Embracing open banking

Traditional banking operated within a closed system, where banks retained complete control over data and customer interactions. This approach limited the banks’ ability to explore revenue opportunity beyond loans and deposits.

In contrast, open banking offers a transformative solution by opening up banks’ data and services through APIs. This enables collaboration with third-party service providers, fintechs, and digital native companies, thereby offering a broader range of financial products and services. Banks are able to unlock new fee-based income opportunities beyond the conventional interest income model.

Open banking fosters a culture of agile innovation, that empowers banks to adapt quickly to changing customer demands and market trends. Collaborating with fintechs allows banks to capitalize on specialized technology, amplifying their offerings and maintaining competitiveness within the industry.

- Asian banks have between 300 to 3,000 APIs across product and service categories as of 2022

- Nearly 40% of banks embedded financial services in third-party marketplaces in 2022

- Embedded finance can lead to ~30% growth in new customer acquisitions in 2023

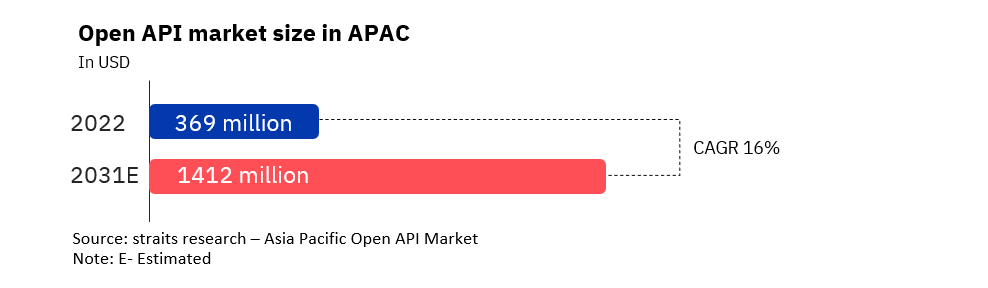

- Asia-Pacific’s Embedded Finance industry is expected to grow by 24.4% annually to reach USD 357,000 million in 2029

Top 5 countries driving Open Banking

- Australia:

Australia pioneers open banking, initiated with the CDR framework, mandating banks to share customer data securely upon their consent. Banks are offering API access to third-party service provider, promoting competition and innovative financial solutions.

- India:

Open banking practices phenomenally increased with the launch of UPI in India. RBI actively promotes the AA framework, enabling seamless integration of financial services with third-party providers to build personalised financial services.

- Singapore:

Singapore’s open banking practices are monitored by MAS guidelines. Banks progressively release APIs, facilitating collaborations with fintechs for enhanced services like payments, and wealth management.

- Thailand:

The Bank of Thailand introduced guidelines in 2019 to facilitate open banking implementation. Open APIs by banks are now enabling third-party service providers to create innovative financial solutions, boosting digital payments and customer experiences.

- Malaysia:

Open banking in Malaysia is primarily driven by market initiatives focusing on data privacy and security. Banks are driving fintech collaborations and API-based solutions, introducing convenient banking experiences.

The next wave

The current banking landscape is witnessing a substantial surge in open banking, characterised by a rising need for comprehensive, customer-focused digital platforms that seamlessly combine financial and non-financial services.

Open banking proves to be a potent instrument for developing innovative financial services and enhancing the overall customer journey. It has unlocked various prospects for banks, such as BNPL (Buy Now, Pay Later), marketplace solutions, data monetization, SUPERAPPs, and Banking-as-a-Service (BaaS).

BaaS stands out as a notable player within the framework of open banking. This service empowers banks, financial institution, and fintechs to extend their services and products to other financial and non-financial businesses It has led to the exploration of new revenue streams and technological capabilities.

