Executive summary

- Telcos are making good headway in growing their enterprise business. It now accounts for 20 percent of their total revenues, growing at an impressive rate of 11.9 percent compared to the total business growth rate of 6.7 percent.

- We project that the enterprise business segment will grow to reach 30 percent of total revenues by 2030.

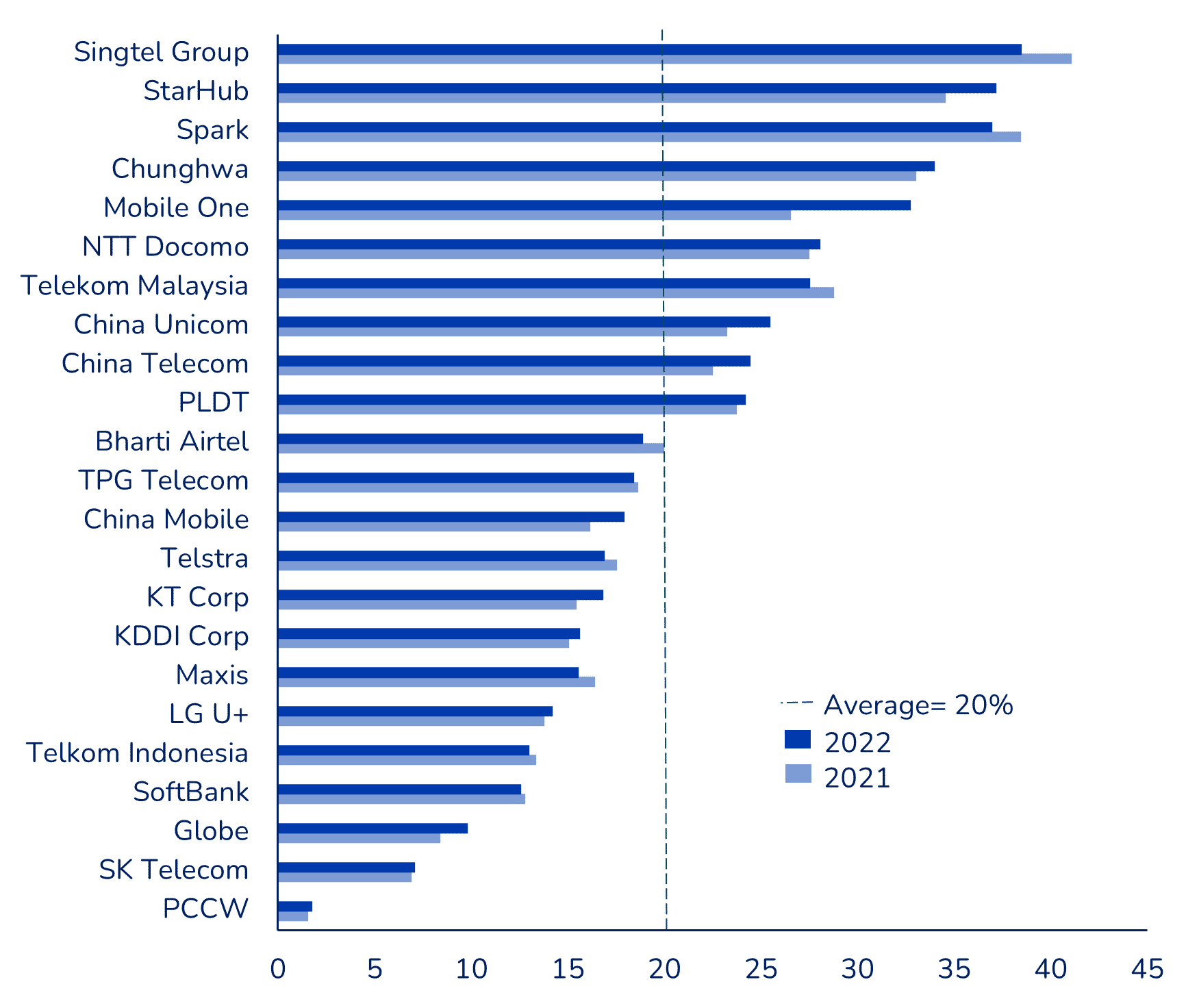

- Eight telcos have already achieved enterprise revenue contributions exceeding 25 percent. Exhibit 1 shows the percentage contribution of enterprise business to total for Asia Pacific’s leading telcos.

