When Apple announced the launch of its first iPhone on 9th June 2007, nobody knew the extent to which big banks would have to alter their business models. Since then, the pervasiveness and the computational ability of smartphones have only increased.

This new technology has irrevocably transformed lifestyles, and with it has created new needs, and unique ways to address them. The first few people to see opportunities in the FinTech domain were Andrew Kortina and Iqram Magdon-Ismail. The duo found their problem statement when they realised they didn’t like the hasle of physical currency when transferring money. Thus, they started Venmo, a mobile payment service that allows its users to pay each other through its mobile app. They specifically targeted millennials, a motif that repeats itself in many other FinTech startups.

For instance, Robinhood allows its users to take part in trading without worrying about commission fees. This offering is wildly popular among millennials as they generally have lower savings and high debt. This financial constraint, however, is not indefinite. As this group gets older, their spending power would increase along with their savings. Moreover, when they transition through different phases in life, they would require the very same services their predecessors did, such as mortgage and investing for their 401k. Losing out on building loyalty within this group is a death knell for banks 20-30 years down the line. Therefore, they must build good relationships with millennials to survive. The question now remains on how to do it.

Why Digitize?

Millennials and Generation Z are also referred to as the smartphone generation for a reason. From dining and traveling to even paying someone or watching movies, a whole host of activities now rely on smartphones. Thus, Airbnb, Netflix, Swiggy, Paytm, Uber, etc., have become household names. In essence, leveraging digital technology has become one of the most effective ways to get closer to the ‘smartphone generation.’ Unfortunately, up until recently, there was hardly anything by banks that could compete with FinTech products. It is only now with apps such as Zelle and others that the big banks have been pushing back.

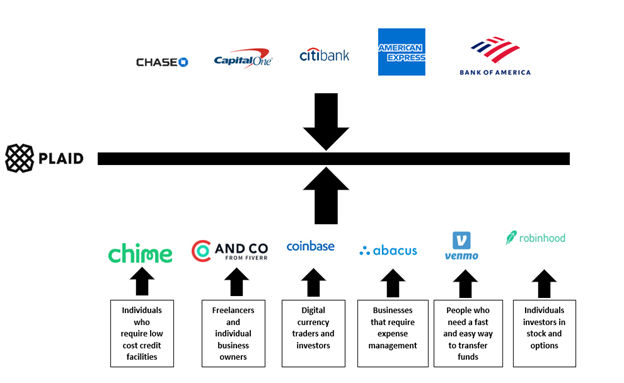

This necessity for digitization is true even in building process capability, both internal and collaborative. Let us take the example of Plaid, a California based startup. It identified that companies faced significant difficulties in aggregating bank accounts and solved it by building a unified banking API which was made available to its clients. Currently, Plaid has over 10,000 banks onboarded. However, had the banks realized the importance of digitization, they could have collaborated and had their version of Plaid with better compliance and offerings. But due to not investing in digital transformation on time, the associated opportunity cost has meant that banks are now losing out on avenues before they even discover them.

The above, however, is only a subset of indications that one can derive from witnessing the changes that the financial sector is undergoing. A more general list is given below:

FIVE KEY OBSERVATIONS

Capturing Millenials Is Vital

As Millennials today get older and enter the next phase of life, they will require a variety of financial services. These include traditional services such as retirement benefits, insurance, investments for their children’s educations, mortgage, credit to fund small business enterprises, etc. Banks have noticed this and are working on expanding the utility function they perform. The primary motivation has been to make these services cheaper and easy to understand with greater availability.

Information Arbitrage Makes Small Competitors Viable

Data collection and analysis have become critical, especially when it comes to delivering and improving service. For instance, if a creditworthy user faces difficulty in obtaining a loan, then he/she would simply shift to a much smaller competitor such as SoFi.

Threat From Big Tech

Banks are not the only ones looking at FinTech startups. Giants on the technology side have also developed a keen interest in their operations. For example, Plaid has venture investments not just from Goldman Sachs but also from Google.

Experts suggest that tech giants pose a far serious threat than FinTech startups. The banks already rely on Big Tech for services in cloud computing, client-facing AI, and Big Data to offer differentiation in their services. If these tech companies decided to enter the industry, then these big banks would face significant difficulties in upscaling their competitive advantage.

The current consensus is that it is only a matter of time before these companies start to make substantial inroads into the world of banking. Consequently, time and capability building has become a matter of survival.

Limitations on Inorganic Growth

Banking is highly regulated, and many big names in the industry cannot expand through M&A by buying other banks due to anti-trust laws. These regulations leave them with limited avenues to invest their funds. Many have found refuge in investments in small tech companies to build their internal capabilities.

The Need To Change Perspective And Business Model

Banking companies have been evolving in how they view themselves. Investment banks such as Goldman and JP Morgan Chase have decided to step into consumer banking to service smaller clients. Moreover, the heads of both these companies declare that they now view themselves not as banks but primarily as tech companies that are into banking.

Why Is It So Difficult For New Players To Enter Banking?

Now, just because FinTech has disrupted the financial sector, it does not mean that banking has become a level playing field. Incumbents enjoy advantages that are not necessarily related just with scale. In a study conducted by Accenture, 75% of people polled said they were cautious about sharing their data. However, 60% said they would be willing to share ‘significant personal information with banks.’

