China are as follows:

- Lowering interest rates by the Central Bank to boost economic growth leads to declining interest rates that banks can charge on loans.

- Intense competition has led to a lending spread decline, further shrinking the difference between the interest rates banks charge and pay on loans.

- The slowing Chinese economy is causing a decline in loan demand, increasing downward pressure on NIMs.

- Singapore

- Singapore banks have witnessed the highest increase in their NIMs at 18.4% between 2022 and 2023. The current average NIM stands at 2.17%.

- MAS (The Monetary Authority of Singapore) has been raising interest rates to slow inflation, allowing banks to charge higher interest rates on loans.

- The concentration of the Singapore banking industry gives the big banks a lot of market power, allowing them to charge higher lending rates and negotiate lower deposit rates.

Average NPL for APAC Banks has reduced by 23 basis points in 2023

- The average NPL (non-performing loans) of the 49 banks analysed decreased from 1.97% in 2022 to 1.74% in 2023.

- 13 of the 49 banks reported an increase in their NPLs.

- South Korea is the only country that reported an increase in NPL at 18%.

- NPLs in South Korea are among the lowest in the APAC region, with an average NPL of 0.42% in 2023.

Exhibit 6: Changes in average NPL between 2022 and 2023 in %

- India

- Indian banks recorded the highest decline in their NPLs at 26.2% between 2022 and 2023.

- Indian banks have improved their NPL with:

- Early identification and resolution of stressed loans

- Loan restructuring or selling them to asset reconstruction companies.

- Increased provisioning for NPLs reduced its impact on profitability.

- Improved credit appraisal and monitoring to identify potential NPLs early and apply corrective measures.

- Stringent credit checks to assess applicants’ creditworthiness and risk of default.

- These initiatives help India avoid disbursing loans to applicants below the acceptable credit risk level.

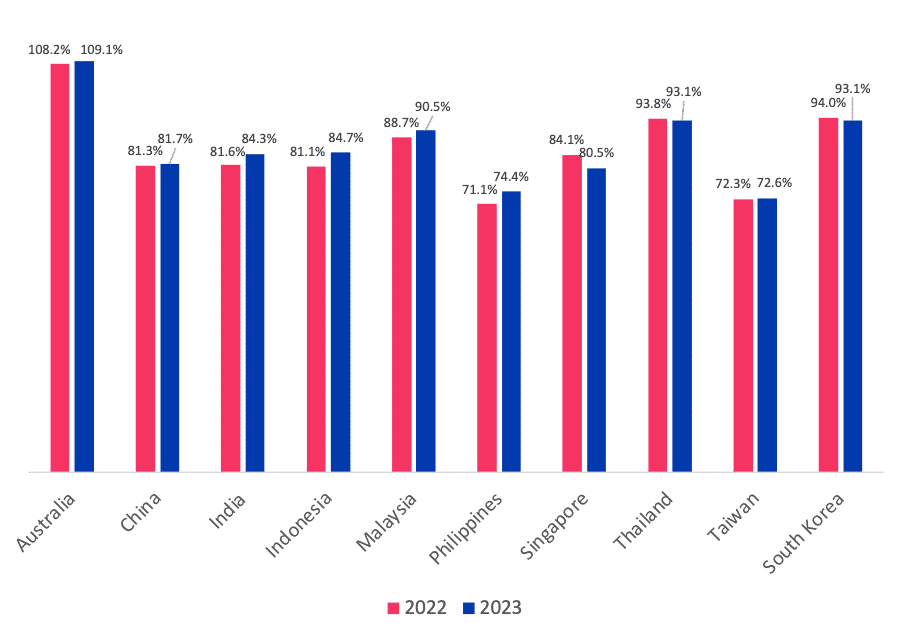

APAC Banks recorded an average cost-efficiency of 45.65% in 2023

- The average cost efficiency of the 54 banks analysed declined by 43 basis points.

- 22 of the 54 banks improved their cost efficiency.

- 16 banks analysed have their cost efficiency above the threshold value of 50%.

- Chinese banks have the best cost efficiency in the APAC region at 29.76% in 2023.

- Banks in Australia, Singapore, Thailand and South Korea improved their average cost efficiency in 2023.

- Banks in the Philippines and Taiwan have an average cost efficiency of 55.6% and 54.1% respectively which is above the threshold value of 50%.

Exhibit 7: Changes in average cost-efficiency ratio between 2022 and 2023 in %

- China

- Chinese banks excel in operational efficiency, boasting an average CE ratio of 29.76% in 2023.

- Their success is attributed to expansive branch networks and substantial customer bases, leading to economies of scale.

- This broad customer reach enables cost distribution across a larger base, reducing unit costs.

- Coupled with rapid technological advancements and government backing, Chinese banks outperform their peers in APAC regions regarding efficiency.

