Market highlights

In 2023, the real GDP growth of Thailand was estimated at 2.5%, the lowest in Southeast Asia.

- The Bank of Thailand paused its tightening cycle after raising interest rates for over a year. Inflation turned adverse to -0.3% YoY in October 2023.

- Inflation was at -0.83% in December 2023, the highest in 34 months.

- The current policy rate in Thailand stands at 2.5% after 8 rate hikes, the highest since 2013.

- SCB, in partnership with KakaoBank, is establishing a virtual bank in Thailand aiming to replicate KakaoBank’s success in disrupting Thailand’s retail banking market.

- Kasikorn Bank opened its 5th branch in Beijing to strengthen regional services and tap into China’s economic opportunities.

- Krungthai’s digital innovation arm, Infitas, collaborated with Google to accelerate open innovation and financial inclusion.

- TMB Thanachart is digitising its CYC application journey and motor insurance renewal experience.

- Net revenues for the top 5 banks in Thailand grew by 14.3% YoY from USD 18.9 billion to USD 21.6 billion.

- Net profits for the top 5 banks grew by 22.9% YoY from USD 4.3 billion to USD 5.3 billion.

- Fee income declined by 4.9% YoY from 3.7 billion to USD 3.5 billion.

- Net interest margin increased by 43 basis points to 3.33% in FY 2023.

- Non-performing loans declined by 22 bps to 3.04%.

- Cost efficiency improved by 129 bps to an average of 43.96% in FY 2023.

- The loan portfolio of the top 5 banks declined by 0.38% from USD 346.8 billion in FY 2022 to USD 345.5 billion in FY 2023.

- Deposits declined by 1.07% from USD 344.6 billion in FY 2022 to USD 340.9 billion in FY 2023.

- The government has launched the Thailand Digital Wallet Project.

- Distribute digital money to individuals above 16 with monthly incomes less than USD 2014 (THB 70,000) and less than USD 14,387 (THB 500,000) in bank deposits.

- Transfer USD 288 (THB 10,000) to 50 million people via a mobile app to spend within six months.

- It is expected to cost USD 14.39 billion (THB 500 billion) and be funded through loan borrowings.

Digital measures of success

- SCB

- 15.1 million mobile app users vs 14.2 million in FY-2022

- 3.8 million registered users on the FINNIX app vs 2.8 million in FY-2022

- 3.7 million registered users on the Money Thunder app vs 3 million in FY-2022

- 4.3 million registered users on the Robinhood app vs 3.5 million in FY-2022

- 1 in 3 Thai investors are INVX customers

- Kasikorn Bank

- 21.7 million K PLUS mobile app users vs. 20 million in FY-2022

- 73% of active users, same as FY-2022

- 47.6 billion total transactions vs. 31.75 billion in FY-2022

- 9.7 billion financial transactions

- TMB Thanachart

- 88% digital transactions vs 82% in FY-2022

- 983 million digital financial transactions

- 2.77 million average daily QR code scan transactions

- 18% of accounts opened digitally vs. 9% in FY-2022

Top innovations by Thai banks

- SCB

Partnership with Hashed

- SCB has partnered with Hashed, a leading Web3 firm from Korea.

- Undertake joint R&D initiatives and events for the widespread adoption of decentralised technology on regional and global scales.

- Contribute to the growth of the Web3 ecosystem and extend its influence in Southeast Asia and on an international scale.

- Hashed will lead tests on Web3 technologies through its research hub, ShardLab.

Responsible AI HackFest

- SCBX and Microsoft Thailand introduced the Responsible AI HackFest, a local tech competition for students, developers, and startups focused on AI.

- Promote responsible AI practices and address pressing challenges in Thailand through AI entrepreneurship.

- Identify and support innovative AI developers contributing to new capabilities, especially in Thailand’s financial services sector.

- Winners gain technical and business mentorship opportunities with SCBX and Microsoft Thailand executives. Unlock access to AI technology through Microsoft Founders Hub and gain connections with community partners, prizes, recognition, and more.

SCB and KakaoBank collaboration for a Virtual Bank in Thailand

- Leverage KakaoBank’s expertise in developing virtual banking businesses and enhance SCB’s competitive advantage.

