Key highlights

Digital trends and innovations

- Krungthai Bank partnered with IBM to launch IBMDT, driving digital transformation via Garage methodology, upskilling talent, and modernizing infrastructure.

- Krungthai introduced a Cloud ERP service for SMEs, integrated with its open banking APIs to streamline operations and boost resilience.

- SCB 10X launched Typhoon-7B, a Thai-language LLM comparable to GPT-3.5, enhancing personalized AI-driven banking.

- SCBX and WeBank formed a virtual banking consortium to expand access to affordable digital financial services under Thailand’s new framework.

- TMBThanachart introduced gamification, tiered loyalty programs, and My Credit widget, boosting customer interaction and lending efficiency.

Financial highlights

- Revenue:

- Net revenue rose 1.73% YoY to USD 16.4 billion.

- Krungthai Bank led the growth of 5%, while TMB Thanachart saw the largest drop of 3.58%.

- Profitability:

- Net profit increased 8.02% YoY to USD 4.5 billion.

- Krungthai Bank’s net profit grew by 16.61% while SCBX saw a slight decline of -0.48%.

- Cost Efficiency:

- CE ratio slightly improved to 44.03%.

- TMB Thanachart Bank showed the most growth in its cost efficiency whereas Krungthai’s CE worsened due to rising costs.

- Fee-Based Income:

- Fee income dipped 0.55% YoY to USD 3.7 billion.

- Krungthai Bank showed growth of 6.33% while TMB Thanachart fell 8%.

- Net Interest Margin (NIM):

- NIM rose 5 bps to 3.35%.

- SCBX improved its net interest margin by 10 bps.

- Non-Performing Loans (NPL):

- NPL ratio declined to 2.91%, down by 5 bps.

- Krungthai saw a 9 bps improvement.

Technology trends in Thailand

Krungthai Bank

- Establishment of IBM digital talent for business (IBMDT)

Krungthai Bank is improving its digital capabilities by investing in its employees and technology. The partnership with IBM, through the company IBM Digital Talent for Business, aims to make the bank’s operations more efficient.

- The IBMDT partnership aims to modernize Krungthai Bank’s operations by enhancing IT skills, infrastructure, and AI integration, driving digital transformation to improve customer and partner services.

- The partnership represents a strategic initiative to increase Krungthai Bank’s position within the digital banking landscape. By leveraging IBM’s technical proficiency and facilitating infrastructure modernization, coupled with the implementation of agile development practices via the IBM Garage methodology, the venture aims to accelerate the bank’s digital transformation and enhance its market position.

The focus on enhancing IT skills and modernizing infrastructure will likely yield operational efficiencies, reduce costs, and improve service delivery. Moreover, the integration of AI and advanced analytics can transform customer experiences, enabling personalized banking solutions and predictive insights.

- Cloud ERP integration

Krungthai Bank is expanding its digital offerings with a Cloud ERP solution designed to help businesses, particularly SMEs, streamline their operations.

- The Cloud ERP solution, seamlessly integrated with Krungthai BUSINESS through open banking API technology, aims to optimize business operations by enhancing real-time connectivity and automation.

- This service empowers SMEs to manage their operations more efficiently, providing advanced digital tools for improved oversight and operational agility.

This initiative benefits the bank by enhancing customer engagement, boosting adoption of financial services, and enabling data-driven insights for personalized offerings, thereby strengthening its digital transformation and competitive edge.

- Krungthai and MINT entered into a cross-currency swap deal linked to decarbonization plan

The bank is committing to sustainable finance by providing innovative solutions that align with environmental goals while managing financial risks.

- Krungthai Bank and Minor International Pcl (MINT) entered into a cross-currency swap agreement aimed at supporting MINT’s decarbonization initiatives.

- The agreement leverages advanced financial technology to manage foreign exchange and interest rate risks associated with MINT’s investment in NH Group.

This initiative strengthens Krungthai Bank’s role in driving sustainable growth, offering tailored financial solutions that balance environmental objectives with the complexities of global financial exposures.

- Digital letter of credit

Krungthai Bank is tapping into trade finance through solutions that modernize cross-border transactions.

- Krungthai Bank has partnered with Contour’s global trade finance network to launch a fully digital, end-to-end letter of credit service.

