Key highlights

Rising interest rates and wealth management fees remain key factors for the higher NIMs across Singapore banks, leading to their strong performance in Q3 2023.

- DBS, UOB and OCBC reported higher incomes in Q3 2023 than in Q3 2022.

- DBS, UOB and OCBC reported a decline in loan portfolios at 2.15%, 1.55% and 1.65%, respectively.

- High loan repricing has led to slow loan growth, further reflecting weaker customer demand for loans.

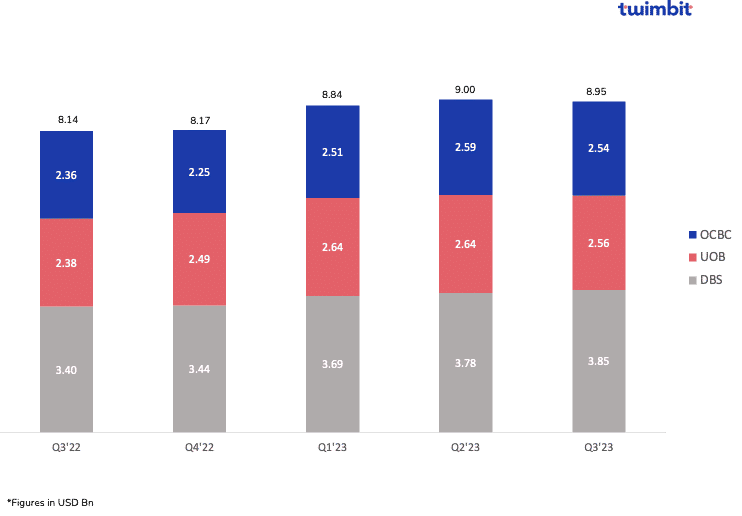

Revenue

Net revenues grew by 9.9% YoY to USD 8.95 billion in Q3 2023 compared to Q3 2022

Revenue growth was driven by a 14.09% increase in net interest income and a 9.75% increase in non-interest income.

- OCBC

- Highest net interest income at 17%, from USD 1.56 billion to USD 1.82 billion, led by 6% growth in bank assets and net interest margin expansion in a rising interest rates environment

- Lowest non-interest income at 4.4%, from USD 691 million to USD 721 million, led by higher fee income and improved investment performance, offset by lower insurance income

- DBS

- Highest non-interest income increase at 12.55%, from USD 1.71 billion to USD 1.92 billion

- Commercial book accounts for 80% of non-interest income and consists of the bank’s fee income and other non-interest income barring treasury markets income

- Commercial book reported a sustained growth at 8.84% from USD 914 million in Q3 2022 to USD 994 million in Q3 2023

- Treasury income accounts for 20% of non-interest income

- Treasury income grew by 45.38% from USD 176 million in Q3 2022 to USD 256 million in Q3 2023

Exhibit 1: Net revenues of the top 3 Singapore banks

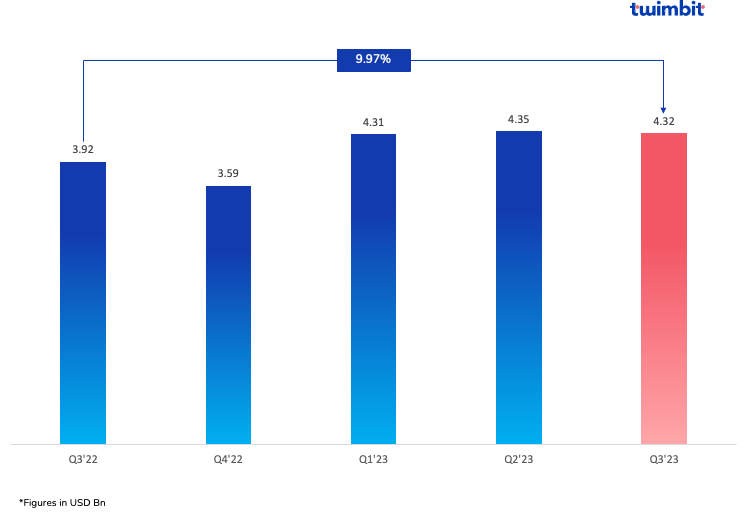

Profitability

Net profits grew by 10% YoY to USD 4.32 billion in Q3 2023 compared to Q3 2022

Net profit growth was majorly driven by a 14.1% growth in net interest income and a 9.7% growth in fee income.

DBS reported the highest growth in its net profits at 16.58%, from USD 1.67 billion to USD 1.95 billion. This growth was driven by a 16% increase in the bank’s net interest income and a 12.55% increase in the non-interest income.

UOB reported a decline in net profits by 2.48% from USD 1.5 billion to USD 1.02 billion. The primary driver was a 25% decline in other non-interest income of the bank.