- Form a consortium, where SCB will hold a majority stake, and KakaoBank will have a stake of at least 20%.

- Emphasise the global issue of income inequality and address financial inclusion through upcoming virtual banks.

- Aims to replicate KakaoBank’s success in disrupting Thailand’s retail banking market.

- Identify new strategic partners and strengthen the consortium’s core competitiveness for winning Thailand’s virtual banking license.

- Kasikornbank

Geographic expansion

- Opened its 5th branch in Beijing to strengthen regional services and tap into China’s economic opportunities.

- Serve Chinese retail and business customers, particularly those in the China-AEC value chain, with investment, trade finance, and value chain financing.

- Facilitate trade and investment between Thailand and China, with plans to extend services to other ASEAN countries.

- Prioritise digital technology for service delivery and generate over USD 143 million in income from its China business within three years.

- Continue digital technology development in the AEC+3 region, fostering connectivity between China and AEC+3 to become a regional bank of choice.

Web3 AI projects

- Launched KXVC, a USD 100 million fund dedicated to AI and Web3 projects.

- Targets technology firms expanding in the Asia Pacific (APAC) region, with plans to fund up to 30 global startups across the European Union, the United States, and Israel.

- Specific AI focus areas include consumer-focused AI tools, cybersecurity, and “problem-specific AI startups.”

- In the Web3 domain, the fund will invest in node validators, middlewares, wallets, NFTs, privacy-focused projects, and may consider Layer-1 (L1) or Layer-2 (L2) blockchains, shared securities, and modularity technologies.

- Bangkok Bank

Partnership with AIS 5G

- Bangkok Bank partnered with telecom provider AIS 5G to enhance domestic spending through a co-branded debit card.

- Aims to add 6 million debit card users in the next 5 years and foster customer loyalty for AIS.

- The partnership can help increase the current debit card user base of 9 million by an additional 2 million within the next 12 months.

- The AIS points program now allows customers to access financial services and earn points due to the partnership.

- Users receive one AIS point for every 200 baht spent online using the card and can accumulate up to 100 points per card per month.

- Points can be redeemed for various benefits, such as phone/internet charges, food and beverage discounts on leading brands, and Line stickers.

- Krungthai Bank

Joint venture with IBM

- Formed a joint venture named IBM Digital Talent for Business (IBMDT) to accelerate the technology workforce and infrastructure development.

- Enhance traditional banking businesses and efficiently meet customer needs for sustainable growth.

- Develop IT workforce skills and acquire new tech talent that aligns with Krungthai’s “7 North Star” strategies.

- Modernise IT infrastructure to ensure security, stability, and efficiency that aligns with the bank’s technology-driven plans.

Collaboration with Google

- Through its digital innovation arm, Infitas, the bank collaborated with Google Cloud to accelerate open innovation and financial inclusion for all in Thailand.

- Focuses on building a scalable co-innovation platform and talent ecosystem.

- Utilises Google Cloud’s Apigee for API management and runs applications on Google Cloud’s energy-efficient infrastructure.

- Apigee enables easy integration of new digital offerings into the Pao Tang mobile app.

Retirement app for self-employed

- Introduced an app-based retirement savings service named “AOMPLEARN.”

- The app enables automatic savings through the Pao Tang digital wallet for millions of self-employed Thai freelancers lacking pension plans.

- Savings are transferred to the National Saving Funds (NSF) program upon reaching 50 baht.

- Prioritises Thai citizens aged 15-60 without social security coverage.

- TMB Thanachart

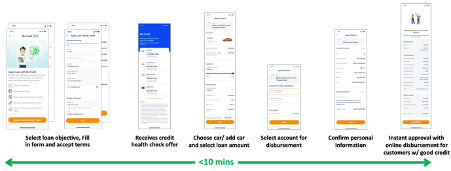

Streamlined CYC application journey – The bank is digitising its offline journey, which took 6 to 7 days, into a much simpler process that now takes less than 10 minutes. The initiative aims for higher conversion and lower abandonment rates.

