Located in Marina Bay, Singapore, DBS Bank Limited is one of Singapore’s ‘Big 3’ banks, along with OCBC and UOB. The bank operates more than 150 branches in Singapore, with services available for customers in 18 countries. In addition, DBS operates in six core markets: Singapore, Indonesia, India, China, Hong Kong, and Taiwan. The bank also has a presence in Malaysia, Thailand, Vietnam, and Japan.

Financial highlights

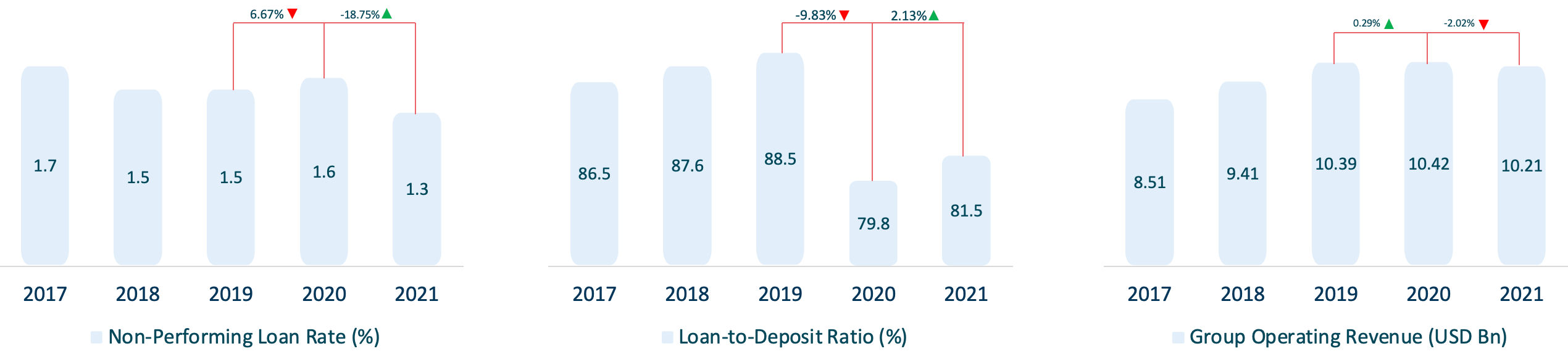

As the bank’s asset quality improved, the non-performing loan (NPL) rate also reduced by 5.22% from FY17 to FY21 (Figure 1). On the other hand, the loan-to-deposit (LDR) ratio declined by 1.18% during the same period. Ideally, the LDR ratio should be between 80% – 90%, but DBS is on the lower end of the threshold. Therefore, DBS should strive to increase its loan disbursement to 90% or above, as it will help DBS improve its declining net interest margin, which has fallen by 3.69% between FY17 and FY21 (Figure 2).

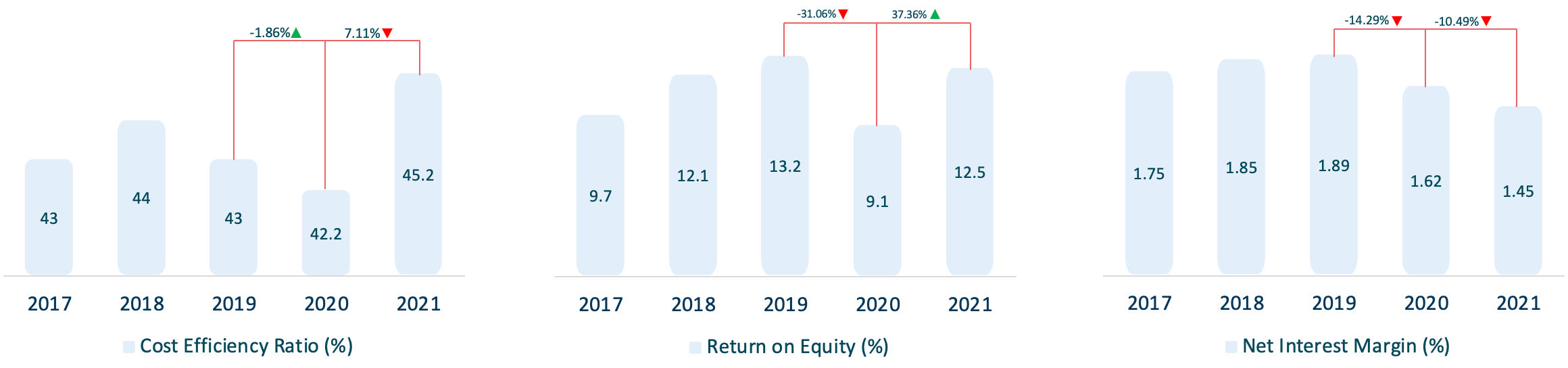

Banks in Singapore generally operate at high-cost efficiencies compared to banks in other regions across APAC. For instance, in 2019, Singaporean banks reported a cost efficiency ratio of 57.96%. However, DBS reported a much lower cost efficiency ratio of 43% in 2019 (Figure 2). Since then, the ratio has increased for DBS by 1.68%, but the bank still operates at a cost efficiency of 45.2%, indicating that it is still operating at high efficiency.

