The downloadable version of the report

Executive summary

- Telcos in Asia Pacific experienced an all-time high growth (in the last five years) of 6.4 percent in 2021. In 2022, the growth has now reached a new high of 6.7 percent YoY. Aggregate revenues of these telcos totalled a commendable US$ 597.5 billion in 2022!

- The telcos collectively added US$37.4 billion in new revenues in 2022, with 87 percent of them experiencing positive YoY revenue growth, and seven achieving double-digit growth.

- Dialog Axiata recorded the highest growth rate of 25.5 percent in 2022. China Mobile added the highest net new revenues yet again of US$ 13.3 billion YoY.

- The Indian market witnessed a cumulative YoY growth rate of 20 percent due to tariff improvements. Notably, Bharti Airtel and Reliance Jio recorded an impressive 22 percent increase, despite their large-scale operations.

- Earnings for the telcos grew at 3.9 percent YoY and the average EBITDA margin was 32.9 percent. Both Bharti Airtel and Reliance Jio record the highest change in EBITDA of 27.5 percent.

- Operational costs continue to grow as 36 percent of telcos report a decline in earnings (EBITDA). This is also partly impacted by the growing emphasis on new business segments such as enterprise which has lesser margins as compared to the dominant consumer business segment.

- Most Asian telcos continued to make steady progress in establishing their enterprise business and diversifying into adjacencies such as media, gaming, e-commerce and financial services. Enterprise business now accounts for 20 percent of total revenues for these telcos.

- Non-connectivity revenues grew from 18.4 percent of revenues to 20.2 percent of revenues. We forecast it to grow between 2 to 3 percentage points annually in net contribution and reach approximately 26 percent of revenues by 2025.

- The APAC region was an early adopter of 5G with commercial availability now across 11 countries. 5G subscriber numbers is estimated at 1.2 billion in 2022 and projected to reach 2.1 billion by 2025 (5G package subscribers considered for China).

- Conversations on private 5G network was the central theme at MWC Barcelona. Governments in the region are actively encouraging private 5G networks to facilitate various industry use cases.