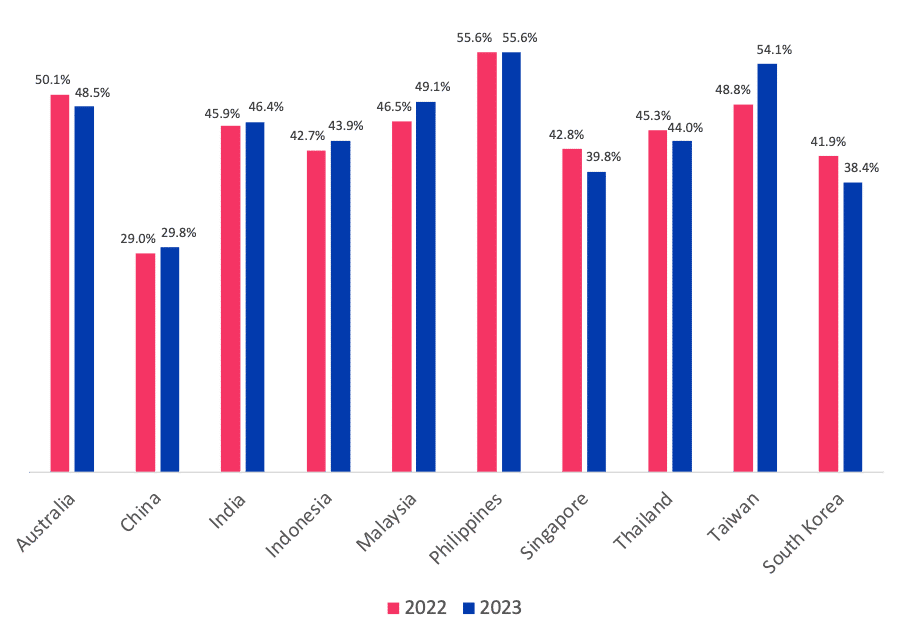

APAC Banks recorded an average loan-to-deposit ratio of 87.5% in 2023

- The average LDR (loan-to-deposit ratio) of the 55 banks analysed increased by 116 basis points from 86.34% in 2022 to 87.5% in 2023.

- Chinese, Indian, Indonesian and Singapore banks have their average LDR within the 80-90% threshold.

- Taiwanese and Filipino banks have their average LDR below the threshold value.

- Australian, Malaysian, Thai and South Korean banks have an average LDR above the threshold value.

- Australian banks have the highest LDR among APAC at an average of 109.1% in 2023, up from 108.2% in 2022.

Exhibit 8: Changes in average loan-to-deposit ratio between 2022 and 2023 in %

- Philippines

- Banks in the Philippines have among the lowest LDRs, with an average LDR of 74.4% in 2023, falling below the ideal threshold value of 80-90%.

- The low LDR can be attributed to 3 key factors:

- Philippine banks must maintain a specific portion of their deposits as reserves at the Bangko Sentral ng Pilipinas (BSP), limiting their lending capacity.

- The stringent lending criteria of BSP minimises the risk of lending to potentially unreliable borrowers, helping banks make better assessments when approving loans.

- The Philippines’ extensive informal economy lacks the conventional financial records and paperwork banks usually demand for loan applications.

- This complicates the assessment of borrowers’ creditworthiness and has deterred banks from extending loans to them.

- These banks have improved their LDRs from 71.1% in 2022 to 72.8%.

- It should be noted that Banco de Oro had an LDR of 80.15% in 2023.

AI in Banking

DBS industrialises AI across its business

The race for AI adoption and corporate pressure can lead organisations to deploy technology without clear objectives. Yet, DBS, Southeast Asia’s largest lender, has spent the past 7 years building a solid data foundation to support future big data and AI initiatives.

- DBS tapping into AI-powered nudges

- DBS has created over 100 AI and ML algorithms that analyse internal data across 15,000 customer data points. This generates 7 types of nudges that can offer personalised product recommendations and celebrate customer milestones.

- Singapore records more than 3.5 million retail and wealth customers that interact with 30 million hyper-personalised nudges every month.

- Harnessing the benefits of Generative AI

- DBS launched DBS-GPT, an internal variant of ChatGPT, supporting staff with content production and writing duties in a protected setting.

- Over 5,000 employees in DBS Singapore have utilised DBS-GPT, with plans for broader integration across the organisation.

CommBank using AI to deliver personalised customer experiences

- Customer Engagement Engine (CEE)

- CEE is an AI tool the bank employs to better understand its customers daily and deliver personalised experiences.

- The CEE conducts over 35 million decisions daily using 1,000 ML models and 157 billion data points.

- CBA aims to provide tailored assistance to customers with options like loan deferment or emergency overdraft facilities.

- CBA Bill Sense uses AI for bill prediction

- The Bill Sense functionality integrated into the CommBank mobile app assists users in forecasting their forthcoming expenses. It empowers customers to anticipate the financial resources required to meet their monthly bills.

- Moreover, this predictive feature extends its foresight to 12 months in advance, aiming to shield customers from potential bill payment burdens by spreading them out over time.

OCBC becomes the first Singapore Bank to roll out generative AI for employees

- OCBC partnered with Microsoft’s Azure OpenAI to deploy a generative AI chatbot.

- The chatbot is OCBC GPT and will be available to 30,000 global employees in November 2023.

- It aims to assist employees with writing, research, and ideation to enhance productivity and customer service.

- ChatGPT’s Large Language Models power OCBC GPT, utilising text-based information from the web to produce comprehensive responses.

- The chatbot operates within a secure environment, ensuring that information entered by OCBC staff remains confidential and is not shared with external parties.

- The bank-wide deployment follows a successful six-month trial from April to September 2023.

- Approximately 1,000 OCBC staff across various functions participated in the trial.

