Key highlights

- Net revenues grew by 10.86% to USD 62.88 billion, driven by a 13.67% growth in net interest income.

- Stringent macroeconomic policies and financial conditions portray an economic slowdown of 1.25% in 2024.

- Australia maintains low unemployment, surpasses potential output, and witnessed increased housing prices following the 2022 correction.

- Potential risks indicate elevated inflation and environmental uncertainty.

- Future revenue and earnings face potential moderation

- Declining mortgage and business credit growth – The market is expected to remain highly competitive despite reduced competition within the crucial home loan sector.

- Inflation-driven escalation in operating expenses – Increased staff, technology, and cybersecurity expenses.

- A slight decline in asset quality – Household finances are under pressure due to increased interest rates and inflation, while businesses grapple with elevated input and labour costs.

- Peaking Net Interest Margin (NIM) constrained by fierce competition for mortgages and deposits – NIM declined in the second half compared to the first half across all banks.

- Australia has introduced the Scam-Safe Accord, a pioneering initiative to enhance customer protection against scams and cyberattacks.

- The average NIM (Net Interest Margins) for Australia’s top 6 banks is 1.83%.

- The average NPL (Non-Performing Loans) for Australia’s top 6 banks is 0.37%.

- Cost efficiency for Australian banks improved by 4.19% in FY 2023.

- Average cost efficiency improved from 51.52% in FY 2022 to 49.36% in FY 2023.

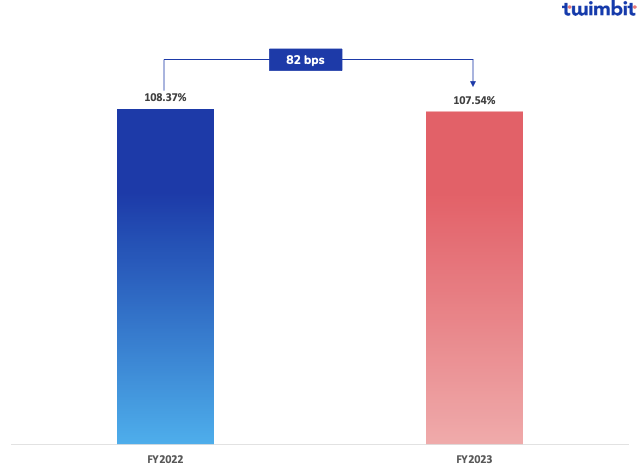

- Australian banks’ current loan-to-deposit ratio (LDR) is at 107.54%, down from 108.37% in FY 2022.

- Between June 2022 and 2023, banks have closed 424 branches or 11% of all bank outlets.

- 122 of the 424 branches were in regional and remote areas outside Australia’s major cities.

- Over 700 ATMs were removed from operation during the same period, accounting for an 11% dip.

- Australian banks have taken the following initiatives during FY 2023:

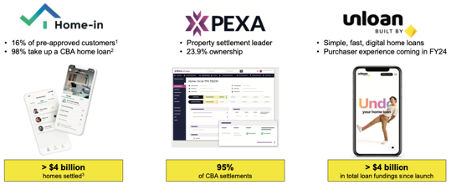

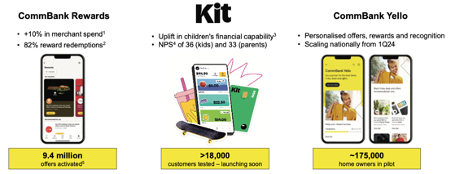

- CBA focuses on digitising home loan journeys, payments and customer rewards to manage them end-to-end.

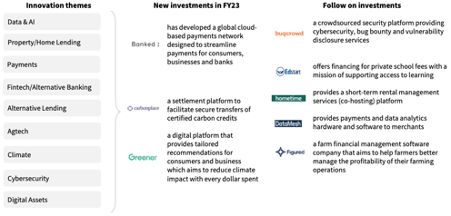

- NAB’s venture capital arm, NAB Ventures, made new investments in a cloud-based payments network in collaboration with Banked.

- ANZ automated their home loan journeys without human intervention through ANZ Plus.

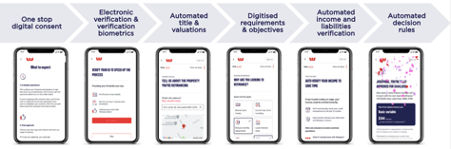

- Westpac simplified its lending process using open data for income verification and pre-populated liabilities from consumer credit reports.