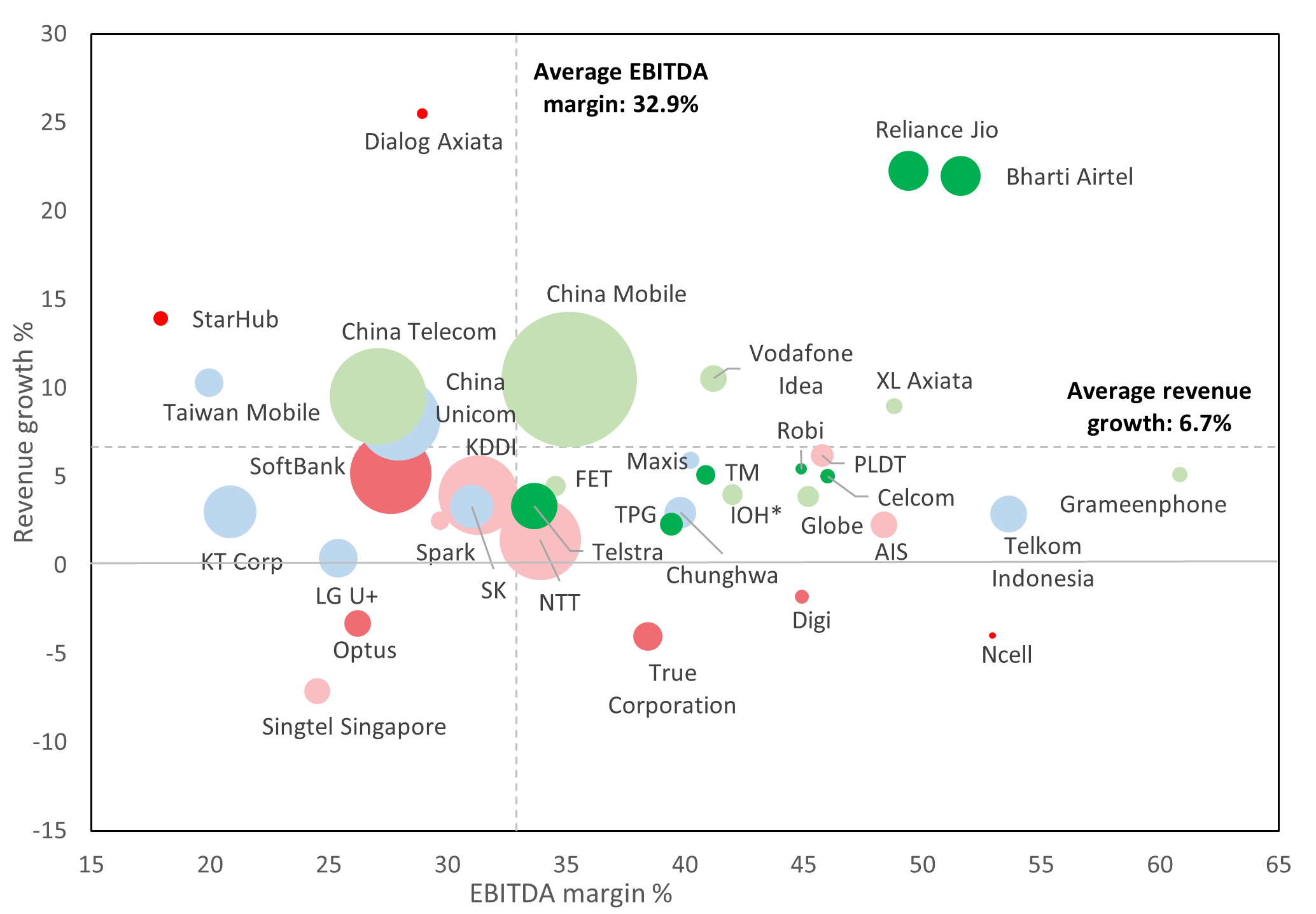

Exhibit 1 captures the relative performance of the 39 telcos across 4 measures, viz., revenue, revenue growth, EBITDA and EBITDA change.

Exhibit 1

APAC telcos benchmark FY 2022

Note: Size of the bubble represents the relative revenue for the telco. Bubble colour is based on EBITDA margins where the telcos with highest EBITDA margins are shown in dark green, while the telcos with lowest EBITDA margins have dark blue colour.

*IOH – estimated revenues post-merger of Indosat Ooredoo & Hutchison Tri

Methodology

We tracked 39 telcos operating in 15 different countries in the APAC region and captured their financial performance related to:

- Revenue,

- Classification and segmentation of revenue

- From enterprise segment and customers

- From beyond core connectivity services like cloud, gaming, e-commerce, etc

- EBITDA (earnings before interest, tax, depreciation and amortisation),

- CAPEX (capital expenditure),

- ARPU (average revenue per user)