Exhibit 1

Enterprise revenue to total revenue, 2022 (%)

- China Mobile, the largest operator in our analysis, showcased exemplary performance with an enterprise business revenue of US$ 25.2 billion, representing 17.9 percent of total revenues and growing at a remarkable rate of 22.6 percent.

- M1 Singapore (Mobile one) recorded the highest growth in the enterprise segment of 33 percent. Additionally, M1’s enterprise revenue as a percentage of total revenue increased from 26.6 percent in 2021 to 32.7 percent in 2022. This difference of 6.2 percentage points is the highest in the industry.

- Singtel Group is an overall strong leader in the enterprise business. It has registered a decline in enterprise revenue due to the sale of Amobee. Enterprise revenues contribute 38.5 percent to its total.

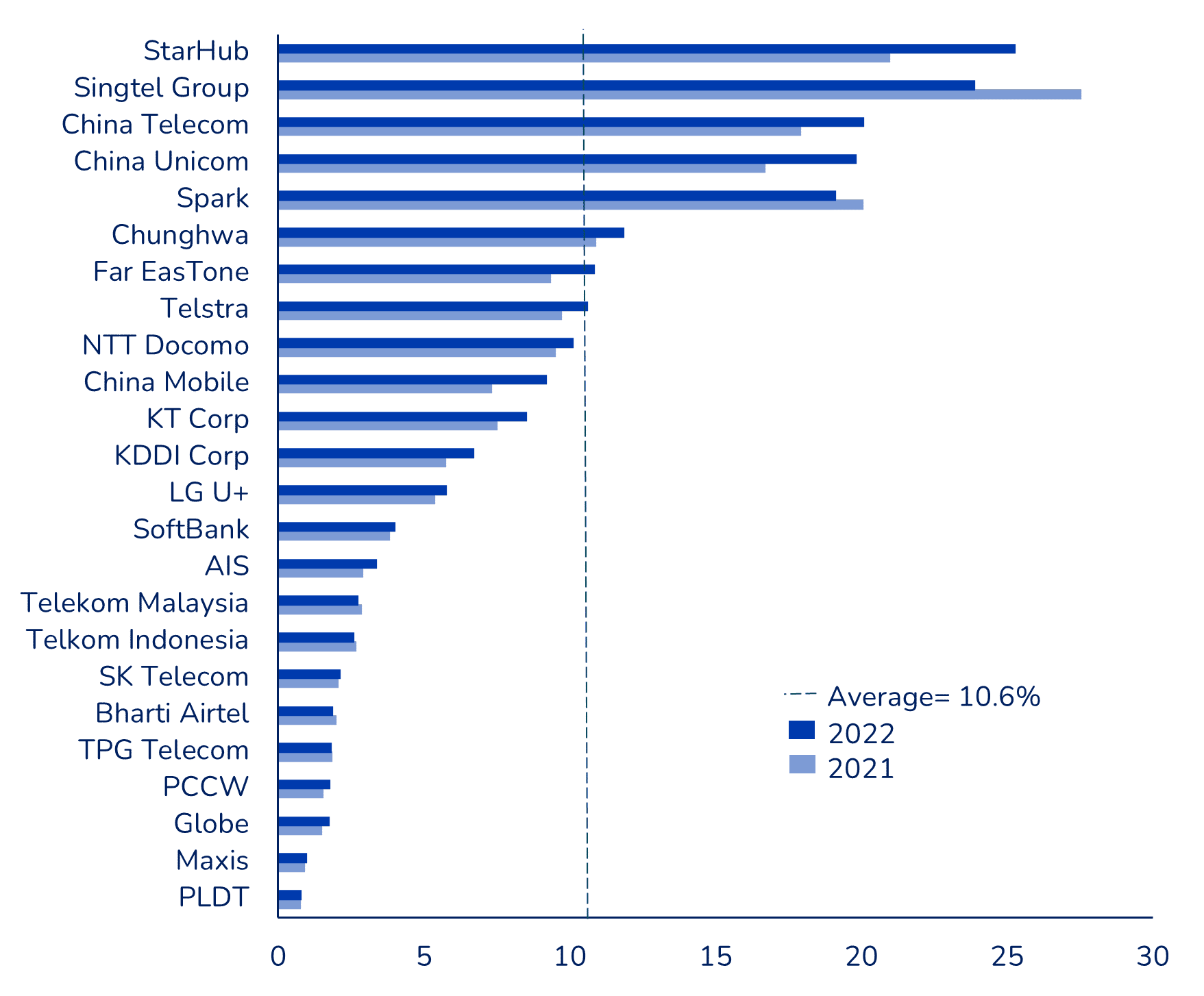

- Telcos have been steadily growing their enterprise non-connectivity business. This encompasses segments such as cloud, managed services and cybersecurity, is witnessing rapid growth of 20.8 percent, accounting for 10.6 percent of total revenues in 2022.

- Interestingly, enterprise non-connectivity revenues accounted for 53.8 percent of total enterprise revenues in 2022 up from 49.8 percent in 2021. Exhibit 2 shows the contribution of enterprise non-connectivity business to the total telco revenues.

Exhibit 2

Enterprise non-connectivity revenue to total revenue, 2022 (%)

Methodology, key terminologies, assumptions and limitations of the research

Scope of analysis: We studied 40 telcos across 16 Asia Pacific countries. The countries were selected based on their economic significance and the availability of reliable data. 23 out of the 40 telcos had made progress in establishing and reporting their enterprise business revenues.

Segmentation and definitions: Enterprise is defined as services provided to the business customers (large, mid and small businesses). It excludes all the B2C revenues. For the purposes of the analysis, the telco enterprise business segments have been defined as follows:

- Total enterprise (connectivity+ non-connectivity): Includes voice, fixed-line, data communications (including leased lines, IP-VPN, SD-WAN, etc) provided explicitly to enterprise customers. It also includes beyond connectivity services like managed services, IoT, etc, provided to businesses.