- The solution utilizes secure blockchain technology to streamline trade processes, reduce transaction costs, and improve efficiency for Thai businesses.

By leveraging blockchain’s inherent transparency and security features, the bank not only reduces transactional risks but also fosters trust among global trading partners. This could lead to faster transaction times, lower costs, and increased adoption of digital trade finance solutions.

- Growth and expansion of digital platform

Krungthai Bank has seen significant user growth across its digital platforms:

- Paotang application: 40 million users

- Krungthai NEXT: 17.8 million users

- Thung Ngern: 2 million users

Krungthai Bank’s digital platforms provide a wide array of accessible services—including fund transfers, point redemption, and digital payments—to individuals and businesses across diverse geographic regions and income levels.

Siam Commercial Bank X

- SCBX launches the LLM model Typhoon

SCB 10X is strengthening its technological edge by developing localized AI capabilities that bridge the language gap and enable more personalized, efficient financial services for Thai consumers.

- SCB 10X launched Typhoon-7B, an open-source Thai language model on par with GPT-3.5, addressing the limitations of predominantly English-based AI systems.

- The model improves customer support by enabling faster, more accurate Thai-language interactions, enhancing user satisfaction and operational efficiency.

- Beyond service enhancement, Typhoon will power personalized financial products and targeted marketing, helping SCB deliver more tailored experiences to Thai consumers.

This initiative will be beneficial for the bank as it will drive customer engagement, increase operational efficiency, and deliver tailored financial solutions in Thailand. By leveraging AI capabilities, the bank can foster deeper connections with Thai consumers, streamline processes, and offer personalized experiences that meet the unique needs of the local market.

- Virtual banking consortium

SCBX is advancing its vision of inclusive finance by partnering with global innovators to develop digital-first banking solutions that expand access to affordable financial services in Thailand.

- SCBX and WeBank have formed a virtual banking consortium to pursue a virtual bank license under Thailand’s new digital banking framework.

- The collaboration leverages cutting-edge technology to deliver accessible, low-cost banking services, particularly targeting underserved and unbanked populations.

- This initiative aligns with SCBX’s broader mission to make financial services more transparent, inclusive, and equitable across the Thai economy.

This initiative focuses on underserved and unbanked populations, providing affordable, accessible banking services that can contribute to broader financial inclusion. Additionally, the integration of advanced technologies is expected to improve operational efficiency while promoting greater transparency and equity within the financial services sector.

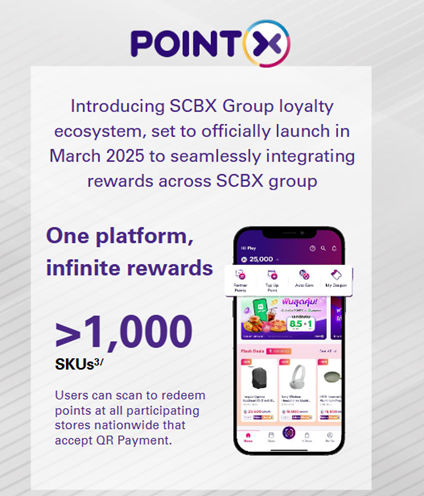

- Loyalty ecosystem

SCBX is redefining customer engagement with the launch of a unified digital rewards ecosystem that enhances loyalty, convenience, and personalization across its financial services network.

- SCBX will launch PointX in March 2025—a centralized loyalty platform that unifies rewards across the SCBX Group.

- The platform enables customers to seamlessly earn and redeem points across multiple stores using QR code payments, simplifying the user experience.

- With over 1,000 SKUs available for redemption, PointX strengthens customer retention while generating valuable insights to support personalized offers and services.

The incorporation of QR code payments enhances transaction efficiency, reflecting the broader shift toward digital, cashless payment solutions. Meanwhile, the diverse selection of SKUs for redemption not only boosts customer loyalty but also provides valuable data insights. These insights can be used to deliver tailored offers and services, fostering stronger customer relationships and supporting sustainable business growth.

Exhibit 1: Digital rewards system

- SCB 10x first purpose-bound money initiative

SCB 10X, with key partners, is advancing Thailand’s cashless economy through digital payment solutions that enhance security, and cross-border accessibility.