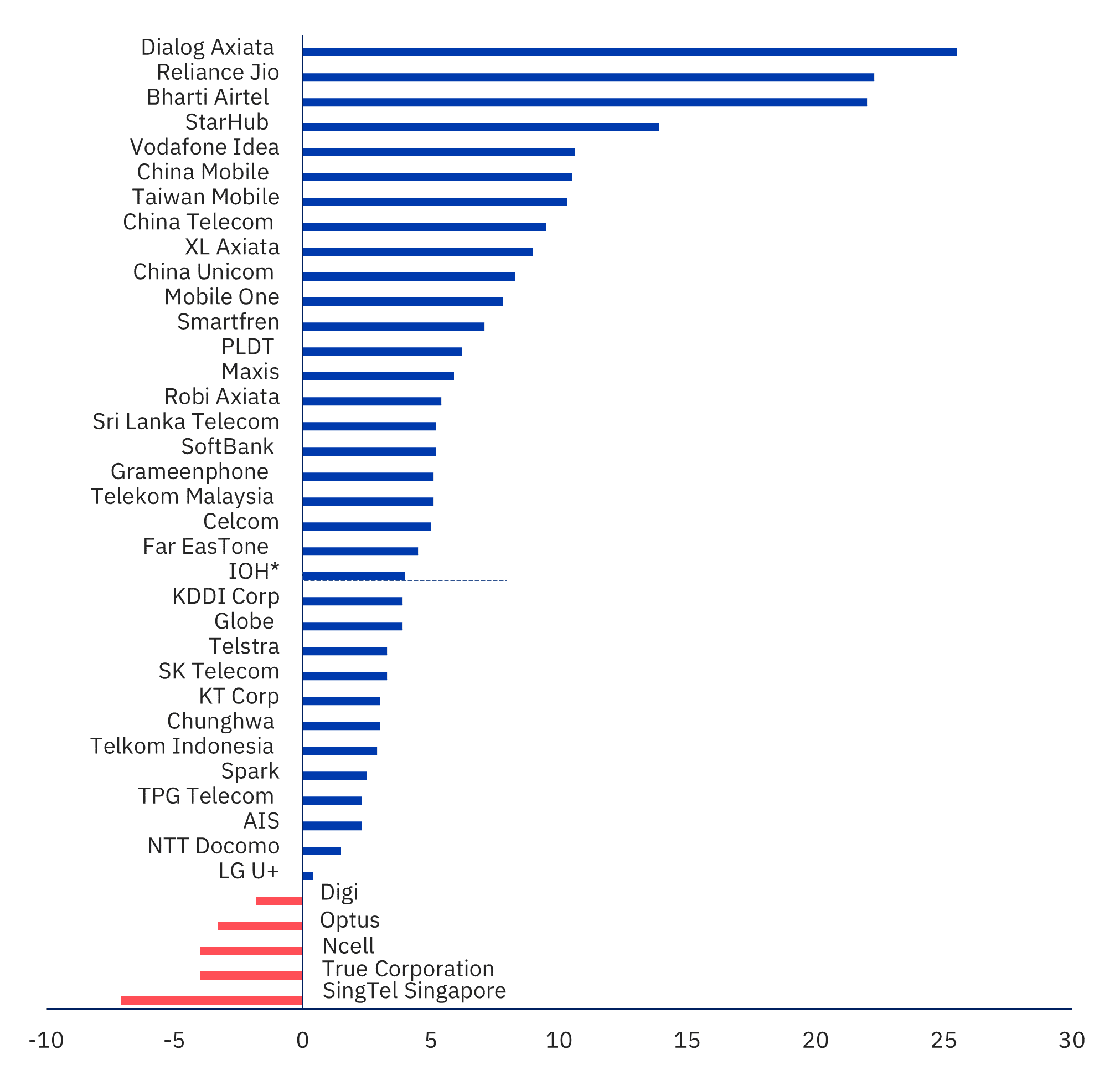

Trend #1 Industry revenue grew 6.7 percent exceeding 2021 growth of 6.4 percent

- 87 percent of telcos registered a positive revenue growth in 2022 (refer to exhibit 2).

- In 2022, Dialog Axiata emerged as the leader with an impressive 25.5 percent growth rate, surpassing its previous highest growth rate set in 2021. The Sri Lankan telco benefitted from the tariff increment in the market and registered growth across all three segments (mobile, fixed & TV).

- Tariff hikes also positively impacted the Indian telcos. ARPU improvement of between 20-25 percent (refer to exhibit 3) impacted the overall operating performance.

- There have been some very impressive revenue growth performances from the likes of StarHub (consolidation of jOS & MyRepublic Broadband), Taiwan Mobile (e-commerce business grew 17 percent YoY), China Mobile (5G enterprise), and good organic growth in connectivity business by Smartfren and XL Axiata.

- IOH reported the first year consolidated results post the merger of Indosat Ooredoo and Hutchison Tri Indonesia. The merger has delivered and exceeded the benefits promised. This is setting the tone for two other big mergers which are underway in Thailand (Tue & DTAC) and Malaysia (Celcom & Digi).

Exhibit 2

Percent revenue change for APAC telcos, 2022

*Indosat Ooredoo YoY growth 8%; IOH combined revenues estimated at 4% growth

Trend #2 Tariff adjustments and 5G help telcos stabilise ARPU

- Telcos are reversing the trend of declining ARPU over the years. 75 percent of telcos experienced a positive ARPU change in 2022 (refer to exhibit 3)

- 5 telcos (15 percent of telcos) recorded a double-digit growth out of which 3 are Indian telcos who benefitted by the tariff change.

- In addition to India, other markets are also taking concrete measures to address the decline in tariffs.

- In Sri Lanka’s TRCSL has approved a tariff revision in September 2022. Mobile, fixed, broadband, and other services up by 20 percent and a 25 percent increase for all Pay TV tariffs

- Unlimited data plans were discontinued by the top three telcos in Indonesia in 2021

- The return to normalcy in travel has brought back roaming revenues and contributed to helping improve ARPU in markets such as Singapore.

Exhibit 3

Percent Mobile ARPU change for APAC telcos, 4Q22 vs 4Q21

Note: ARPU change for the Chinese telcos is represented by FY 2022 vs FY 2021; ARPU change for Spark and TPG Telecom is based on H2 2022 vs H2 2021