- Enterprise non-connectivity: This is defined as beyond core connectivity services provided to the enterprise customers. It mainly comprises of cloud, managed services (collaboration, contact centers, other IT services and applications), IoT, cyber-security, etc. Excludes all the connectivity solutions provided to business customers

Revenue breakdown and peer comparisons: Our analysis primarily focused on understanding the contribution of enterprise business to total revenues. Further we conducted a detailed peer comparison of the telcos in our analysis. This enabled us to identify industry leaders and best practices

Limitations: The data collected may be subject to reporting discrepancies, and the analysis is based on publicly available information.

The following segment delves into the strategies and best practices implemented by some of the leading telcos China Mobile, M1, Singtel and StarHub to capitalize on the growing enterprise market.

#1 China Mobile: Pioneering revenue growth and innovation in the enterprise market

China Mobile stands out among the 40 telcos we analysed with its largest enterprise operations, generating an impressive revenue of US$ 25.2 billion (17.9 percent of total revenues). It achieved an exceptional double-digit growth rate of 22.6 percent in this segment, highlighting its robust performance despite its already substantial scale. Let’s delve into some noteworthy highlights from its operations.

Building the “Two New Elements”:

- New information infrastructure- the key components include 5G, CFN (cloud, fiber, and network) and Capability Middle Platform

- New information service system- integrates connectivity, computing force and capability

The Capability Platform:

Utilizing artificial intelligence, blockchain, and precise positioning, China Mobile’s Capability Middle Platform offers a range of general capabilities applicable both internally and externally. This one-stop-shop for digital intelligence empowerment supports their broader goals of cloud migration, digitalization, and intelligent transformation across society.