- Bendigo launched its multi-year Financial Inclusion Action Plan to collaborate with stakeholders and promote financial well-being.

- BOQ modernised its core by migrating its three apps, ME Go, myBOQ and Virgin Money, to the new cloud-based system.

Digital measures of success

CBA:

- USD 53 billion in monthly transactions via the mobile app

- 8.7 million digital active customers in FY 2023

- 75% of digital transactions by value

- 39.1 monthly digital logins per active customer

NAB:

- 61% of personal transaction accounts were opened digitally

- 3.5 million digital active customers in FY 2023

- 74% of everyday banking products are opened digitally

- 3 million mobile active customers in FY 2023

ANZ:

- 333 million digital payments processed in FY 2023

- 68% of deposit accounts opened through digital channels

- 4 million digital active users in FY 2023

Westpac:

- 87% of mortgages processed on digital platforms

- 5.8 million digital active customers in FY 2023

- 395 million digital transactions

- 5.43 million average app sessions per day

Top Innovations by Australian Banks

CBA prioritises home loan journeys, payments and customer rewards to manage them end-to-end digitally

Exhibit 1: Journey 1 – Home buying and ownership

Exhibit 2: Journey 2 – Payments

Exhibit 3: Journey 3 – Customer Rewards

NAB focuses on enhancing its digital banking touchpoints for superior CX

In FY 2023, the bank delivered the following features to its digital channels to provide simpler, safer and more personalised customer experiences (CX).

NAB Mobile App

- Apply for new products directly

- View and control bills and payments with PayTo

- Enhancements to in-app calling when updating SMS security

- Proactive scams and fraud alerts in key payment flows

NAB Internet Banking

- Real-time authenticated chat

- Apply for business transaction accounts within Internet banking

- Proactive scam and fraud alerts

- Proactive and targeted notifications

NAB Connect

- Faster payments via the all-new Domestic Payments experience

- Increase self-service support and help capabilities

- Enhanced security and fraud warnings for security tokens

- Equipment finance capability

- Introduced a new digital user amendment process

Innovating with NAB Ventures – Works alongside other parts of the bank that test and leverage new customer propositions and technological developments.

Exhibit 4: NAB Venture’s new and follow-up investments in FY 2023

ANZ unlocks value for customers with customer journey management and strategic partnerships

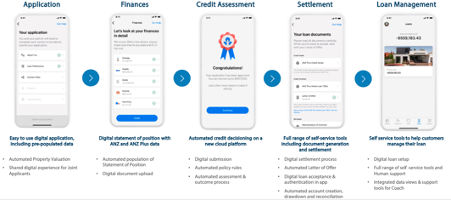

ANZ Plus allows customers to automate their home loan journey without human intervention.

Exhibit 5: ANZ Plus’ Automated Home Loan Journey

ANZ partners with Worldline to provide small business, commercial and institutional customers in Australia access to market-leading point-of-sale and online payment technology.

Deployment of a market-leading merchant platform in April 2023

- New customers are onboarded with flexible customer-led pricing options, including fixed-price bundled packages.

- Customer migration from ANZ’s platform to the new platform is underway.

Launched Tap to Pay on iPhone in September 2023

- The Worldline Tap on Mobile app allows iPhones to accept contactless card payments.

- The app provides customers with a simple onboarding experience and the ability to transact on the same day.

Enabled Payments through Alipay+ and WeChat Pay in September 2023

- The Worldline Tap on Mobile app allows iPhones to accept contactless card payments.

- The program is enabled through a single Worldline Move 5000 EFTPOS terminal.

- No additional hardware or payment terminal is needed.

Westpac revamps its digital banking capabilities for superior CX

Digital mortgage

The bank simplifies its lending process, using open banking data for income verification and pre-populated liabilities from consumer credit reports. Today, more than 10,800 customers use the digital mortgage solution, and the volume settled was USD 607.4 million in FY 2023. The proposition also allows lenders to save 60-90 minutes per application.

Exhibit 6: Digital mortgage process at Westpac

EFTPOS Air

The bank launched a convenient way for mobile businesses such as trades and market stalls to get paid seamlessly using their iOS or Android devices. EFTPOS AIR also provides sales insights and customer payment tracking. Westpac is the only central bank in Australia that offers this capability across iOS and Android devices.