- OCBC GPT was utilised for tasks such as writing investment research reports, translating content, and drafting customer responses.

- Participants reported completing tasks around 50% faster than before, including time spent verifying OCBC GPT’s output for accuracy.

AI in action: How banks enhance customer experience

- AU Small Finance Bank embraces FICO’s technology

- By adopting FICO’s cloud-based platform, AU Small Finance Bank experienced a significant 30% rise in vehicle loan automation. This immediate rise helped transform lending services, reinforcing its dedication to financial inclusivity, especially for marginalised and underbanked communities.

- Development of Sabrina, the AI chatbot

- Sabrina provides information on products, promos and events, and BRI offices. It also connects customers to agents in the contact centre. Sabrina aims to help customers in communicate and attain information on BRI.

- Sabrina frees up human agents to handle more complex inquiries and build customer connections.

- Bangkok Bank’s Thai conversational AI engine

- Bangkok Bank, through its innovation program InnoHub, developed TT01 in collaboration with Singapore-based fintech Pand.ai.

- The engine achieved an accuracy rate of 96%.

- The engine is trained to process mixed-use language in Thai, English, and emoticons.

- Kookmin Bank has a human-based AI avatar

- The bank collaborated with DeepBrain to pioneer the introduction of a kiosk-style AI Banker, a groundbreaking initiative in the nation.

- This virtual entity can interact in real-time through speech synthesis, video synthesis, natural language processing, and speech recognition technologies.

- Kookmin Bank has revolutionised customer interactions by providing non-face-to-face services, significantly reducing waiting times through swift responses.

Cybersecurity is still a concern

Cyber breaches remain a significant challenge for banks

- Legacy Systems – Many banks still rely on outdated legacy systems that were not designed with modern cybersecurity threats in mind. These systems can be difficult to secure and integrate with newer, more secure technologies.

- Organized Crime – Many cyberattacks are orchestrated by well-funded and organized criminal groups that operate like businesses, with significant resources to plan and execute attacks.

- Lack of Awareness – Customers may not be aware of the security risks and may engage in unsafe practices, such as using weak passwords or falling for phishing scams.

- Digital Services Expansion – The rapid expansion of digital banking services increases the attack surface and introduces new vulnerabilities. Ensuring the security of these services requires continuous monitoring and updating of security protocols.

- Third-Party Vendors – Banks rely on a variety of third-party vendors for services and software. Security breaches at any point in the supply chain can compromise the bank’s security.

Cyber breaches and outages in 2023/24

- DBS

DBS experienced an outage in May 2024 which lasted for more than two hours. Customers reported difficulties using “Paylah!” and when logging into their bank accounts, either online or on the app. This is in addition to 5 major disruptions that the bank faced in 2023, in which 4 out of 5 disruptions were software-related.

- Maybank and CIMB

Maybank and CIMB experienced disruptions in services affecting their debit card, online banking, and ATM services in April 2024. This caused inconvenience for customers who couldn’t make online payments or transactions at retail outlets.

- ANZ

In September 2023, ANZ Bank reported a suspected network outage that caused disruptions to various services nationwide. These included app access, internet banking, credit/debit card transactions, ATMs, and even branch services.

- CBA

A network outage impacted Commonwealth Bank in June 2023. Customers experienced disruptions to internet and mobile banking functionalities. The extent of the outage and its impact varied based on different locations.

Top initiatives by APAC Banks

- Australia

- Westpac revamps its digital banking capabilities for superior CX

- Digital mortgage – The bank simplifies its lending process, using open banking data for income verification and pre-populated liabilities from consumer credit reports. Today, more than 10,800 customers use the digital mortgage solution, and the volume settled was USD 607.4 million in 2023. The proposition also allows lenders to save 60-90 minutes per application.

- BOQ is modernising its core by migrating to a cloud-based system

- ME Go – The 3rd app on the bank’s new cloud-based system, with the others being my BOQ banking app and Virgin Money. This new app is designed to create a complete in-app banking experience with features including bill tracking, live chat, and face and touch-based biometrics.

- ANZ unlocks value for customers

- Launched Tap to Pay on iPhone in September 2023

- The Worldline Tap on Mobile app allows iPhones to accept contactless card payments.

- The app provides customers with a simple onboarding experience and the ability to transact on the same day.

- Enabled Payments through Alipay+ and WeChat Pay in September 2023

- The Worldline Tap on Mobile app allows iPhones to accept contactless card payments.

- The program is enabled through a single Worldline Move 5000 EFTPOS terminal.

- No additional hardware or payment terminal is needed.

- Launched Tap to Pay on iPhone in September 2023

- China

- Industrial and Commercial Bank of China promotes intelligent asset allocation to improve value for wealth management customers

- Focused on iterating “Intelligent Brain” marketing strategies, enhancing customer perception and computational accuracy.

- Deployed 61 intelligent models and 7,200 marketing service strategies covering 50,000+ products and services.

- Generated real-time differentiated service plans for 740 million customers, fostering a new approach to digital services.

- Served 200 million customers with “Intelligent Brain” strategies, facilitating USD 264.6 billion in product purchases in 2023.

- Improved “intelligent asset allocation” service system, providing personalised asset allocation services to nearly 6 million customers.

