Key highlights

Digital trends and innovation

- BOQ introduced over 35 digital self-service tools and achieved a 34% growth in customer base through automation and digitisation.

- ANZ enhanced customer engagement with AI-driven tools like ANZ Plus and ANZ Falcon, improving fraud detection and customer experience.

Revenue

- Net revenue decreased slightly by 0.24% YoY to USD 61.67 billion in FY 2024.

- Bendigo and Adelaide Bank reported the highest revenue growth (1.11%), while Bank of Queensland (BOQ) experienced the largest decline (8.15%).

Profitability

- Overall net profit of the top six banks declined by 4.84% YoY to USD 20.39 billion in FY 2024.

- BOQ posted a remarkable 130% increase in net profit due to reduced goodwill impairment and successful integration of ME Bank.

- Bendigo and Adelaide Bank achieved a 9.66% rise in net profits.

Cost efficiency

- The average cost-efficiency ratio rose to 53.03% in FY 2024, with BOQ showing the largest increase (from 58% to 66.8%) due to higher operating expenses.

- Administrative expenses and employee costs contributed significantly to the rise in costs across several banks.

Fee-based income

- Fee income increased by 3.84%, reaching USD 6.8 billion in FY 2024.

- The Commonwealth Bank of Australia reported the highest growth in fee income (9.29%), while BOQ recorded a decline (3.52%).

Net-interest margin (NIM)

- NIM fell by 7 basis points to 1.78% in 2024 due to increased competition and higher funding costs.

- BOQ and ANZ saw the largest declines, with their NIM dropping by 13 basis points.

Non-performing loans (NPL)

- The average NPL ratio of the top six banks improved, declining to 1.87% in FY 2024 from 2.32% in FY 2023.

- CBA showed a 25% improvement in its NPL ratio, while Westpac reported a 20.5% rise.

ICT spending

- ICT spending increased by 14.48% YoY, totaling USD 6.1 billion in FY 2024, reflecting significant investments in digital transformation.

- Westpac recorded the largest increase (25.01%) due to investments in Project Unite.

Loan-to-deposit ratio (LDR)

- The average LDR ratio rose by 1.41% to 102% in FY 2024, driven by strong loan demand, especially in housing (19% growth) and business property purchases (20.8%).

The future of banking in Australia: Key trends and innovation

Bank of Queensland

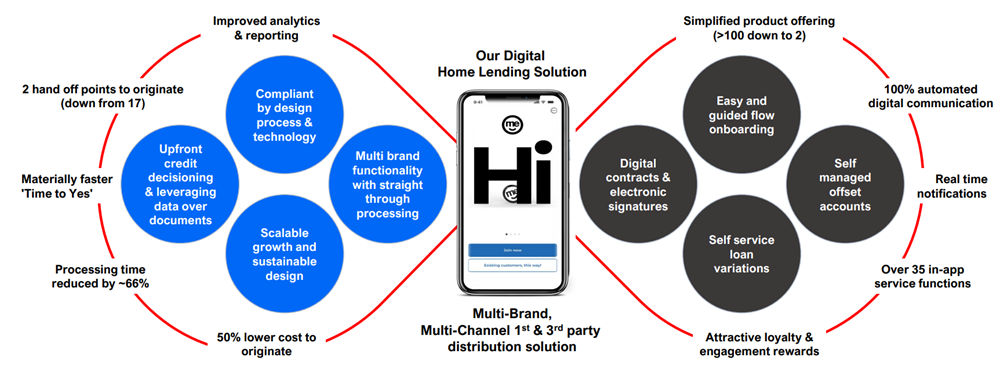

Exhibit 1: Bank of Queensland digital Home Lending solution

Bank of Queensland’s digital transformation initiatives focus on modernising its home lending solutions by enhancing automation and improving customer engagement.

- Streamlined operations: BOQ integrated automation to cut credit decision process from 17 to 2 steps.

- Innovative customer engagement: The bank introduced over 35 digital self-service tools, including e-contracts for seamless document handling, enhancing transparency and customer experience.

- Measurable outcomes: The digital transformation led to a 34% increase in customer growth and significantly improved customer satisfaction.