Research, development and innovation:

China Mobile demonstrates a strong commitment in this area, investing US$ 3.2 billion in R&D, up 17 percent YoY in 2022. It has bolstered its strategic technological capabilities by aligning with the national innovation system, gaining approval from the Ministry of Science and Technology to build the “National Open Innovation Platform for Smart Network New Generation Artificial Intelligence.”

Open collaboration:

The telco places great emphasis on collaboration for mutual benefit, establishing strategic partnerships with local governments, public institutions, and enterprises. Through cross-disciplinary collaboration, they drive the industrialization of digital technology, digital transformation, and information services, thereby supporting the development of the digital economy.

Understanding China Mobile’s business and success in the enterprise market

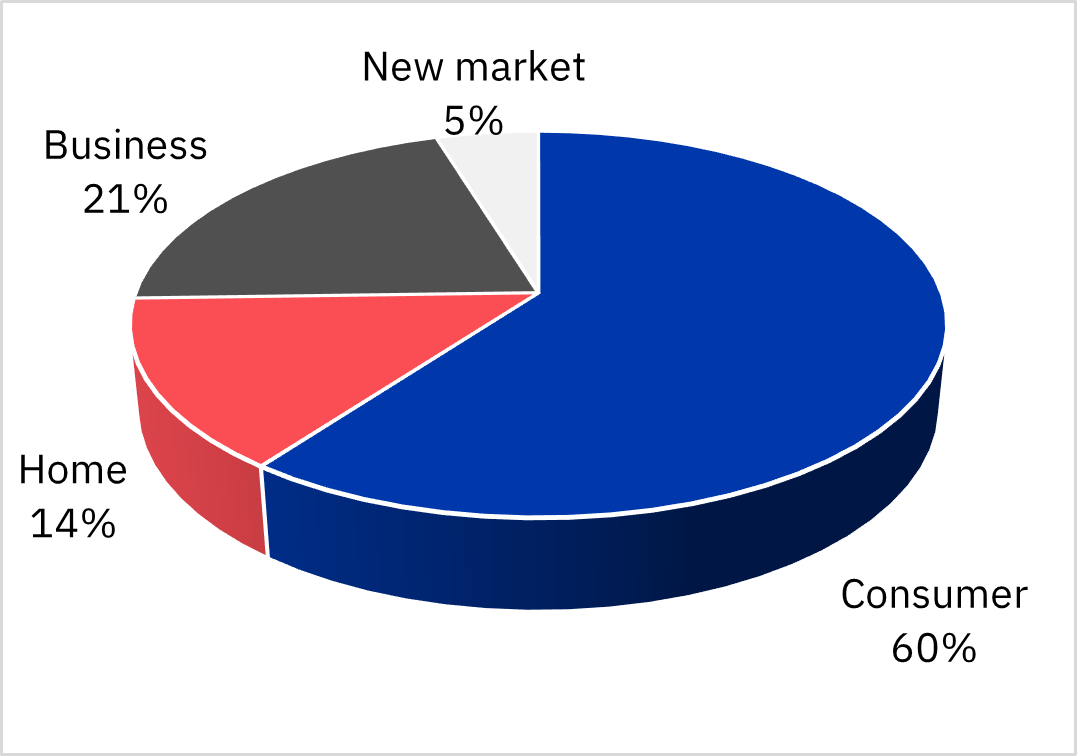

China Mobile classifies its business into Consumer, Home, Business, and New (CHBN) segments. Exhibit 3 illustrates the spilt of the service revenue in 2022 into these four segments.

Each segment has an impressive product ecosystem. The “New market” stands out as the fastest-growing sector, poised for tremendous success in the near future. This segment encompasses promising areas such as financial technology, digital content, and equity investments.

Exhibit 3

Break up of total service revenue, China Mobile, 2022 (US$ 121.8 billion)

New market: refers to segments such as financial technology, digital content and equity investments;

Home: includes broadband and smart home solutions.

