The Asian telecoms industry has responded well to the challenges presented by Covid-19. They have supported consumers with additional mobile data plans to enable increased consumption of the internet in home environments. The financial performance, however, has been impacted because of the weakening economy and financial impact on the livelihood of millions of consumers in the region. The majority of the operators have seen a decline in their quarterly and half-yearly performances. However, a few companies have bucked this trend and emerged stronger.

Top Performers (Q1 2020 vs. Q1 2019)

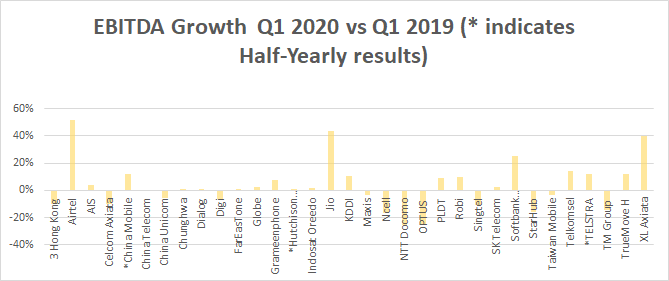

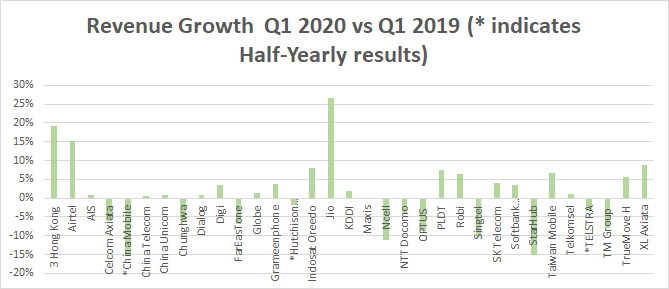

- Reliance JIO recorded an EBITDA growth of 42% and net profit growth of nearly 178% in its latest quarterly report. Tariff increases and net new addition of 17.5 million subscribers are the key drivers of the growth numbers. The company has seen investments from global investors who see JIO Platforms as a key player for long term growth in the Indian internet businesses. JIO Platforms is central to Reliance Group’s strategy to transform into a global technology powerhouse.

- Bharti Airtel recorded an EBITDA growth of over 50% owing to tariff increases and expanding the 4G customer base. 4G subscriber numbers have grown from 86 million in Mar 2019 to 136 million in Mar 2020. The company promoters have offloaded 2.75% of total equity to repay debt and strengthen the balance sheet.

- Axiata Group Bhd’s Indonesian subsidiary XL recorded strong revenue and EBITDA growth despite the challenges to the economy. Revenue grew by nearly 9% and EBITDA by 40% QoQ. EBITDA growth is driven by cost optimization and IFRS adjustments. The ARPU has seen a growth of 9.1% on the back of strong data monetization.

Major trends

The COVID-19 pandemic has transformed how businesses operate, and it is a key catalyst to the digital transformation agenda. While telecom companies will benefit significantly in the long term, it is not isolated from the challenges that are posed by the slowing economy and the impact on customers.

1. Declining Revenue & EBITDA (Q12020 vs. Q1 2019):

Both the top line and operating revenue saw some erosion for most telecom companies. The overwhelming majority of telcos have experienced negative or little revenue growth (-10% to 5% YoY). Consumers have seen a huge spike in the consumption of data. Telcos have played an important role and supported the customers by offering increased data allowances. They have not passed on the cost to the consumers of the increased consumption of data.

2. Rise In Data Demand:

There has been an increase in average data consumed per user across the Asia Pacific region. However, a large variation exists between countries. For instance, India recorded an approximate increase of 55%, Bangladesh 55%, Malaysia 20%, Indonesia 20%, and Sri Lanka 50% YoY. In Singapore, despite both postpaid and prepaid ARPU seeing a significant decline (19% and 15% in the case of Singtel), average smartphone data usage per user saw a nearly 50% YoY increase.

2. Roaming Revenue Loss:

The restriction on travel has impacted the roaming revenues. According to Rajan Matthews, director-general of the Cellular Operators Association of India, international roaming contribution to mobile service revenue could fall below 8%, if the crisis worsens. The standard contribution is around 12%, and last year it grew by 15% YoY. One of the worst-hit operators has been Singtel, which recorded a 36% fall in postpaid roaming revenue.

