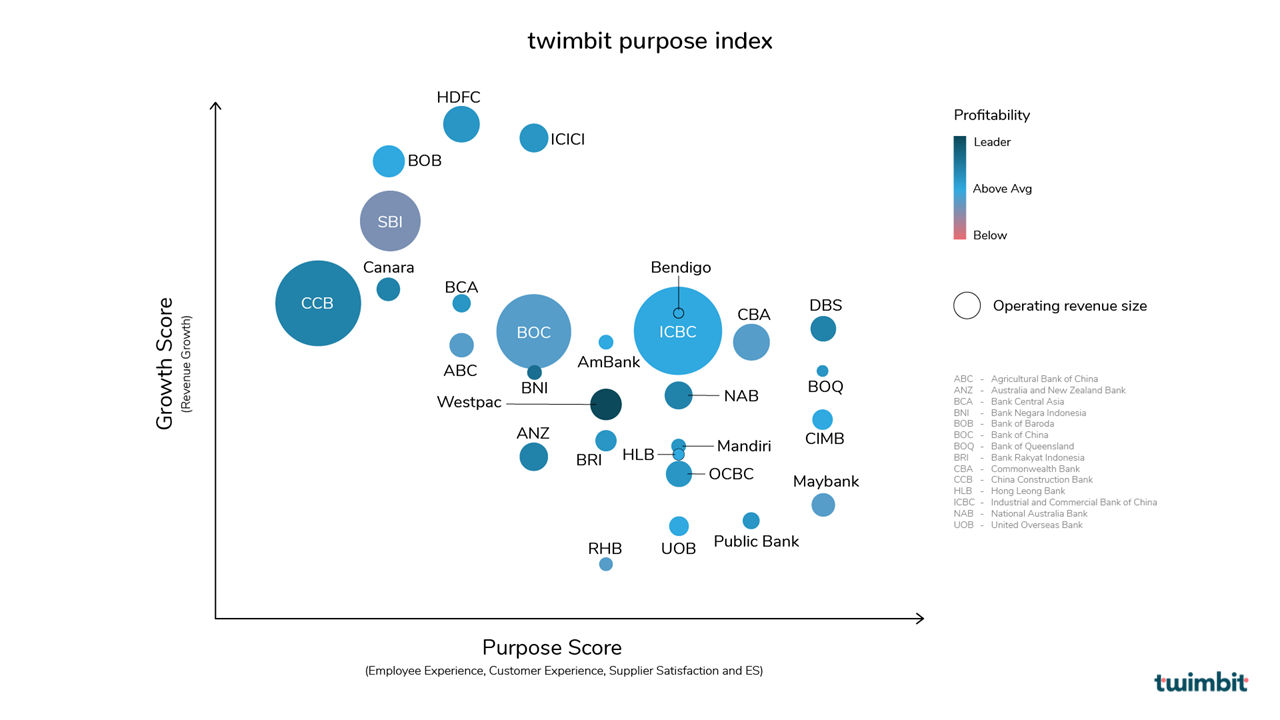

twimbit purpose index

Companies need to serve a purpose beyond just shareholder value. ESG is not just a compliance requirement, but a way of being. The twimbit purpose index is about helping Asia’s leading corporations migrate to the future desired state of being purpose driven organisations. It is our belief that every organisation, (including every bank) should serve all its stakeholders in equal measure. It should be equally accountable to all five stakeholders:

- Shareholders

- Customers

- Partners / Suppliers

- Planet / Society

- Employees

This report benchmarks Asia Pacific’s top 28 banks across these five pillars. They provide a basis of understanding best practices and innovation opportunities for the industry.