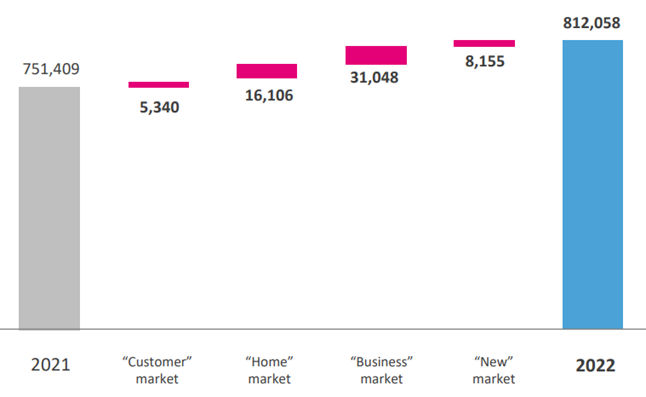

For the purpose of this analysis, our focus will be on China Mobile’s enterprise business segment. Notably, the investor presentation reveals that the largest portion of growth stems from the business market.

Exhibit 4

Growth by business segment, China Mobile

Source: China Mobile

Within the enterprise business, there are diverse components contributing to revenue. To provide a clearer understanding, exhibit 5 highlights the revenues for the major business segments within the enterprise business.

Exhibit 5

Revenue for major product segments, China Mobile, 2022

| Business segments | Revenue US$ billion 2022 | % growth YoY |

| Mobile Cloud | 7.5 | 108.1 |

| Value of 5G projects | 5.5 | n/a |

| IDC | 3.8 | 17.2 |

| Digital government projects | 3.0 | n/a |

| ICT | 2.9 | 33.7 |

| IoT | 2.3 | 35.5 |

| Big data | 0.5 | 96.1 |

| CDN | 0.4 | 11.2 |

| 5G dedicated network | 0.4 | 107.4 |

There is a substantial contribution from cloud and 5G projects. This trend is not unique to China Mobile; other Chinese telcos have also made significant strides in the cloud business, demonstrating their strong presence and progress in this area.

#2 M1 strengthens enterprise business with growth of 33 percent

M1 has strengthened its enterprise business proposition in the last 24 months and registered an impressive growth of 33 percent for this division. It benefits by being part of the Keppel group which enables it to drive early adoption for innovative applications across its diverse industry businesses.

Innovation in the 5G space:

- Has conducted over 15 5G use cases and partnerships.

- Notable achievements include deploying Singapore’s first autonomous vessel operations with Keppel Offshore & Marine and introducing a 5G AR/VR Smart Glasses solution for enhanced workplace safety.

Collaboration and public initiatives:

- Actively collaborates with government bodies such as the Infocomm Media Development Authority (IMDA) and the Maritime and Port Authority of Singapore (MPA).

- Established Singapore’s 5G@SEA, the world’s largest public 5G Maritime testbed, enabling the testing, innovation, and commercialization of 5G use cases in the maritime sector.

- Additionally, M1’s partnerships with Gardens by the Bay and the National Heritage Board provide 5G connectivity and immersive experiences at indoor venues and museums.

#3 Singtel’s enterprise business grows 4.8 percent (excluding Amobee divestment)

- Singtel’s enterprise contribution to total revenues dropped from 41 percent in 2021 to 38.5 percent in 2022.

- Total revenue and enterprise revenue saw a YoY decline of 5.1 percent and 11.1 percent respectively in 2022.

- This decline was primarily due to the sale of Amobee, Singtel’s digital marketing unit.

Strategic reset and Amobee Sale:

- Amobee is a prominent demand-side platform (DSP) serving advertisers and agencies.

- Financial figures for FY 2021 & 2022 reflected weakness in Amobee’s performance.

- Amobee was classified as a subsidiary held for sale in March 2022 and ceased to be consolidated from April 2022.

- The sale to Tremor International was completed in September 2022 for US $239 million.

- Singtel aims for optimal resource allocation towards new growth drivers.

Organic revenue Comparison:

- Excluding Amobee’s revenue, Singtel’s overall revenue and enterprise revenue would increase by 1.4 and 4.8 percent YoY respectively.

Enterprise leadership intact:

- Singtel maintains leadership in the enterprise segment, with enterprise revenues contributing 38.5 percent to the total.