- Grew assets under management (AUM) up by USD 61.5 billion and facilitated USD 69.8 billion in product transactions.

- CCB Cloud improved the bank’s business-technology integration

- CCB Cloud offers a comprehensive financial cloud solution comprising FinTech infrastructures, financial business operating systems, and premium applications.

- Integrated core banking business capabilities, AI, big data, and financial-level security capabilities into the “CCB Cloud”.

- CCB Cloud achieved a computing power of 463.3 PFlops by the end of 2023.

- CCB Cloud continuously improved the layout of “Multi-Zone, Multi-Region, Multi-Technology Stack and Multi-Chip” and integrated multiple computing power.

- These improvements enabled the incorporation of ultra-large-scale core financial services, key businesses and intelligent services.

- ABC’s intensified efforts in the construction of the “Digital Village” project

- The digital rural platform is utilised by over 100,000 customers, including government entities, village committees, and agriculture-related enterprises across 2,400 counties.

- Continuously iterated and optimised existing agriculture-related scenarios, introducing new ones like smart forestry and “Party Building + Credit Village”.

- By the end of 2023, 1,830 counties were contracted to the management platform for “rural collective capitals, resources, and assets”, with 1,654 counties launching the platform.

- India

- IndusInd bank collaborates with IGL

- The collaboration with Indraprastha Gas Limited (IGL) facilitates the acceptance of the digital rupee and the Central Bank Digital Currency (CBDC) by RBI.

- Customer Access – Customers can pay digital rupees at select IGL stations in Delhi NCR, promoting the use and acceptance of India’s digital currency.

- UPI Interoperability – Customers can utilise UPI interoperability to scan any UPI QR using their Digital Rupee App across all IGL stations, enhancing convenience and accessibility.

- User-friendly Experience – The Digital Rupee solution is available on iOS and Android, ensuring a user-friendly experience. It has features like peer-to-peer (P2P) and peer-to-merchant (P2M) payments with full UPI QR interoperability.

- Canara Bank’s new Data and Analytics Centre (DnA)

- The data centre is designed as a hub of excellence with modern facilities for innovation and collaboration.

- The inauguration marked a milestone as the bank entered partnerships for Data Lakehouse implementation and an Advanced Cloud Analytics Platform.

- This enabled various analytics initiatives focused on customer experience, business generation, and employee upskilling with AI/ML.

- Canara Bank organised the “DACOETHON Hackathon”, where finalists competed on themes like customer experience, fraud prevention, and default prediction.

- State Bank of India’s handheld device for financial inclusion

- The technology-driven initiative aims to empower financial inclusion and extend essential banking services to the masses. The Customer Service Point (CSP) agents can reach out to customers wherever they are.

- The device will provide five core banking services in the initial phase, including cash withdrawals, cash deposits, fund transfers, balance enquiry and mini statements. These services account for 75% of transactions conducted at CSP outlets.

- There are plans to expand service offerings further, including account opening, card-based activities, enrolment under social security schemes and remittances.

- Axis Bank – The bank has partnered with the RBI Innovation Hub to launch two lending products powered by the Public Tech Platform for Frictionless Credit (PTPFC).

- Kisan credit cards (KCC) for agricultural growth:

- The initiative will initially be launched in Madhya Pradesh, catering to the agricultural community in the region.

- Eligible customers can access KCC with a credit limit of up to USD 1920 (INR 160,000).

- The application process is entirely digital, eliminating the need for customers to provide physical documents.

- Unsecured MSME loans for business growth:

- The bank is introducing unsecured lending on the PTPFC platform to bolster the growth of MSMEs.

- Unlike the region-specific KCC, these loans will be available throughout the country.

- Eligible applicants can secure loans of up to USD 12000 (INR 1 million), enabling business expansion.

- Kisan credit cards (KCC) for agricultural growth:

- ICICI Bank – The bank has launched ‘iFinance’, which enables retail and sole proprietor customers to attain a consolidated view of their savings and current accounts across all banks in one place.

- Users can securely link and view all their bank accounts, including savings and current accounts, in one place for easy access.

- The facility offers a comprehensive overview of income and expenses, aiding users in effective financial monitoring.

- Users can monitor spending and access category-specific expenditure details, enhancing overall financial management.

- This service allows users to link or unlink accounts in real time, providing greater control and convenience.

- Users can download consolidated account statements for all their linked bank accounts, streamlining financial record-keeping.

- Malaysia

- Maybank’s cross-border QR Pay service to China

- The expansion aims to benefit over 8 million Maybank MAE app users visiting China and more than 700,000 Maybank QRPay merchants in Malaysia, facilitating transactions made by visitors from China.

- Malaysian MAE app users can make cashless payments with Alipay merchants in China. Users scan the QR code, enter the payment amount, and receive instant payment confirmation with details in CNY and RM.

- The strategic initiative results from Maybank’s collaboration with Payments Network Malaysia (PayNet) to assist Malaysians travelling to China and inbound Chinese tourists visiting Malaysia.

- CIMB’s branch with green features

- The bank unveiled its first branch with integrated sustainable features at IOI City Towers, Putrajaya.

- The branch comes equipped with tailored facilities and services, including a priority ATM lane with improved accessibility for customers with special needs, as well as wheelchair services and designated low counters for over-the-counter transactions.