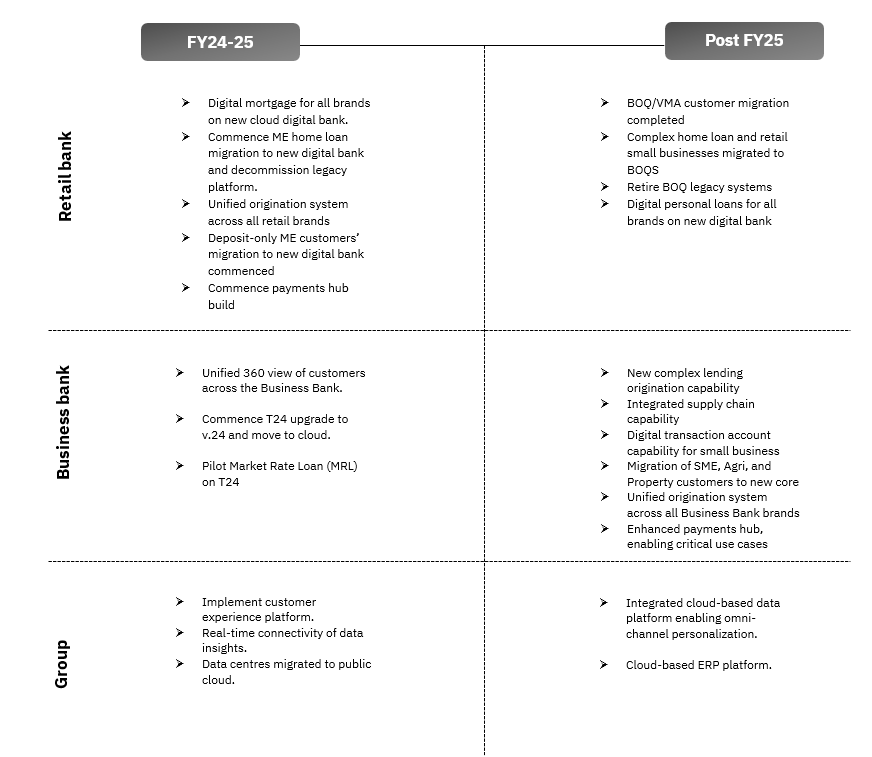

BOQ’s roadmap towards digitisation

The table presents a phased digital transformation roadmap for BOQ Bank across retail bank, business bank, and group functions from FY24 to post FY25. The roadmap emphasises modernisation and operational efficiency to support BOQ’s strategic goals.

Exhibit 2: Bank of Queensland roadmap

Australia and New Zealand Bank

Exhibit 3: ANZ Plus App

ANZ’s digitisation initiatives focus on integrating technology to streamline services and offer customised customer experiences.

- Efficient digital onboarding: ANZ Plus offers fast account setup under 3 minutes with Selfie ID, used by 50% of new customers.

- Personalised engagement and protection: ANZ Circle enables 1.5 million customer interactions with over 300 million personalized messages, while ANZ Falcon ensures constant transaction monitoring.

- Multi-channel customer service: AI messaging resolves 50% of queries, and secure video coaching boosts customer satisfaction, reflected in NPS ratings above 50.

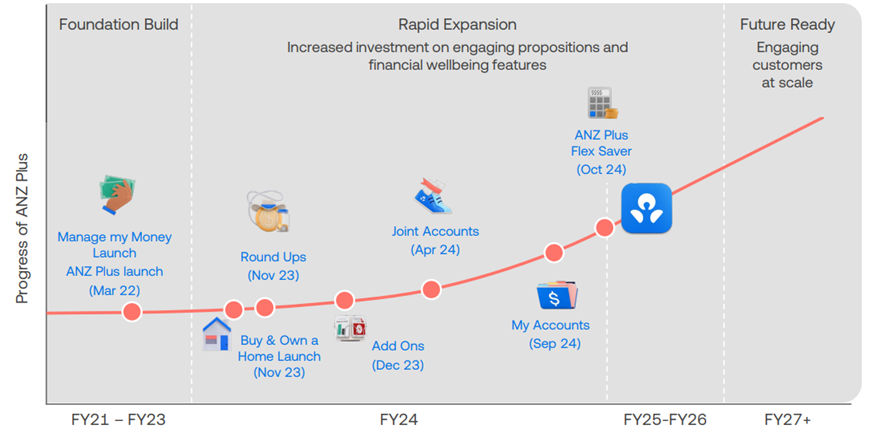

This timeline details ANZ Plus’s development milestones, starting with the foundation build and core feature launches, and progressing through FY24-FY26 to introduce new features and services.

Exhibit 4: ANZ Plus development timeline

National Australia Bank

Fraud detection

- NAB uses BioCatch biometrics and real-time scam alerts to strengthen platform security.

- Digital insights and automation blocked high-risk crypto transactions, recovering AUD 280 million and USD 184.7 million in scam losses since 2021.

- Engaging over 7,000 participants in scam prevention education which led to a 20% reduction in customer scam losses, even amidst an 18% rise in scam attempts in FY24.

NAB’s initiatives in digital transformation and customer-centric innovations

- NAB’s AI- tool “Customer Brain” enhances engagement by automating loan payments, updating compliance details, and connecting customers to services like home lending specialists.

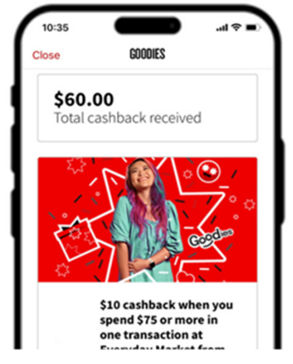

- NAB’s ‘Goodies’ program provides app-based personalised cashback and discounts from over 80 brands, distributing over USD 1.97 million since June, while business account holders receive additional partner benefits.