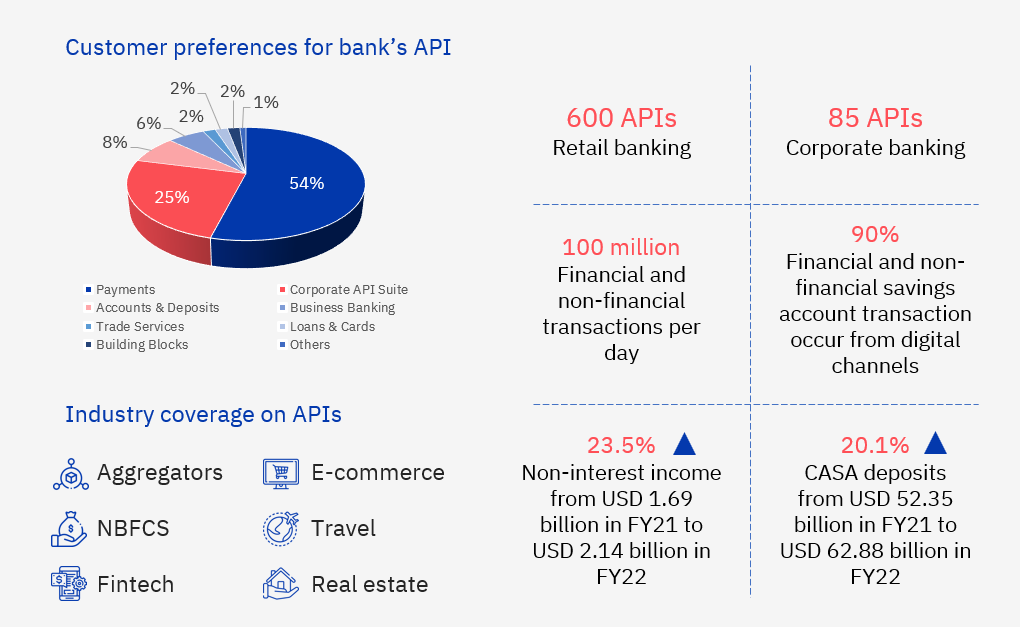

In the dynamic Asia-Pacific (APAC) banking landscape, BaaS now contributes to fee-based income among banks who are actively building developer-focused API stacks. Fee income acts as a pivotal measure of growth and financial robustness beyond traditional interest income. APAC banks witnessed an impressive CAGR of 5% in their fee income from 2018 – 2022. Notably, Singapore and India have outperformed the industry norm, boasting remarkable CAGRs of 12.11% and 11.05%, respectively (figure below).

As open banking continues to reshape the financial sector, these CAGR figures highlight the region’s proactive approach towards embracing innovation and enhancing financial resilience.

The power of fee-based income

BaaS growth opportunities

- BaaS is expected to grow customer base for banks by 50% by 2024

- BaaS represents a USD 7 trillion opportunity by 2030

- As of 2022, more than 30% of customer transactions occur outside the bank’s platform

- Banks could cut costs by up to 30% with BaaS adoption.

- BaaS is projected to increase banks’ CASA by approximately 5% to 10% by 2024

- Banks leveraging BaaS can attain a CAC as low as USD 5 to 35 per customer, versus the traditional of USD 100 to USD 200 per customer

How is BaaS different from open banking?

| Open banking | BaaS | |

| Definition | Open banking is a data sharing mechanism between banks and third-party service providers that allows secure financial data access from the bank’s ecosystem via APIs. | BaaS model allows banks to provide their infrastructure and services to non-bank businesses to create new financial products and services via APIs. |

| Model | APIs do not permit third-parties to build banking services on top of them. | APIs empower third-parties to build customized banking services on top of existing ones, offering tailored solutions to their customers. |

| Example | PhonePe using AA framework within open banking, enabling customers to aggregate all their accounts in a single interface. Banks share only customer account data with PhonePe through APIs, maintaining control over their core banking functions. | Shopify integrates with Stripe using BaaS to provide easy payment setup for merchants on their websites. Stripe collaborates with Goldman Sachs, Evolve Bank & Trust, Citibank, and Barclays to offer Stripe Treasury. |