Data and Digital Capability

The bank’s skill upliftment program prepares its workforce for challenges and opportunities in an ever-increasing digital world.

- Improved over 5,000 employees’ critical data and digital skills, mindsets and behaviours.

- Co-created by over 150 experts from Westpac and Deloitte.

- Offers eight learning pathways at a foundational or intermediate proficiency level to improve capabilities across 29 skills.

Bendigo is transforming its business by becoming a market leader in innovation

Up Digital Bank

In collaboration with Ferocia, Up offers savings tools, a Save Now Buy Later model, gamified user engagement and tracking tools.

Performance highlights from FY 2023:

- Save Up 1000 – 145,000+ customers started saving with ‘Save Up’, 10,800 completed, USD 13.38 million saved, ~20% have never saved AUD 1k before

- Locked Savers – USD 49.50 million saved in 30,000+ locked ‘Savers’, ~21 days average lock duration

- Maybuy SNBL – 64% of customers bought the product, and 36% chose not to buy, resulting in customers avoiding USD 535,000 in impulse purchases

- Up Home mortgages – USD 344 million in identified savings towards a home, USD 49.50 million in completed Up Home loans

- 2Up Joint Accounts – 24% of active customers have 2Up joint accounts

2024 Victorian Flood Appeal

The initiative is conducted by the Community Enterprise Foundation (CEF) to support Victorian communities affected by recent flooding.

Partnership with CBA

The collaboration aims to test the ‘NameCheck’ technology in its Up banking app and safeguard Australians from financial fraud.

Financial Inclusion Action Plan

The bank has taken a significant step towards financial inclusivity by introducing its inaugural Financial Inclusion Action Plan (FIAP). Developed collaboratively with stakeholders, the FIAP guides the bank’s actions in promoting financial well-being.

The plan focuses on four key areas:

- Products and services – Provide fair, affordable and accessible products and services.

- Financial capability – Enhance the financial capabilities of staff, customers and the community by fostering a deeper sense of organisational culture.

- Financial vulnerability – Investigate and collaborate on improved responses to better understand financial vulnerability.

- Economic security – Remove barriers and provide opportunities for equality and growth with improved economic security measurements.

BOQ is modernising its core by migrating to a cloud-based system

ME Go

ME Go is the 3rd app on the bank’s new cloud-based system, with the others being my BOQ banking app and Virgin Money. This new app is designed to create a complete in-app banking experience with features including bill tracking, live chat, and face and touch-based biometrics.

Partnering with Microsoft to streamline its end-to-end digital banking experience, BOQ can now accelerate the delivery of its cloud strategy and enhance the customer experience across all delivery channels.

BOQ also collaborated with 5 charity partners: Beyond Blue, Australian Wildlife Conservancy, Minus18, National Breast Cancer Foundation and OrangeSky. Customers can select from 5 charity-linked debit cards that align with their values. And with each digital wallet payment, one cent will be donated to the charity of their choice.

ThanQ

In the last quarter of FY 2023, BOQ launched ThanQ, a unified recognition program across all brands. This program achieved an adoption rate of 69% in the first 30 days, recording over 850 recognised individuals in its success.

The focus on employee uplifting will continue in FY 2024 with plans to dive deep into inclusivity, including background, age and caring responsibilities to deliver on the bank’s diversity, equity and inclusion strategy.