Exhibit 5: NAB ‘Goodies’ program

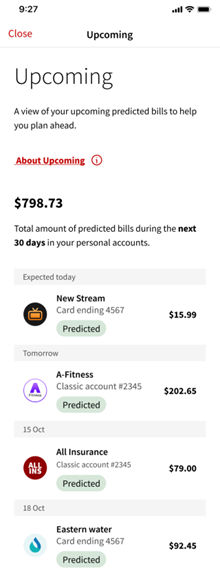

NAB’s ‘Upcoming’ feature analyses past payment data to predict and display bills and subscriptions for the next 30 days.

Exhibit 6: NAB ‘Upcoming’ feature

NAB Connect feature enhancements include strengthened fraud controls, simplified account transfers, increased platform stability, and advanced corporate card services migration during the Citi transition.

Exhibit 7: NAB Connect App

Westpac Bank

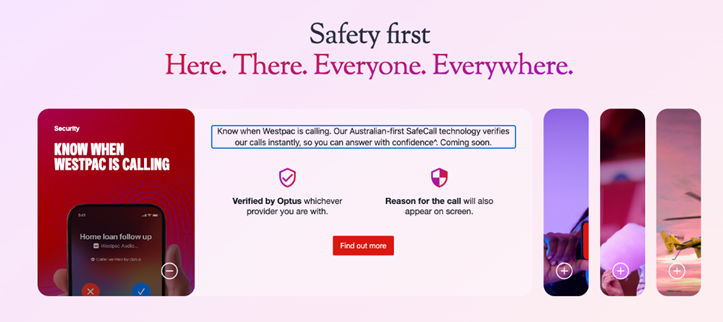

Collaborated with Optus, which has implemented an in-app calling feature to address bank impersonation scams. This feature includes a Verified Caller ID, facilitates secure app-based interactions, and enables customers to confirm their identity through app login, enhancing overall security measures.

Exhibit 8: Westpac SafeCall feature

The Westpac Unite program aims to streamline technology infrastructure by reducing the number of platforms and systems, focusing on simplifying Westpac’s IT landscape over the financial years 2025 to 2028.

- Consolidated 18 consumer processes into one using the mortgage identity verification framework, unifying 22 total processes.

- For customers, the process provides a faster and more straightforward experience.

- For employees, it frees up time for customer interaction, while shareholders see a USD 16.5 million investment expected to generate USD 10 million in annual savings and ensure compliance with the Australian Banking Association’s scam-safe accord.

Commonwealth Bank of Australia (CBA)

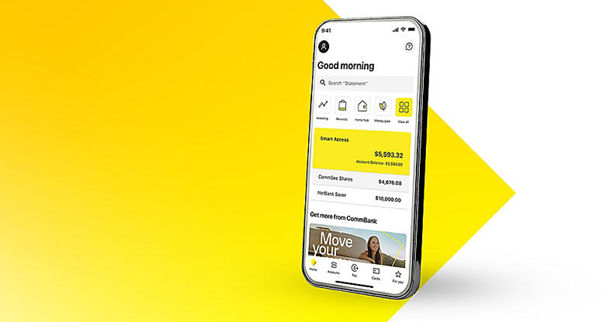

CommBank App 5.0 enhanced customer experience with personalised navigation, improved search features, seamless CommSec integration for share trading, and easy switching between personal and business profiles, alongside curated content and a streamlined login process.

Exhibit 9: CommBank App

Commonwealth Bank has launched Smart health for Pharmacies and upgraded travel booking features to improve customer experiences in healthcare and travel.

- Smart health for pharmacies: Partnered with Scrypt Ventures to provide secure medication payment options, with verifications via the CommBank app.

- Travel booking: Collaborated with Hopper to offer travel-saving goals and allows customers to use CommBank award points for travel expenses through the app.

Exhibit 10: CBA Smart Health of Pharmacies

Bendigo and Adelaide Bank

2Up is a joint account designed for managing shared expenses while keeping individual finances separate.

- Offers equal access to spending insights, providing both partners with clear visibility of financial activities.

- Streamlined joint spending with a digital card compatible with Apple and Google wallets. Each customer receives a distinct card number for efficient online transactions.