Exhibit 1: To be CYC application journey

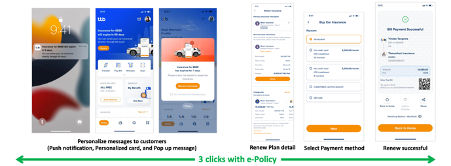

Motor insurance renewal experience – The bank will launch its new digital motor insurance renewal journey, enabling customers to renew their policy in just 3 clicks.

Exhibit 2: To be motor insurance renewal journey

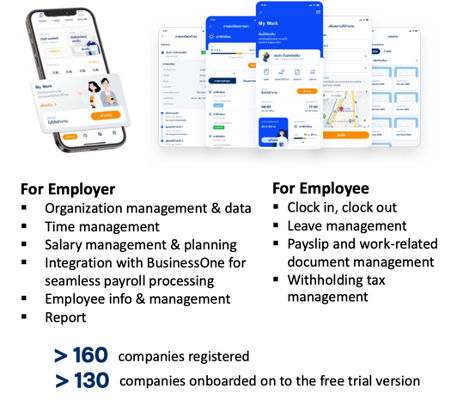

My Work by TTB

Exhibit 3: Financial well-being solutions for employees and companies

Challenges pressuring Thai economic growth

From global economic slowdown and geopolitical conflict to high household debts and strict credit policies, these challenges will affect economic growth in 2024.

Positive factors:

- The increase in foreign tourist numbers contributes to the service sector’s recovery, reducing vulnerabilities within the labour market.

- Anticipated growth in private investment aligns with positive trends in investment approvals by the BOI and export recovery.

Negative factors:

- The anticipated slowdown in the Chinese economy is poised to pressure Thailand’s export market.

- As relief measures for household debt face expiration, there is a heightened risk of rising defaults, impacting overall consumption.

- The agricultural sector faces potential consequences due to a severe drought.

Risk factors:

- China faces increasingly severe economic challenges, evolving into a financial crisis beyond initial expectations.

- Accelerating inflation compels the Federal Reserve to persist in raising interest rates.

- Global geopolitical risks (Russia-Ukraine conflict and US-China economic polarisation) may impact Thai goods’ global supply chain and exports.

- Increasing concerns that the drought may worsen beyond anticipated levels, leading to a significant slowdown.

Despite the challenges, there are opportunities for the Thai economy. These include gradual consumption recovery and government stimulus. Businesses that align with ESG or digitisation trends will benefit from policies that control agricultural exports from competing countries.

Six sectors are expected to see revenue growth in 2024: healthcare, power (renewable), solar PV, restaurants, grocery stores, and F&B. However, the commercial real estate (office), coal, steel (producer), petrochemical, and plastic sectors will decline in 2024.

Thailand digital wallet scheme

Thailand’s government aims to jumpstart the economy with a USD 288 (THB 10,000) digital wallet distribution to 50 million citizens. Delayed from February, the program now targets a launch in May, with recipients having 6 months to spend the funds at specified stores.

While the scheme can potentially lead to a temporary GDP boost of over 5% in 2024, concerns about Thailand’s long-term impact linger. The expensive stimulus balances potential benefits like increased spending against drawbacks, rising fiscal costs and fiscal space reduction. Striking this trade-off is crucial to addressing future uncertainties and securing financial stability.

Scenario 1: Secured funding to allocate the budget resources of FY 2024 and reimburse prior disbursements

The reimbursement will require using augmented tax revenue and shifting funds from other budget areas. Scenario 1 forecasts a 5.4% YoY GDP growth fueled by secured funding and strategic budget allocation.

Scenario 2: A long-term approach for full reimbursement

While this increases government spending, it reduces revenue transferred from the agency. The GDP forecast is expected to be 6.4% YoY in this scenario. Without the scheme, the forecasted public debt to GDP is expected to be 71.3% in 2032. However, with the scheme, it is expected to be ~72.5%.