Revenue

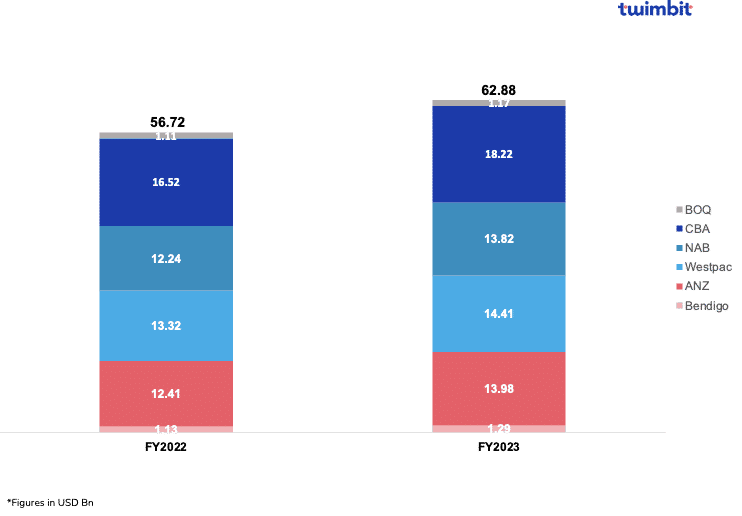

Australian banks generated USD 62.88 million in net revenues in FY 2023

Net revenues grew by 10.86%, driven by a 13.67% growth in the net interest income from USD 45.97 billion to USD 52.26 billion.

NAB

- Highest revenue growth at 12.89%, from USD 12.24 billion in FY 2022 to USD 13.82 billion in FY 2023

- The highest increase in operating expenses at 9.05%, from USD 5.53 billion to USD 6.04 billion

Westpac

- Lowest operating income growth at 8.22%, from USD 13.32 billion in FY 2022 to USD 14.41 billion in FY 2023

- 10.89% growth in net interest income partially offset by a 5.18% decline in non-interest income from USD 2.21 billion to USD 2.09 billion

- Declining fee incomes due to the sale-off of business, which generated USD 392 million in FY 2022 and USD 140 million in FY 2023

The business sale was concluded in Q1 2023. No revenue was generated in Q2 and Q3 2023.

Exhibit 7: Net revenue of Australian banks in FY 2023

The success of the initiatives taken to automate and digitise home loans by CBA, ANZ and Westpac can be attributed to the growth in the net interest incomes.

- The banks reported an 18.40%, 11.48% and 10.89% increase in their net interest incomes, respectively.

- Automation expedited the loan assessment and approval process, enabling banks to attract borrowers seeking quick decisions and potentially closing more deals.

- Automation has also helped these banks keep the growth in their operating cost lower at 3.76%, 5.85% and 0.50%, respectively.

- The three banks have reported the lowest growth in operating expenses out of all the six banks analysed.

These initiatives have also helped them reduce the abandonment rates as they:

- Streamline the application process – Automation reduces the need for human intervention and manual verification, making the process quicker and more user-friendly. CBA’s unloan offers a speedy 10-minute online application process.

- 24/7 availability – Automation has made the platforms available anytime, anywhere, allowing potential borrowers to start and complete applications at their convenience, even outside traditional banking hours.

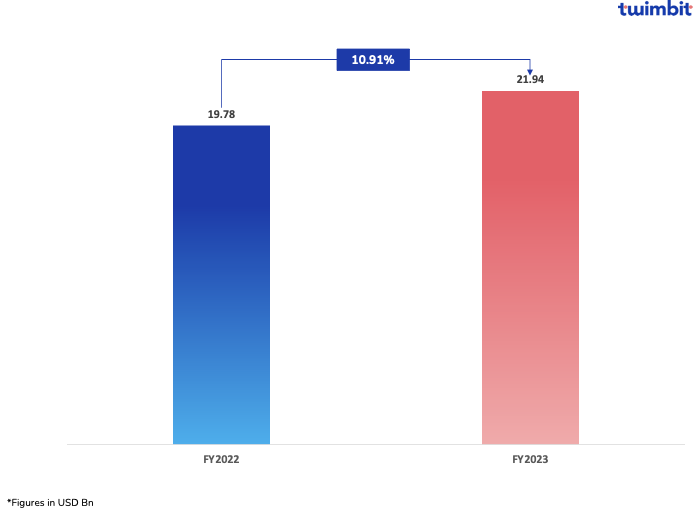

Profitability

Net profits grew by 10.91% YoY to USD 21.94 billion in FY 2023 from FY 2022

Westpac

- Highest net profit growth at 26.36%, from USD 3.81 billion to USD 4.81 billion

- 6% growth in average interest-earning assets due to loan growth and higher liquid assets

- The loan portfolio grew by 4.56% from USD 495 billion to USD 517 billion

BOQ

- Net profit declined by 69.68% from USD 0.27 billion in FY 2023 to USD 0.08 billion in FY 2023

- A USD 133.79 million goodwill impairment of the retail banking cash-generating unit (CGU) was recognised in H1’23 after conducting an impairment test