Exhibit 11: Bendigo Bank 2Up joint account

Financial performance

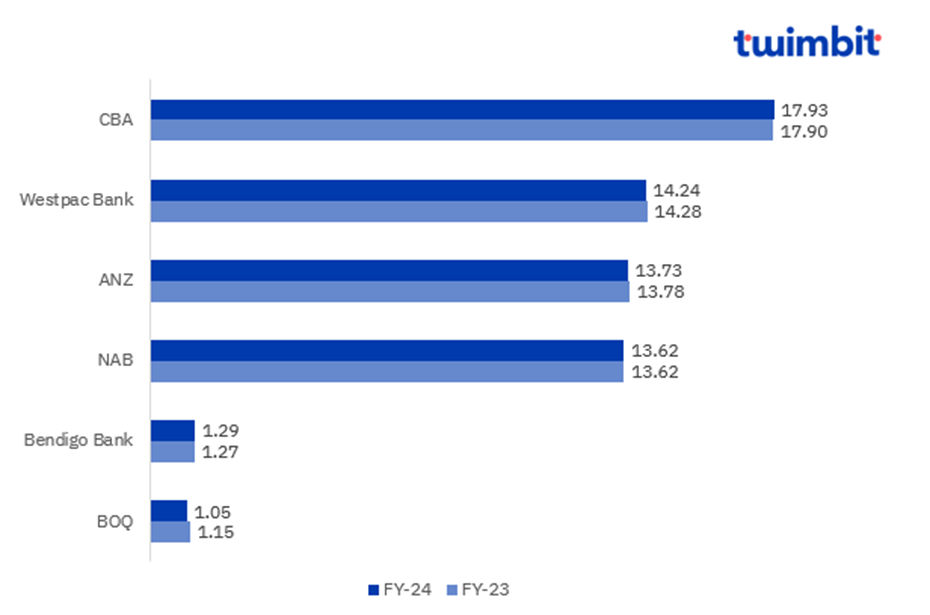

Revenue

Exhibit 12: Net revenue of Australia banks in FY 2024

Source: Bank Financials, Twimbit analysis

Net revenue decreased by 0.24% YoY, reaching USD 61.67 billion in FY 2024, down from USD 61.81 billion in FY 2023.

Bank of Queensland

- BOQ recorded the largest YoY drop in net revenue, with a decrease of 8.15% in 2024.

- Net revenue decreased from USD 1.1 billion in 2023 to USD 1 billion in 2024 due to the following reasons:

- Net interest income declined by 9% from USD 1,055 million in 2023 to USD 965 million in 2024, driven by a 2% contraction in the housing portfolio due to lower market growth, prioritisation of returns, while a 1% growth in customer deposits was offset by a shift towards term deposits and reduced savings and transaction account balances.

- Operating expenses grew by 6%, from USD 666 million to USD 705 million, primarily due to a 13% rise in employee expenses, driven by a 7.75% increase in salaries, wages, and superannuation contributions. Additionally, administrative expenses surged by 56%, largely attributed to a 33.33% rise in professional fees.

Bendigo and Adelaide Bank

- Bendigo and Adelaide Bank reported the highest YoY growth in net revenue, with an increase of 1.11% in 2024.

- Net revenue increased from USD 1.27 billion in 2023 to USD 1.28 billion in 2024.

- Other operating income grew by 6.5%, rising from USD 178 million to USD 190 million.

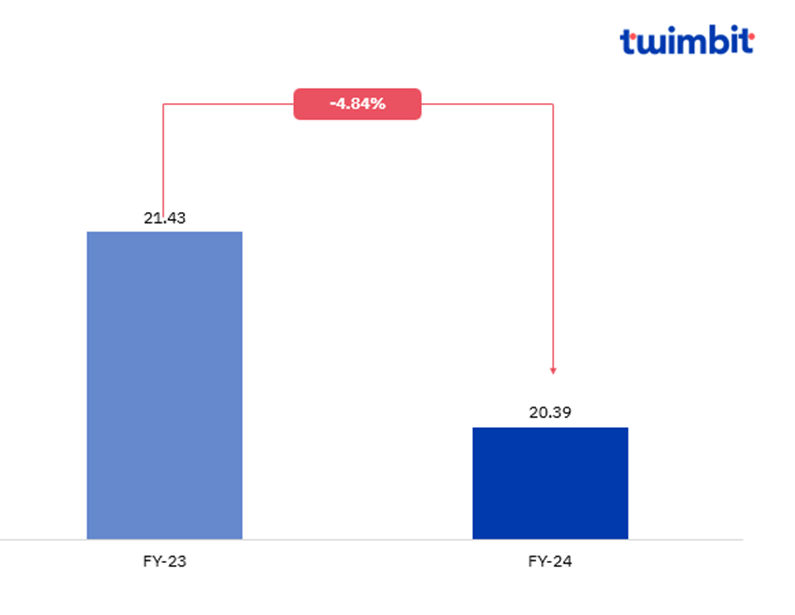

Profitability

Exhibit 13: Net profit of Australia banks in FY 2024

Source: Bank Financials, Twimbit analysis

Net profits for the top 6 banks in Australia declined by 4.84% YoY, falling from USD 21.43 billion in 2023 to USD 20.39 billion in 2024.

- BOQ saw an increase of 130% in their net profits.

- Australia and New Zealand Bank declined in its net profits by 8.04%.

- National Australia Bank reported a decrease of 5.21% in net profits.

- Westpac Bank reported a modest 2.85% decline in net profits.

- Commonwealth Bank of Australia saw a decline of 6.09% in their net profits.

- Bendigo and Adelaide Bank saw an increase of 9.66% in their net profits.

