Welcome to Telecom Digital Odyssey

The APAC telecom market is at a pivotal crossroads, driven by a confluence of financial, technological, and competitive forces that are reshaping the industry. The “Telecom Digital Odyssey” report offers a deep dive into these shifts, providing critical insights into the performance of telecom operators across the region.

From key financial trends to advancements in digital infrastructure and network capabilities, this report dissects how leading APAC telcos are navigating the complex challenges of the digital age. It highlights the strategic initiatives, investments, and innovations that are shaping the future of connectivity in APAC.

Key highlights

#1 Industry revenue growth experiences structural slowdown

Industry revenue growth deaccelerates to 3.1% (average) YoY in FY-2024 from 7.1% YoY in Q1-2023, signaling a significant market shift. Developing countries continue the strong growth driven by increased data consumption.

- Growth drivers include 5G network expansion, subscriber base evolution, strategic pricing optimization, M&A synergies, and enterprise segment acceleration.

- Telcos in India and Pakistan continued to maintain revenue growth momentum in 9M-2024, while Chinese telcos experience moderated growth trajectories.

- DITO emerges as growth leader with 47.2% YoY expansion in 9M-2024, reaching revenue of USD 209 million.

- China Mobile maintains market leadership, adding highest USD 2.2 billion in net revenue (2% YoY) to reach USD 110 billion total revenue in 9M-2024.

- VEON group companies leverage digital and data services as key revenue catalysts.

- Indian telcos drive growth through combination of strategic pricing initiatives and subscriber base expansion.

- Mature markets show divergent patterns. Japanese, Korean, and Australian telcos report muted growth, while Singaporean operators face revenue contraction.

#2 Telcos in the APAC region demonstrate varied ARPU momentum

Emerging markets (India, Indonesia, Philippines) demonstrate ARPU resilience, outperforming developed markets through increased data adoption and digital services.

- Average ARPU maintains stability at approximately USD 10.8 in Q3-2024.

- Developed market telcos face marginal ARPU contraction due to heightened competitive dynamics.

- Emerging markets such as India, Indonesia, and the Philippines registered ARPU growth.

- VEON Group’s telcos in Pakistan and Bangladesh leverage increased 4G and digital service adoption to bolster ARPU.

- Intense competition drives downward pressure on ARPU in China.

#3 EBITDA margin stabilizes through systematic transformation

Telcos maintain ~30% margins in 2024 through operational excellence initiatives, digital transformation, and infrastructure optimization.

- EBITDA margins for telcos consistently maintained a range of 29%-34%, demonstrating stable financial performance, with median EBITDA margin of 32.9% since FY-2023.

- APAC telcos have achieved stable and robust EBITDA momentum, underpinned by rigorous cost control measures and operational efficiency programs.

- Increased top-line revenue for many telecom operators further underpinned EBITDA momentum and its consistency.

- Around 22% of telcos in the Asia-Pacific region achieved double-digit YoY EBITDA growth for the first nine months of 2024.

- Grameenphone maintained industry leadership with an EBITDA margin of 60.1% for the first nine months of 2024, demonstrating superior financial leverage.

#4 Enterprise and Beyond-connectivity drives next growth horizon

Telcos continue to pivot toward B2B and digital services, the contribution from which is estimated to reach ~30% and ~40% respectively of total revenue by 2028, marking a strategic shift from traditional telco models.

- Average enterprise revenue contribution reached 23% of total telecom revenue in 9M-2024, up from 21.7% in the same period of 2023, underscoring its growing importance.

- Telco enterprise segment revenue climbed to an estimated USD 94.3 billion, achieving an 8.8% YoY in 9M-2024.

- Projected enterprise segment revenue contribution to overall telcos’ revenue will expand from 23.8% in 2024 to 30.5% by 2028, indicating a robust contribution trajectory.

- Average “Beyond Connectivity” revenue for the 23 telecom companies analyzed enhanced their cumulative total revenue share to 25.3% in 9M-2024, up from 23.6% in the same period of 2023.

- “Beyond Connectivity” services increasingly fuel telecom industry revenue and is growing more faster than the industry average.

- Estimated “Beyond Connectivity” revenue contribution to overall revenue will achieve approximately 39.6% by 2028.

- Strategic focus on non-traditional areas, including Cloud, Security, and Digital transformation services, propels non-connectivity revenue.

#5 5G monetization faces market-specific challenges

While China, India, and Thailand led 5G subscriber growth, price competition and use case development remain critical hurdles for sustainable 5G monetization.

- Network coverage expansion, increased adoption of 5G, enhanced affordability of devices, and strategic promotional offers propel the expansion of the 5G subscriber base.

- APAC 5G subscriber count is expected to surpass 2.7 billion by 2028, growing at a CAGR of around 10% from 2024-2028.

- Overall 5G subscriber penetration is estimated to reach 30% by 2028.

- Developed markets like Australia, South Korea, Japan, China and Singapore to surpass 70% penetration by 2028.

