Key highlights

Growth opportunities in South Korean banking in digital currency and AI innovations

- Digital currency & stablecoin offerings- Legislation and private-sector pilots set to drive won-based stablecoins by 2026, opening new transaction and wallet opportunities.

- AI-powered anti-vishing platforms- Banks can boost fraud prevention via real-time scam pattern analysis and account-freezing automation.

- FX lending expansion- Government’s USD 247.74 billion export finance initiative enables banks to scale cross-border FX lending and structured trade finance.

Key trends and innovations

- Shinhan Bank partnered with DeepBrain AI to deploy GenAI bank tellers, providing real-time, lifelike interactions and 24/7 customer service via digital desks and kiosks.

- The Super SOL App unified services across five Shinhan Group affiliates with loan comparison tools and gamified engagement features, enhancing user retention and cross-service convenience.

- Industrial Bank of Korea (IBK) introduced Loan Pathway Box, blending online loan applications with same-day offline approvals for SMEs, significantly shortening the traditional loan process.

Financial performance

Net revenue

- Net revenue increased by 5.25% YoY to USD 20.6 billion in FY 2024.

- Woori Financial Group recorded the largest growth at 21.61%, while Hana Bank saw a slight decline of 1.41%.

Profitability

- Overall net profit rose by 2.63% YoY, reaching USD 11.73 billion in FY 2024.

- Woori Financial Group reported the highest net profit growth at 20.73%, driven by gains on financial instruments and dividend income.

- Hana Bank posted the largest decline in net profit at 5.01%, due to higher non-operating expenses and reduced operating income.

Fee-based income

- Woori Financial Group led with a 21.26% YoY increase in net fee income, rising from USD 1.2 billion to USD 1.46 billion.

- This was driven by a 12.02% rise in fee income and a 6.78% decline in fee expenses.

Net interest margin (NIM)

- The average NIM of South Korean banks declined by 5 bps to 1.64% in FY 2024.

- Woori Bank experienced the largest drop, by 12 bps to 1.44%, while Hana Bank was the only bank to see an increase, of 6 bps to 1.69%.

Non-performing loans (NPL)

- Average NPL ratio increased by 15 bps to 0.78% in FY 2024, still among the lowest in APAC.

- Woori Bank’s NPL rose by 20 bps to 0.57%, reflecting higher credit stress among SMEs and retail borrowers.

- Industrial Bank of Korea recorded the highest NPL at 1.34%, up 29 bps from 2023.

Cost efficiency:

- The average cost-to-income ratio increased by 120 bps to 41.06% in 2024.

- Woori Financial Group improved its cost efficiency with a 70 bps decrease to 42.8%, while Industrial Bank of Korea saw the largest increase of 340 bps to 35.1% due to rising service and labor expenses.

Growth Opportunities for South Korean Banks

- Digital currency and stablecoin offerings: The increasing focus on won-based stablecoins, driven by proposed legislation and private-sector pilots for launch by 2026. These developments open the door for banks to issue and manage regulated digital-won instruments. This would allow them to capture transaction flows that currently move offshore via dollar-backed coins. Even without a central bank digital currency (CBDC) rollout in FY25, commercial banks can collaborate on consortium platforms to offer digital wallets, tokenized deposits, and real-time corporate treasury solutions.

- Leverage AI-driven Anti-Vishing Platform: South Korean banks can enhance fraud prevention capabilities by integrating with the upcoming AI-based anti-vishing platform. This enables access to real-time data and AI-analyzed patterns of scams. This enables faster account freezing, proactive risk mitigation, and improved customer trust, thereby positioning banks as secure and tech-forward institutions.

- FX lending expansion: The South Korean government’s planned allocation of USD 247.74 billion in export financing through state-run banks in 2025 presents a strategic growth opportunity for commercial banks. Designed to counter rising U.S. tariff pressures, this policy initiative enables banks to scale their involvement in structured trade finance and FX-linked lending. In parallel, regulatory easing around corporate foreign borrowing expands access to offshore funding, allowing banks to originate FX-denominated loans and deliver tailored risk-hedging solutions. These developments position banks to strengthen their role in cross-border financing and deepen corporate client engagement.