The improvement in BOQ’s performance was primarily driven by a significant reduction in goodwill impairment, reflecting no major impairments in the current period. Additionally, the completion of ME Bank integration eliminated associated costs, while the absence of remedial action plan expenses further contributed to the improved profit.

Fee-based Income

Exhibit 14: Fee income of the top 6 banks in Australia

Source: Bank Financials, Twimbit analysis

Fee income increased by 3.84%, reaching USD 6.8 billion in 2024, compared to USD 6.5 billion in 2023.

Commonwealth Bank of Australia has reported the highest growth at 9.29% YoY, from USD 1.8 billion in 2023 to USD 2 billion in 2024. Bank of Queensland reported a significant drop in its growth at 3.52%, from USD 93.6 million to USD 90.3 million.

Commonwealth Bank of Australia

CBA has reported a 9.29% YoY increase from USD 1.8 billion in 2023 to USD 2 billion in 2024

- Earnings from foreign exchange and card transactions surged as customer engagement in these activities increased.

- The rise in fee income is driven by higher lending activity among individual, business, and institutional customers.

Bank of Queensland

- Bank of Queensland reported a decline in its growth at 3.52%, from USD 93.3 million to USD 90.3 million.

- Banking fee income declined by 16% YoY compared to FY 2023, primarily due to a decline in housing volumes and reduced trading income, partially offset by higher foreign exchange sales and gains from the sale of leasing equipment.

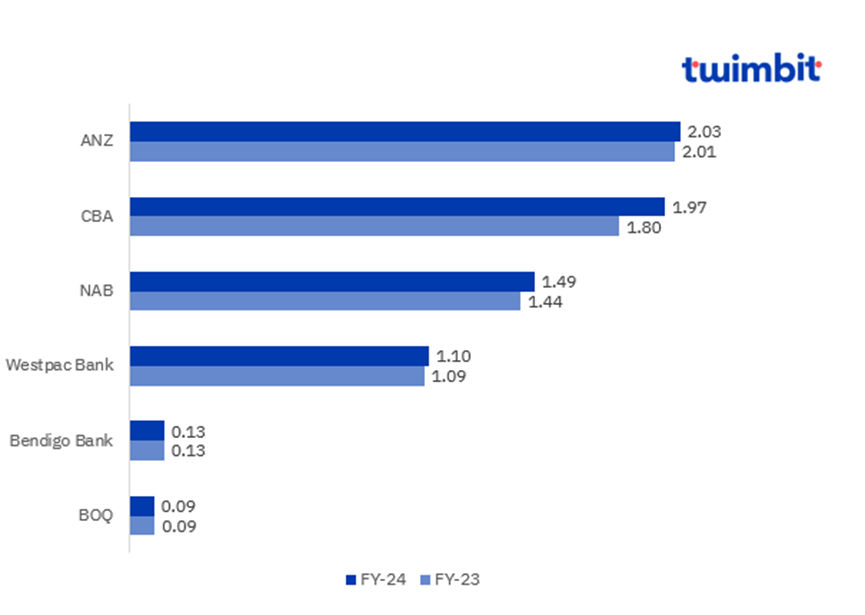

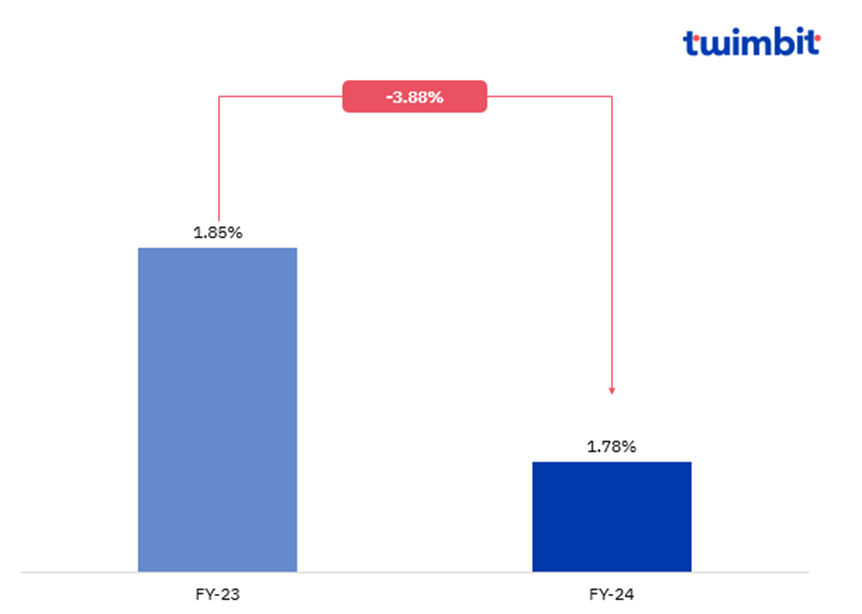

Net interest margin (NIM)

Exhibit 15: Average net-interest margin of the top 6 banks in Australia

NIM decreased by 7 basis points, dropping to 1.78% in 2024, down from 1.85% in 2023.