Exhibit 2: Consolidated net profits of the top 3 Singapore banks

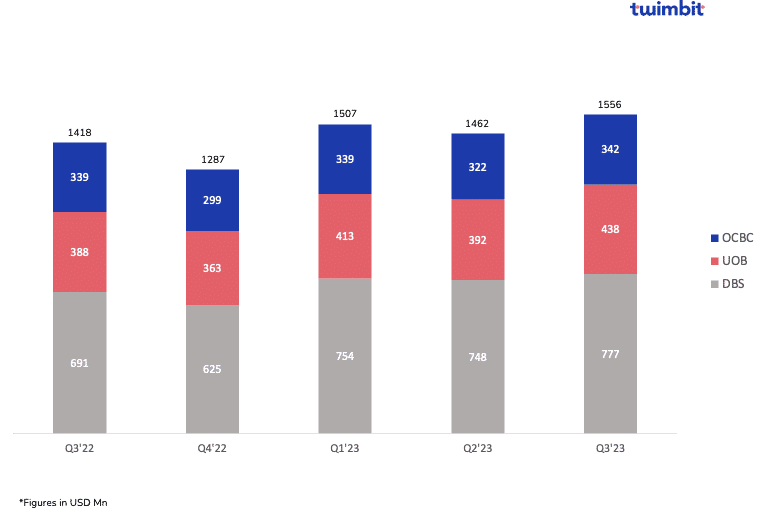

Fee-based income

Fee income grew by 9.7% to USD 1.56 billion in Q3 2023 compared to Q3 2022

UOB reported the highest growth of 12.73%, from USD 388 million to USD 438 million, primarily due to:

- 89% growth in card-related fees from USD 41 million to USD 77 million

- 45% growth in wealth management fees from USD 97 million to USD 108 million

OCBC reported a marginal growth of 0.75%, primarily due to a decline in its:

- Investment banking fees by 25%

- Loan-related fees by 2.36%

- Fund management fees by 13.33%

This decline was offset by a 9.5% increase in wealth management fees from 132.6 million to USD 145.2 million.

As observed, a contributing factor for these banks was the steady increase in their wealth management fees. However, it is expected to remain weak despite rising assets under management (AuM) and the YoY increase of 15.75% from USD 471 million to USD 545 million.

Exhibit 3: Fee incomes of the top 3 Singapore banks

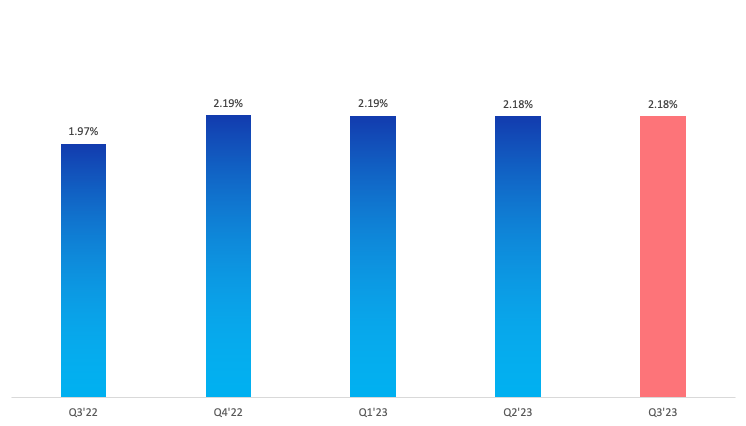

Net interest margins (NIM)

NIM grew by 21 basis points to 2.18% in Q3 2023 compared to Q3 2022

The increase in the NIM primarily occurred due to a higher interest rate environment. Overall, the average NIM for Singapore banks stood constant at 2.18% from the previous quarter.

Exhibit 4: Consolidated NIM of the top 3 Singapore banks

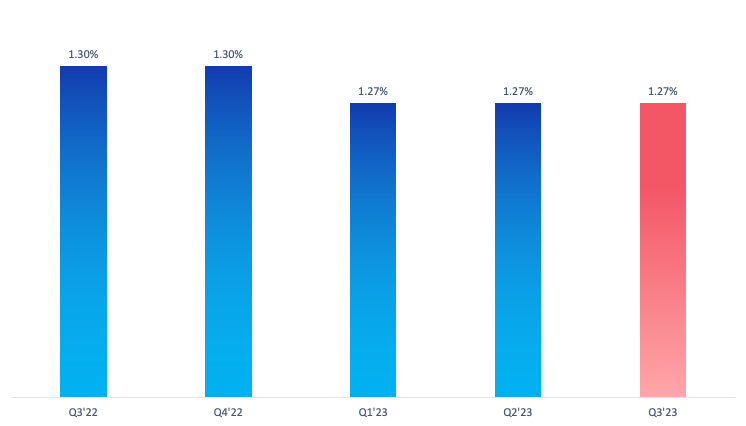

Non-performing loans (NPL)

NPL fell by 3 basis points (bps) in Q3 2023 compared to Q3 2022

The top 3 banks’ average NPL witnessed a 3 basis points decline, resulting in a current NPL of 1.27% (Exhibit 5).