- The branch also includes features that will reduce energy consumption and emissions, including energy-efficient cooling and lighting systems, sustainable materials, recycled content and reused office furniture.

- Bank Islam’s Be U

- The bank introduced “Be U,” a fully cloud-native digital banking platform, that is expected to set the standard for future digital banks in Malaysia.

- Be U aims to provide a seamless, branch-free banking experience targeting the younger, digital-native generation. Its user-friendly interface empowers users to manage finances effortlessly.

- Be U focuses on early-stage working professionals who provide essential financial services. As users’ financial stability grows, Be U plans to offer a broader range of Bank Islam’s products and services.

- Philippines

- Union Bank partnered with Tala to launch an e-wallet for underbanked Filipinos

- The new Tala Wallet allows Filipino customers to receive credit directly, pay bills, and transfer money without transaction fees or travel. It is powered by EON and owned by Union Digital Bank.

- The partnership aims to empower individuals with access to seamless, secure, and reliable financial services, helping customers achieve their financial goals.

- In its beta phase, Tala’s digital wallet grew by 18x, with nearly two billion pesos in loans disbursed to the Tala Wallet.

- BizKo by BPI digital platform for SMEs

- BizKo is an online banking platform for sole proprietors, freelancers, professionals, partnerships, and startups.

- This subscription-based service is cost-effective and doesn’t require a maintaining deposit balance, offering a wide array of digital solutions, including:

- Invoicing for customers

- Payment collection

- Fund transfers to suppliers and employees

- Financial report generation

- VYBE by Bank of the Philippine Islands

- BPI’s digital wallet and rewards platform introduces interoperable payments via QR Ph, enabling secure payments.

- Offers a user-friendly platform for clients to access and redeem rewards points from various BPI products.

- Serve as an acquisition tool in the future towards business growth and financial inclusion due to its affordability and accessibility.

- Singapore

- DBS improving the livelihood of low-income and underserved

- The bank announced its intentions to commit USD 741 million to improve the livelihood of the low-income and underserved. The bank will deploy USD 74 million annually in Singapore and its other key markets from 2024 to enact its initiative. The funds will predominantly go towards programs dedicated to:

- Assisting individuals with their immediate daily necessities, such as food and housing

- Empowering underprivileged communities with education on digital and financial literacy

- UOBs’ ‘Better U’

- UOB announced the progressive rollout of employee support at its annual employee festival, ‘Better U’ today. The program aims to help employees further expand and gain a greater understanding of their careers at UOB, covering everything from career opportunities to benefits extending beyond retirement, including:

- A 1-year work initiative collaboration with 5 Polytechnic and 3 ITE (Institute of Technical Education) colleges in Singapore to develop the skills of their students

- A physical ‘Better U’ Campus at the Singapore Institute of Management (SIM) that focuses on upskilling and reskilling opportunities for employees

- A transition program to assist employee’s post-retirement

- UOB announced the progressive rollout of employee support at its annual employee festival, ‘Better U’ today. The program aims to help employees further expand and gain a greater understanding of their careers at UOB, covering everything from career opportunities to benefits extending beyond retirement, including:

- Thailand

- SCB collaborates with Kakaobank for a Virtual Bank in Thailand

- Leverage KakaoBank’s expertise in developing virtual banking businesses and enhance SCB’s competitive advantage.

- Form a consortium, where SCB will hold a majority stake, and KakaoBank will have a stake of at least 20%.

- Emphasise the global issue of income inequality and address financial inclusion through upcoming virtual banks.

- Aims to replicate KakaoBank’s success in disrupting Thailand’s retail banking market.

- Identify new strategic partners and strengthen the consortium’s core competitiveness for winning Thailand’s virtual banking license.

- Bangkok Bank partners with AIS 5G

- The partnership aims to enhance domestic spending through a co-branded debit card.

- Aims to add 6 million debit card users in the next 5 years and foster customer loyalty for AIS.

- The partnership can help increase the current debit card user base (9 million) by an additional 2 million within the next 12 months.

- The AIS points program now allows customers to access financial services and earn points due to the partnership.

- Users receive one AIS point for every 200 baht spent online using the card and can accumulate up to 100 points per card per month.

- Points can be redeemed for various benefits, such as phone/internet charges, food and beverage discounts on leading brands, and Line stickers.

- Krungthai’s retirement app for the self-employed

- Introduced an app-based retirement savings service named “AOMPLEARN.”

- The app enables automatic savings through the Pao Tang digital wallet for millions of self-employed Thai freelancers lacking pension plans.

- Savings are transferred to the National Saving Funds (NSF) program upon reaching 50 baht.

- Prioritises Thai citizens aged 15-60 without social security coverage.

- South Korea

- Shinhan Bank’s groupwide cloud-based AI contact center

- The AICC (AI contact centre) platform aims to streamline operations, reduce costs and improve customer service across Shinhan’s Financial Group affiliates.

- Shinhan Bank and Shinhan Card upgraded AI counselling, notification, and customer support services, utilising multimodal web views and AI voice bots for improved customer experience.

- Shinhan Investment & Securities plans to offer additional services via chatbots, while Jeju Bank introduces AI counselling and chatbot services tailored to local needs.