- BOQ reported a 13-bps decline in its NIM, which now stands at 1.56%.

- ANZ Bank NIM dropped by 13 bps, now reaching 1.57%.

- NAB reported a 3-bps decline in its NIM, which now stands at 1.71%.

- Westpac Bank reported a 2-bps decrease in its NIM, currently standing at 1.93%

- CBA reported an 8-bps decline in its NIM, which now stands at 1.99%.

- Bendigo Bank reported a 4-bps decline in its NIM, which now stands at 1.9%.

Overall, banks in Australia have seen a decline in their NIM, mainly due to higher operating costs and intensified competition in the mortgage market. Efforts to attract new loans, along with increased payouts to depositors, have further compressed margins.

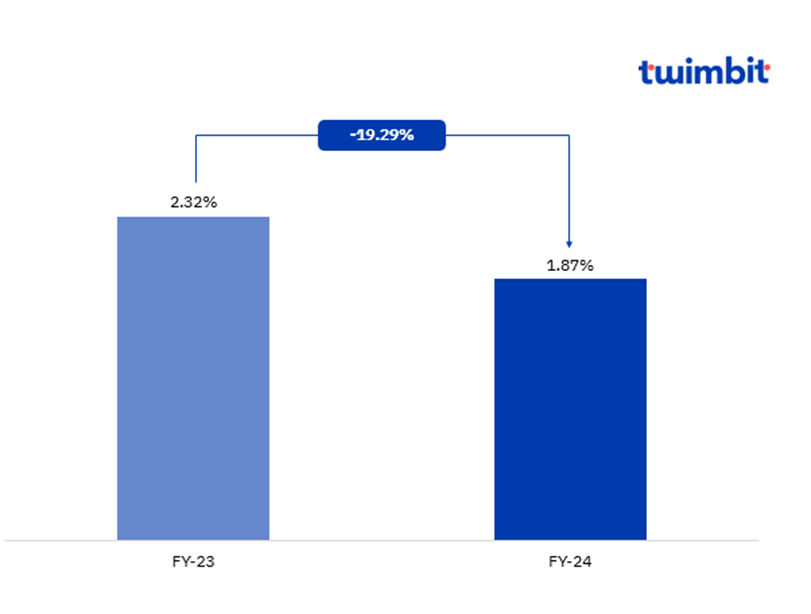

Non-performing loans (NPL)

Exhibit 16: Average NPL of the top 6 banks in Australia

The average NPL ratio of the top 6 banks decreased from 2.32% in 2023 to 1.87% in 2024, reflecting a YoY decline of 19.29%.

- BOQ reported an 18.46% increase in its NPL, which has now reached 1.25%.

- ANZ Bank’s NPL decreased by 2%, now standing at 0.21%.

- NAB reported an 11.11% increase in its NPL, which now stands at 0.20%.

- Bendigo Bank reported a 20% increase in its NPL, which now stands at 0.12%.

- CBA’s NPL ratio decreased by 25% YoY, from 12% in 2023 to 9% in 2024.

- CBA reported a decrease in loan impairment expenses, falling from USD 730.8 million in FY-23 to USD 529 million in FY-24, reflecting improved credit quality and a lower expectation of losses from its lending activities.

- Westpac Bank’s NPL ratio increased by 20.5% YoY, rising from 0.39% in 2023 to 0.47% in 2024.

- Westpac has reported a significant rise in delinquencies, particularly in residential mortgages and consumer finance. This increase reflects broader economic pressures and challenges faced by borrowers, leading to a higher proportion of loans being classified as non-performing.

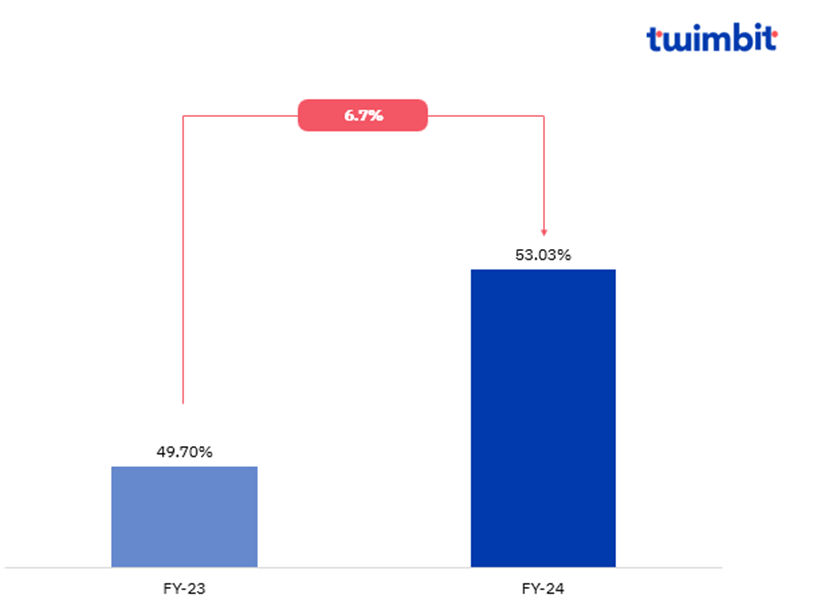

Cost-efficiency (CE)

Exhibit 17: Consolidated cost-efficiency of the top 6 banks in Australia

The average cost-efficiency ratio for the top 6 banks in Australia increased to 53.03% in 2024, compared to 49.7% in 2023.