- USD 38.13 million of the cost associated with the final year of the integration of ME Bank

- USD 28.1 million after-tax provision for the estimated costs of the multi-year Remedial Action Plans (RAP), namely Program rQ and AML First

- USD 23.41 million in restructuring costs as part of the bank’s simplification program

Exhibit 8: Consolidated Net Profits of Australian Banks

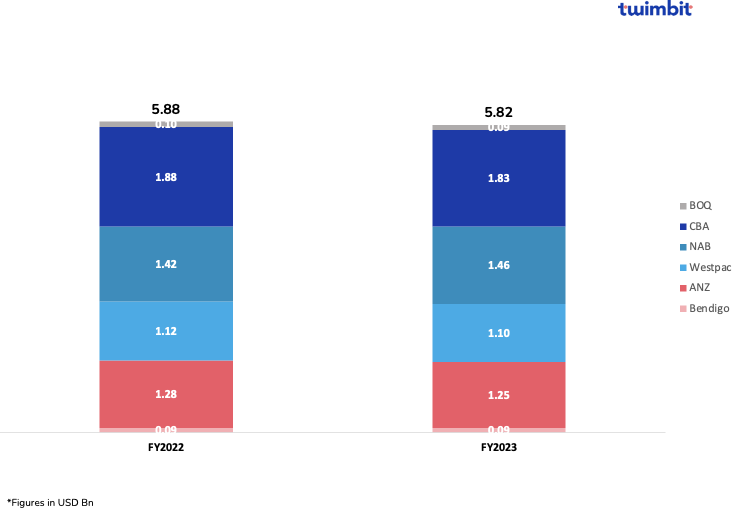

Fee-based income

Australian banks generate 9% fee income to revenue in FY 2023

Fee income declined by 1.12% to USD 5.82 billion in FY 2023 from FY 2022.

CBA reported a decline in its fee income at 2.88% due to lower CommSec equities income and institutional lending fees.

ANZ reported a decline in its fee income at 2.36% due to:

- USD 54.85 million decrease in the Australian Commercial division driven by lower revenue post Worldline business divestment

- USD 20.07 million decrease in the New Zealand division driven by lower card revenue due to regulatory fee changes introduced in November 2022

Westpac reported a decline in its fee income at 1.61% due to:

- Lower income from product simplification and lower wealth management income post-divestment

The changes in the 3 banks mentioned above were marginal regarding dollar value.

BOQ reported the highest decline in its fee income at 5.37% due to:

- Decrease in other fee income for the bank by 26% from USD 50.84 million to USD 37.46 million

- It was driven by one-off revenue items in FY 2022 relating to updated card service arrangements and an insurance termination fee

- Reflects lower gains from the sale of leasing equipment

- Partially offset by a 16% increase in banking fees from USD 48.83 million to USD 56.86 million

All banks reported declining fee incomes except NAB, which reported a slight growth at 3.02%.

Exhibit 9: Fee income of Australian banks in FY 2023

ANZ’s partnership with Worldline for a point of sale and online payment technology returned an annual revenue of USD 196 million in 2021. Australia boasts widespread adoption of electronic payments, securing the fourth global position in payment terminals per capita. The use of contactless cards and digital wallets by consumers is notably high on a global scale. Anticipated revenue growth for the alliance is expected to be in the double digits, driven by opportunities in digital onboarding, alternative payment methods, and fraud detection within the existing merchant portfolio.

Similarly, Westpac’s EFTPOS Air’s use of Android or iOS devices to accept payments allows the bank to increase its fee income.

These initiatives are expected to help these banks open new fee income revenue streams.

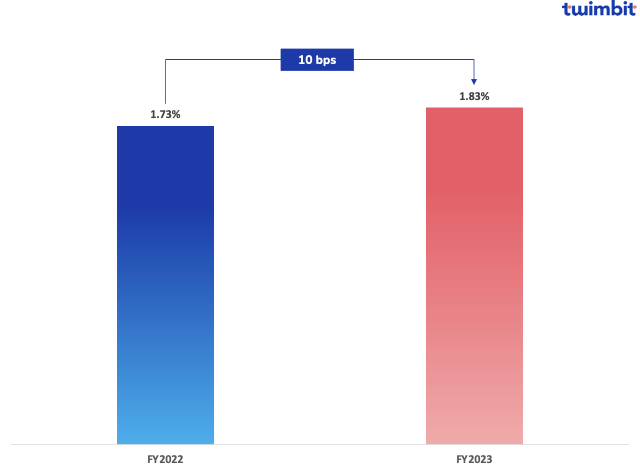

Net interest margin (NIM)

NIM has gone up by 10 bps in FY 2023 from FY 2022 level

The average NIM for Australian banks stood at 1.83% in FY2023 (Exhibit 4). RBA’s tightening of monetary policies was a key driver in the increase of NIMs. All banks reported increased NIM except BOQ, which declined by 2 bps.