- SCB 10X, together with SCB, InnovestX, Fireblocks, Elliptic, Circle, and Base, launched Rubie Wallet—a digital wallet enabling closed-loop QR payments using regulated USD-pegged stablecoins and THBX (Thai Baht Stablecoin).

- The wallet incorporates Purpose-Bound Money (PBM) technology to reduce reliance on cash, lower transaction fees, and minimize foreign exchange risks, especially for international visitors.

- By offering a secure, stablecoin-based payment system, SCB positions itself at the forefront of the digital payment revolution, supporting both domestic and cross-border financial inclusion.

The incorporation of Purpose-Bound Money (PBM) technology not only reduces reliance on cash and lowers transaction costs but also mitigates foreign exchange risks, particularly benefiting international visitors.

TMB Thanachart Bank

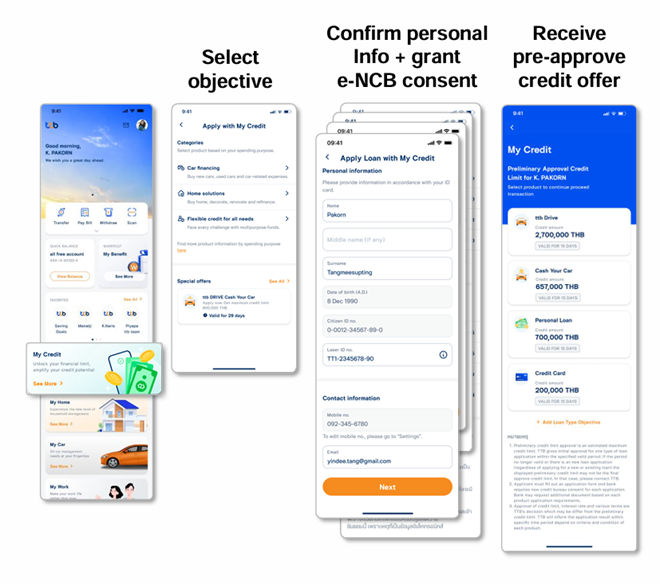

- My Credit widget

TMB Thanachart Bank is streamlining the lending journey by introducing digital tools that offer faster, more accessible credit services.

- TMB Thanachart launched My Credit, a digital widget that enables customers to choose loan types, verify personal information, and provide e-NCB consent entirely online.

- The platform delivers instant pre-approved credit offers, reducing processing time and removing manual steps—leading to faster, frictionless loan approvals.

- The impact is evident with credit card bookings growing 54%, CYC loans surged 122%, and personal and flash card loans rose 29% and 32%, respectively—reflecting rising consumer confidence and the effectiveness of the digital lending model.

This initiative improves the customer experience by reducing approval times and streamlining the process, while also allowing the bank to efficiently handle the growing demand for quick credit solutions.

Exhibit 2: TMB Thanachart bank credit widget

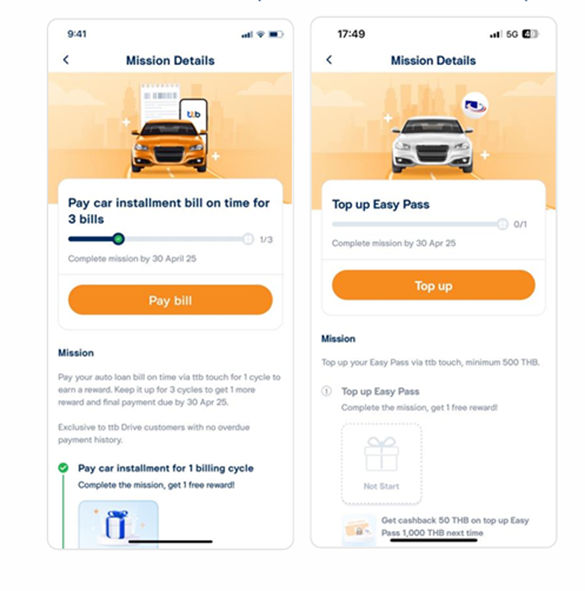

- Gamification

TMB Thanachart Bank is enhancing customer engagement and promoting responsible financial behavior through gamification, transforming everyday banking into an interactive, rewarding experience.