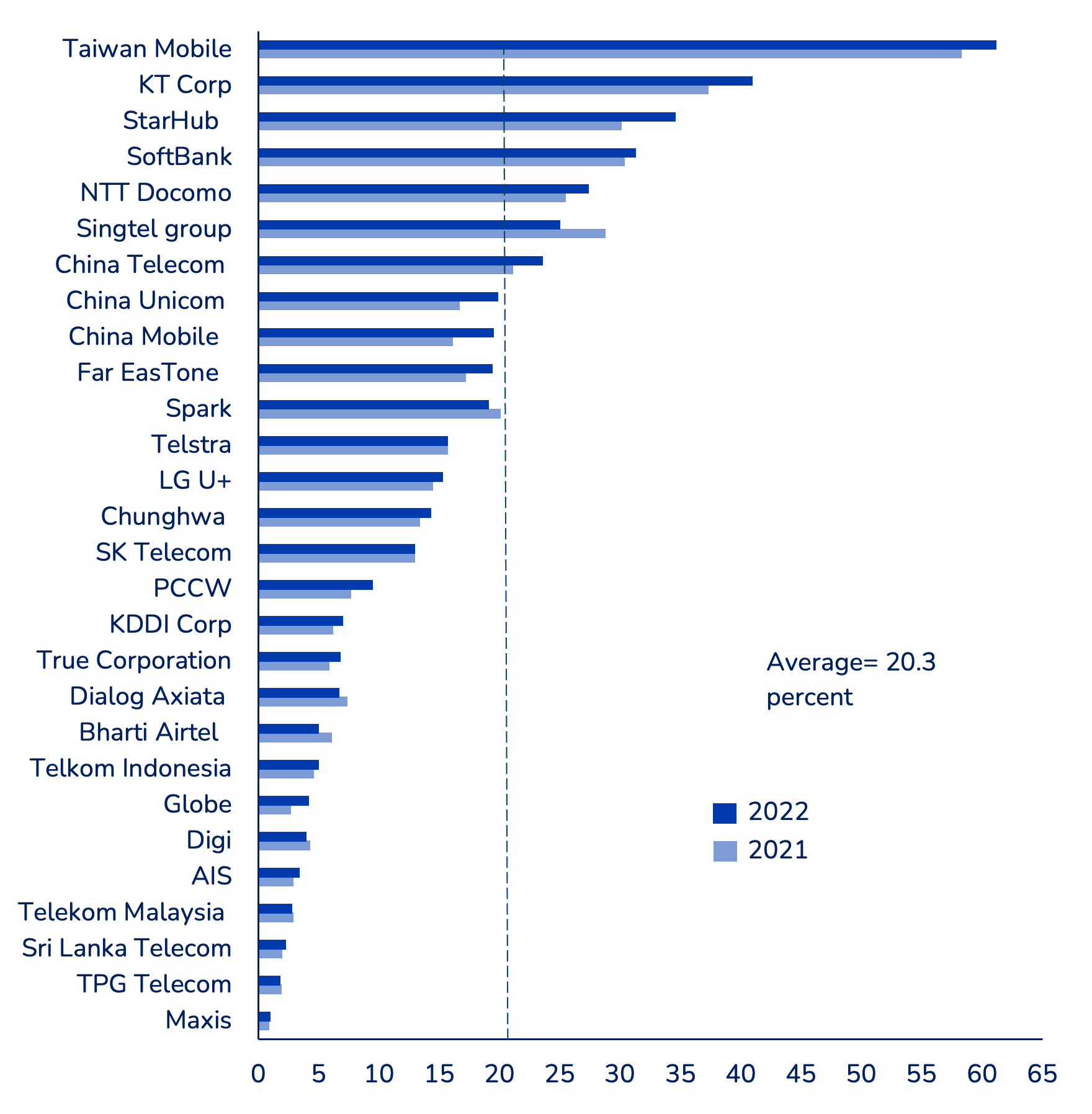

Trend #3 Non-connectivity businesses grow 17.4 percent as compared to industry growth of 6.7 percent

- 28 telcos disclose their non-connectivity revenues in their annual report. These range from enterprise services such as cloud, security and managed services. It also includes consumer services such as content and media, gaming, e-commerce, payments and so on.

- Compared to the total revenue growth, the non-connectivity segment shined with a YoY revenue change of 17.4 percent during 2022 (Analysis of 28 telcos). We anticipate non-connectivity to increase from 20.4 percent of total telco revenues to 26 percent of total by 2025.

- Taiwan Mobile remains at the forefront with non-connectivity revenues accounting for 61.2 percent of the total. Its e-commerce business continues to exhibit remarkable growth.

- Singtel’s revenue was impacted by the divestment of its Amobee business, leading to a decline in the contribution of non-connectivity revenues.

- Chinese telcos are gradually expanding their enterprise portfolio with cloud and Industry 4.0 solutions.