Key trends and innovation

Shinhan Bank

GenAI bank tellers

DeepBrain AI’s innovative GenAI bank tellers transform customer service at Shinhan Bank, combining human touch with AI efficiency.

- GenAI bank tellers, based on Shinhan Bank employees, provide real-time speech and video interaction through digital desks and kiosks.

- The system uses AI-driven personalization to facilitate customer interactions and address inquiries or problems.

- The tellers operate continuously, which helps reduce customer wait times and contributes to lower operational expenses.

Super SOL App

Super SOL consolidates banking, credit card, securities, insurance, and savings bank services from five Shinhan Group affiliates into a unified, all-in-one finance app.

- The home screen provides access to key features such as fund transfers, card payments, and stock trading.

- The loan comparison feature allows users to compare and apply for loan products across Shinhan Bank, Shinhan Card, and Shinhan Savings Bank with a single data entry.

- The app includes interactive tasks such as balance checks, activity tracking, and point accumulation. These contribute to the “My Shinhan Point” system, which can be exchanged for financial or service-related benefits.

Super SOL reflects Shinhan Group’s approach to integrating financial services within a unified platform, with a focus on centralized access and user interaction mechanisms.

KB Kookmin Bank

KB Kookmin Bank’s implementation of AI‑OCR and text analytics

The Financial Services Commission has approved the commercialization of KB Kookmin Bank’s proprietary AI engines KB AI‑OCR and KB‑STA for group-wide deployment.

- KB AI OCR, a Hangul OCR system using deep learning, is applied across 20 internal service areas, including credit, pensions, and foreign exchange. It is also used for account photo transfers in the KB Star Banking app.

- KB STA processes unstructured text and financial terminology to support functions such as interest rate forecasting, business data analysis, and chatbot inquiry categorization.

These AI systems have reduced processing times by over 50% and increased human resource efficiency by 240%, impacting service speed and operational volume.

Stock AI

KB Securities has integrated Stock AI, an AI-based chat service, into its M able Mini mobile trading platform, becoming the first Korean securities firm to do so.

- Stock AI uses natural language processing to analyze market data and portfolio characteristics. It delivers investment-related information based on this analysis.

This integration is part of KB Securities’ ongoing digital initiatives and reflects broader developments in Korea’s brokerage industry.

Woori Financial Group

WooriGPT

In December 2024, Woori Bank launched WooriGPT, an in-house generative AI system developed to support corporate banking processes.

- The system integrates a large language model with retrieval-augmented generation (RAG) and has been trained on over 10 million data points. It is used across corporate banking functions.

- The “knowledge consultation” function queries internal and external sources to reduce time spent on corporate report preparation.

- During customer interactions, WooriGPT references historical cases in real time to assist staff in responding based on past data.

Generative AI service “W-Sketch”

Woori Bank deployed W‑Sketch, its in-house generative‑AI 3D image production model

- W Sketch converts text prompts into 3D graphics, icons, and illustrations. It was trained on over 4,000 reference images and is currently used to generate visual materials in Woori WON Banking’s non-face-to-face channels.

- By automating complex design tasks (marketing banners, interactive 3D objects) and centralizing asset delivery across departments, W‑Sketch increases workflow efficiency.

Industrial Bank of Korea

IBK Loan Pathway Box

- IBK Industrial Bank launched Loan Pathway Box, an O2O service that combines online loan applications with offline branch consultations.

- Through the Loan Pathway Box, corporate customers can enter application data and upload documents online, they complete the process with a single visit to a branch, replacing the previous multi-visit procedure.

- The system includes non-face-to-face screening, enabling individual businesses to access credit loans of up to ₩100 million on the same day, without a prior relationship with IBK.

i-ONE Bank

i-ONE Bank has introduced a One-Click Document Submission and Verification Service.

- Through a single consent action in the i-ONE app, customers can transmit required documents to administrative agencies.

- The process integrates e-signature and automated verification within the mobile platform, removing the need for in-branch submission.

- By combining document submission and verification into one step, the service consolidates administrative workflows and reduces processing time for both the institution and the user.

Financial performance

Net revenue

Exhibit 1: Net revenue of South Korean banks in FY 2024

Source: Bank Financials, Twimbit analysis

Net revenue increased by 5.25% YoY, reaching USD 20.6 billion in FY 2024, up from USD 19.58 billion in FY 2023.