Key takeaways

- #1 DBS is the best performer among all 28 banks in driving the highest stakeholder value across the four purpose pillars

- #2 Along with DBS, BOQ, CIMB, & Maybank scored high on purpose pillars across all 28 banks

- #3 CIMB and Maybank purpose score is reflective of their strong investment in increasing stakeholder value across the four purpose pillars, a big feat for Malaysian banks

- #4 Westpac is the clear leader in driving profitability across all 28 banks

- #5 Despite having a good growth score and revenue, SBI is fairing lowest in profitability and purpose score

- #6 The largest operating revenue pool of ICBC, CCB, ABC and BOC is not translated in their profitability scores

- #7 Indian financial services market is fast growing with HDFC, ICICI, and BOB having the highest growth score with above average profitability despite small operating revenue size compared to the other banks

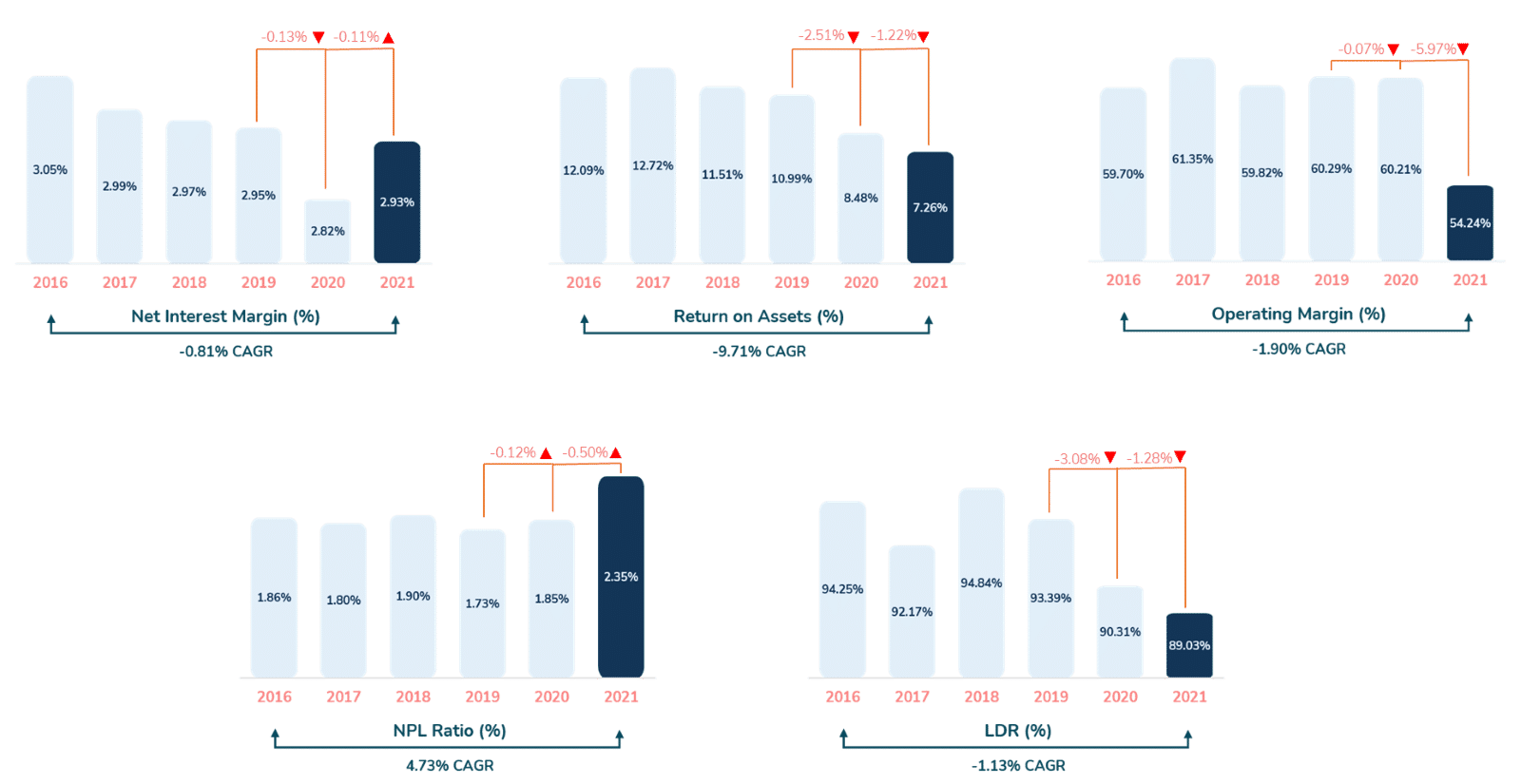

In the last two years because of the pandemic, we saw banks’ operational efficiency and profitability take a hit. This is mainly a result of low loan to deposit ratios and net interest margins, and at the same time, a rise in non-performing loans.