Australian banks have some of the lowest NIMs among the APAC regions. This is due to lower home loan margins, continued pricing pressure on mortgages and changing customer preference from fixed-rate to floating-rate loans.

- Interest margins are under pressure due to intense pricing competition in the mortgage market and the rising cost of deposits and wholesale funding.

- Net interest income grew by 13.67% from USD 45.97 billion to USD 52.26 billion.

- Interest income grew by 99.08%, from USD 62.57 billion to USD 124.56.

- Interest expense grew by 310% from USD 18.18 billion to USD 74.55 billion.

Exhibit 10: Consolidated NIM for the top 6 banks in Australia

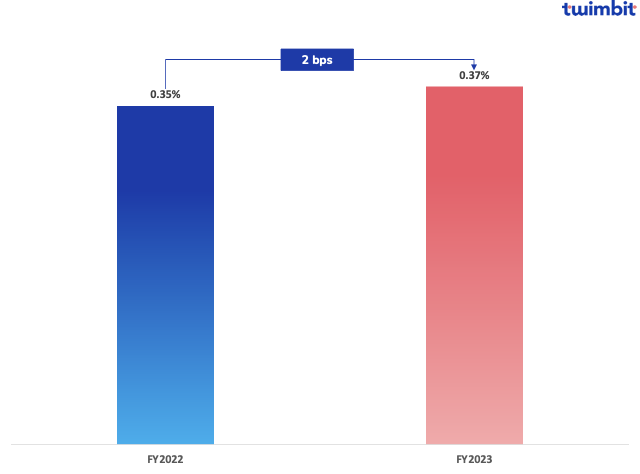

Non-performing loans (NPL)

Top 6 banks in Australia recorded an average NPL of 0.37% in FY 2023

Consolidated NPL increased by 2 bps in FY 2023 from FY 2022 (Exhibit 5), resulting in a current NPL of 0.37%. AVerage NPL grew by 4.29% between FY 2022 and FY 2023.

- BOQ declined by 5 bps from O.19 to 0.14%

- Bendigo declined by 3 bps from 0.17% to 0.14%

- CBA declined by 3 bps from 0.36% to 0.33%

- ANZ increased by 4 bps from 0.36% to 0.40%

- Westpac increased by 10 bps from 0.51% to 0.61%

- NAB increased by 6 bps from 0.51% to 0.57%

NPL in Australia has inherently low NPL because of the:

- Sound lending policies

- Diversified loan portfolios

- Superior underwriting

- Stringent credit checks

Exhibit 11: Consolidated NPL of the top 6 banks in Australia

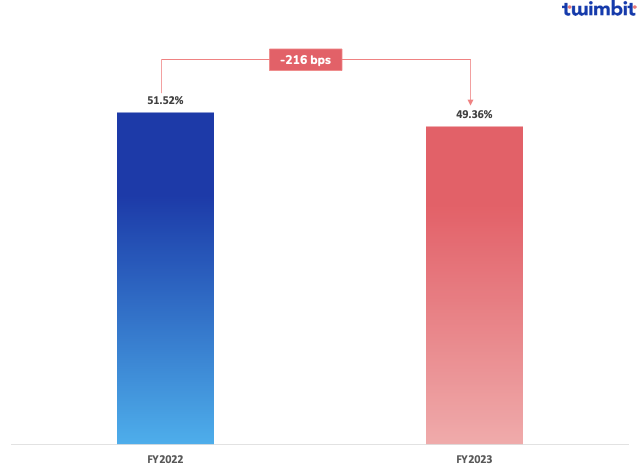

Cost efficiency (CE)

Consolidated CE improved by 4.19% between FY 2022 and FY 2023. The average cost efficiency of Australian banks improved from 51.52% in FY 2022 to 49.36% in FY 2023 (Exhibit 6).