Revenue highlights

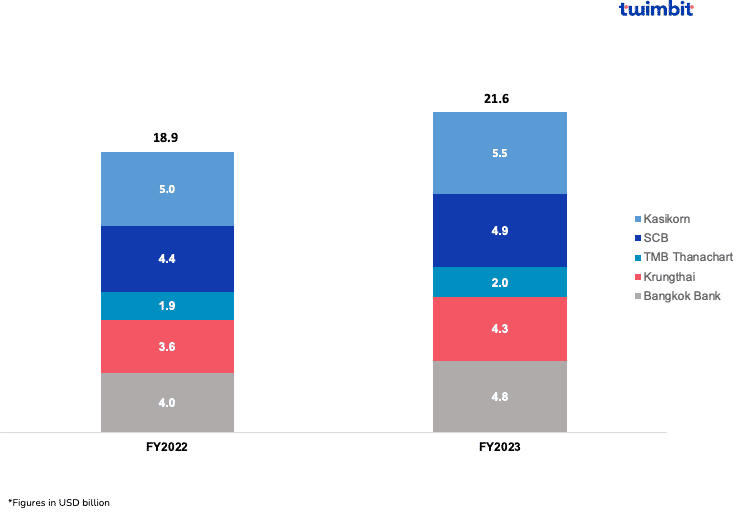

Net revenues for the top 5 banks in Thailand grew by 14.3% YoY

The top 5 banks in Thailand increased from USD 18.9 billion in FY 2022 to USD 21.6 billion in FY 2023 (Exhibit 4). Average net revenues stood at USD 4.3 billion in FY 2023.

- 18.5% increase in the net interest income from USD 14 billion to USD 16.5 billion.

- 1.6% increase in the non-interest income from USD 4.9 billion to USD 5 billion.

- Bangkok Bank

- 20.6% increase in net revenues from USD 4 billion to USD 4.8 billion.

- 1% decline in fee income from USD 791 million to USD 784 million.

- 28% increase in net interest income from USD 2 billion to USD 2.4 billion.

- The growth was driven by rising yields on earning assets and interest rates.

- The growth was partially offset by the growing cost of deposits, which increased in line with the rising deposit interest rates and the resumption of the FIDF fee to the normal rate of 0.46% at the beginning of 2023.

- Krungthai Bank

- 19.2% increase in net revenues from USD 3.6 billion to USD 4.3 billion.

- 25.5% increase in net interest income from USD 2.6 billion to USD 3.3 billion.

- 3% increase in non-interest income from USD 1.01 billion to USD 1.04 billion.

All other banks also reported an increase in their net revenues.

- Kasikorn Bank reported an increase of 11.2% from USD 5 billion to USD 5.5 billion.

- SCB reported an increase of 10.8% from USD 4.4 billion to USD 4.9 billion.

- TMB Thanachart reported an increase of 7.7% from USD 1.9 billion to USD 2 billion.

Exhibit 4: Net revenues of the top 5 Thai banks

The success of the initiatives taken by SCB and Kasikorn Bank in the development of Web3 will enable them to unlock the following opportunities:

- Reduce operational costs with more direct processing, reduce overlapping KYC burdens, and minimise manual reconciliation for significant cost savings.

- Investments in cloud platforms and generative AI empower banks to deliver more personalised and convenient customer experiences.

- Web3 revolutionises data storage by leveraging open-data structures like blockchains. This decentralised approach ensures data integrity, security, and transparency, addressing traditional centralised database challenges.

TMB Thanachart embarks on a digitisation drive to elevate the customer experience by streamlining KYC applications and motor insurance renewals. This strategic move unlocks potential revenue growth through:

- Cost reduction – Streamlining processes through digitisation unlocks cost savings and operational efficiencies.

- Reduce customer abandonment rate – Simplified digital onboarding reduces complexity, streamlines customer engagement and decreases abandonment rates.

- Enhanced customer experience – Improved digital experiences attract and retain customers to engage in additional services, leading to increased cross-selling opportunities and revenue generation.