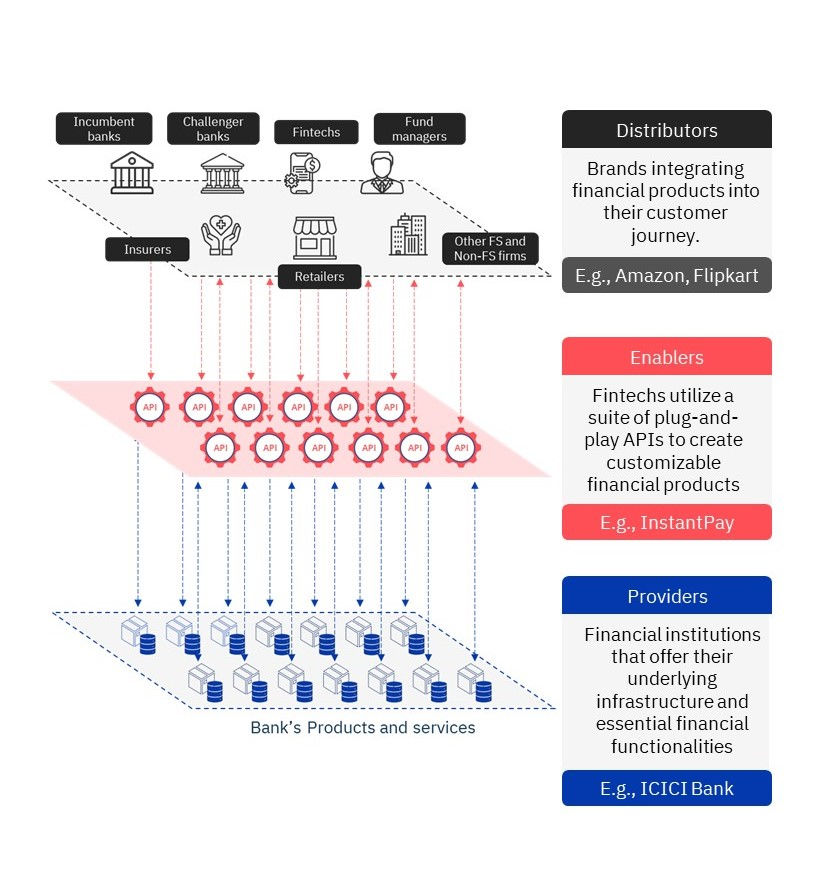

Building blocks of BaaS

BaaS provider

- Financial institutions or banks that possess banking licenses and provide core banking products and services via APIs to third-party service provider and non-banking businesses.

- BaaS providers adopt diverse strategies, influenced by their size and focus on specific use-cases or market segments.

- Larger BaaS providers often follow a dual approach, utilizing their existing relationships to collaborate with non-banking businesses and form partnerships with specialized fintechs.

- Smaller banks encounter difficulties in directly partnering with major non-banking businesses , which leads them to predominantly rely on collaborations with fintechs.

Providers have three preferred ways to monetize BaaS:

- Offer specialized solutions:

Provide products or services that are tailored to the specific needs of a particular customer or market, helping banks create a competitive advantage and deliver a better customer experience. - White label front‑to‑back customer journeys:

Process of providing a complete customer experience, from start to finish, using a white label solution, allowing banks to offer new products and services quickly and efficiently. - Secure access to a marketplace:

Gain access to a wider range of customers through third-party service providers and non-banking business, helping banks to reduce cost of customer acquisition and scale-up their services.

Distinctive capabilities of providers

- Data management: Handle data storage, retrieval, and management. They often provide databases, file storage, and other data-related services.

- Scalability: Offer scalable infrastructure and resources, allowing applications to handle varying workloads and user demands.

- Simplified integration: Allow fintechs to manage and customize their front-end experiences using pre-existing APIs, making implementation less complex.

- Security: Ensure the security of data and infrastructure, offering authentication, authorization, and other security features.

- Brand identity: Banks have a long history of trust with customers, as they ensure that the services are offered in a safe and secure manner.

Benefits for BaaS providers

- Broaden customer base: Leverage extensive customer base of non-banking businesses to up-sell and cross-sell their services

- Reduce customer acquisition cost: Significantly reduce the cost of customer acquisition and distribution by using distribution network of non-banking businesses

- New revenue streams: Generate new revenue streams by monetizing their existing financial capabilities by charging subscription fees, transaction fees or white-label fees

BaaS enablers

- BaaS Enablers are typically Fintech companies, harness APIs to craft unique and innovative solutions, meticulously designed to cater to the needs and preferences of end consumers.

- Enablers explore opportunities to collaborate with providers through API marketplace platforms.

- They contribute value by introducing innovative enhancements in banking products, including underwriting data, improving user experiences, and enhancing brand value.

- Enablers adopt an analytical approach to identify strategic opportunities for sustainable growth within the BaaS ecosystem.

Enablers need three key capabilities to monetize BaaS:

- A scalable, stable, and secure API marketplace to act as an intermediary between providers and non-banking businesses

- Offer ancillary professional services including billing, KYC, risk analytics and fraud protection for SME and Corporate banking use-cases

- System integration and digitisation support for non-banking businesses across various sectors.

Distinctive capabilities of enablers

- Streamlined integration: Existing integrations are made extendable to new use cases, enabling non-banking business to add new capabilities without significant re-work.

- Customisation: Personalizing traditional banking products and services that cater to specific industries or use cases.

- Comprehensive service range: Combining features from multiple providers and offering multiple product lines allowing non-banking business to rely on single sources

- Customer base & analytics: Enhancing success rates of customer acquisition and conversion campaigns by leveraging the existing customer base and robust analytics capabilities.