- TMB Thanachart introduced a gamification feature that allows customers to earn rewards by completing tasks such as timely car installment payments and Easy Pass top-ups.

- This approach promotes positive financial habits while making routine transactions more engaging and enjoyable.

This initiative drives higher customer engagement while strengthening client relationships, and enhancing satisfaction and loyalty. Additionally, user interaction data offers insights to optimize marketing strategies and service offerings, supporting the bank’s growth and retention goals.

Exhibit 3: Gamification feature

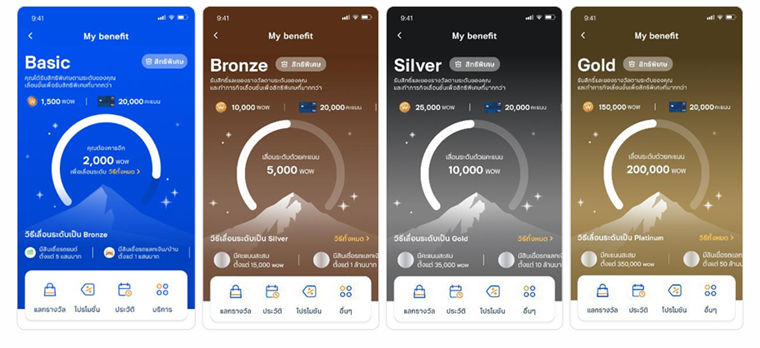

- Customer status tiers

The bank is deepening customer relationships with a structured loyalty program that rewards engagement and encourages long-term banking behaviour through personalized incentives.

- In Q2 2025, TTB will launch a tier-based loyalty program featuring four levels—Basic, Bronze, Silver, and Gold—determined by WOW points earned through transactions and banking activities.

- As customers move up the tiers, they gain access to progressively more valuable rewards, with the Gold Tier (200,000 points) offering premium benefits and exclusive banking privileges.

This tier-based loyalty program deepens customer relationships by incentivizing engagement through personalized rewards. By offering benefits, it aims to enhance customer retention, strengthen brand loyalty, and drive long-term value within its ecosystem.

Exhibit 4: Tier based loyalty program

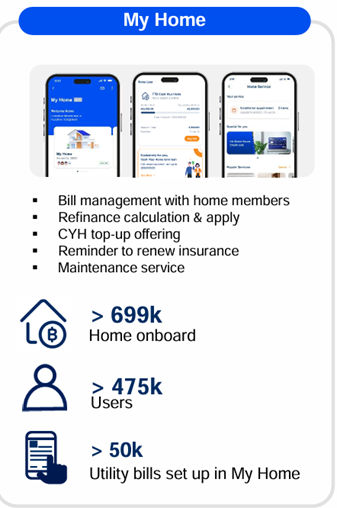

- My Home

TMB Thanachart Bank is enhancing its homeowner experience with digital tools that centralize property-related services and unlock financial flexibility through intuitive, user-friendly features.

- TMB Thanachart Bank launched “My Home,” a digital feature that simplifies homeownership management.

- Through the platform, users can manage utility bills, split payments, get insurance renewal reminders, access refinance calculators and explore home equity options.

The “My Home” feature enhances customer engagement by centralizing property-related services in a single platform. It improves convenience and supports smarter financial planning.

Exhibit 5: My Home digital feature

Bangkok Bank

- E-wallet white labelling service

- Bangkok Bank partnered with a fintech provider to launch a white-label service for corporate customers.

- The solution addresses the growing consumer preference for e-wallet payments over traditional bank transfers.

- It minimizes businesses’ need for system development and maintenance, offering faster time-to-market and reduced IT costs for quick adaptation to evolving payment trends.

This white-label service allows Bangkok Bank to provide scalable, cost-effective payment solutions to corporate clients. It supports the bank’s ability to meet the growing demand for e-Wallet payments, strengthens corporate relationships, and contributes to revenue through digital payment services.

- Seamless transactions

- Bangkok Bank introduced a scan-to-pay service through its Mobile Banking app.

- It enables Thai customers traveling to China to make payments using Weixin Pay QR (WeChat Pay) and UnionPay QR, enhancing cross-border payment convenience.

