Over the last few weeks, most of the region’s telecoms service providers released their annual reports for 2020. The reports allowed us to do a detailed deep dive into the performance of the telecom service providers and provide insights into other trends such as CAPEX, profitability, and 5G adoption. This insight captures the top trends from 2020.

1. Modest growth in revenues, driven by a handful of service providers

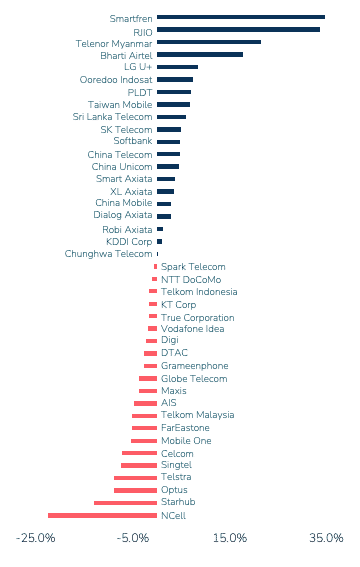

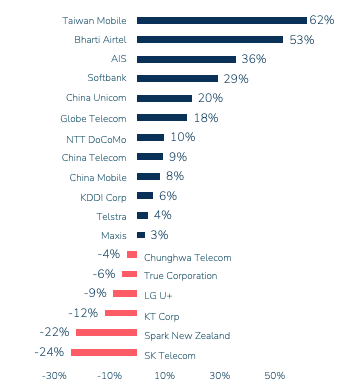

- Telecoms service provider revenues recorded a modest 2.1% year-on-year (Y-o-Y) growth in 2020, adding over USD 10 billion in net revenue during the year. From the list of major telecom operators in the APAC region, 45% saw positive Y-o-Y revenue growth for FY2020.

- Roaming revenues have adversely affected revenue growth for service providers in the APAC.

- The release of new 5G handset models, such as iPhone 12, served as a strong tailwind for 5G service uptake towards the end of the year. For some telecom service providers, this reversed the possible income loss from device sales.

Figure 1: Revenue change for Asia Pacific telecom service providers, 2020

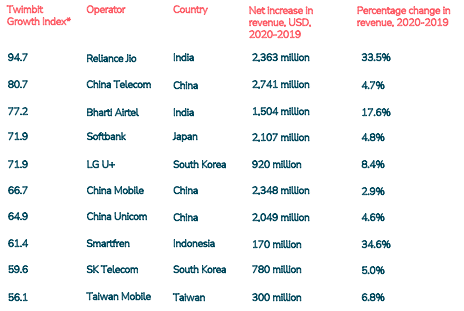

2. Reliance JIO, China Telecom, and Bharti Airtel lead the Twimbit Growth Index for 2020 in the Asia Pacific

Tariff hikes and increased data consumption key driver in emerging markets; 5G drives growth in China and South Korea.

- Indian operators continue to grow revenues largely driven by multiple tariff hikes during the year. Operators benefited from accelerated migration to 4G services and increased data consumption supported by the evolving digital ecosystem.

- Bharti Airtel and Reliance JIO ramped their enterprise businesses (for both large and small business segments) with a focus on executing multiple partnerships to offer cloud, collaboration, and security services.

- The region’s largest operators in China have gained around USD 7,000 million in net revenues during 2020. Growth in 5G subscriptions improved ARPU and data consumption. For China Mobile, ARPU for 5G package customers is about 6% higher compared to blended ARPU for its mobile customer base.

- The launch of new 5G handset models has improved 5G monetisation by bundling higher rate plans with new devices.

- Operators are driving growth by participating in market adjacencies, particularly content, media, and ecommerce. SK Telecom aims to evolve its core business into a subscription-based platform that will offer various digital products. The products include FLO for music streaming, Wavve for video-on-demand, cloud games, and V Coloring – a Video Ring Back Tone service.