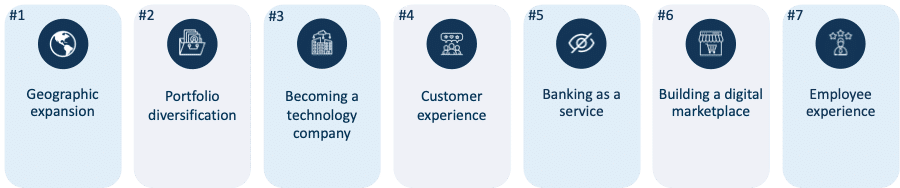

Strategic focus areas

- #1 Geographic expansion

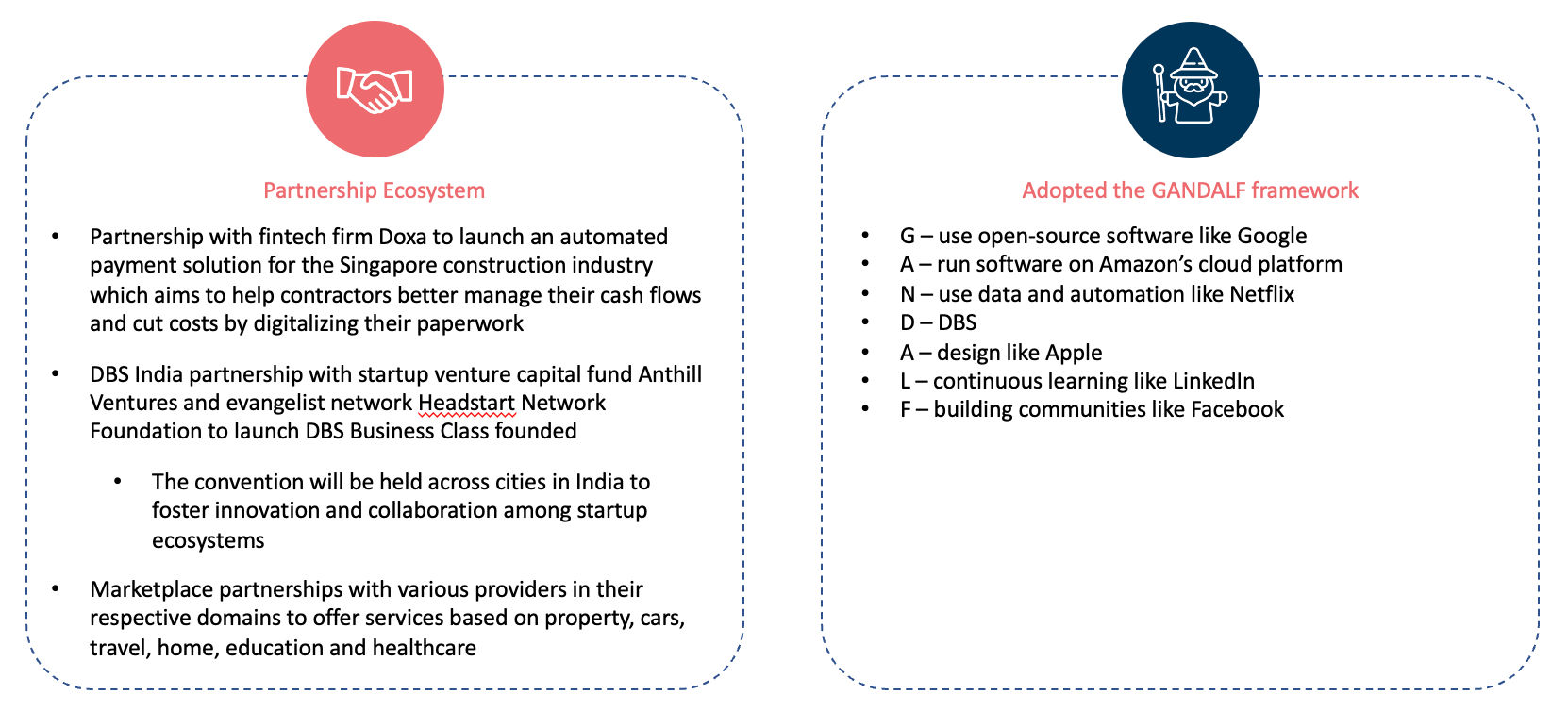

Reflecting upon the belief in Asia’s long-term prospects, DBS capitalised on this opportunity, strategically strengthening its franchise in key growth markets. The bank merged with Lakshmi Vilas Bank (LVB) of India, creating an enlarged footprint, mainly in Southeast India. The merger helped DBS overlay its digital strategy in India by adding LVB’s 600 branches and 1,000 ATMs.

DBS entered into an agreement with Shenzhen Rural Commercial Bank of China, subscribing to a 13% stake. This allowed DBS to accelerate its expansion in the Greater Bay Area. DBS also acquired Citigroup Taiwan’s consumer banking business, helping DBS accelerate its growth in Taiwan by 10 years.

The geographic expansion and new businesses are expected to add USD 940 million to the bank’s revenue.