Woori Financial Group

- Woori Financial Group recorded the largest YoY increase in net revenue, with an increase of 21.61% in 2024.

- Net revenue increased from USD 2.45 billion in 2023 to USD 2.98 billion in 2024 due to the following reasons:

- Fee and commission income increased by 12.02% increasing from USD 1.8 billion in 2023 to USD 2.01 billion in 2024.

- Fee and commission expenses declined by 6.78%, from USD 591.7 million to USD 551.6 million.

- Dividend income increased by 29.14% from USD 168.2 million in 2023 to USD 217.2 million in 2024.

Hana Bank

- Hana Bank recorded the largest YoY drop in net revenue, with a decrease of 1.41% in 2024.

- Net revenue decreased from USD 3.14 billion in 2023 to USD 3.09 billion in 2024 due to the following reasons:

- Net interest income declined by 1.98% from USD 5.2 billion in 2023 to USD 5.1 billion in 2024. This decrease was primarily driven by a drop in market interest rates. Additionally, increased competition in the asset market led to a decline in loan interest rates, further contributing to the overall reduction in net interest income.

- Fee and commission expenses grew by 3.97%, from USD 172.7 million to USD 179.5 million.

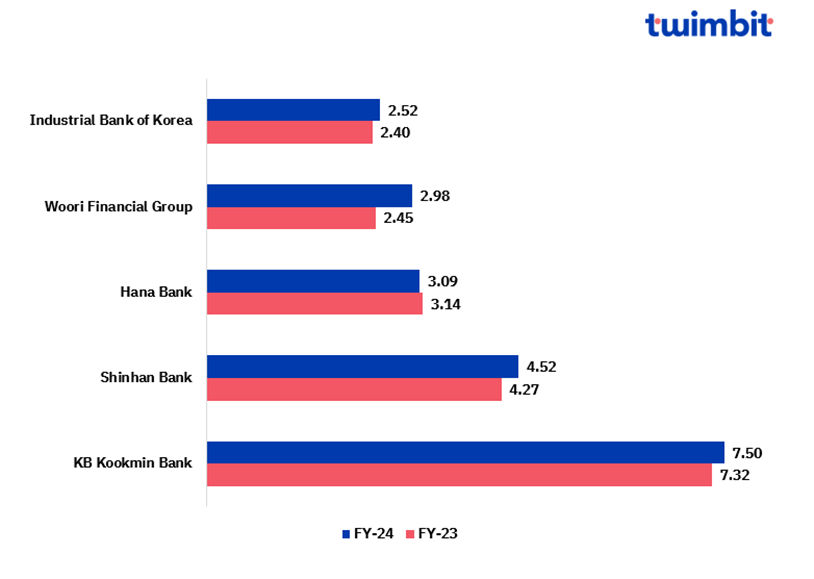

Profitability

Exhibit 2: Net Profit of South Korean banks in FY 2024

Source: Bank Financials, Twimbit analysis

Net profit increased by 2.63% YoY, reaching USD 11.73 billion in FY 2024, up from USD 11.43 billion in FY 2023.

Woori Financial Group

- Woori Financial Group recorded the largest YoY increase in net profit, with an increase of 20.73% in 2024.

- Net profit increased from USD 1.84 billion in 2023 to USD 2.22 billion in 2024 due to the following reasons:

- Dividend income increased by 29.14% from USD 168.2 million in 2023 to USD 217.2 million in 2024.

- Net gain(loss) on financial instruments at FVTPL increased by 205.59% from USD 342 million in 2023 to USD 1045 million in 2024.

Hana Bank

- Hana Bank recorded the largest YoY drop in net profit, with a decrease of 5.01% in 2024.

- Net profit decreased from USD 2.3 billion in 2023 to USD 2.19 billion in 2024 due to the following reasons:

- Non-operating expenses increased by 100.33% from USD 132.6 million in 2023 to USD 265.6 million in 2024.

- Other operating income declined by 5.05%, from USD 5.5 billion in 2023 to USD 5.2 billion in 2024.