- Hana Bank’s partnership with BitGo for digital asset custody

- Accumulating over USD 448 billion in assets, Hana Bank aims to partner with BitGo to integrate advanced custody solutions to enhance transparency and security.

- Foster consumer trust by combining BitGo’s expertise with Hana Bank’s financial prowess and compliance standards.

- BitGo plans to establish an office in South Korea by late 2024 and recently secured USD 100 million in funding, raising its valuation to USD 1.8 billion.

- KB Kookmin’s AI Banker

- In collaboration with DeepBrain, the initiative is a first in the country. The proposition is a virtual human capable of real-time interactive communication directly with users using a fusion of speech synthesis, video synthesis, natural language processing and speech recognition.

- AI Banker greets customers at the kiosk and answers queries using KB-STA, a bank-developed financial language model.

- Answers are delivered through AI Banker’s video and voice interface, powered by DeepBrain’s AI human technology.

- It guides customers on using devices, such as Smart Automated Machines and ATMs, introduces financial products, and directs them to kiosk installation points.

- Provides information on financial topics, daily weather, and nearby facilities.

- In idle mode, the AI Banker exhibits gestures, recognises customers, and bids farewell with a Thank You when they leave.

Growth opportunities for APAC Banks

- Australia

- Combatting financial scams to safeguard customers

- Financial frauds within Australian banks have triggered a surge in consumer grievances.

- Complaints surge – Australia’s financial services dispute resolution system notes a significant uptick in complaints related to bank scams, imposing an unsustainable strain on the system.

- Diverse scam tactics – These fraudulent activities encompass various tactics, from enticing customers with high-yield fixed-term deposits to employing glossy brochures and professional follow-ups. Moreover, there’s an emerging trend of remote-access scams via chat platforms, posing risks to individuals and businesses.

- To address this issue, Australian banks have begun to roll out the Scam-Safe Accord, spearheaded by the Australian Banking Association (ABA) and the Community-Owned Banking Association (COBA).

- Financial frauds within Australian banks have triggered a surge in consumer grievances.

- Brach transformation

- The Australian Prudential Regulation Authority (APRA) reported a significant reduction in bank branches in the last year. By June 2023, 424 branches (including 122 in rural areas) have closed, exacerbating banking accessibility challenges. APRA also highlighted a worrying decline in public ATMs.

- Since 2017, Australia has seen a 60% decrease in operational ATMs, leaving less than 6,000. In 2023, over 700 ATMs were removed, contributing to an 11% decrease.

- This trend resulted in a 34% drop in rural branch numbers and a 37% overall decline since June 2017.

- The closures were attributed to customers’ preference for online/mobile banking, with little consideration for non-transactional branch visits.

- China

- Risk management

- Invest in granular data analysis – Move beyond traditional credit scoring methods and utilise big data to assess creditworthiness based on a wider range of factors (e.g., online spending habits and social media activity).

- Strengthen stress testing – Regularly conduct scenario planning to assess the impact of potential economic downturns or financial shocks on loan portfolios.

- Global integration

- Develop expertise in international regulatory compliance – Hire experienced staff to navigate complex regulations in different countries.

- Partner with established international banks – Collaborate with foreign banks to leverage their expertise in global markets and risk management.

- Focus on niche markets – Target specific sectors or regions where Chinese banks have a competitive advantage (e.g., trade finance with Belt and Road Initiative countries).

- Liquidity management

- Develop longer-term funding channels – Encourage the issuance of bonds and attract deposits with longer maturities.

- Diversify funding sources – Explore alternative funding sources such as securitisation and commercial paper.

- Improve interbank liquidity management – Strengthen cooperation between banks to facilitate smoother transfers of funds and manage short-term liquidity needs.

- India

- Establishing partnerships for new revenue streams

- Fee-based income is limited to general banking services and commissions for most Indian banks. However, Yes Bank and Federal Bank have created ecosystems to generate revenue through partnerships.

- Yes Bank has an expansive API ecosystem of 450+ APIs and 30+ fintech partnerships, with 15 more partnerships in the pipeline. The bank is taking a one-bank approach and leveraging the strengths of its existing digital assets.

- Federal Bank has a fintech landscape comprising 300+ APIs offered to 50+ fintech in 13 bundles.

- Ecosystems are efficient for banks to monetise their internal capabilities and partner with third-party providers.

- Partnerships allow banks to disaggregate and securely market their products and services to their partners’ customer base and tap into new revenue streams.

- Other Indian banks should establish ecosystems and partnerships to diversify their revenue streams and eliminate their dependence on interest income as their primary source of income.

- This is because interest income tends to become erratic since it fluctuates with interest rates.

- Potential to increase revenues

- Bank Credit – Expected to grow at 14-15% per annum in FY2024-25

- The push for better government infrastructure and higher working capital demands have incentivised banks to expand their lending portfolio.

- Retail Loans – Grew at 18.1% YoY in February 2024.

- Despite the RBI suspending the increase in repo rates and increasing interest rates during May 2022, the demand for home loans stays robust.

- Corporate Credit – Credit to corporates was up 19.4% between March 2021 and September 2023.

- Corporate borrowing is gaining momentum, yet the uncertain climate might hinder the growth linked to capital expenditure.

- Bank Credit – Expected to grow at 14-15% per annum in FY2024-25

Retail Loans

- Expects to continue growing for another 2 quarters

Despite the RBI suspending the increase in repo rates and increasing interest rates during May 2022, the demand for home loans stays robust.