Exhibit 4

Percent of non-connectivity revenues to total revenues, 2022

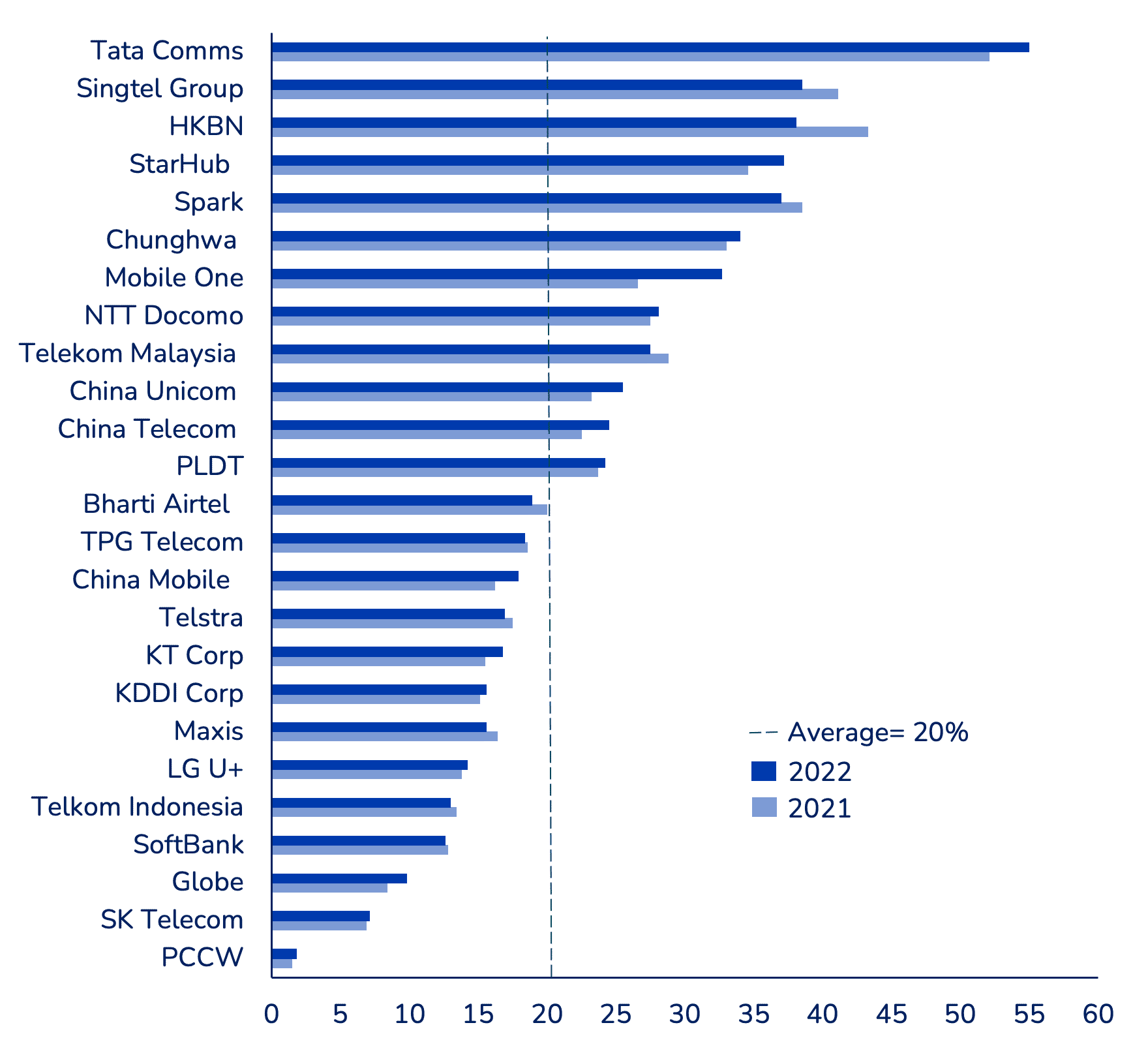

Trend #4 Enterprise business sees impressive growth of 11.8 percent, accounts for 20 percent of total revenues

- The growing urgency to monetise 5G has necessitated a focus on developing the enterprise business. This has been achieved through a combination of organic growth and acquisitions of smaller companies that have expertise in cloud, systems integration, and security.

- Our projections indicate that the enterprise business could contribute up to 30% of total revenues by the end of the decade.

- Please do note a caveat when reviewing the data in exhibit 5. A few telcos do include their wholesale connectivity numbers in their enterprise revenues, making it harder at times to estimate the true value of their enterprise business.

- One telco that has performed impressively in recent times is StarHub in Singapore through acquisitions. Meanwhile, all the three Chinese telcos, viz., China Mobile, China Telecom and China Unicom have all strengthened their cloud and 5G capabilities and are enjoying impressive growth rates powered by their enterprise business.