In FY 2024, Bendigo and BOQ reported cost-efficiency ratios of 57.5% and 66.8% respectively. The remaining banks had a cost-efficiency ratio below Australia’s 53% threshold, a trend consistent with FY 2023.

BOQ saw the largest increase in its cost-efficiency ratio, rising from 58% in 2023 to 66.8% in 2024, reflecting a 4% YoY decline in non-interest income. While higher income from third-party credit cards, insurance products, and trading activities provided some support, it was insufficient to offset the overall decrease.

The ratio was further impacted by a 6% rise in operating expenses, driven by a 13% increase in employee costs and a substantial 56% surge in administrative expenses, including a notable rise in professional fees.

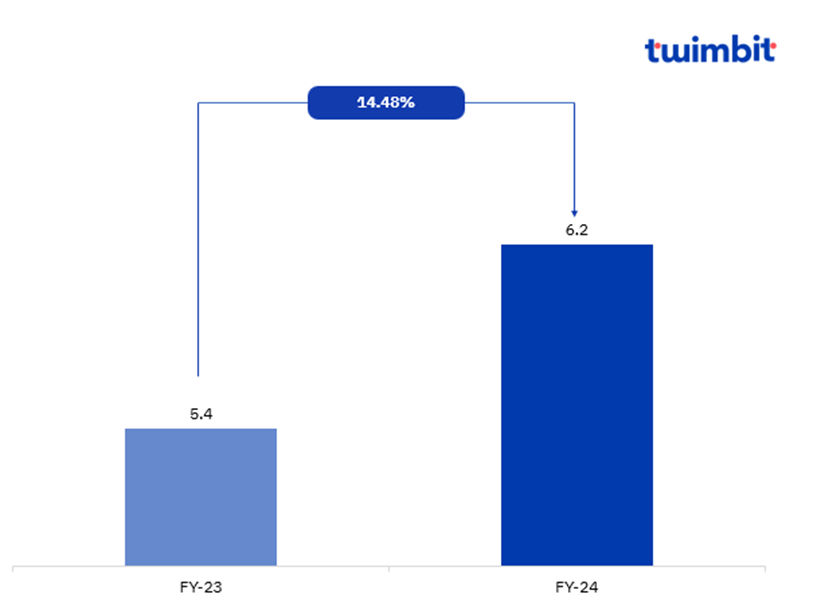

ICT spending

Exhibit 18: Consolidated ICT spending of the top 6 banks in Australia

Source: Bank Financials, Twimbit analysis

ICT spending for Australian banks increased by 14.48%, rising from USD 5.4 billion to USD 6.1 billion.

- CBA reported a 9.28% increase in its ICT, from USD 1.3 billion in 2023 to USD 1.5 billion in 2024.

- ANZ Bank’s ICT spending increased by 12.65%, from USD 1.1 billion in 2023 to USD 1.2 billion in 2024.

- NAB reported a 12.11% increase in ICT spending, rising from USD 1.2 billion in 2023 to USD 1.3 billion in 2024.

- Bendigo Bank reported a 17.95% increase in its ICT spending, rising from USD 62 million in 2023 to USD 73 million in 2024.

Westpac Bank

- Westpac Bank recorded a 25.01% YoY increase in ICT spending, rising from USD 1.45 billion in 2023 to USD 1.82 billion in 2024.

- Westpac’s increase in technology expenses in 2024 is mainly driven by significant investments in the Project Unite initiative, rising software and vendor costs.

Bank of Queensland

- BOQ recorded a 3.96% decrease in ICT spending, falling from USD 199.2 million in 2023 to USD 191.3 million in 2024.

- The decrease was due to reduced amortisation and changes in investment spending that moved project costs between technology and employee expenses. However, inflation and increased license and cloud computing costs partially balanced this out.

