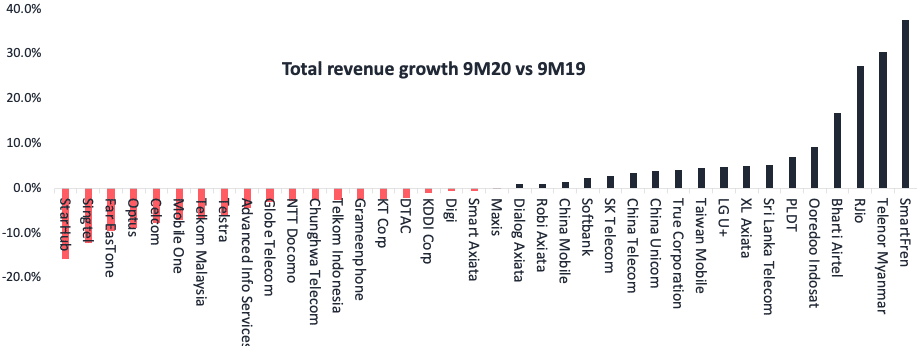

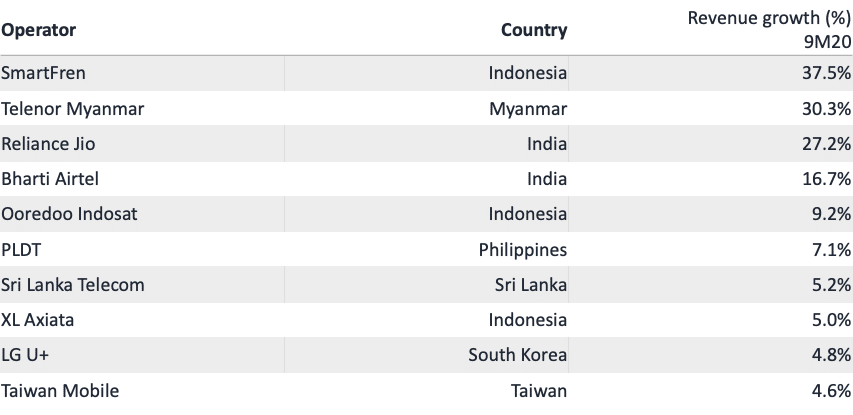

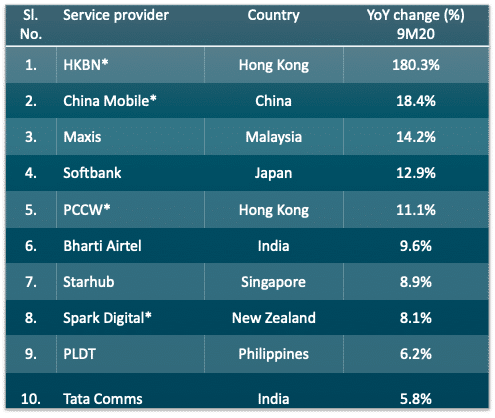

A handful of telcos performed well

Where some operators noted strong revenue growth during the first three quarters of 2020 (9M20), only 50% of the service providers maintained that positive revenue growth. Well penetrated South East Asian and developed markets faced additional challenges with travel restrictions impacting revenues from roaming services. Operators also noted loss of income from device sales.

Lack of fixed infrastructure in emerging Asia benefited mobile operators

Operators in emerging markets perhaps noted better growth in revenues. As mobile broadband stepped in to fill the gap left by lacking fixed broadband infrastructure, challenger operators from Indonesia including SmartFren, Ooredoo Indosat, and XL Axiata capitalized on the change. In terms of absolute net increase in revenue, China and India dominated. Operators in these two markets added over $6bn in revenues during the first 9 months of 2020.

- Service providers 9M20 revenues increased about 1% YoY for the period that ended September 2020. The growth was driven by India and China.

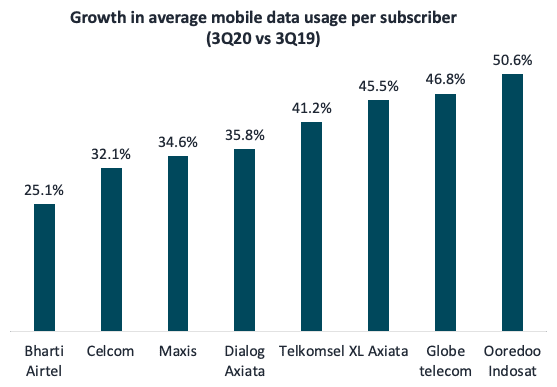

Appetite for data with expanded choice on digital services

Operators across multiple Asian markets witnessed an increase in mobile data usage, setting long-term demand trends, including but not limited to remote working, online schooling, and an accelerated shift towards digital lifestyles. This increase in data appetite was complemented by a range of promotional offers from service providers.