Bendigo and BOQ had their cost efficiencies at 59.10% and 55.70%, respectively, in FY 2022. All the Big Four banks had their cost efficiency below the threshold value of 50%. It was a similar case in FY 2023.

CBA leads with a cost efficiency of 43.54%, closely followed by NAB at 43.69%.

The improvements in the cost efficiency of Australian banks are due to a controlled growth in operating expenses, which grew by an average of 4.64%. This was shrouded by the 10.86% growth in the average net revenues of the banks.

BOQ is the only bank that reported a decline in cost efficiency from 55.70% to 58%. A potential reason for this decline is a 7.79% increase in operating expenses, more than the 5.07% increase in the bank’s net revenues.

Exhibit 12: Consolidated CE of the top 6 banks in Australia

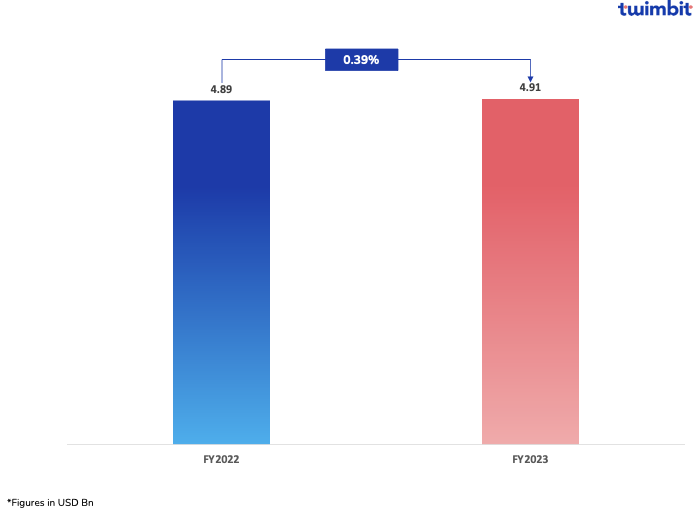

ICT spend

ICT spending for Australian banks increased by 0.39%, from USD 4.89 billion to USD 4.91 billion (Exhibit 7).

The average ICT spend to revenue decreased from 8.62% to 7.8%.

The overall average ICT spending increased to USD 818 million in FY 2023 compared to USD 815 million in FY 2022.

Westpac

- Inflation contributed to higher third-party vendor costs, increasing software maintenance and license costs.

- Higher software amortisation related to growth, productivity and regulatory and risk investments.

ANZ

- Increased expenses were driven by incremental costs associated with strategic initiatives, higher software license costs, inflationary impacts on vendor costs, and costs previously attributed to discontinued operations.

BOQ

- Increased expenses were driven by investment in the bank’s digital transformation and risk mitigation programs led by higher usage volume and investment in cyber risk mitigation.

CBA

CBA reported a decline in ICT spending at 13.69%, from USD 1.58 billion to USD 1.36 billion.

- Lower amortisation and write-offs of software assets were reduced by 48.09% from USD 509 million to USD 264 million.

- 7.88% increase in the system development and support cost from USD 662 million to USD 714 million partially offset its decline in ICT spending.

Exhibit 13: Consolidated ICT spend of the top 6 banks in Australia

BOQ’s investment in a new cloud-based system is evident by the increase in ICT spending by 20.65% YoY, the highest among the top six banks. ICT spending increased from USD 123 million in FY 2022 to USD 149 million in FY 2023. The bank’s ICT to revenue spending has also increased from 11.10% to 12.74%.

Loan-to-deposit ratio (LDR)

LDR for Australian banks decreased by 82 bps, from 108.37% to 107.54% (Exhibit 8).

Australian banks have historically high LDR as loans comprise most of their business. In recent years, low interest rates have led to a borrowing surge in debt and low deposit rates, which has reduced customers’ incentive to save and increased LDR.

High LDR for Australian banks puts them under pressure to maintain sufficient reserves that cover unexpected contingencies and cash runouts.

Exhibit 14: Consolidated ICT spend of the top 6 banks in Australia

Growth opportunities for Australian banks

- Cybersecurity risks associated with technological enhancements

In December 2023, Westpac was hit with a significant outage, causing its online banking system to crash for at least 8 hours. Customers had to leave their purchases at supermarkets or restaurants because of their inability to make contactless payments.