This initiative allows support for cross-border transactions by providing payment options for Thai travelers in China. It improves customer convenience, integrates with the bank’s digital payment services, and may lead to increased transaction volume through partnerships with WeChat Pay and UnionPay.

Financial performance

Revenue analysis

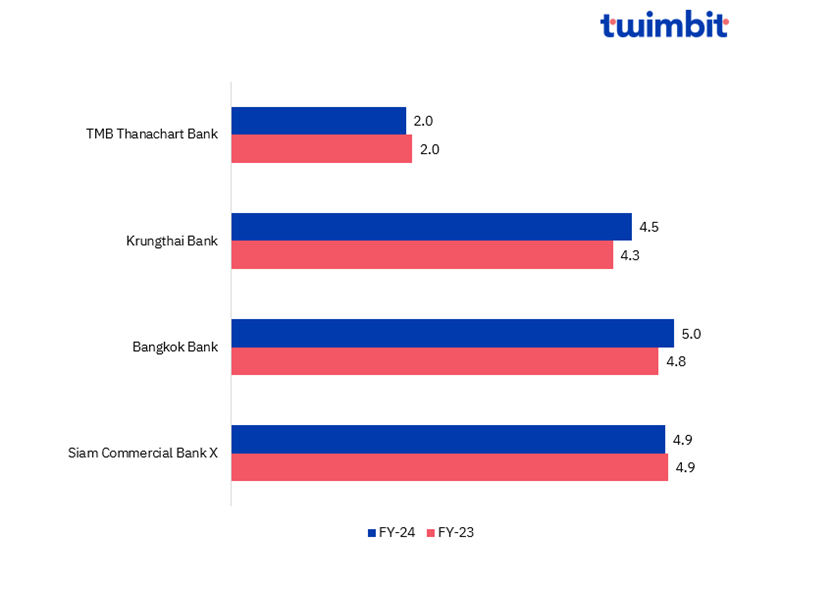

Thailand’s leading banks demonstrated steady growth in FY-24, with overall net revenues increasing by 1.73% YoY, from USD 16.1 billion in FY-23 to USD 16.4 billion in FY-24.

Exhibit 6: Net revenue of top Thailand banks

Source: Bank Financials, Twimbit analysis

- Krungthai Bank

Krungthai Bank achieved an impressive 5% YoY increase in net revenue, rising from USD 4.3 billion in FY-23 to USD 4.5 billion in FY-24. This growth was primarily driven by a 7% increase in interest income, which rose from USD 4.4 billion in FY-23 to USD 4.7 billion in FY-24, and a 3.88% increase in loans to customers increasing from USD 3.9 billion to USD 4.03 billion.

- TMB Thanachart Bank

TMB Thanachart Bank experienced a 3.58% decline in net revenue, dropping from USD 2.04 billion in FY-23 to USD 1.97 billion in FY-24. This decline was driven by an 18.42% increase in interest expense rising from USD 631.4 to USD 747.8.