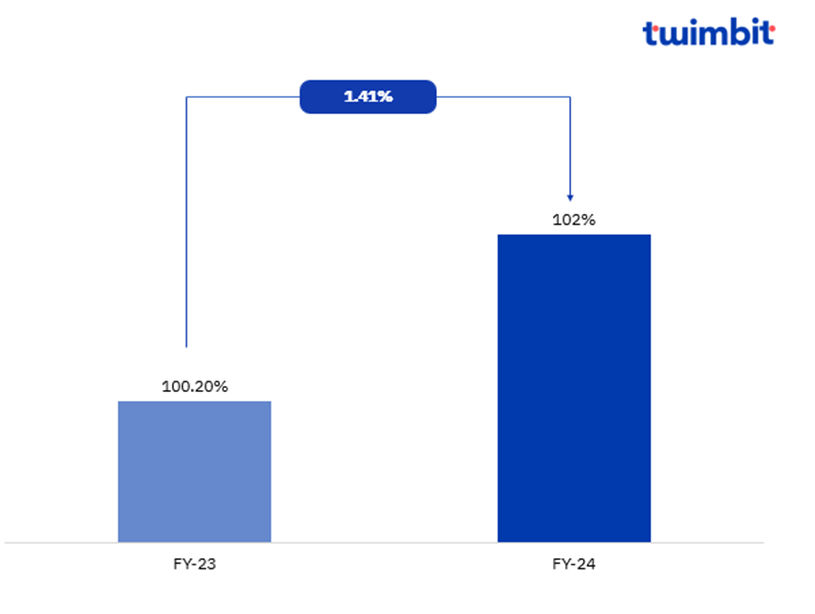

Loan-to-deposit ratio (LDR)

Exhibit 19: Average LDR ratio of the top 6 banks of Australia

The average LDR ratio of Australian banks increased by 1.41%, from 100.2% in 2023 to 102% in 2024.

There has been a notable increase in loan demand, particularly in the housing sector, which grew by 19% and in the business sector with property purchases rising by 20.8%

Australia and New Zealand Bank

- ANZ recorded the largest YoY increase in its LDR ratio, rising by 2.76% from 109.8% in 2023 to 112.8% in 2024.

- Gross loans and advances increased by 13.6%, rising from USD 468.7 billion in 2023 to USD 532.3 billion in 2024.

- Customer deposits increased by 10.5%, rising from USD 426.8 billion in 2023 to USD 471.7 billion in 2024.

Key lessons for Australian banks

Insights from service disruption in Westpac Bank

In October 2024, Westpac and St George experienced a multi-day disruption in online and mobile banking services.

- Customer impact: Over 6,000 complaints due to inaccessible funds and stalled transactions.

- Technical issues: Linked to technical failures, with cybersecurity threat speculation prompting government evaluation for possible DDoS attacks.

- Customer reactions: High customer frustration expressed on social media, with demands for better communication and app/infrastructure improvements.

Key lessons for banks:

- Robust infrastructure: Ensure resilient and scalable IT infrastructure to prevent prolonged outages.

- Effective communication: Prioritize clear, timely updates to affected customers during disruptions.

- Proactive cybersecurity measures: Regularly assess and fortify against potential threats to safeguard services.

- Transparency: Provide comprehensive explanations and corrective actions post-incident to rebuild trust.

- Customer-centric approach: Enhance digital platforms based on customer feedback to improve customer experience and satisfaction.

Combatting cyber frauds through government and bank interventions

- Launch of national anti-scam centre (NASC): Established in July 2023 to facilitate scam intelligence sharing among government bodies, law enforcement, and private sector entities.

- Collaborative initiatives: NASC, alongside federal agencies, has taken action to remove websites hosting phishing and investment scam content.

- Bank measures on cryptocurrency: From mid-2023, banks have implemented controls to limit transactions involving ‘high risk’ cryptocurrency exchanges.

- Support for scam victims: Automatic referrals to IDCARE offer victims vital support and guidance.

- Potential further interventions: Collaboration with telcos and digital platforms could provide additional measures to enhance scam prevention efforts.

These interventions involve multi-agency collaboration and proactive measures to combat scams in the financial sector.

Growth opportunities for Australian banks

Amid evolving market dynamics and technological advancements, Australian banks can capitalise on key growth opportunities to strengthen and enhance their market presence:

- Australian banks can drive trading efficiency and strengthen competitiveness by adopting algorithmic trading strategies, exemplified by NAB’s FX Algorithmic solutions. By automating large-scale order execution and leveraging parameters such as price, volume, and timing, these strategies optimize transactions, delivering cost efficiency and precision.

- The Reserve Bank of Australia (RBA) and the Digital Finance Cooperative Research Centre (DFCRC) have embarked on “Project Acacia,” a strategic initiative focused on advancing wholesale Central Bank Digital Currency (CBDC) and asset tokenization. This project represents a significant opportunity for Australian banks to leverage the potential of wholesale CBDCs. By adopting this innovative technology, banks can effectively mitigate counterparty and operational risks, optimize the use of collateral, and drive enhanced transparency across the financial ecosystem. As the project progresses, it could serve as a catalyst for greater efficiency and stability in the financial markets.

- Australian banks can harness GenAI to deliver hyper-personalized financial solutions by analyzing real-time transaction patterns, spending behaviors, and credit histories. AI-driven automation enhances loan processing, reduces errors, and strengthens risk assessment, while intelligent compliance systems ensure seamless adherence to APRA and ASIC regulations. Advanced fraud detection models identify anomalies more effectively, minimizing false positives and reinforcing security. By embedding GenAI across core operations, banks can improve efficiency, elevate customer experience, and build greater trust in an increasingly digital financial landscape.