Profitability

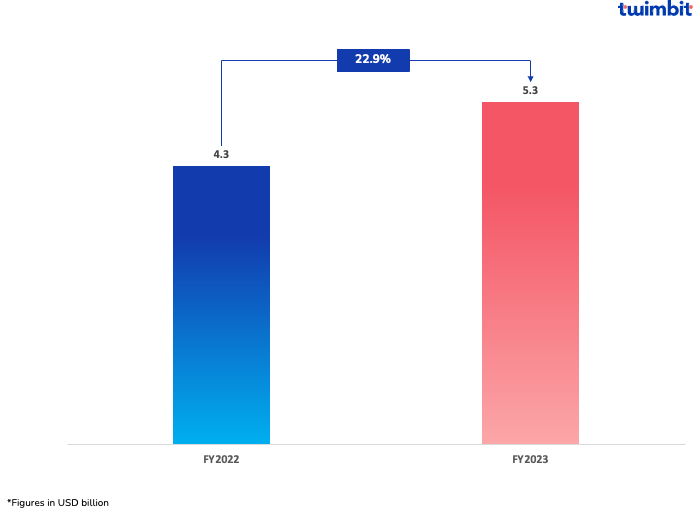

Net profit for the top 5 banks in Thailand grew by 22.9% YoY

Aggregated net profits increased from USD 4.3 billion in FY 2022 to USD 5.3 billion in FY 2023. Average net profits grew by 22.9% (Exhibit 5) from USD 865 million in FY 2022 to USD 1.06 billion in FY 2023.

- Bangkok Bank: 42.1% net profit growth

- TMB Thanachart: 30.1% net profit growth

- Kasikorn Bank: 20.8% net profit growth

- SCB: 17.4% net profit growth

- Krungthai Bank: 11.5% net profit growth

Bangkok Bank reported a 42.1% growth in net profits from USD 843 million in FY 2022 to USD 1.2 billion in FY 2023. 28% YoY net interest income grew from USD 2.9 billion in FY 2022 to USD 3.8 billion in FY 2023.

Exhibit 5: Consolidated net profits of the top 5 Thai banks

The formation of a virtual bank by SCB in collaboration with KakaoBank can help SCB in the following ways:

- Cost-efficient customer acquisition – Virtual banks operate with lower overhead costs than traditional banks. SCB can leverage the low-cost digital infrastructure to attract new customers at lower acquisition costs.

- Innovation and technology adoption – KakaoBank’s innovative tech empowers SCB to develop hyper-personalised products, boosting customer satisfaction.

By leveraging KakaoBank’s technology, SCB faces lower development costs than if built solo. This results in faster revenue growth and greater overall profitability.

Fee-based income

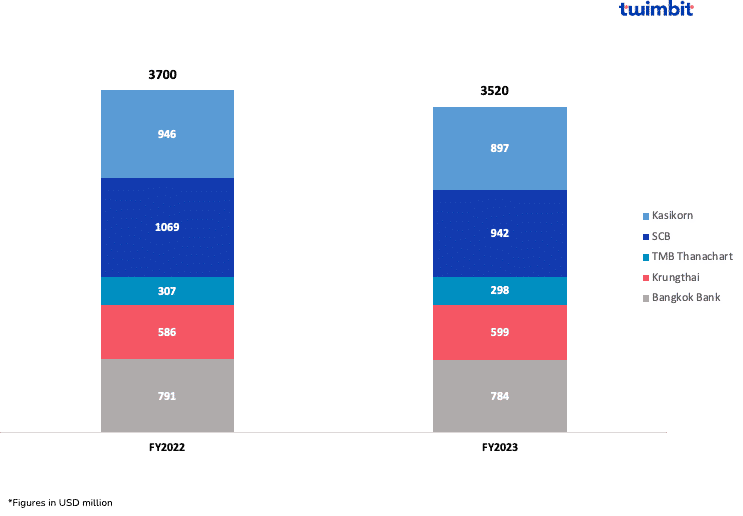

Fee income for the top 5 banks in Thailand declined by 4.9% YoY

Fee income declined from USD 3.7 billion in FY 2022 to USD 3.5 billion in FY 2023 (Exhibit 6). Krungthai Bank stood out among its peers, reporting an increase in fee income at 2.3% from USD 586 million to USD 599 million.

- SCB

- Fee income declined by 11.9% from USD 1.1 billion to USD 942 million.

- Lower bancassurance fees declined by 23.8% from USD 434 million to USD 331 million.

- Wealth management revenue declined by 2.6% from USD 224 million to USD 219 million.

- Lower transactional banking fees declined by 10.2% from USD 394 million to USD 354 million.

All other banks reported declining fee incomes.

- Kasikorn Bank – 11.9% decline from USD 946 million to USD 897 million.

- TMB Thanachart – 3% decline from USD 307 million to USD 298 million.