The above suggests that people are receptive enough to provide banks with information such as data about their location, lifestyle, and financials. However, in return, they expect lower prices, a relaxed and faster loan approval process, and personalized local offers.

This trust, however, is not replicated to the same extent in the case of FinTech startups.

Another aspect that limits potential competitors is burdensome banking regulations. Obtaining banking licenses are challenging, and the amount of regulatory requirements and government oversight is immense. Moreover, Basel III norms put stringent requirements on the bank’s capital assets. Even Big Tech players have avoided direct intrusion into the banking sector due to low-risk appetite for the very same reasons. Instead, they thus have taken to a more collaborative approach (e.g., Apple Card in collaboration with Goldman Sachs).

Two Ways Banks Are Responding To The Challenge

- Inorganic Growth – This method of growth refers to acquiring tech startups to build internal capability or to roll out a differentiated service.

- In-House Capability Building – Big banks spend a considerable amount on technology each year. For example, JP Morgan Chase spends $11 billion each year on tech alone. Moreover, it has 40,000 technologists and over 18,000 developers creating intellectual property for the bank. It spends a third of those $11 billion on investments and $2-$3 billion on cybersecurity.

Emerging Operating Models

With this kind of focus towards digital transformation and development of tech-oriented intellectual properties, a lot of these banks have sought to diversify into some combination of the following three models:

Banking As A Utility

The motivation here is to maximize the utilitarian function that banks already perform. The transformation of credit services is a good example. Over the past 40 years, public perception of credit services has shifted. In a 2018 survey of 1669 US credit card users conducted by AITE Group, 91% of Millenials regretted their credit card debt compared to 81% of Baby Boomers. However, surprisingly, they aren’t averse to credit card usage. 85% of them ranked low or zero annual fees as the most crucial factor in choosing a specific credit card.

An even greater surprise was that this was not much ahead of rewards and perks, which stood at 82%! Recognizing this as an opportunity, banks have poured an immense amount of money trying to woo this generation. For instance, JP Morgan Chase has released Chase Sapphire Reserve Card. The card’s success was substantiated when users started to use bonus points faster than the bank’s initial anticipation. Trying to emulate this success, Wells Fargo and American Express have come out with similar cards catering to different credit needs of millennials.

Credit, however, is not the only field that has witnessed the impact of digitization. Usage of Big Data has allowed banks to reduce their reliance on high-risk assets for better returns and thus can extend the same benefit to its shareholders. It is particularly true in the case of HFT (High-Frequency Trading). Many Investment Banks use algorithmic trading, which leverages large quantities of data and cutting edge AI to decide upon which trades to make. Moreover, these trades are carried out in large volumes within a fraction of a second. As such, trading has become the primary source of revenue for many IBs, such as Goldman Sachs far surpassing what they receive from their traditional roles.

Deep Expertise Banks

These refer to banks that have developed a high degree of specialization in servicing the specific needs of their customers. For instance, if a low-income US citizen needs a mortgage to pay for his/her house, Citi caters, particularly to their needs. Typically, low income corresponds to low down payment, which Citi has expertise in managing. Similarly, Wells Fargo calls itself “America’s leading small business lender,” and their track record substantiates it.

An important aspect that defines this expertise is how well these banks are able to securitize their assets and, thus, lower risk. To this end, Big Data, just as in trading, becomes critical in analyzing risk and mitigating losses to the bank.

Financial Supermarkets

This model seeks to widen the net as far as possible to reach as many potential customers as possible. In this, banks try to act as an aggregator of financial services from the general to the very specific. For instance, JPMC, apart from Sapphire Reserve Card, has also delved into its currency called JPM Coin, which is a dollar-backed cryptocurrency, apart from the traditional services it offers. Additionally, it has made its mobile trading platform called YouInvest. Other services include J.P. Morgan Access, Chase Connect, Corporate Quick Pay, and Corporate Quick Collect. The bank also has plans to launch a digital bank in the United Kingdom where open banking is taking root.

However, that’s not all. The company also offers services through its acquisitions such as WePay and InstaMed, the latter of which is a payment network utilized heavily in the healthcare sector. This strategy of leveraging capability through acquisition is highlighted by its CEO, Jamie Dimon, saying, “We are looking, and will be much more aggressive with acquisitions.”

In this regard, other banks are not far behind. Recently, Morgan Stanley struck a $13 billion deal to buy E-Trade. Even companies without much history of acquisitions have broken onto the scene with firms such as American Express purchasing LoungeBuddy and Pocket Concierge, which are into traveling and dining.

Now, the above examples highlight how banks can act as aggregators and offer in-house products. However, there is just as much legitimacy in collaborating with third parties and providing an array of services. For example, HDFC Bank’s mobile application allows the aggregation of merchants’ applications to enable users to transfer funds, shop, pay utility bills, book tickets, and recharge phones.

Conclusion

Technology offers multiple avenues for banks to grow and service their customers. Digitization, in particular, has emerged to be the critical investment area in this regard. Two questions now remain – ‘What are the pillars of this digitization effort?’, and ‘How can this effort be implemented in reality?’