Fee-based income

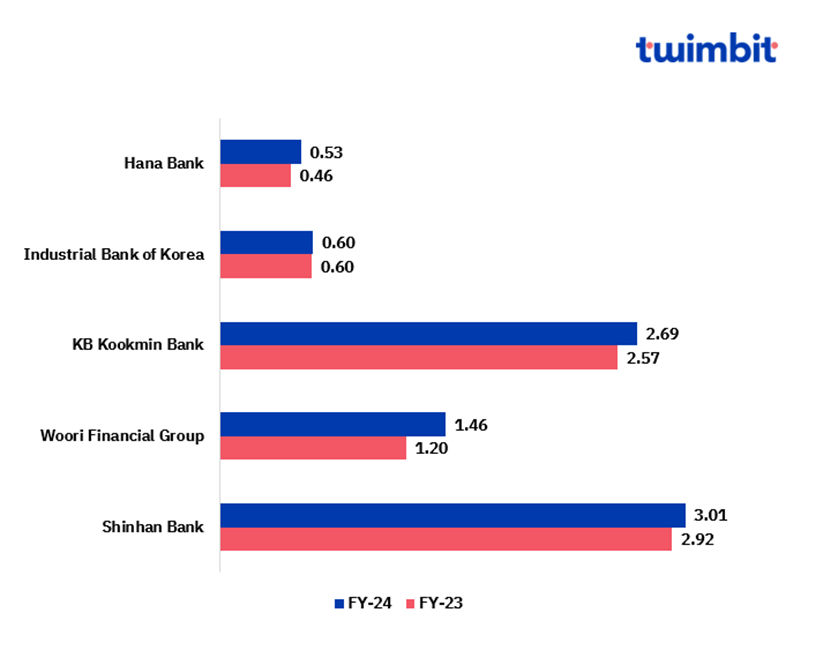

Exhibit 3: Fee incomes of the top banks in South Korea

Source: Bank Financials, Twimbit analysis

Woori Financial Group

- Woori Financial Group recorded the largest YoY increase in fee income, with an increase of 21.26% in 2024.

- Net fee income increased from USD 1.2 billion in 2023 to USD 1.46 billion in 2024 due to the following reasons:

- Fee and commission income increased by 12.02% increasing from USD 1.8 billion in 2023 to USD 2.01 billion in 2024.

- Fee and commission expense decreased by 6.78% decreasing from USD 591.7 million in 2023 to USD 551.6 million in 2024.