Exhibit 5

Percent of enterprise revenues to total revenues, 2022

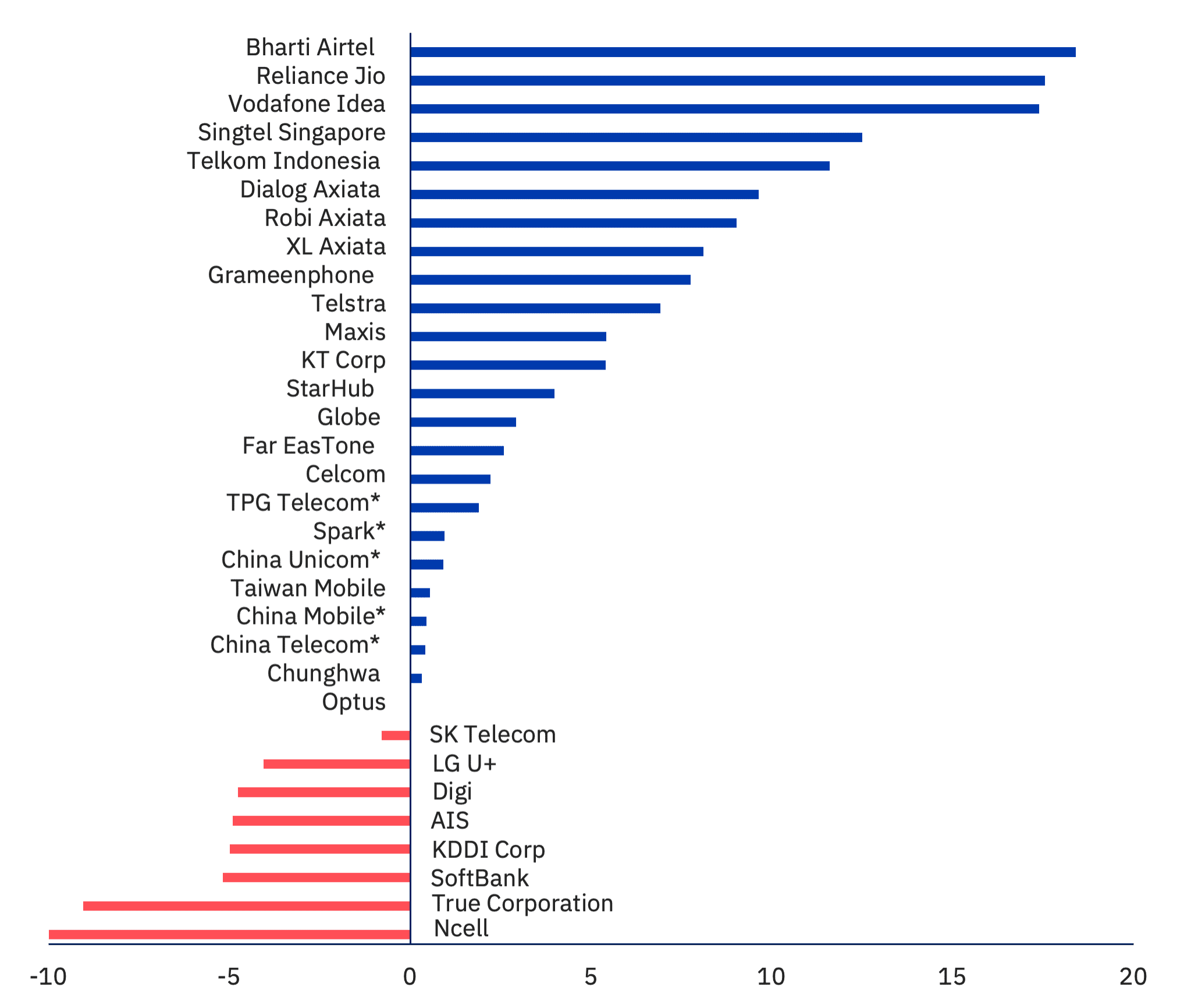

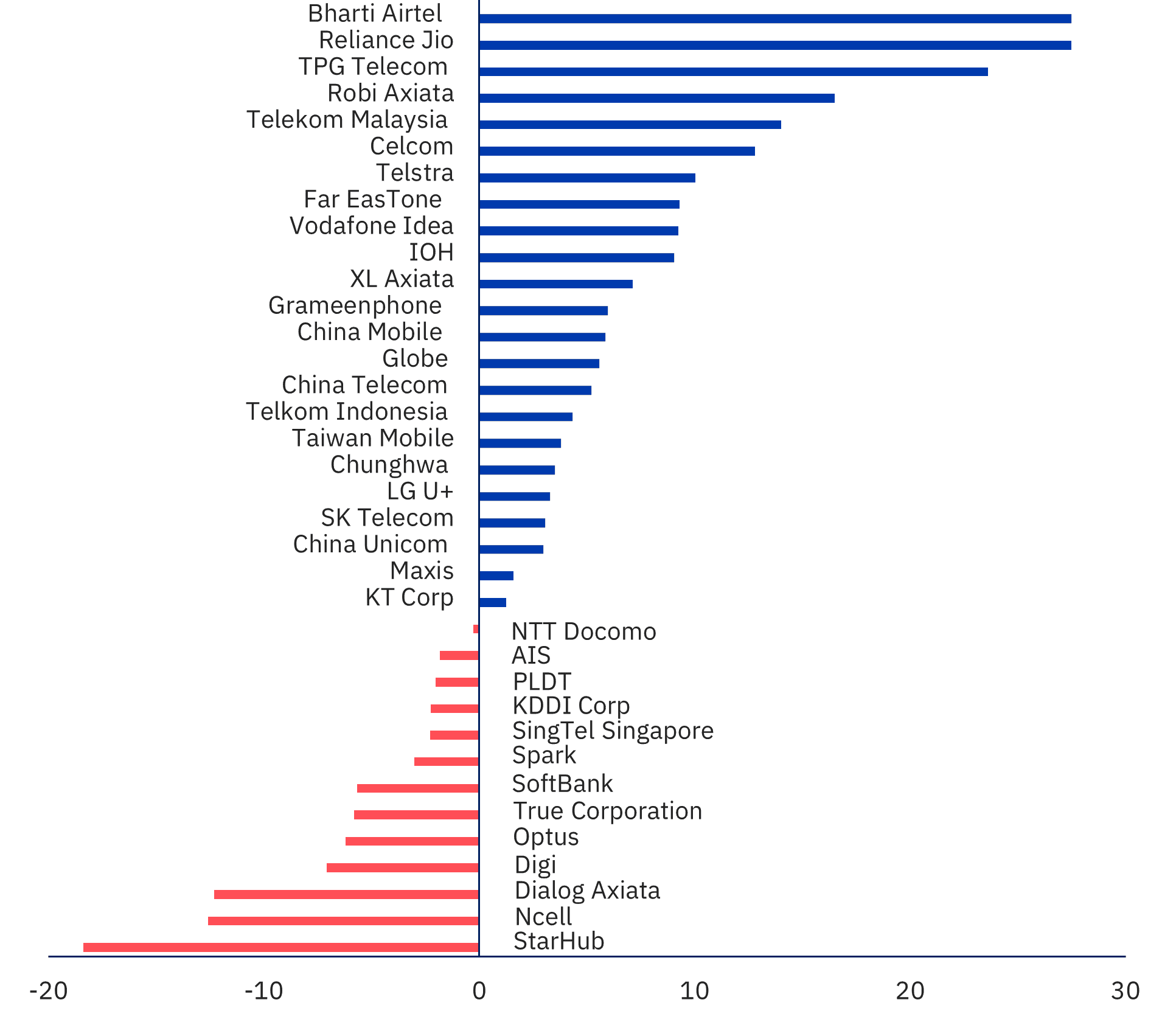

Trend #5 A few strong outliers of strong EBITDA performance, but continued pressure on earnings for majority of telcos

- 36 percent of telcos have reported a decline in earnings (EBITDA) due to an increase in operational costs (refer to exhibit 6).