MSME Segment

- Grow due to the government’s “Atmanirbhar Bharat” initiative and the Productivity Linked Incentive Scheme

Corporate Credit

- Comprises 45% of overall credit

- Expected to grow at an annual average rate of 11% till March 2024

- Driven by additional working capital requirements due to high inflation and a move from bond markets to bank loans due to interest rate movements

- Indonesia

- Financial inclusion – A significant portion of the Indonesian population, particularly in remote areas, lacks access to formal banking services.

- Establish low-cost branch formats or partner with local agents to expand physical touchpoints in underserved areas.

- Develop mobile banking solutions with minimal data requirements and user-friendly interfaces for those with limited internet access or digital literacy.

- Partner with the government and NGOs to implement financial literacy programs, educating citizens about financial products and safe banking practices.

- Digital transformation – While Indonesian banks are making strides in digitalisation, there’s room for improvement in user experience and security.

- Streamline mobile app interfaces and online platforms to create a smoother user experience.

- Implement AI-powered chatbots for 24/7 customer service and personalised financial recommendations.

- Invest in robust cybersecurity systems to protect customer data and transactions in the digital realm.

- Risk management – Ensuring financial stability requires strengthening risk management practices.

- Implement stricter credit assessment processes to minimise bad loans.

- Invest in technology to detect and prevent fraudulent activities.

- Malaysia

- Buy Now Pay Later (BNPL)

- As a more popular payment choice among APAC consumers, BNPL fintech companies have begun to offer this lucrative payment option, which is currently dominating the market share of traditional bank fees.

- The adoption of Malaysian BNPL payment seeks to grow at a CAGR of 35.4% between 2022 and 2028 and reach USD 6.88 billion by 2028.

- None of Malaysia’s top banks currently offer a true BNPL service. The closest to this are AmBank and CIMB, who both offer an instalment service on their credit cards. For instance, AmBank’s AmFlexi-Pay charges a 6% interest rate, while CIMB’s Easy Payment Plan (EPP) does not charge any interest.

- A competitive BNPL offering will help Malaysian banks in the following ways:

- Attract younger customers who prefer flexible payment options.

- Increase customer engagement with user-friendly payment experiences.

- Increased transaction volume.

- Form new merchant partnerships to strengthen and expand market reach.

- Increase revenues and improve profitability through interest charges, late fees, and merchant fees.

- Improve cross-selling of other products and services by utilising customer data and insights from BNPL transactions.

- Offering BNPL can differentiate a bank from its competitors since none currently offer a true BNPL service in the country.

- Digital-only banks

- Neobanks have been disrupting traditional banks with superior customer experience, ease of use, and popularity among the younger generation, attracting a large customer base at lower acquisition and service delivery costs.

- Malaysia’s nascent neobank sector presents a significant opportunity for local banks to leverage, with a CAGR growth of 14.24% in transaction value between 2023 and 2027.

- Recently, Bank Negara Malaysia announced 5 digital banking licenses that were approved by the Ministry of Finance Malaysia. The licenses have been split into two categories and are given to the following consortiums:

- Financial Services Act 2013 (FSA):

- Boost Holding and RHB Bank Consortium

- GXS Bank and Kuok Brothers consortium

- Sea Group and YTL Digital Capital consortium

- Islamic Financial Services Act 2013 (IFSA):

- AEON Financial Service Co., Ltd., AEON Credit Service (M) Berhad and MoneyLion Inc. consortium

- KAF Investment Bank Consortium

- Financial Services Act 2013 (FSA):

Malaysian banks should digitise their offering end-to-end. They can do this by:

- Customer Onboarding – Simplify account opening and loan applications with digital verification without visiting physical branches.

- Account Management – Offer online tools for transactions, transfers, and financial insights and analytics.

- Lending and Credit – Automate loan processes using digital platforms and analytics for risk assessment.

- Risk Management and Compliance – Utilise AI for fraud detection, AML compliance, and cybersecurity.

- Customer Service – Provide omnichannel support with AI-powered chatbots and online assistance.

- Ecosystem Integration – Collaborate with fintech partners to expand service offerings and enhance the digital banking experience.

- Philippines

- Financial inclusion – Many Filipinos remain unbanked, particularly in remote areas. Banks can address this by:

- Expanding digital banking – User-friendly mobile apps and online account opening can make banking more accessible.

- Leveraging partnerships – Collaborate with local businesses and NGOs to reach underserved communities.

- Tailoring products – Develop microfinance options and accounts with lower minimum balances.

- The Asian Development Bank (ADB) has recently sanctioned a $300 million loan to aid the Philippine government in fortifying institutional frameworks and policies. The objective is to enhance financial service accessibility for Filipinos, especially vulnerable groups, while fostering economic growth.

- Branch optimisation – The Philippines’ geography presents challenges. Banks can optimise their branch network by:

- Strategic branch placement – Prioritise underserved areas while maintaining a presence in urban centres.

- Streamlining branch operations – Utilise technology to improve efficiency and reduce wait times.

- Financial literacy – Many Filipinos lack financial knowledge. Banks can play a role by:

- Offering financial education programs – Educate customers on saving, budgeting, and investment options.