- Bangkok Bank – 1% decline from USD 791 million to USD 784 million.

The Thailand banks’ fee incomes dip despite the boost in banks’ profit margins from lending activities in a high-interest-rate environment.

Exhibit 6: Fee incomes of the top 5 Thai banks

Bangkok Bank’s partnership with telecom provider AIS 5G can help the bank in the following ways:

- Add 6 million debit card users in the next 5 years by providing customers with financial inclusion and literacy.

- Increase fee income through additional transaction fees, FX, annual, ATM, and card replacement fees.

- Position Bangkok Bank as a technologically advanced and forward-thinking institution to attract a broader customer base and increase market share.

- Open avenues for cross-promotion opportunities between both customer bases to increase usage of the co-branded debit card.

Net interest margins (NIM)

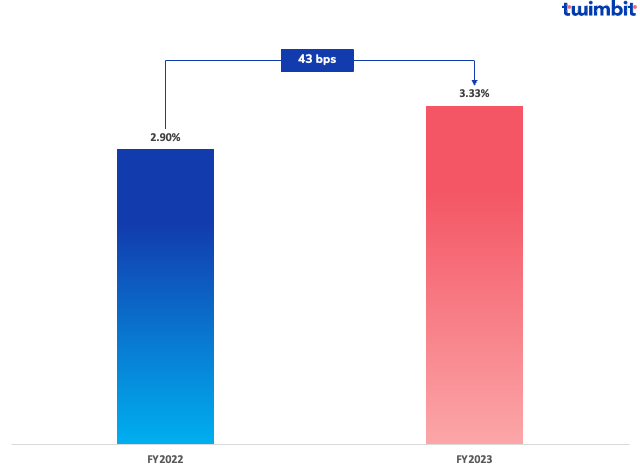

NIM for the top 5 banks in Thailand increased by 43 basis points

The average NIM increased from 2.90% in FY 2022 to 3.33% in FY 2023 (Exhibit 7). All analysed banks reported increasing NIM thanks to optimised portfolios and favourable interest rates despite higher deposit costs.

Exhibit 7: Consolidated net interest margins of the top 5 Thai banks

Non-performing loans (NPL)

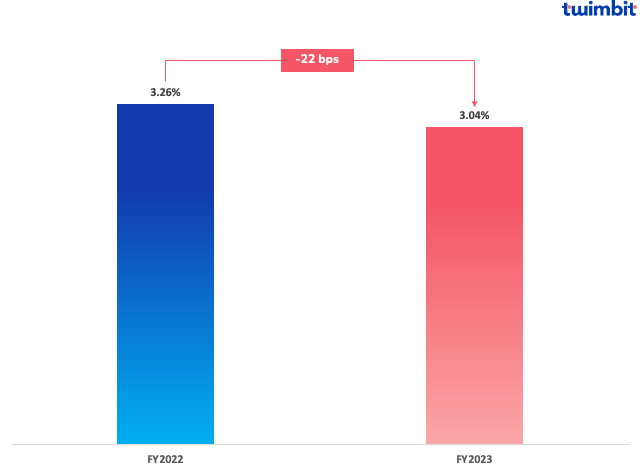

NPL for the top 5 banks in Thailand declined by 22 basis points

The average NPL declined from 3.26% in FY 2022 to 3.04% in FY 2023 (Exhibit 8). All the banks reported a decline in their NPL.

- Bangkok Bank: 12% decline

- Kasikorn Bank: 9.4% decline

- Krungthai Bank: 5.5% decline

- SCB: 4.7% decline

- TMB Thanachart: 1.5% decline

Exhibit 8: Consolidated non-performing loans of the top 5 Thai banks

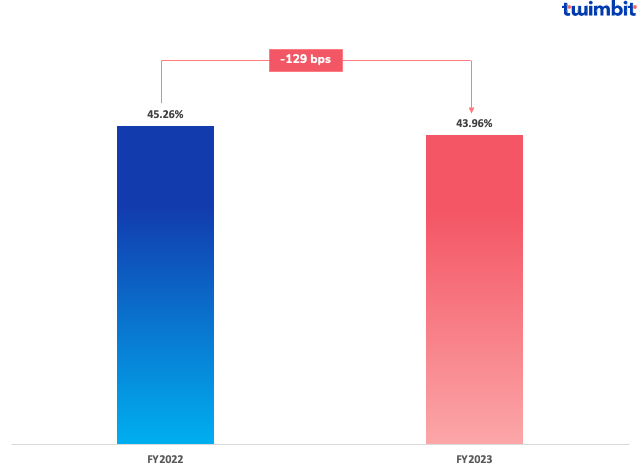

Cost efficiency (CE)