Profitability analysis

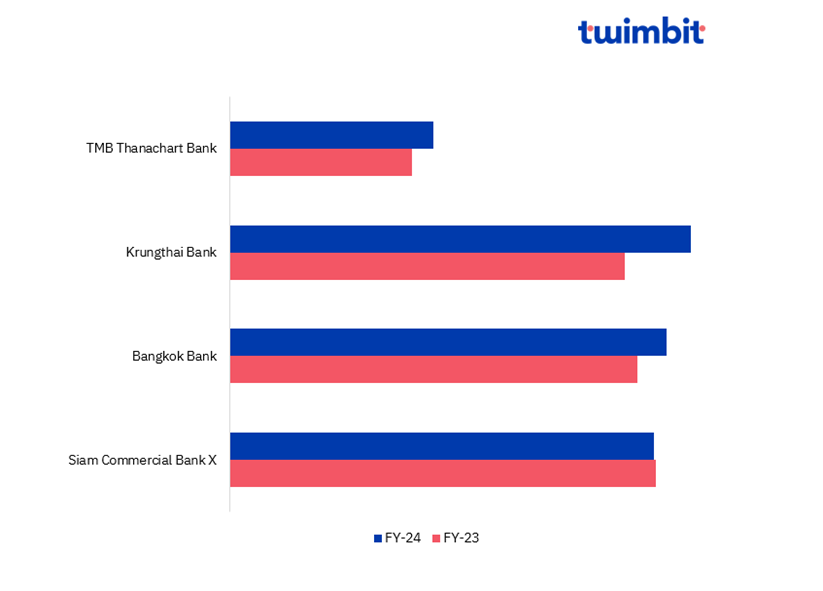

Thailand’s top banks recorded an 8.02% YoY increase in net profits, rising from USD 4.1 billion in FY-23 to USD 4.5 billion in FY-24.

Exhibit 7: Net Profit of top Thailand banks

Source: Bank Financials, Twimbit analysis

- Krungthai Bank

Krungthai Bank delivered a 16.61% YoY increase in net profit, rising from USD 1.2 billion in FY-23 to USD 1.4 billion in FY-24. This was primarily driven by a 15.06% YoY increase in other non-interest income, climbing from USD 437 million to USD 503 million, along with a 17.4% decrease in expected credit losses, which declined from USD 1.06 billion to USD 0.88 billion.

- Siam Commercial Bank X

Siam Commercial Bank X showed a slight decline of 0.48% in its net profit, decreasing from USD 1.3 billion in FY-23 to USD 1.2 billion in FY-24. This decline was due to an 8% YoY increase in interest expenses rising from USD 1.04 billion to USD 1.1 billion and a 47% YoY decrease in its other operating income decreasing from USD 122 million in FY-23 to USD 65 million in FY-24.

Fee-based income analysis

Fee income across Thailand’s top banks declined slightly by 0.55% YoY, declining from USD 3.8 billion in FY-23 to USD 3.7 billion in FY-24.

Exhibit 8: Fee incomes of the top banks in Thailand

Source: Bank Financials, Twimbit analysis

- Krungthai Bank

Krungthai Bank achieved a 6.33% YoY increase in fee income, reaching USD 878 million, up from USD 826 million in FY-23. This growth was primarily driven by its strategic focus on maximizing economic value and profitability by fully leveraging the bank’s current business ecosystems. A significant driver of this success was the sustained increase in fee-based income from wealth management. This growth was fueled by strong performance in mutual funds and bancassurance, alongside expanded revenue streams from credit card-related services.

- TMB Thanachart Bank

TMB Thanachart Bank showed a decline of 8% in its fee income, decreasing from USD 403.4 million in FY-23 to USD 371.6 million in FY-24. This decline was due to a 5% YoY decrease in acceptance, avals (financial guarantees provided by banks to ensure payment of a debt), and guarantees instruments declining from USD 16 million to USD 15.2 million, and a 12.73% YoY decrease in its funds and bancassurance decreasing from USD 205.1 million in FY-23 to USD 179 million in FY-24.

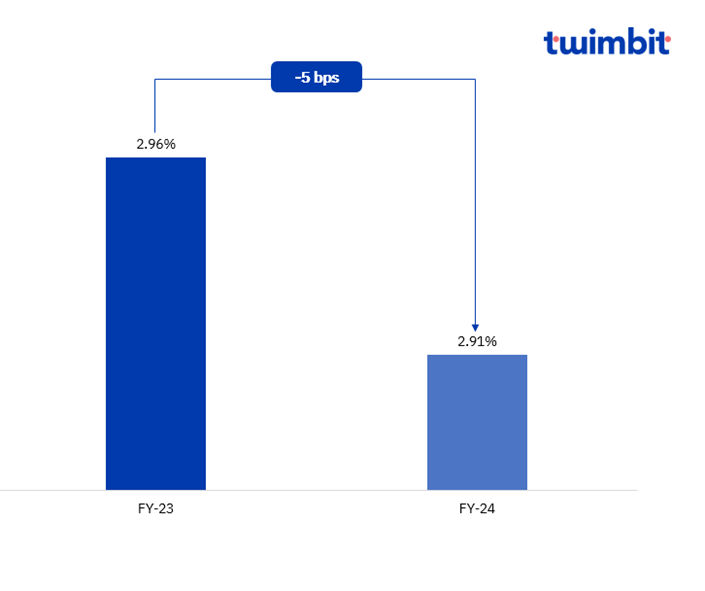

Non-performing loans (NPL)

The average NPL ratio across Thailand Banks declined by 5 bps, improving from 2.96% in FY-23 to 2.91% in FY-24.