- Simplifying financial products – Make product information clear and easy to understand.

- Thailand

- Alternate sources of revenue – To enhance their fee revenues, banks should explore alternative income streams:

- Focus on Advisory Services – Banks can transition from a product-centric approach to an advisory-focused one. This change fosters deeper customer engagement, leading to increased fee-based earnings. It enables banks to excel in consumer finance amidst the digital era.

- Embrace Real-Time Payments (RTPs) – Thai banks facing a downturn in fee income from transfers can pivot their retail strategies towards prioritising faster payments. RTPs are a cornerstone in this endeavour, enabling banks to compete with fintech firms and reduce the risk of payment revenue erosion.

- Collaborate with Fintechs – Partnering with fintech entities allows banks to introduce cutting-edge digital solutions, generating fresh revenue streams. These collaborations could include offerings like personal finance management tools or specialised lending platforms.

- Open banking – With open banking, Thai banks can provide the following functionalities:

- On-Demand Salary – Modelled after neobanks like Jupiter in India, customers can withdraw a predetermined sum based on their monthly earnings, which can be repaid in full or in instalments, offering financial flexibility when needed.

- Data Collaboration – Customers can unlock access to diverse products and services by sharing their financial information with external entities. This facilitates cost-saving opportunities on loans, mortgages, insurance, etc., by enabling comparisons with offerings from different providers.

- Simplified Identity Verification – Open banking streamlines account verification and Know Your Customer (KYC) procedures. Banks can efficiently and securely authenticate customers’ identities by leveraging their financial data. For instance, CIMB Bank Philippines utilised Junio’s AI-powered identity verification solution, enhancing digital onboarding convenience for the Filipino market.

- Taiwan

- Internationalisation – Focus on niche markets – Taiwan’s strong manufacturing and technological base positions its banks well to cater to niche markets beyond geographically focused expansion.

- Industry-Specific Expertise – Partner with industry associations and research institutions to gain a deep understanding of the financial needs within specific sectors like:

- Semiconductors – Offer specialised loan products for research and development (R&D) in chip design and fabrication, new production facilities, and inventory financing for essential materials.

- Electronics Manufacturing – Provide trade finance solutions for electronics manufacturers importing components and exporting finished goods, customised insurance products for high-value equipment, and supply chain financing to manage cash flow effectively.

- Biotechnology and Healthcare – Develop financing solutions for clinical trials, equipment purchases for research labs, and bridge loans to support companies navigating regulatory hurdles to bring new drugs or medical devices to market.

- Focus on Innovation – Cater to startups and early-stage ventures within these niche markets. This could involve:

- Venture Capital and Angel Investing Platforms – Partner with venture capital firms or create dedicated platforms to connect startups with potential investors, facilitating access to funding for innovative ideas.

- Innovation-focused Loan Products – Develop loan structures with flexible repayment schedules and relaxed collateral requirements, catering to the risk profile of young companies with high growth potential.

- Mentorship Programs – Partner with industry veterans or successful entrepreneurs to offer mentorship programs that guide and support young businesses navigating the complexities of scaling their ventures.

- Industry-Specific Expertise – Partner with industry associations and research institutions to gain a deep understanding of the financial needs within specific sectors like:

- South Korea

- Embracing digitalisation – To enhance their operations, South Korean banks should prioritise investment in AI and machine learning (ML), extending beyond chatbots. They can utilise AI and ML to customise customer experiences, automate processes, and enhance fraud detection:

- Utilise AI for data analysis to identify trends, enabling personalised products to cater to diverse customer needs.

- Early detection of anomalies can mitigate fraud and minimise loan defaults by restructuring loans accordingly.

- Employ predictive analysis using AI to formulate risk models, assessing the probability of defaults and market fluctuations.

- Develop AI-driven wealth management tools that customise investment strategies based on individual risk profiles and objectives.

- Expanding into new markets – To expand internationally, South Korean banks can:

- Industry Focus – Target healthcare, technology, and renewable energy sectors. Provide tailored solutions for these industries and offer specialised financial services to Korean firms venturing into new markets.

- Geographical Expansion – Explore entry into Southeast Asia and China. Collaborate with local banks for cross-border financial services. Unveil new revenue streams in untapped markets. Yet, banks must cautiously assess the risks associated with market expansion.

Research Methodology and Assumptions

- Data collection has been done based on secondary research about the information provided by the respective banks through their investor presentation and quarterly financial statements. Twimbit follows the calendar year approach for the analysis in this report (meaning Q1 is equivalent to the period of January to March of the year).

- For fair representation and analysis, we have considered a constant currency rate for conversion from local currency to USD value. The USD conversion rate is the average calculated value from January to March 2024.

- The report analyses revenue, net profit, fee income, net interest margin (NIM) and loan-to-deposit ratio (LDR) for 55 banks. For non-performing loans (NPLs), the analysis is for 49 banks. Additionally, for cost efficiency, the analysis is for 54 banks.

- The revenue figures for all the banks analysed are net of interest and non-interest expenses.

- The fee incomes for all the banks analysed are net of their fee expenses.

- Since not all banks report their LDRs, figures for certain banks are calculated based on the loans and deposits reported in the quarterly financial statements.

Download the PDF version of the report below.

To learn about the State of APAC Banks in 2023, click here.