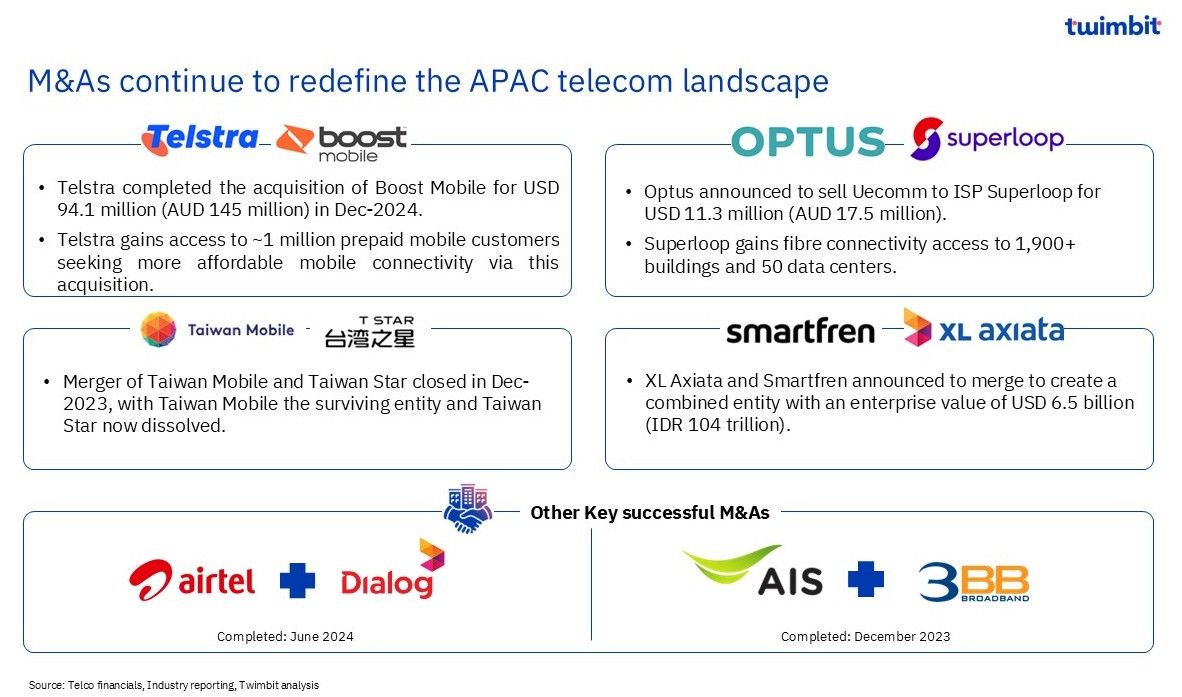

#6 M&As reshape the competitive landscape

The consolidation wave gains momentum with regulators also recognizing the need to support growth and investments in digital infrastructure.

- M&A activity continue to rise indicating industry consolidation to continue and redefine the APAC telecom landscape

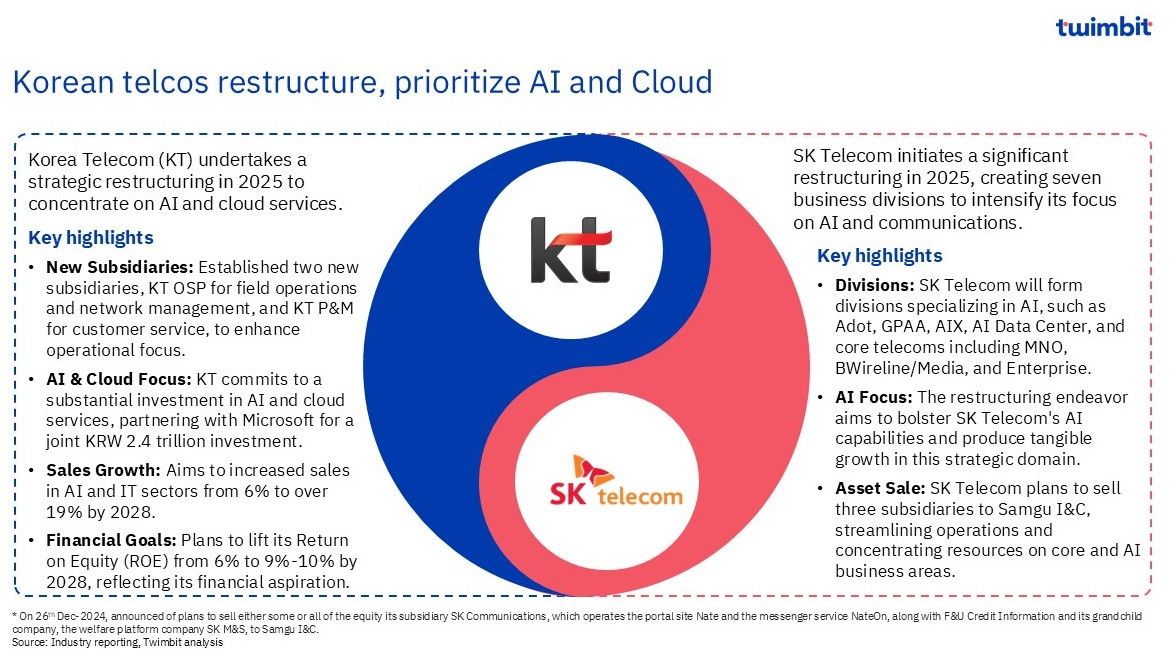

#7 AI becoming integral to telecom operations

AI adoption accelerates across telco value chain, with South Korean telcos leading APAC in AI/cloud integration for operational excellence and revenue growth.