Figure 2: Twimbit’s Top 10 Asia Pacific telecom service providers to ace growth in 2020

Note: Twimbit Growth Index is calculated as a combination of two parameters, viz, absolute increase in revenues and percentage change year-on-year. The growth score assigns a weightage of 67% to absolute increase in revenue and 33% to YoY growth percentage.

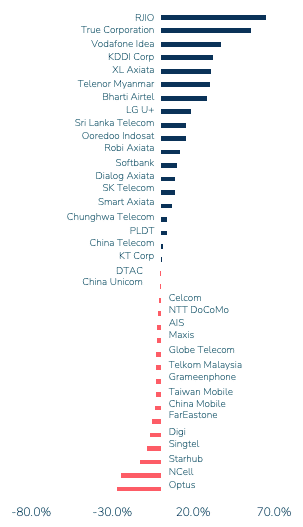

3. 5G operators felt the drag on margins

EBITDA margins for China Mobile, China Telecom, and China Unicom saw a decline in 2020. Higher costs associated with running 5G infrastructure impacted EBITDA margins. For the three operators, EBITDA margin reduced by two to three percentage points as expenses went up across main categories, network operations and support, as well as power consumption.

Figure 3: EBITDA change for Asia Pacific telecom service providers, 2020

4. Asian consumers appetite for data grew with expanded choice on digital services

Operators across multiple Asian markets witnessed an upward trend in mobile data usage, setting long-term demand trends, including remote working, online education, and an accelerated shift towards digital lifestyles. A range of promotional offers from service promoters complements the increase in data appetite.

- Many operators across developing and developed Asia launched unlimited data packages, although most were via the Fair Usage Policy.

- There were more choices available in terms of access to over-the-top services. The specific needs of various consumer segments supported the trend.

- By offering more choices, service providers strengthened their ability to introduce service variants and their capabilities to on-board partners quickly.

Figure 4: Average monthly data usage per SIM for Asia Pacific telecom service providers, 4Q2019 vs 4Q2020

Source: tefficient

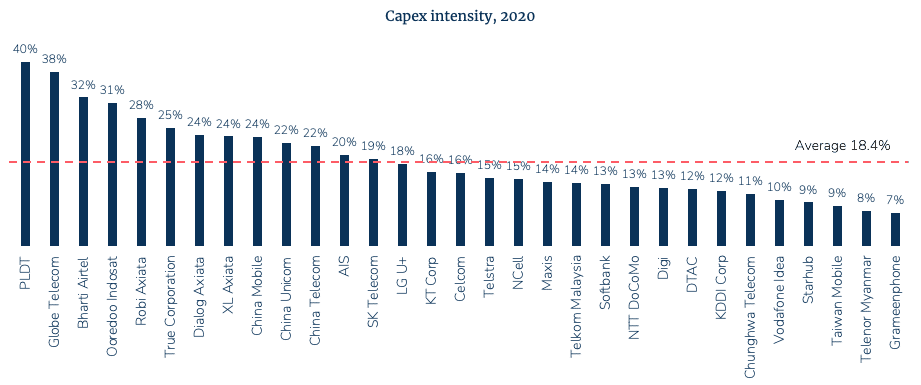

5. Need for high-speed broadband boosted investments in access infrastructure

Elevated capital investments (CAPEX) result from the accelerated roll-out of fiber-to-home lines and the upgrade of mobile access networks for capacity and coverage. The roll-out of 5G networks also drove the increase in CAPEX.

Figure 5: CAPEX intensity for Asia Pacific telecom service providers, 2020

6. Network sharing models emerge as operators rationalise 5G CAPEX

Telecom operators are also emphasising on the sharing and the joint construction of the 5G infrastructure to rationalise CAPEX spending. This trend is gaining momentum across the APAC region.

China

The arrangements by operators in China to co-build, operate, and co-share have helped keep 5G investments under control. China Telecom and China Unicom entered into a co-build and co-share 5G infrastructure agreement in 2019. According to the operators, the new model has resulted in a cumulative savings of USD 8,800 million in 5G CAPEX during 2020. The two also cited some rationalisation in operating expenses, particularly for tower leases and network maintenance charges.