- It remains bullish about enterprise services, especially with the advent of 5G. Here are some concrete initiatives taken in the year.

- Announced that it is set to launch Microsoft Azure Edge Zones integrated with its 5G network, providing MEC for Asian enterprises. This will further empower developers to deploy and oversee mission critical applications

- Formed a strategic partnership with Telkom and Medco Power for its inaugural data centre project in Indonesia. This is the third market for Singtel as it expands its regional data centre strategy.

Innovation and consumer application:

- It increased investments in Innov8, its corporate venture arm, by an additional US$100 million, bringing the total commitment to US$350 million. Innov8 focuses on funding start-ups aligned with Singtel Group’s interests in 5G, AI, digital economy, sustainability, cybersecurity, and emerging technologies.

- SK Telecom and Singtel signed MOU to collaborate on metaverse business growth, beginning in Singapore and then expanding to country where the group operates. Singtel will share its 5G and tech expertise across the region, while SKT will contribute insights from its metaverse platform (ifland) and related technologies

#4 Consolidation of JOS helps strengthen StarHub’s enterprise porfiolio

StarHub’s acquisition of HKBN JOS:

- StarHub acquired a 60 percent stake in HKBN JOS- Singapore & Malaysia for US$ 10.7 million

- The objective is to establish leadership as a system integrator and solutions provider

JOS SG and JOS MY expertise:

- JOS SG and JOS MY have a successful track record of over 30 years in the ICT market

- They serve nearly 1,500 government entities and blue-chip companies across industries

- Specialization in end-user computing, IT maintenance, IT infrastructure support services, and digital/cloud transformation solutions.

Enterprise business growth and contributors:

- StarHub’s enterprise business accounts for 37.2 percent of its total revenue (US$ 640 million).

- The segment growth of 22.6 percent YoY in 2022 is largely attributed to the consolidation of JOS SG and JOS MY under Regional ICT Services.

- Higher revenues from Network Solutions, including MyRepublic Broadband (US$ 9.6 million), and increased revenue from Cybersecurity Services also contributed to the growth.

Organic revenue growth:

- Excluding contributions from JOS SG, JOS MY, and MyRepublic Broadband, the enterprise service revenue would have grown by 3.8 percent YoY.

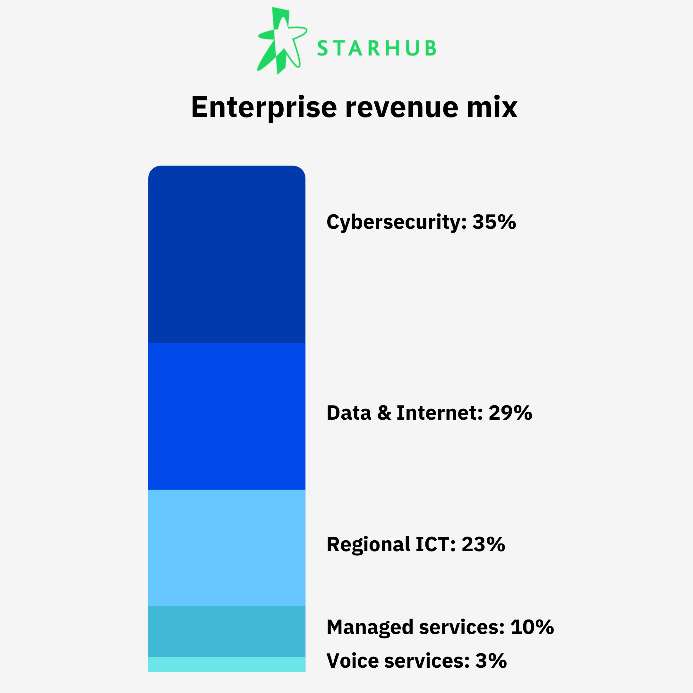

Exhibit 6

StarHub enterprise revenue by service type, 2022

Enjoyed the read? We are sure you will like this Top 10 Asia Pacific telcos to ace non-connectivity revenues in 2023

Explore our content on telecoms