- It is no surprise that the Indian telcos have registered impressive growth backed by the strong growth in ARPU and revenues in 2022.

Exhibit 6

Percent EBITDA change for APAC telcos, 2022

- Telekom Malaysia delivered a strong financial performance with a 14 percent increase in EBITDA. The healthy revenue growth of 5.1 percent revenue growth was supported by a decrease in total cost/revenue percentage from 86.5 percent in 2021 to 83.9 percent in 2022.

- TPG Telecom benefited from the sale of passive tower and rooftop assets, while Robi Axiata achieved higher EBITDA through cost management and favourable one-off adjustments in Q4.

- StarHub’s lower EBITDA was due to higher OPEX caused by non-recurring provisions related to DARE+ initiatives.

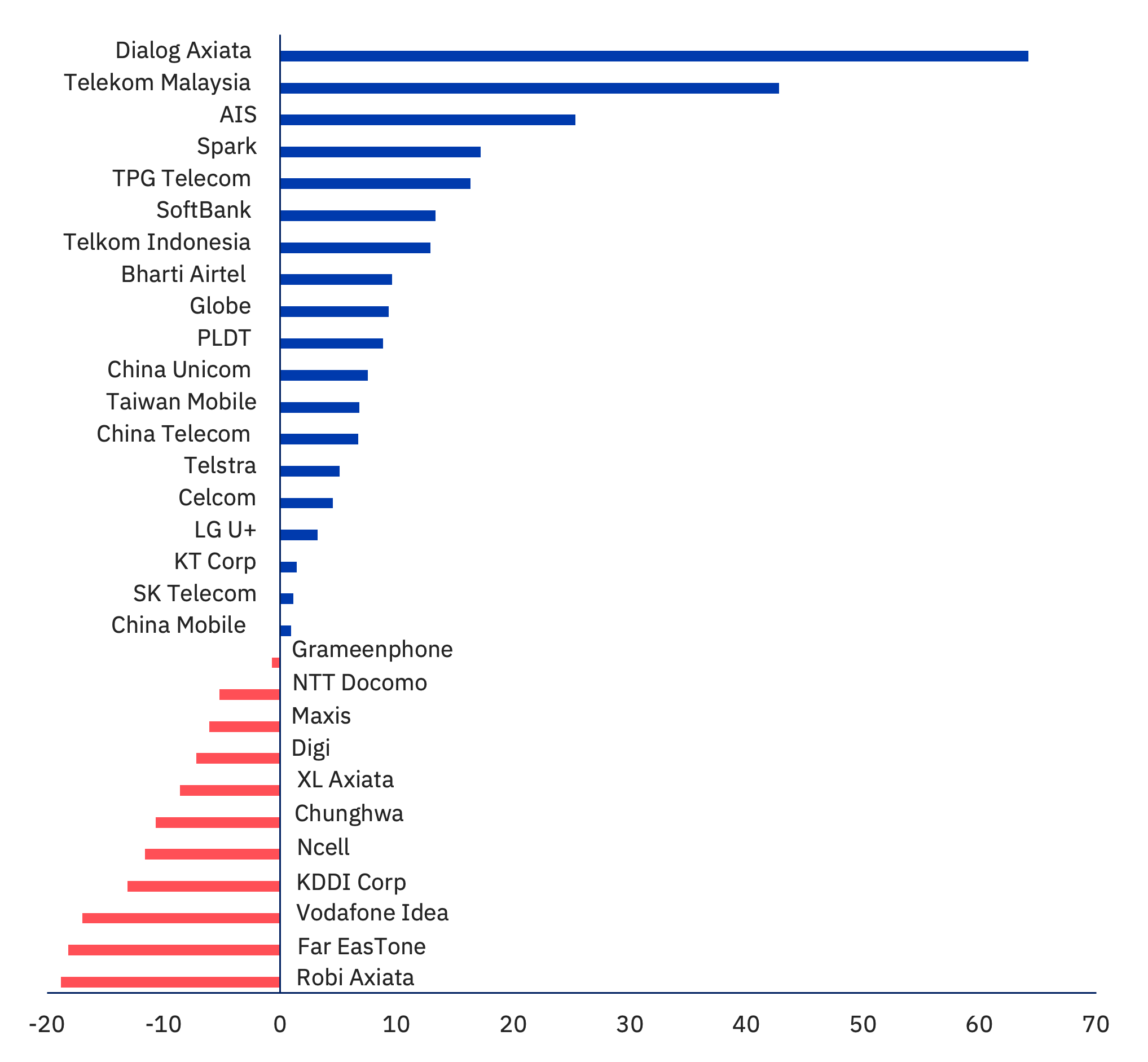

Trend #6 CAPEX spending starts slowing down and consolidation is emerging as a hot trend for the region

- 37 percent of the telcos charted a negative change in their CAPEX in 2022 and 40 percent recorded a change ranging from 0-10 percent (refer to exhibit 7)

Exhibit 7

Percent CAPEX change for APAC telcos, 2022

- Dialog’s CAPEX grew by 64 percent YoY, similar to 2021. Their focus has been on network expansion, including adding 450 new sites and increasing capacity at over 2,100 sites. They also deployed alternative energy solutions such as solar and Li-ion batteries to improve network availability.