Exhibit 9: Average NPL of the top banks in Thailand

- Krungthai Bank

Krungthai Bank recorded a 9 bps decline in its NPL ratio, reducing it from 3.08% in FY-23 to 2.99% in FY-24. This was driven by a 2% decrease in Allowance for Expected Credit Losses, falling from USD 5.2 billion to USD 5.1 billion.

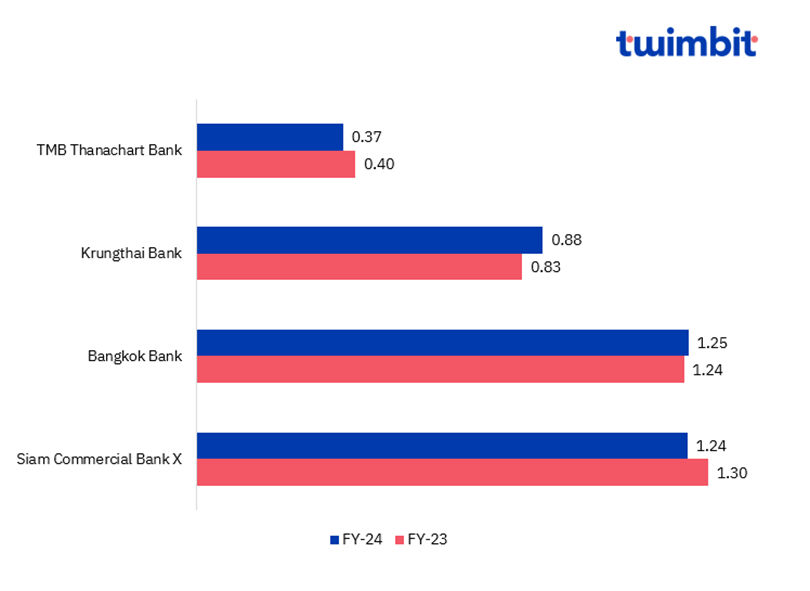

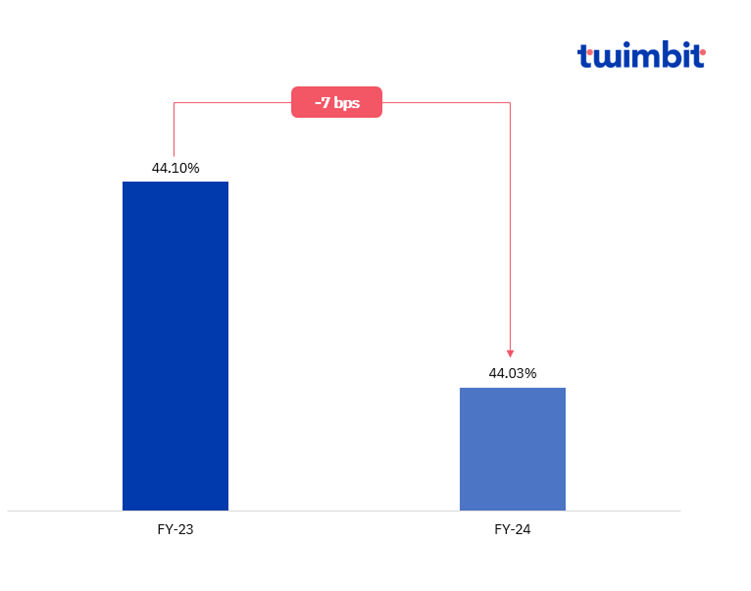

Cost Efficiency (CE)

The average cost efficiency across Thailand Banks improved by 7 bps, from 44.1% in FY-23 to 44.03% in FY-24.

Exhibit 10: Average CE of the top banks in Thailand

- Krungthai Bank

Krungthai Bank recorded a 160 bps increase in its CE ratio, from 41.6% in FY-23 to 43.2% in FY-24. This was driven by a 9.12% increase in Total other operating expenses, rising from USD 1.8 billion to USD 2 billion.