- AI becomes the core of modern telecom operations, with adoption across various use cases including Network Optimisation, Energy Efficiency, Spam and Fraud Detection, AI-Powered Customer Service, Retail and Promotions, Security and Risk Management, IoT and Smart Cities, Content Personalization

#8 APAC telcos bolster cybersecurity defense

Telcos continue to enhance security posture through AI-powered solutions, strategic partnerships, and targeted investments in security centers, prioritizing network resilience and data protection.

- In June 2024, Singtel swiftly detected and eradicated malware associated with Chinese state-sponsored Volt Typhoon, underscoring robust cybersecurity measures.

- Singtel discovered the breach following the detection of suspicious traffic and sophisticated malware on a core router, demonstrating vigilant network monitoring. By promptly addressing the malware, Singtel ensured no data exfiltration occurred, maintaining service integrity and reinforcing customer trust.

- In January 2025, NTT Docomo encountered a distributed denial-of-service (DDoS) attack, resulting in website failure and temporary service disruption.

- The DDoS attack triggered a system glitch at 5:27 am, impairing access to the company website and ‘goo’ portal for nearly 12 hours, though mobile and communication services remained operational. Customers faced challenges with the ‘d payment’ mobile money service due to network congestion caused by the overwhelming traffic directed at NTT Docomo’s servers.

#9 AI provides opportunity for growth in data centre business

APAC telcos leverage cloud infrastructure and data centers as strategic assets, enabling AI-driven innovation and new digital service capabilities.

- Mainland China, Japan, India, Australia, Singapore, and South Korea command over 80% of the region’s data center capacity, with Hong Kong and Malaysia emerging as close contenders.

- Japan, India, and Australia are poised for robust expansion, driven by escalated investments from cloud providers and colocation players.

- Leading providers prioritize policy initiatives, leverage targeted incentives, and implement energy efficiency and carbon footprint reduction through innovative technologies.

#10 Tech innovations will unlock future growth

Telcos pursue next-generation technologies (APIs, RAN, Quantum, Satellite) through ecosystem partnerships, creating new value pools beyond traditional connectivity.

GSMA Open Gateway drives Network APIs adoption by Asian telcos

- Bridge Alliance’s API Exchange (BAEx), supported by 13 Asia-Pacific operators, simplifies API deployment and fosters regional digital innovation through collaboration.

- APAC telcos Bharti Airtel, Reliance Jio, and Singtel joined a global initiative to advance network APIs, enabling developers to leverage enhanced network features and drive sector-wide digital transformation.

APAC telcos accelerate Open RAN adoption for 5G and future-proof networks

- Open RAN adoption is accelerating among APAC telecom operators aiming for flexible, cost-effective, and future-ready networks, driving innovation and efficiency.

- Increased investment in 5G network deployment, alongside demand for high-speed and low-latency connectivity, propels telco investments in Open RAN solutions.

- The Asia-Pacific Open RAN market is projected to exceed USD 500 million by FY-2024, with anticipated highest growth over the next five years until 2030, highlighting robust market potential.

Asian Telcos drive Quantum Tech adoption and innovation

- The United Nations designated 2025 as the International Year of Quantum Science and Technology, highlighting global advancements in quantum technologies.

- Singapore, China, and Japan lead efforts in quantum-safe communication, post-quantum cryptography, and quantum-driven optimization for diverse sectors.

- The Indian government committed USD 730 million to establish itself as a global quantum powerhouse by 2031, driven by the National Quantum Mission aiming to develop scalable quantum computers within eight years.

Satellite Internet expands in Asia-Pacific through strategic telco alliances

- The entry of players like SpaceX’s Starlink into the APAC market intensifies competition, with Starlink outperforming traditional providers like NBN’s Sky Muster in Australia in terms of speed and reliability, shifting consumer preferences.

- In India, the government’s administrative allocation of satellite spectrum paves the way for companies like Starlink to offer services, potentially sparking a price war with entrenched telecom operators such as Reliance Jio.

- Malaysia, Indonesia, and the Philippines plan to collaborate with Starlink to launch satellite-based internet services in 2025, positioning these countries to enhance connectivity infrastructure.

Click here for more contents on telecom

APAC Telecom Radar – Winter 2024