CE for the top 5 banks in Thailand improved by 129 basis points

Cost efficiency stood at 43.96% in FY 2023, slightly improving from the average cost efficiency of 45.26% in FY 2022 (Exhibit 9).

- All the banks have cost efficiencies below the threshold value of 50%.

- Kasikorn Bank reported a decline in cost efficiency by 88 basis points from 43.17% to 44.05%

- SCB reported the highest improvement in cost efficiency by 325 basis points from 45.25% to 42%.

The cost efficiency for the platforms and digital assets at SCB was 128%, attributed to digital technology and platform investments. However, the contribution to the net revenue from the division is minimal at USD 181.3 million, representing 3.7% of the bank’s total net revenues.

Exhibit 9: Consolidated cost efficiency ratio of the top 5 Thai banks

Growth opportunities for Thai banks

- Alternate sources of fee income

Banks in Thailand are witnessing a decline in their fee incomes due to the following factors:

- Portfolio Realignment – The shift towards low-yield assets has led to a noticeable dip in the performance of the top Thai banks. This shift has resulted in increased outstanding mortgages and a transition from SME lending to corporate lending.

- Impact of Digital Transactions – The contraction in fee-based income from fund transfers is primarily due to waived fees on digital banking transactions. As a result, there has been a decrease in overall fee incomes for these banks.

- Regulatory Pressure – The Bank of Thailand has pushed banks to lower their fees, particularly cash transactions.

To boost their fee incomes, banks should look at different revenue sources:

- Advisory-Focused Model – Transitioning from a product-focused model to an advisory-focused one can deepen customer engagement and increase fee-based income. This shift allows banks to excel in consumer finance in the digital age.

- Real-Time Payments (RTPs) – To counter the decline in fee income from money transfers, Thai banks should make faster payments a centrepiece of their retail strategies. RTPs can help them level the playing field with financial technology companies, potentially mitigating the threat of cannibalisation of payment revenues.

- Partner with Fintechs – Banks can collaborate with fintech companies to offer innovative digital services that generate new fee streams, such as personal financial management tools or specialised lending platforms.

- Open banking

The Bank of Thailand (BOT) released the Financial Landscape Consultation Paper, aiming to transform Thailand’s financial sector for a sustainable digital economy. The primary goal is to harness technology and data, enhancing service development to meet consumer needs responsibly. This initiative revolves around three key principles:

- Open Infrastructure – Providing service providers access to financial infrastructure at reasonable costs.

- Open Data – Facilitating better utilisation of data.

- Open Competition – Promoting fair competition between incumbent and new players.

Aligned with these principles, a forthcoming policy initiative centres around Open Data for Consumer Empowerment. This policy establishes a mechanism enabling consumers to securely and conveniently transfer their data from one provider to another. The overarching goal is to empower consumers by allowing them to exercise their rights, ultimately facilitating the application and receipt of enhanced services from any provider.

With open banking, Thai banks can offer the following features:

- Salary on demand – Offered by neobanks like Jupiter in India, customers can withdraw a predefined amount based on their monthly salary and pay it back in full or equal instalments. This provides them with money when they require it the most.

- Data sharing – Gain access to various products and services by sharing their financial data with third-party providers. Save money on loans, mortgages, insurance plans, etc., by comparing them with similar offerings from other service providers.

- Identity verification – Open banking simplifies the account verification and KYC processes. Banks can also verify customers’ identities more efficiently and securely by accessing customers’ financial data. For example, CIMB Bank Philippines leveraged Junio’s AI-powered end-to-end identity verification and authentication solution. This partnership offered CIMB a streamlined, user-friendly, and convenient digital onboarding solution for the Filipino market.