- TMB Thanachart Bank

TMB Thanachart Bank showed a 140-bps decline in its CE ratio, decreasing from 44% in FY-23 to 42.6% in FY-24. This decline was due to a 6.22% YoY decrease in other operating expenses, declining from USD 895.5 million to USD 839.8 million, and an 11.82% YoY decrease in its expected credit loss, decreasing from USD 639.3 million in FY-23 to USD 563.8 million in FY-24.

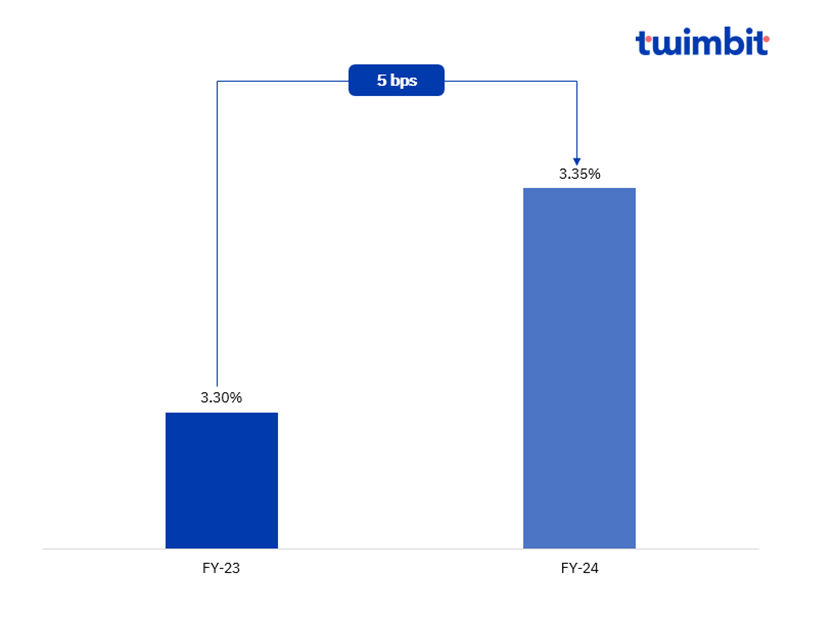

Net interest margin (NIM)

The average NIM across Thailand Banks increased by 5 bps, from 3.3% in FY-23 to 3.35% in FY-24.

Exhibit 11: Average NIM of the top banks in Thailand

- Siam Commercial Bank X

Siam Commercial Bank X showed a slight increase of 10 bps in its NIM ratio, increasing from 3.7% in FY-23 to 3.8% in FY-24. This rise was due to a 2.36% YoY increase in net interest income, rising from USD 3.6 billion to USD 3.7 billion.

Outlook

Thailand’s banking sector in 2025 is poised to navigate a landscape marked by modest economic growth, evolving government policies, and technological advancements. The economy is projected to grow at an average of 2.8% annually over 2025-2027, with a gradual recovery following the projected 2.7% growth in 2024. This environment presents opportunities for banks operating in the country.

- Thai banks are rapidly investing in emerging technologies to drive growth and efficiency. A survey reveals that 81% of banking CEOs prioritize generative AI (Gen AI) as the key to business transformation. SCB 10X is advancing AI with its Thai-language model, Typhoon, and partnerships like TogetherAI to enhance customer service. These initiatives underscore Thailand’s banking sector’s strategic focus on digital innovation, positioning institutions to enhance operational efficiency and drive customer-centric solutions in an increasingly digitized financial ecosystem.

- Thailand’s Buy Now Pay Later (BNPL) market is set to grow 14.9% annually, reaching $3.94 billion by 2025, driven by e-commerce growth and demand for flexible payments. Strategic partnerships between banks and fintechs are critical, enabling seamless integration with payment networks, expanding consumer reach, and enhancing merchant adoption. For example, Bangkok Bank’s ‘Be Smart’ installment plan allows customers to repay monthly while merchants receive full payments promptly after fees and interest deductions. As the market evolves, such alliances will be pivotal for banks to leverage customer ecosystems, drive innovation, and maintain a competitive edge in the digital payments landscape.