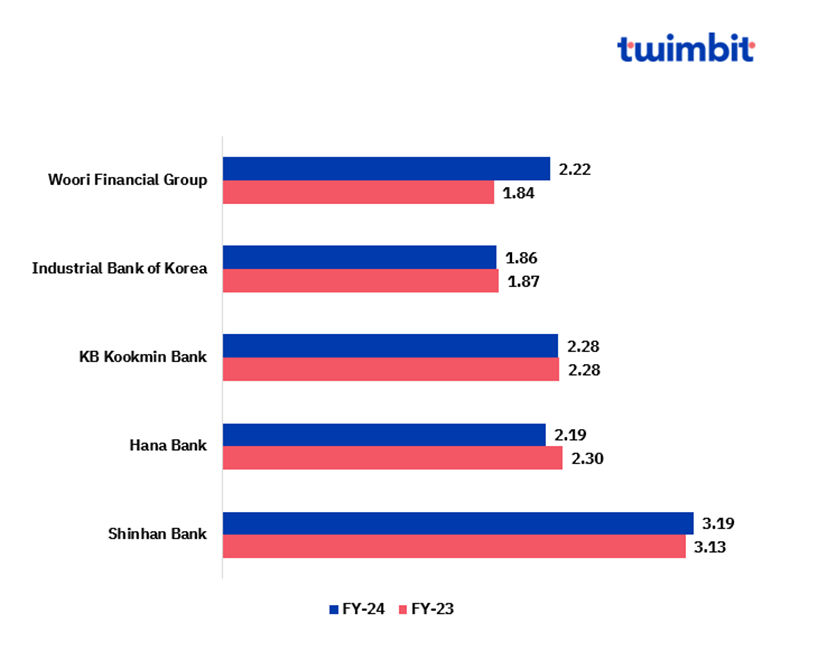

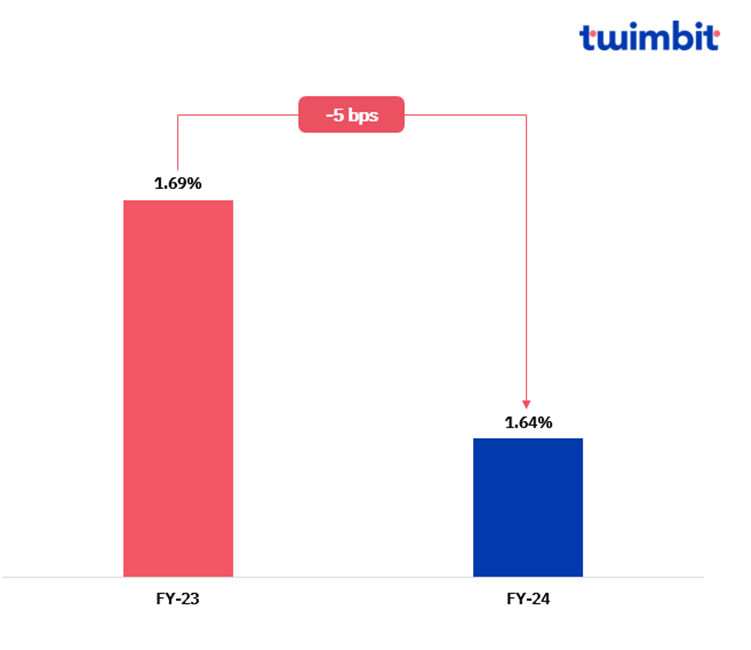

Net interest margin (NIM)

Exhibit 4: Net interest margins of the top banks in South Korea

NIM decreased by 5 basis points, dropping to 1.64% in 2024, down from 1.69% in 2023.

- Shinhan Bank reported a 4-bps decline in its NIM, which now stands at 1.58%.

- KB Kookmin Bank NIM dropped by 5 bps, now reaching 1.78%.

- Hana Bank reported a 6 bps increase in its NIM, which now stands at 1.69%.

- Woori Financial Bank reported a 12-bps decrease in its NIM, currently standing at 1.44%

- Industrial Bank of Korea reported a 9-bps decline in its NIM, which now stands at 1.7%.

Overall, banks in South Korea have experienced a decline in their Net Interest Margin (NIM), primarily driven by rising competition from digital challengers such as KakaoBank, KBank, and Toss Bank. These digital banks initially offered elevated deposit rates to rapidly build market share. In response, traditional banks were compelled to match these higher rates on term and savings products, increasing their overall funding costs. However, this rise in costs was not accompanied by a corresponding increase in loan yields, thereby putting downward pressure on NIMs across the sector.

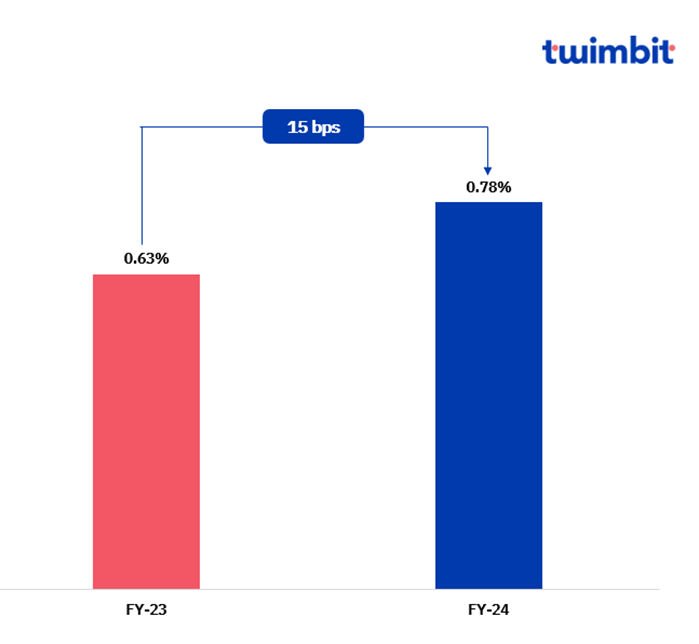

Non-performing loans (NPL)

South Korean banks demonstrate strong asset quality, maintaining the lowest non-performing loan (NPL) ratios in the APAC region, reflecting their strong risk management practices and resilient credit portfolios.