- NPL for DBS remained static at 1.2%

- NPL for UOB increased by 10 bps from 1.5% in Q3 2022 to 1.6% in Q3 2023

- NPL for OCBC declined by 20 bps from 1.2% in Q3 2022 to 1% in Q3 2023

It should be noted that the transport, storage and communications sector had the highest NPL among major banks in Singapore at 6.58%.

Exhibit 5: Consolidated NPL of the top 3 Singapore banks

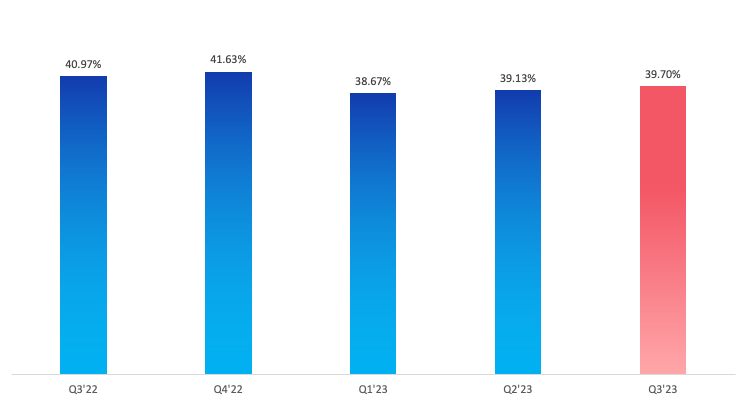

Cost efficiency (CE)

CE for Singapore banks improved by 127 bps in Q3 2023 compared to Q3 2022

Singapore banks are among Asia Pacific’s most efficient, behind Chinese and South Korean banks. The average cost efficiency for the top 3 banks in Singapore stood at 39.7% (Exhibit 6), with each bank recording a cost efficiency below the threshold value of 50%.

All 3 banks reported improved cost efficiency between Q3 2022 and Q3 2023. The improvement in cost efficiency is primarily due to a 9.9% growth in net revenues, and a marginal growth of 1.83% in operating expenses.

Exhibit 6: Consolidated cost-efficiency ratio of the top three Singapore banks

Top Initiatives by Singapore Banks

- #1 DBS

DBS announced their intentions to commit USD 741 million to improve the livelihood of the low-income and underserved. The bank will deploy USD 74 million annually in Singapore and its other key markets from 2024 to enact its initiative.

The funds will predominantly go towards programs dedicated to:

- Assisting individuals with their immediate daily necessities, such as food and housing

- Empowering underprivileged communities with education on digital and financial literacy

- #2 UOB

UOB announced the progressive rollout of employee support at its annual employee festival, ‘Better U’ today.

The program aims to help employees further expand and gain a greater understanding of their careers at UOB, covering everything from career opportunities to benefits extending beyond retirement, including:

- A 1-year work initiative collaboration with 5 Polytechnic and 3 ITE (Institute of Technical Education) colleges in Singapore to develop the skills of their students

- A physical ‘Better U’ Campus at the Singapore Institute of Management (SIM) that focuses on upskilling and reskilling opportunities for employees

- A transition program to assist employees post-retirement

- #3 OCBC

OCBC is set to introduce a GenAI chatbot to support 30,000 employees worldwide in writing, research and idea generation.

- Microsoft’s Azure OpenAI powers the OCBC GPT chatbot and leverages sophisticated language models to analyse queries and generate responses.

- The chatbot is hosted in a controlled environment, safeguarding data confidentiality and inaccessibility to Microsoft and external entities.

- Following a successful six-month trial involving 1,000 OCBC staff, OCBC GPT showcased efficiency in various tasks, leading to a 50% reduction in average task completion time.

Increased NIMs have greatly benefitted Singapore banks, which began raising rates in early 2022 to address inflation concerns. As economies recovered from the pandemic, banks successfully transmitted increased interest rates to borrowers. However, the tightening has slowed in recent months, and interest rates are anticipated to reach their peak.

Research methodology and assumptions

- Data collection has been done based on secondary research about the information provided by the respective banks through their investor presentation and quarterly financial statements. Twimbit follows the calendar year approach for the analysis in this report (meaning Q1 is equivalent to the period of January to March of the year).

- For fair representation and analysis, we have considered a constant currency rate for conversion from local currency to USD value. The USD conversion rate is the average calculated value from January to September 2023.

- The report analyses net revenue, net profit and fee income, net interest margin, non-performing loan and cost efficiency for 5 banks.

- The fee income figures taken for OCBC and UOB are net of fee expenses.

- The revenue figures for all the banks analysed are net of interest and non-interest expenses.

To learn about how the leading Indian banks performed in Q3 2023, click here.

To learn about how the top 5 Indonesian banks performed in Q3 2023, click here.

To learn about how the leading banks in the Philippines performed in Q3 2023, click here.

To learn about how the leading banks in South Korea performed in Q3 2023, click here.