Benefits for BaaS enablers

- Speed to market: Leverage bank’s core financial capabilities directly and provide differentiating digital offerings in less time.

- Agility and reduce cost: Scale up effortlessly in functionalities and geographies by integrating banking functionalities without licensing or infrastructure investment.

- Better growth and returns: Create innovative products and solutions that can be offered to multiple industries and geographies leading to faster growth and better returns

BaaS distributor

These are non-banking businesses with large customer bases that can offer financial products to their customers as an extended service. Distributors embed the financial solutions into their customer journeys provided by technology companies.

Distributor propositions primarily focus on retail products, such as checking accounts and payments/credit cards for their customers. However, the growth potential of these products vary across different industries. For instance:

- Buy Now Pay Later (BNPL) services are expected to see higher adoption from e-commerce and fintech distributors.

- Core banking and virtual ledgers are projected to have more growth potential in the automotive sector.

- Foreign exchange (FX) services are likely to gain traction from healthcare and e-commerce distributors.

- SME lending shows promise for growth in healthcare, banking, and retail sectors.

- Cash management and treasury services are expected to flourish among banking and telecom distributors.

Distinctive capabilities of Distributor

- Hyper-personalisation: Offers personalised services to customer effectively addressing their previously unmet needs.

- Seamless integration: Integrates new propositions within the existing ecosystem by non-financial companies, introducing additional value-added features for customers and minimizing barriers to adoption.

- Regional expertise: Understands local markets and regulatory requirements, enabling them to offer localised solutions and support to customers .

- Market insights: Offer valuable market insights and trends based on interactions with enablers and customers, helping BaaS providers improve their offerings.

Benefits for BaaS distributors

- Hyper-personalisation: Provide a seamless experience to their customers without them realizing the switch between purchasing a product and doing a financial transaction

- Customer retention: Improve customer retention as the financial service offerings and capabilities drive the stickiness towards the product, also resulting in loyalty points for customers many reward offerings

- Ease of scale and integration: Integrate any required service through plug & play capabilities provided by Baas platforms, thereby reducing initial investment in building them as an overhead

Top 3 banks acing the BaaS model

- The bank has a suite of 600+ APIs

- An API banking portal for developers to build, test and integrate new APIs across banking product categories.

- ICICI Bank witnessed an increase in their fee income by 23.9%, from USD 1.54 billion in 2021 to USD 1.90 billion in 2022.

- The bank has a suite of 200+ APIs

- DBS API developer platform is well-positioned to embed services on partner platforms to acquire and distribute at scale.

- Net fee and commission income of DBS accounts to 18.73% of its total income which is USD 12.3 Billion

- The bank has a suite of 500 APIs

- Implemented a host of embedded finance solutions for the education, energy, government, and insurance sectors to streamline KYC and payments.

- Generated USD 1.9 billion from their fees and commission, which increased by 12% in 2022.

Case-in-point

ICICI Bank established an API ecosystem for core and SME banking

ICICI Bank is at the forefront of building a robust third-party API platform. The focus on BaaS has significantly transformed the banking landscape for ICICI Bank in the country.

The portal incorporates a detailed workflow for conveniently moving the API solution to the final production stage, thereby eliminating the hassles of manual to and fro.

6 steps to successfully implement BaaS

- 1. Customer-centric approach

Keep the end customers in mind while designing the BaaS offerings. Focus on delivering seamless and personalized experiences to enhance customer satisfaction for both partners and end-users.

- 2. Ensure regulatory compliance

Ensure compliance with all relevant financial regulations and data privacy laws. Collaborate closely with legal and compliance teams to navigate the regulatory landscape and address any potential challenges.

- 3. API design and development

Develop robust and well-documented APIs that are easy to integrate and use. Prioritize security to protect sensitive customer data and transactions, while adhering to industry-standard encryption and authentication protocols.

- 4. Infrastructure and scalability

Invest in a scalable and reliable infrastructure that can handle increased API traffic and ensure high availability. Consider cloud-based solutions that offer flexibility and scalability.

- 5. Partner onboarding and support

Establish a streamlined onboarding process for potential partners, making it easy for them to access and integrate the APIs. Offer comprehensive developer documentation, training, and support to assist partners during the integration process.

- 6. Continuous API performance monitoring

Track API usage, partner engagement, and customer feedback with comprehensive analytics. Monitor API performance for continuous improvement. Foster an innovative and flexible culture and adapt BaaS offerings based on feedback and market trends.