Exhibit 5: Average NPL of the top banks in South Korea

NPL increased by 15 bps, increasing from 0.63% in 2023 to 0.78% in 2023.

- Shinhan Bank reported a 15-bps increase in its NPL, which now stands at 0.71%.

- KB Kookmin Bank NPL increased by 8 bps, now reaching 0.65%.

- Hana Bank reported no change in its NPL, which now stands at 0.62%.

- Industrial Bank of Korea reported a 29-bps increase in its NPL, which now stands at 1.34%.

Woori Financial Group

Woori Financial Bank recorded a 20-bps increase in its non-performing loan (NPL) ratio, rising from 0.37% in 2023 to 0.57% in 2024. The uptick reflects growing credit stress, particularly among small and medium-sized enterprises (SMEs) and retail borrowers, amid a cooling economic environment and persistently high household debt service burdens.

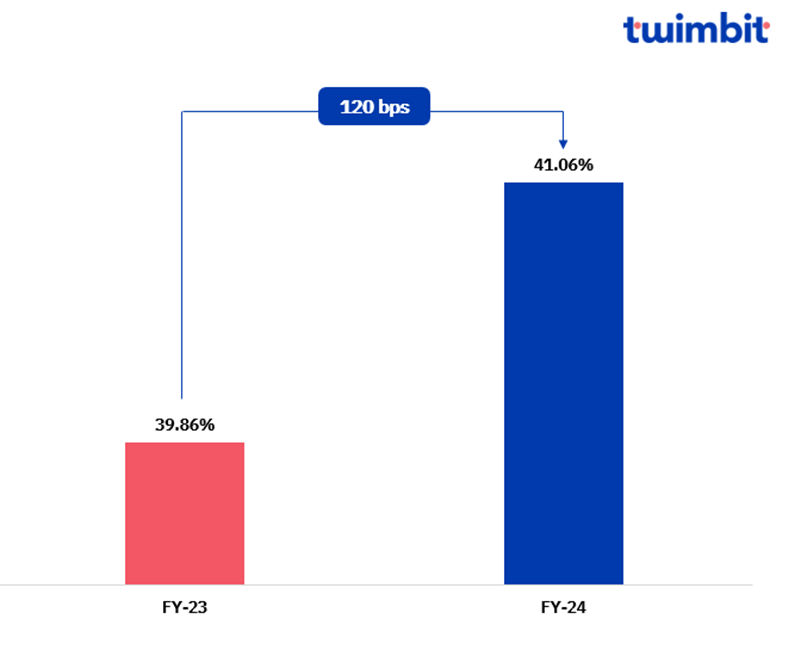

Cost efficiency (CE)

Exhibit 6: Average cost-efficiency ratio of the top banks in South Korea

The average cost-efficiency ratio for the top banks in South Korea increased by 120 bps, rising from 39.86% in 2023 to 41.06% in 2024.

Industrial Bank of Korea

- Woori Financial Group recorded an increase in its cost-to-income ratio, with a rise of 340 bps in 2024.

- Cost-to-income ratio increased from 31.7% in 2023 to 35.1% in 2024 due to the following reasons:

- Service fees increased by 15.64% increasing from USD 72.5 million in 2023 to USD 83.8 million in 2024.

- Advertising and marketing expenses increased by 5.87% increasing from USD 46.4 million in 2023 to USD 49.2 million in 2024.

- Labor expenses increased by 5.25% increasing from USD 1.1 billion in 2023 to USD 1.2 billion in 2024.

Woori Financial Group

- Woori Financial Group recorded a decrease in its cost-to-income ratio, with a decline of 70 bps in 2024.

- Cost-to-income ratio improved from 43.5% in 2023 to 42.8% in 2024 due to the following reasons:

- Rent expenses decreased by 0.25% decreasing from USD 87.1 million in 2023 to USD 86.8 million in 2024.

- Advertising expenses decreased by 3.15% decreasing from USD 113.3 million in 2023 to USD 109.7 million in 2024.

- Printing expenses decreased by 1.93% decreasing from USD 4.3 million in 2023 to USD 4.2 million in 2024.