- #2 Portfolio diversification

DBS launched a joint venture, DBS Securities (China), to capitalise on the two-way deal flow in China as the country opens. The joint venture engages in business’ including brokerage, securities investment consulting, security underwriting and sponsorship.

The bank became the anchor investor in the Muzinich Asia Pacific Private Debt I fund. The fund was set up to provide financial assistance to sound businesses dislocated by the disruptions as a result of the pandemic. In addition, the DBS Digital Exchange platform offers tokenisation, trading and custody services of digital assets, including cryptocurrencies.

- #3 Becoming a technology company

DBS has set up various ventures:

- Partior – A blockchain-based cross-border multi-currency clearing and settlement provider in collaboration with J.P.Morgan and Temasek to enable more efficient digital clearing and settlement solutions across the banking industry.

- Climate Impact X (CIX) – A global exchange and marketplace for high-quality carbon credit-based investment set up in partnership with Singapore Exchange, Standard Chartered and Temasek.

- Fixed Income Execution (FIX) Marketplace – Asia’s first fully digital and automated fixed income execution platform allows issuers to issue their bonds in the marketplace.

Also, DBS is launching DBS BetterWorld on the Sandbox metaverse.

- #4 Customer experience

At DBS, the customer comes first, the employees second, and the stakeholders third. To achieve this, the bank introduced a customer journey mapping tool to solve customer queries and better visualise the customer’s interaction with the bank from their perspective.

The launch of the DBS PayLah lifestyle app for customers to conduct everyday transactions was one of the bank’s efforts to elevate the customer experience. The lifestyle app allows customers to book tickets and rides, pay expenses, access rewards and order meals. It also allows customers to scan to pay at more than 180,000 points.

- #5 Banking as a service

DBS has developed a strategy of developing APIs to seamlessly embed its products and services into its partner ecosystem and platforms. The bank launched the developer platform of APIs in 2017, enabling software developers to communicate with the bank and link up services such as peer-to-peer service payment and mortgage affordability assessment. Currently, the network has more than 1,000 open APIs.

- #6 Building a digital marketplace

DBS launched its customer needs-driven marketplace in 2017, titled the DBS Marketplace. The marketplace encompasses the DBS Electricity Marketplace, the DBS Property Marketplace and the DBS Travel Marketplace in 2019. On top of that, the DBS Property and Car Marketplaces generated more than USD 730 million in loans across Singapore, Taiwan, and Hong Kong markets in 2020.

- #7 Employee experience

DBS has taken various initiatives to enhance its employee experience. One of them included the bank introducing the MOJO campaign to remove meetings that did not prove meaningful. The campaign established five characteristics – agile, continuous learning, customer obsession, data-driven experimentation and risk-taking. In addition, the bank has created a flexible working environment and a job-sharing scheme that allows a full-time job to be divided among two employees.

To know more about DBS’ employee experience, check out this article.

DBS digital strategy

DBS plans to deliver its digital strategy through the following (Figure 4).

4 growth opportunities for DBS

- #1 Enhancement of the branch network

DBS is redesigning its self-service branches and kiosks to leverage solar power along with an overhaul to the ATM and self-service management using data analytics and machine learning. In addition, the bank is rolling out self-service banking machines in the form of Video Teller Machines (VTMs) and Branch Teller Machines (BTMs). These enable customers to complete complex transactions securely.

The next step for the bank is to transform the branches into community hubs to boost social engagement. For example, the bank can work to create safe play areas for children within the existing branches. The bank should also make its branches age-friendly for senior customers unfamiliar with digital tools.

- #2 Cost to serve

The net income ratio for DBS has increased. The increase in net interest income, fee & commission income, and trading income significantly contribute to DBS’ net income ratio. On the other hand, the bank has reduced its cost per employee by 1.16% and occupancy-related expenses by 8% between FY2017 and FY2021.

- #3 Shaping a climate-aligned future

DBS became the first bank in Singapore to sign the United Nations-convened Net-Zero Banking Alliance. The bank is committed to growing its suite of sustainable investments and products to more than 50% of its AUM by 2023 and zero thermal coal exposure by 2039.

In the future, DBS should encourage its employees to use green modes of transportation, i.e., electric vehicles and cycles to further reduce their carbon footprint. Another central area that the bank can seek to improve on is in regards to renewable energy. Currently, 0.95% of the bank’s energy usage comes from renewable sources.

- #4 Buy Now Pay Later (BNPL)

DBS launched the ‘Mastercard instalments with Pine Labs’ program to its two million DBS and POSB credit card holders. The program is available exclusively to all DBS and POSB Mastercard, Visa and American Express credit card users and allows flexible instalment repayment periods with no interest charge.

The next step for the bank is to expand the program’s scope to its debit card holders. In addition, the bank should also increase the tenure for repayment and broaden the program’s acceptance to online e-commerce channels and online retail stores.

Conclusion

DBS has been a pioneer and at the forefront of digital innovation, with the bank winning various awards for its digital initiative and digitalisation efforts. The bank is considered by many as the perfect bank. However, there are areas such as enhancement of the branch network and new opportunities like buy now pay later by which DBS can improve profitability and enhance the customer experience and employee experience offered.