3. Rise In ARPU In India:

The Indian market has seen an increase in ARPU for the three major telecom companies Airtel, JIO, and Vodafone Idea Limited (Rs. 109). The primary reasons are tariff hikes and the rise in data consumption. For instance, Airtel recorded a 29% and 57% increase in overall data consumer base and 4G consumer base, respectively.

4. 5G:

The current crisis has, in many ways, demonstrated the appetite for data consumption. While the business case for 5G is not yet clear, many operators see the opportunity of the transformative impact it can have on their business.

- Thailand is gearing up to implement commercial 5G services this year. AIS is planning to invest over $1.2 Bn in 5G network expansion.

- Hong Kong, also recently saw the launch of commercial 5G services in April this year with multiple operators such as China Mobile, HKT, and Hutchison joining the party.

- In the Philippines, Globe has announced that it is going to continue with the network rollout. This is in line with Globe’s existing 5G strategy as it had already rolled out fixed-wireless 5G services last year.

- Singapore’s telecom authority, IMDA, has awarded Singtel and JVC (a joint venture between M1 and StarHub) as the winners of the 5G spectrum. The winners are expected to roll out standalone 5G networks by 2021.

However, other countries have had their progress impeded. In Malaysia, spectrum licenses were recently revoked, which could delay the rollout by one year. 5G spectrum auctions in India are likely to be delayed further to 2021 due to AGR disputes and the current pandemic.

5. Capital raising gathers momentum:

Telecom companies have rushed off the block to strengthen their balance sheets. Some of the examples are as follows:

- Telstra has issued 500 Mn Euros worth of bonds for general purposes, including pre-funding of future debt maturities. Moreover, it has monetized over A$ 1 Bn in assets that have resulted in a 12.1% decrease in fixed-costs during the half-yearly period. These cost reductions and efficiency building come as a part of building network capability in light of soon to be Vodafone-TPG merger. Vodafone, too would have to do some sort of capital raising as $6 Bn in debt would transfer to the parent level, leaving very little for network improvements.

- Reliance JIO has gone on a funding spree with many Big Tech companies as well as investment funds getting involved. The primary focus has been to reduce the net debt on its balance sheet aggressively to zero by March 2021. The following is the list of companies that have invested in JIO:

| Company | US$ Billion | % Stake |

| General Atlantic | 0.86 | 1.34% |

| Silver Lake Partners | 1.34 | 2.08% |

| 5.66 | 9.9% | |

| Vista Equity Partners | 1.48 | 2.32% |

| Mubdala | 1.2 | 1.85% |

| Total | 10.54 | 17.49% |

- Airtel promoters have sold 2.75% of the total stake in the company, chiefly, to reduce debt. One of the buyers was the French multinational bank Societe Generale, which acquired a 0.65% stake.

7. Global tech giants investment into telecom companies:

In what may be a defining trend for the coming years, we saw Facebook invest in Reliance JIO. There is considerable talk of Amazon investing in Airtel and Google investing in Vodafone-Idea. Currently, this trend is restricted mainly to India. Countries with a large population such as Indonesia are possible markets that could follow this trend in the near term.

8. Consolidation amongst telecom companies:

We are likely to see another wave of consolidation in the coming months:

- Axiata is in talks to buy a smaller Indonesian rival and is looking for similar opportunities in Malaysia and Sri Lanka as well. It already has a strong presence in both these countries.

- In Australia, Vodafone Hutchison is scheduled to finish its merger with TPG by mid-2020. This will give it a significant push to compete against Telstra.

Summary

The world was changed radically in this last quarter. There is a newfound wave of optimism on the growth opportunities and the role of telecom companies in the coming decade. They include the following:

- Opportunity to increase ARPU in medium to long term

- Attach rates for digital services for telecom companies are encouraging. Security, streaming, and gaming services are emerging as good potential growth drivers.

- Cloud services will get a boost, and telecom companies will strengthen their ability to leverage this both for their own digital transformation as well as support the journey of their customers.

- Enterprise business will be the key long term growth driver. Telecom companies need to be more ambitious in their effort to achieve a higher revenue contribution from growth with both large as well as small and medium businesses.

The economic downturn also presents an opportunity for telecom companies to attract a fresh set of talent, which will be important to develop a more agile growth development mindset.