In the next phase of the 5G network buildout, operators in China expect moderate growth in CAPEX based on the guidance provided for 2021. There is scope for further optimisation of the industry’s CAPEX if operators choose to build a shared single 5G network in rural localities.

Singapore

M1 and StarHub formed a joint venture for a 5G standalone radio access network infrastructure buildout using 3.5GHz band. The active radio network sharing involves spectrum pooling, a common radio base station equipment including antennas, and a shared backhaul.

The two operators will maintain separate 5G core networks, platforms, and business support systems for service differentiation. They will also equally share all OPEX, CAPEX, and profits from the infrastructure.

South Korea

A similar approach towards co-building a 5G network infrastructure got its approval from the Ministry of Science and Information Technology, South Korea, under the Rural 5G joint-use plan. While the three operators will develop the infrastructure in dedicated rural localities, the network will be available to all mobile network operators and virtual network operators (MVNOs).

Malaysia

In Malaysia, the 5G network roll-out will begin late in 2021. Taking a unique approach, the government has announced the provisioning of 5G infrastructure to be conducted through Digital National Bhd, a special purpose vehicle (SPV) wholly owned by the government of Malaysia and regulated by the Malaysian Communications and Multimedia Commission (MCMC).

The entity will be awarded the required 5G spectrum and will have the responsibility to build, own, and manage the country’s 5G infrastructure. The SPV will lease the required infrastructure and spectrum on a wholesale basis to mobile operators wishing to offer 5G services to their customers.

A USD3.7 billion investment over ten years will happen through the SPV as Malaysia progresses with its phased 5G roll-out.

While the Malaysian government’s approach to building 5G networks appears unique, similar models have existed with respect to the roll-out of fixed broadband infrastructures across multiple markets, including Singapore, New Zealand, and Australia.

Figure 6: CAPEX change for Asia Pacific telecom service providers, 2020

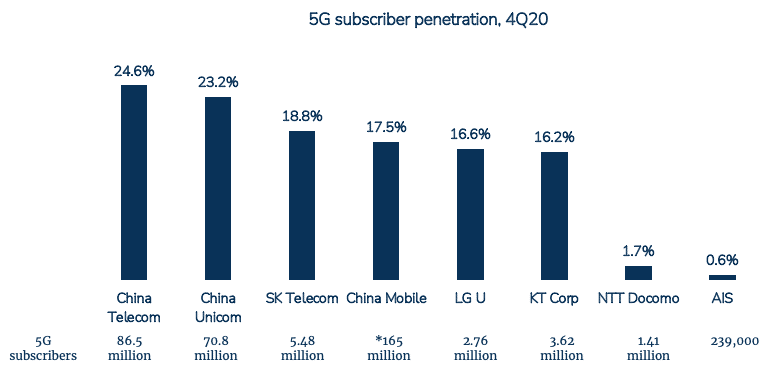

7. 5G momentum continued, ARPU uplift noted for early adopters

About 24 operators from 12 markets have already launched 5G for commercial use. The markets include China, South Korea, Japan, Hong Kong, Taiwan, the Philippines, Thailand, Singapore, New Zealand, Australia, and some Pacific Islands. In December 2020, Vietnam was the most recent to launch commercial trials via its state-owned Viettel.

China and South Korea continued to expand their 5G coverage. The countries first made 5G available in 2019 and have shown promising uptake. For both, a major share of CAPEX investments diverted towards a 5G roll-out. In China, operators invested USD 50.7 billion in 5G networks in 2020, representing about 52.8% of total capital expenditure by the three incumbent operators.

- An operator’s 5G success is associated with minor pricing difference in the existing 4G plans and the introduction of premium unlimited data packages bundled with relevant 5G services.