- Open marketplace for financial services – Create an open marketplace where customers can access financial services and products from the bank and third-party providers. DBS marketplace allows consumers to buy or rent property, book flights or hotels, switch their electricity supplier, and buy or sell a car.

- Cost to serve

The top five banks in Thailand reported an 11.3% increase in operating expenses from USD 8.6 billion in FY 2022 to USD 9.6 billion in FY 2023.

- Bangkok Bank: 18.5% increase

- Kasikorn Bank: 13.7% increase

- Krungthai Bank: 13.5% increase

- TMB Thanachart: 4.4% increase

- SCB: 2.7% increase

Bangkok Bank, Kasikorn Banks and Krungthai reported double-digit growth in operating expenses. By managing their expenses efficiently, banks can further boost their profitability through:

- Business Realignment – Improve efficiency by realigning their business, exiting low-margin lines, and focusing on areas with higher profitability.

- Channel Optimization – Optimising digital platforms and branches can enhance efficiency and reduce bank costs.

- Streamline Operations – Simplify products and services to eliminate redundancies and automate processes to enhance efficiency.

- Process Costs Optimisation – Optimising process costs and operational workflows can generate significant savings in operating expenses.

- Staff Productivity Improvement – Training and technology adoption can streamline processes and reduce bank operating expenses.

- Invest in technology – Generate higher efficiency gains, reduce the need for manual interventions and lower bank operating costs.

- Establish a standalone digital bank

The Bank of Thailand has chosen to issue only three virtual bank licenses. This quantity is apt to ensure the stability of the local financial market and safeguard depositors from the risks associated with new ventures.

The bank is finalising the licensing regulations, which will be submitted to the finance ministry for approval. In 2024, the opening of license applications is expected to be followed by the commencement of official business operations in 2025.

The central bank believes 3 operators will adequately foster competition and facilitate effective supervision. While these new virtual banks will not be classified as Domestic Systemically Important Banks (D-SIBs), any risks or problems could impact public confidence and the overall financial system.

Digital-only banks offer several advantages that cater to the modern, tech-savvy consumer. Some of the benefits are:

- Convenience – Digital-only banks allow users to manage their finances anytime, anywhere.

- Enhanced Features – Help banks diversify their offerings and explore new revenue sources for comprehensive digital experiences.

- Cost Savings – Digital-only banks reduce overhead costs, resulting in higher interest rates on savings accounts and lower user fees. Higher deposit rates can help with customer acquisition.

- Security – Digital-only banks prioritise cutting-edge security measures, including encryption and multi-factor authentication, to safeguard customer information and transactions.

- Innovative Solutions – These banks often leverage technology to introduce innovative solutions, such as AI-driven financial insights and personalised recommendations, enhancing the overall customer experience.

Outlook for 2024

Thailand’s economic growth is projected to accelerate to 3.2% in 2024, up from 2.5% in 2023. However, a significant economic challenge – household debt – soared to 90.9% of GDP in Q3 2023, totalling USD 466 billion. This impacted the overall economic recovery. Despite this, private consumption and tourism recovery is anticipated to drive GDP growth in 2024.

On a contrasting note, the government’s digital wallet project is expected to have a short-term and temporary impact on the economy, primarily boosting private consumption. However, concerns from investors led to a decline in the benchmark SET equity index and the Thai Baht after the project’s announcement.

Thailand’s economic growth is poised for improvement in 2024, driven by private consumption and the recovery of the tourism sector, despite the challenges posed by high household debt. However, while providing a temporary boost, the government’s digital wallet project has raised investor concerns, impacting critical financial indicators.

Research methodology and assumptions

- Data collection has been done based on secondary research about the information provided by the respective banks through their investor presentation and quarterly financial statements. Twimbit follows the calendar year approach for the analysis in this report (meaning Q1 is equivalent to the period of January to March of the year).

- For fair representation and analysis, we have considered a constant currency rate for conversion from local currency to USD value. The USD conversion rate is the average calculated value from January to December 2023.

- The report analyses net revenue, net profit and fee income, net interest margin, non-performing loan and cost efficiency for 5 banks.

- The revenue figures for all the banks analysed are net of interest and non-interest expenses.

To learn about the State of Australian Banks in 2024, click here.