- Collaboration in CAPEX spending and infrastructure sharing has become a consistent trend.

- The two largest markets in South Asia, Indonesia and India, are expected to witness a substantial increase in CAPEX spending in 2023 due to 5G.

The increased requirement for capex to fuel the growing appetite for data services continues to put tremendous pressure on the telcos This trend is driving consolidation in the industry. In 2022, three major telecom markets in the region, Indonesia, Malaysia, and Thailand, witnessed mergers between two leading players to drive scale and capex efficiency. Exhibit 8 shows the major mergers in 2022. We expect this trend to continue for the next few years.

- In Thailand, True and Dtac merged to enhance their services and strengthen their position in a fiercely competitive market.

- In Indonesia, the merger of Indosat Ooredoo and 3 Hutchison (now called Indosat Ooredoo Hutchison) has created a strong second player in the market with over 100 million subscribers.

- In Malaysia, the merger of Celcom and Digi (now called CelcomDigi) has resulted in the largest player in the country.

Exhibit 8

Major mergers in 2022

Recommendations

#1 Pricing strategy

A combination of factors such as intense competition, regulatory intervention and inadequate emphasis on differentiation has led to a steep APRU decline in the last decade. Added to this is the perception that telcos are poor at customer service and experience making it difficult to drive price improvement. Telcos need to prioritise and drive a pricing strategy that can drive overall ARPU increase. This can drive an inordinate impact on the profitability of companies. The exemplary performance of Indian telcos in 2022 is ample proof that this can be done. There are several opportunities to drive a positive price change.

- The launch of 5G services and its co-existence with 4G provides telcos an avenue to offer differentiated propositions. Integrating high quality access and bundling with premium devices and customer service has been done effectively in many markets.

- Consumer needs are evolving rapidly. Preliminary research suggests that close to 30 percent of customers are willing to pay a premium of 30 percent if they can get better service and experience. There is an opportunity to develop a premium brand to meet with the lifestyle needs around devices, content subscriptions and personalised experiences.

- Majority of the sub-brands and digital brands have been positioned as discount or lower priced alternatives. The ability to collaborate with other powerful premium brands present an opportunity to created differentiated new experiences.

#2 Partnering for growth to drive non-connectivity business

Telcos in every country have by far the biggest reach into consumers, small and medium businesses as well as large enterprises. They are the biggest potential channel for distribution of innovative digital services ranging from finance, gaming, healthcare, insurance, cybersecurity and many others. Partnerships are a critical level for helping telcos build their new non-connectivity business. It enables them to leverage off the skills of the partners to establish and scale these new businesses. Several telcos have already seen early successes with these partnerships.

- Globe Telecom partnered with Ant Financial for scaling its payment and financial services business G-Cash. It has achieved operational profitability and is now valued at over US$2 billion.

- SingTel has partnered with SK Telecom to grow the Metaverse business in Asia Pacific. It will leverage SKT’s metaverse platform, ifland, and drive innovation in new digital used cases for consumers as well as enterprise customers.

- Telcos around the world have partnered well with hyperscalers to leverage the full potential of the public cloud for their own consumption as well as to support their enterprise customers transitioning to the cloud.

- Indosat Ooredoo Hutchison has partnered with Google to develop a marketplace of customised software-as-a-service offerings to support the digitalisation of 62 million SMEs in the country.

The nature of these partnerships are new to telcos. They need to nurture these well and support with the right talent to ensure success.

#3 Cost optimization

While telcos have slowly discovered the mojo to drive revenue growth, they are also experiencing an increase in operational costs. 36 percent of telcos have reported a decline in earnings (EBITDA) (refer to exhibit 6). Margins in new business segments are significantly lower than the traditional connectivity business. Credit is also due for the telcos on playing the role of ideal corporate citizens and not resorting to extensive layoffs when economic conditions have shown signs of deterioration around many parts of the world.

There exists considerable opportunity to reduce the cost to serve.

- AI and automation is still in its infancy and there will be considerable opportunities to leverage this and bring cost down.

- Simplification of plans have helped many a telco reduce complexity and in turn reduce costs.

- Network sharing and network outsourcing continue to be a source of cost efficiency. Additionally, there now a growing momentum towards consolidation as growth in connectivity business is now trending towards very low single digits around the region.

Hope you enjoyed the read. Here is some more exciting content on telecom

Stay tuned for an updated version of these reports in the coming weeks