- Service providers in these markets retained the focus on developing ecosystems for both devices (5G handset, AR & VR devices) and related services such as 8K video, cloud gaming, AR & VR based applications, and immersive content.

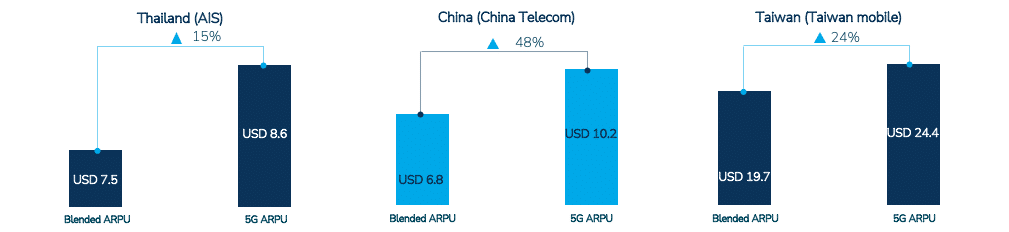

- Also, the bundling of higher rate plans with premium 5G devices resulted in an ARPU uplift among 5G early adopters.

Figure 8: 5G ARPU for Asia Pacific telecom service providers, 2020

8. 5G in enterprise picks up with private networks and vertical use cases

Operators in China and South Korea are focusing on the enterprise market segment with 5G. The incumbents have identified key vertical industries, possible services and business models where 5G delivers value through relevant applications.

China Telecom, China Unicom, and China Mobile have introduced 5G private network service portfolios. There are three key deployment scenarios offered:

- 5G private network using network slicing

- Public-private hybrid by sharing mobile operators public 5G network resources

- Isolated 5G private network, independent of mobile operators public 5G network

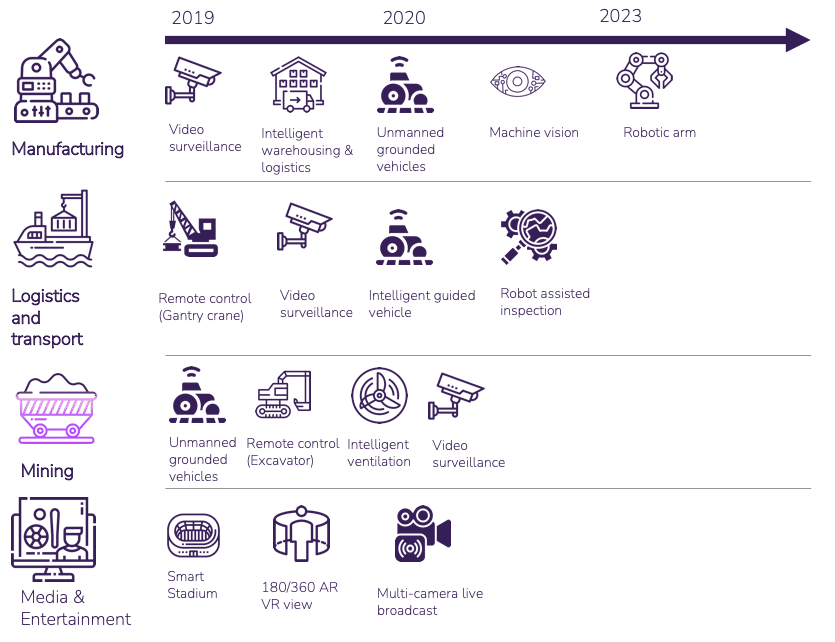

Enterprises are deploying private networks either by using local 5G frequencies or mobile operators licensed frequencies. Some of the key vertical industry used cases are visible in figure 9 below.

Figure 9: 5G vertical use cases (pre-commercial, PoCs, and commercial deployments)

Read here for previous update: Future of Telecoms in Asia 3Q20 update

Find out how the future of telecoms in APAC looks in 2021: Cloud, EDGE, and 5G – how innovation will shape the future of telecoms?