- Many operators across developing and developed Asia launched unlimited data packages, although most were with FUP.

- There were more choices available in terms of access to over-the-top services. The trend was supported by specific needs of various service users.

- By offering more choices, service providers strengthened their ability to quickly introduce service variants and capabilities for on-boarding partners.

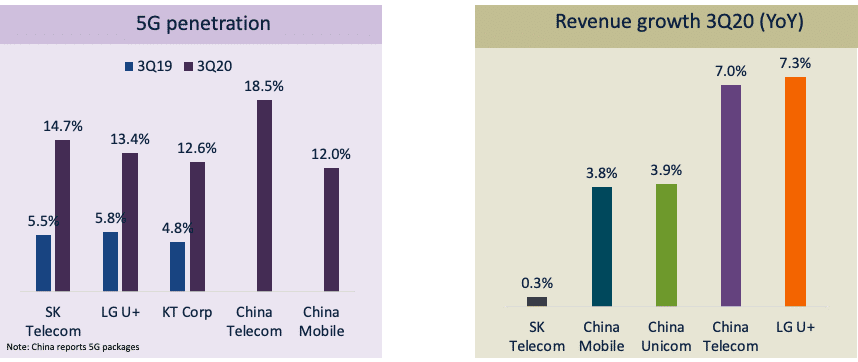

5G momentum continued, early signs to monetization showed up

According to GSA, 59 operators across 31 Asian markets are investing in 5G technology. Of these, 24 operators from 12 markets have already launched 5G for commercial use. These markets include China, South Korea, Japan, Hong Kong, Taiwan, the Philippines, Thailand, Singapore, New Zealand, Australia, and some pacific Islands. In December 2020, Vietnam was the most recent to launch commercial trials with state-owned Viettel.

Both China and South Korea continued to expand 5G coverage. The countries first made 5G available in 2019 and have shown promising uptake. Operator 5G success is associated with minor pricing differential in the existing 4G plans, along the introduction of premium unlimited data packages bundled with relevant 5G services. Service providers in these markets retained focus on developing ecosystems for both devices (5G handset, AR & VR devices) and related services such as cloud gaming, AR & VR based applications, and immersive content.

- Operator revenue growth benefited from an increasing shift toward 5G services.

Digital transformation continued; operator introduced digital sub-brands

Past quarters have highlighted significant digital transformations undertaken by regional telcos. However, readying telcos to catch up with digital natives demands a complete overhaul of their existing technology stacks, processes, and skills. Where we noted service providers continuing with one-off projects, major transformation did come in the form of launching digital-only brands. The initiatives are driven by two key factors. While competition is a given, more important is the opportunity to engage with the next generation of customers in ways more relevant to them.

Telco growth is pivoting to B2B

As growth from consumer segment slows, telcos have started building focus on improving their capabilities to serve the enterprise segment. For many, B2B business arm has delivered better growth, augmenting the performance by telcos. Even in the B2B space, connectivity revenues continued to remain under pressure. The new growth is driven by an increasing push for positioning telcos as system integrators and making them more ICT centric.

- Acquisitions are becoming more relevant. In 2020, service providers grew inorganically and made several acquisitions to strengthen B2B capabilities.

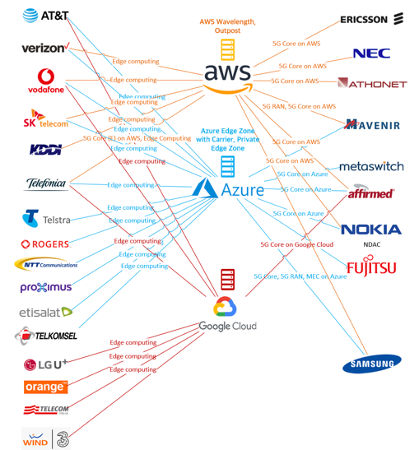

While hyperscalers ramped up, service providers also gained

COVID-19 has been a driving force for many enterprises in moving their workloads to the cloud and speeding up their respective digital transformation. Where hyperscalers benefitted most from the accelerated push for cloud adoption, service providers also gained as they augmented hyperscalers’ main cloud with their edge capabilities.

Many new B2B use cases in retail, manufacturing, and transportation will emerge with edge computing. For example, manufacturers can run AI-based visual inspections directly though 5G-enabled devices where the core computing task is executed at the edge.

In the next article, we are discussing Key issues & challenges that shaped telcos in 2020.