While the banks witness a slow operational performance, they indicate strong resilience and maintained digital investment throughout 2020 and 2021.

Our analysis of these banks unlocked a multitude of innovation opportunities across the following four purpose pillars:

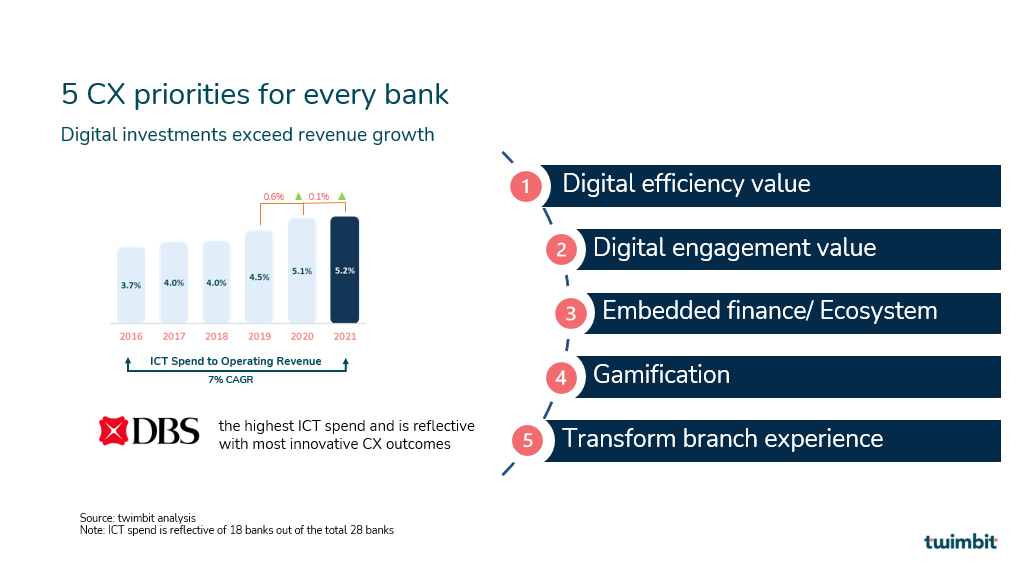

#1 Customer experience CX – Re-imagine the path to CX success

Banks are at the forefront of becoming digital-first businesses. They are using technological advancements to provide customers with reimagined experiences. In our study, we see that the banks have adopted 5 priorities (see figure 1) which they are fulfilling through increased digital investments.

DBS has the highest ICT spend out of all 28 banks and that is reflected through its most innovative CX initiatives.