Banks should aim to strengthen their risk management systems to avoid these disruptions.

- Conduct comprehensive evaluations of third-party service providers, assessing their cybersecurity measures, policies, procedures, infrastructure, and incident response capabilities.

- Implement a vendor risk management program to assess, monitor, and manage cybersecurity risks related to third-party services.

- Regularly monitor third-party service providers’ security controls and practices, utilising network, system, and data handling tools.

- Collaborate with third-party providers to establish incident response protocols, roles, and communication channels. Conduct drills to test response effectiveness.

- Enforce data protection and privacy standards with third-party providers, defining handling requirements, encryption standards, access controls, and breach notification procedures in contracts.

- Combatting financial scams to safeguard customers

Financial scams in Australian banks have led to a surge in consumer complaints.

- Complaints Surge – Australia’s dispute resolution scheme for financial services reports a substantial increase in bank scam-related complaints, creating an unsustainable burden on the system.

- Diverse Scam Tactics – These scams range from offering customers fixed-term deposits with impressive rates to glossy brochures and professional follow-ups. Remote-access scams using chat are also on the rise, posing a threat to individuals and businesses.

To counteract this situation, Australian banks are introducing an industry-first Scam-Safe Accord. This pioneering initiative is led by the Australian Banking Association (ABA) and the Community-Owned Banking Association (COBA).

6 key measures in the Scam-Safe Accord:

- Industry-wide confirmation of payee solution

- Biometric checks

- Warnings and payment delays to alert customers of potential scam payments

- Major intelligence-sharing expansion across the sector

- Limiting payments to high-risk channels

- Implementing an Anti-Scams Strategy

In the initial stage, a significant USD 67 million (AUD 100 million) investment is dedicated to developing a state-of-the-art Confirmation of Payee system.

- Branch transformation

The Australian Prudential Regulation Authority (APRA) confirmed a notable disappearance of bank branches in the past year.

Leading up to June 2023, APRA revealed that 424 bank branches (11% of Australia’s total branches) have ceased operations. Of the 424 branches, 122 were located in regional and remote areas. This exacerbated the challenge communities faced regarding access to banking.

Additional data by APRA underscores a concerning decline in available public ATMs. Since 2017, Australia has experienced a staggering 60% decrease in operational ATMs, leaving fewer than 6,000. In the past year, there was an 11% reduction in ATMs, resulting in more than 700 cash machines being removed. This ongoing trend has led to a 34% decline in branch numbers in regional and remote areas and a 37% decline overall since the end of June 2017.

The reasoning behind this closure is a growing trend among customers who prefer conducting their banking activities online or via mobile, with a minimal percentage opting for in-person banking services. However, these banks only considered interactions involving transactions in their reasoning. Visits to branches for advice or other assistance were excluded from the assessment.

Outlook for Australian Banks in 2024

Australian banks expect to face ongoing challenges: persistent competition for mortgage loans, escalating funding costs that pressure banks’ NIMs, slowing loan growth and a rise in impairment charges.

With their balance sheets heavily tilted towards loans, the banks also face challenges sustaining net interest income, which remains their primary revenue source. The compression of NIMs is poised to complicate revenue growth in FY 2024.

In response, the major Australian banks have continued investments in simplifying customer journeys, digital banking channels, touchpoints, and app enhancements. These initiatives help banks adapt to the evolving industry landscape and meet modern customer expectations.

AI is another key strategic consideration, such as ANZ’s new AI-driven capability in fraud detection. NAB is using AI in the automation and digitisation of its business, contributing to USD 266 million in productivity benefits. Meanwhile, CBA is using an AI-powered Customer Engagement Engine to deliver personalised and relevant experiences like Bill Sense and Benefits Finder to its customers digitally. With mass-scale AI adoption in employee productivity, conversational AI and customer engagement in Southeast Asian banks, this indicates immense potential for Australian banks.

On the other hand, since a major contribution to the revenue comes from the mortgage business, the focus on automation is currently skewed towards home loan automation. Therefore, banks should embrace automation in other business divisions to streamline the processes and deliver an enhanced customer experience.

To know how the Australian Banks have fared from 2023, click here.