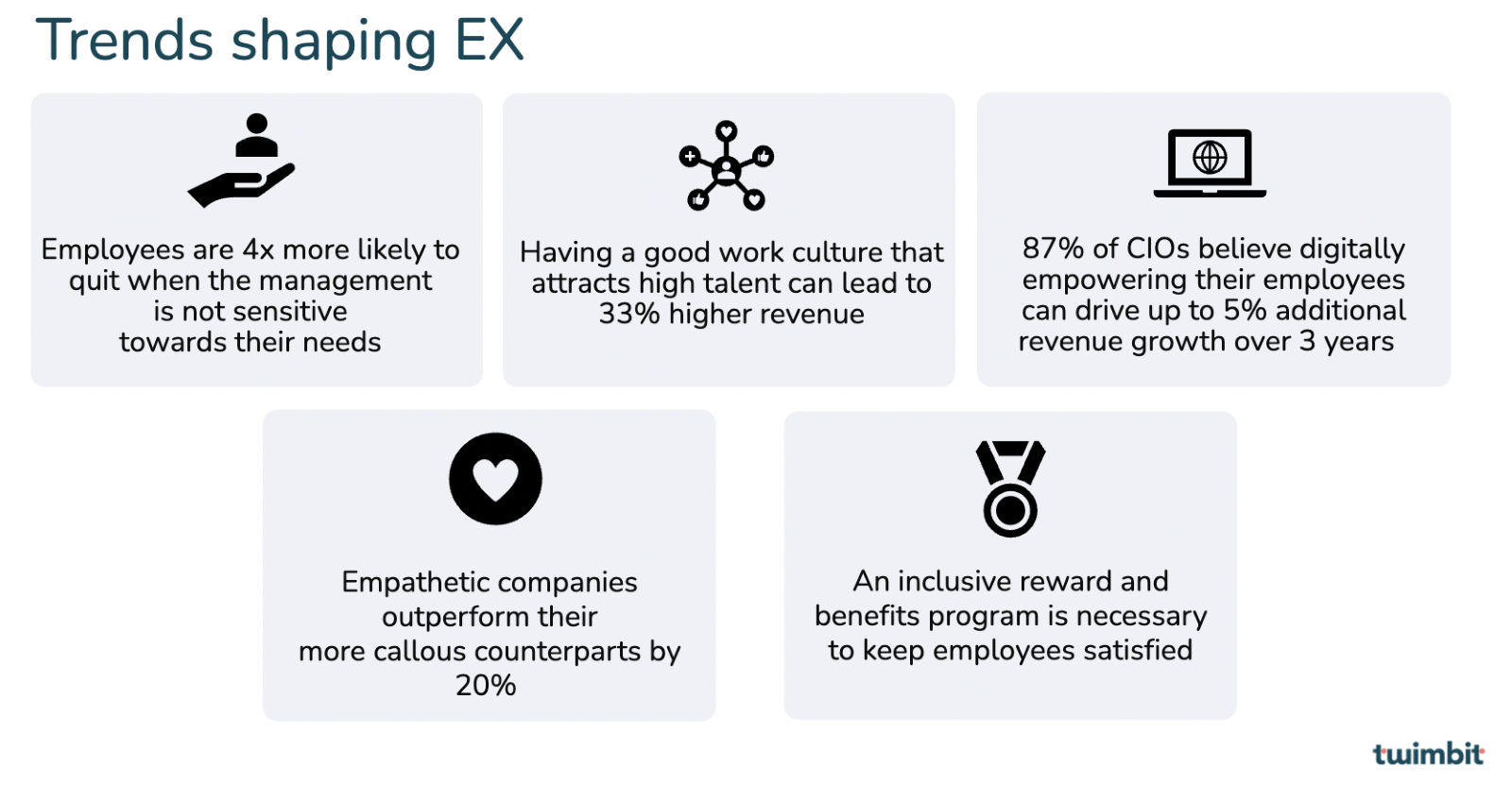

#2 Employee experience (EX) – Learn best practices to deliver exceptional EX

Banks realise the potential to craft experiential EX that accelerates organisational growth. Exceptional growth can be achieved by creating a digitally forward and relevant organisation. In our study, we see 5 trends that shape up employee experience, which can be seen in the image below:

Source: Gallup 2018, TinyPulse 2020, People matters, VMware 2018, Rise people 2019 (see endnote 1).

Some of the best practices driving EX across all banks include:

- Scholarships for higher studies

- Diversity and inclusion programs

- Technology for upskilling

- Health and wellness initiatives

- Financial wellbeing programs

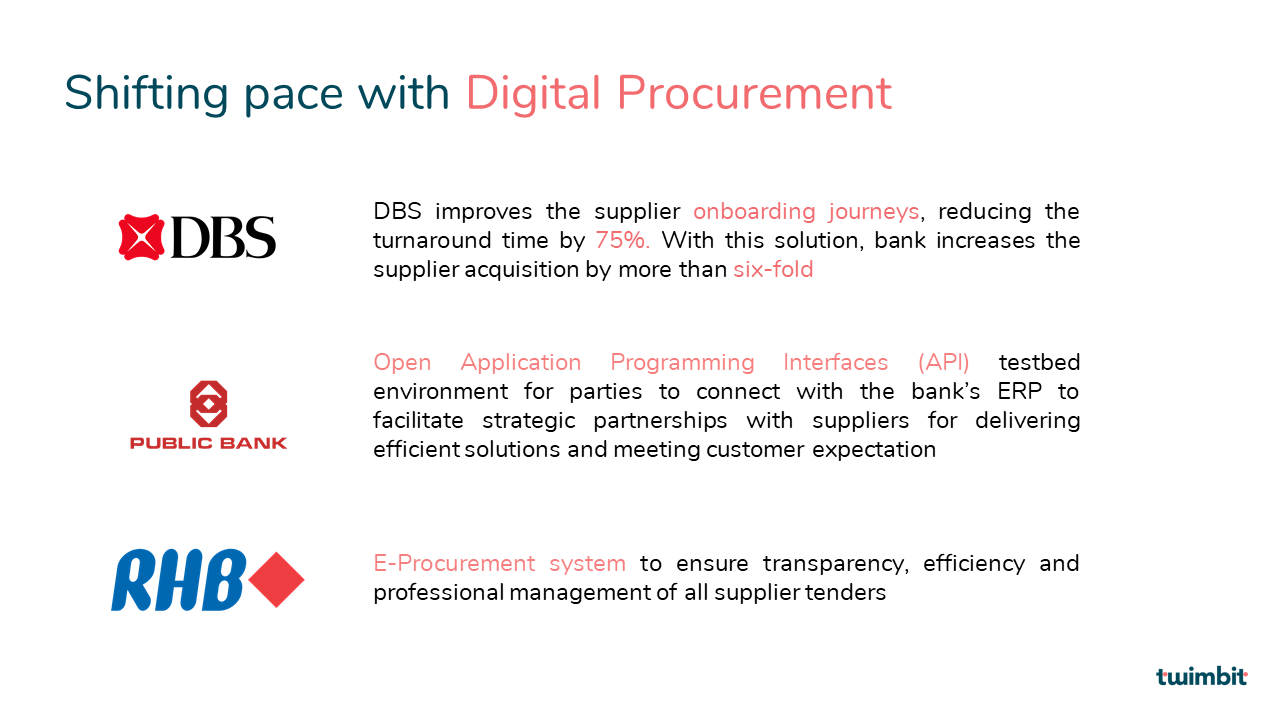

#3 Supplier Satisfaction – What does it take to treat suppliers as customers

One of the big feats for banks towards their suppliers’ satisfaction is the shift from traditional procurement methods to digital procurement. Digital procurement can cut up to 40% of costs in traditional procurement practices. These banks have eased onboarding journeys, facilitation of partnerships, and ensured efficiency for their suppliers as we can see in the image below:

Banks drive supplier satisfaction through 4 sustainable best practices:

- ESG in supply chain

- Indigenous procurement

- Diversity and inclusion

- Shared purpose

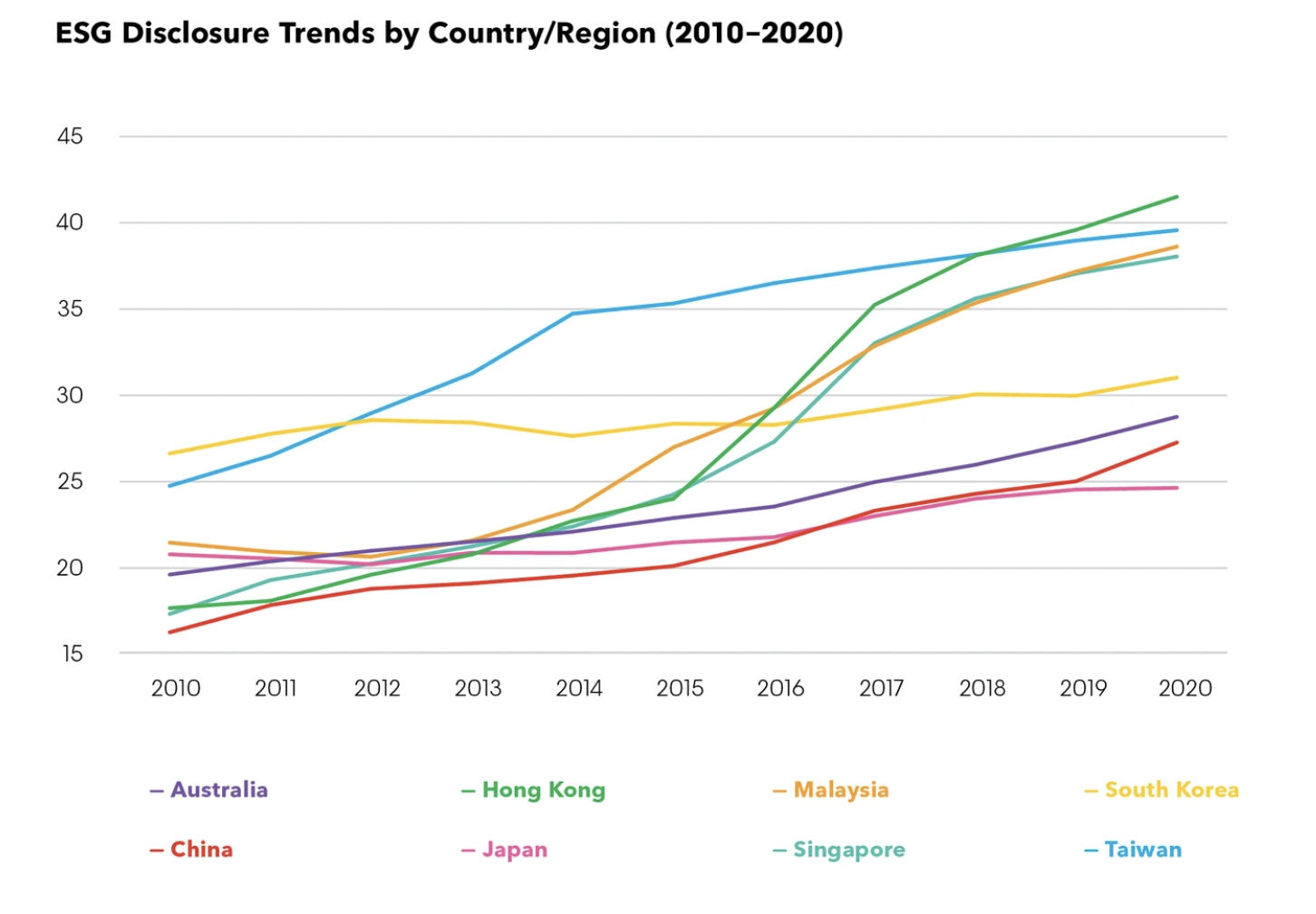

#4 Society and Planet Impact – Ensuring compliance and responsible reporting

Disclosure of ESG data has increased in all countries and regions in APAC over the past decade, but the region is still lagging behind the global average. The main hurdle APAC banks face is a lack of standardised regulation and reporting methodology, where regulators in each market predominantly work in isolation.

With Asia being the largest primary energy consumer, regulations must be bolstered to encourage sustainability-decision making and drive the ESG agenda. Corporate governance is the weakest area for ESG in APAC.

For the purposes of this study, governance initiatives were not included as part of the analysis; hence, we only evaluated the initiatives taken by the banks for environment and society impact (ES).

Source: Bloomberg 2021 (see endnote 2).

APAC banks are winning ES through these best practices:

- Green lending and investing

- Financial literacy programs to empower communities

- Adopting tech for improved ES reporting

- Align with central banks’ ESG initiatives

- ESG lending exclusion lists for greater transparency

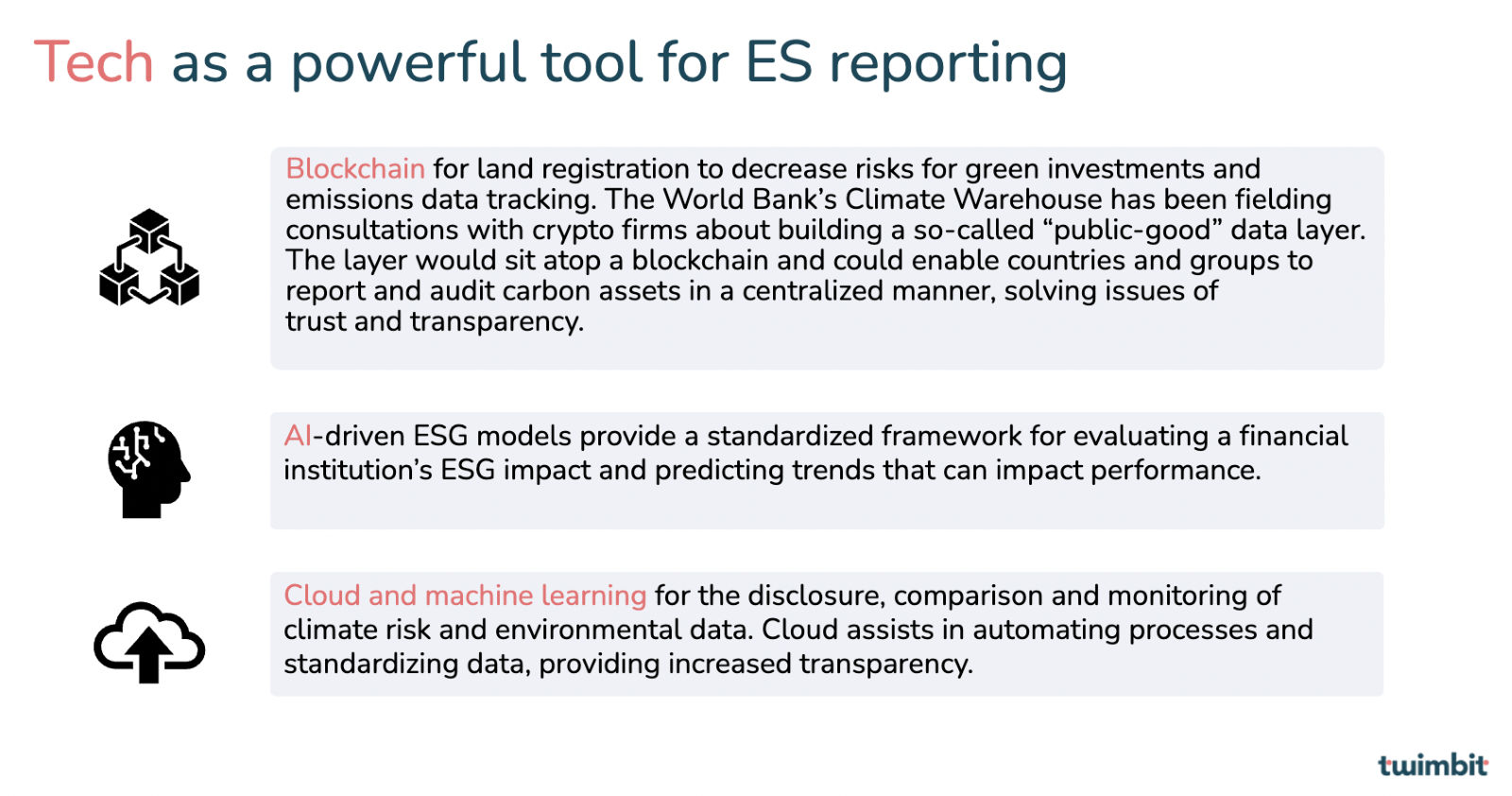

The emergence of tech-enabled use cases to improve the quality and accuracy of ES reporting is acting as a powerful tool for banks to rethink their existing ESG practices. Here are a few ways in which banks can leverage technology for reporting:

For detailed insights, download the State of top APAC banks 2022 report.

Endnotes

- Gallup 2018( Culture Wins By Getting the Most Out of People (gallup.com), TinyPulse 2020 (17 Surprising Statistics about Employee Retention (tinypulse.com), People matters (Article: Future Ready, Job Ready: Where and How to Find the Best Talent for the Future of Work – People Matters), VMware 2018 (vmw-impact-of-digitally-empowered-workforce.pdf (vmware.com), Rise people 2019 (The importance of showing empathy in the workspace)

- Bloomberg. (2021). ESG disclosures gain traction in APAC. [Online] Available: https://www.bloomberg.com/professional/blog/esg-disclosures-gain-traction-in-apac/. [Accessed: 5-January-2022].