Hyper-personalisation in banking

- The primary goal of hyper-personalisation is to provide more relatable services and offers that enhance the customer experience

- Utilising behavioural data science and the use of Artificial Intelligence (AI) to offer relatable products and services to consumers

- Collecting and analysing the right data to improve customer loyalty across all channels, including mobile banking apps.

- Reducing acquisition costs by as much as 50%, lifting revenues by 5% to 15% and increasing the efficiency of marketing spend by 10% to 30%

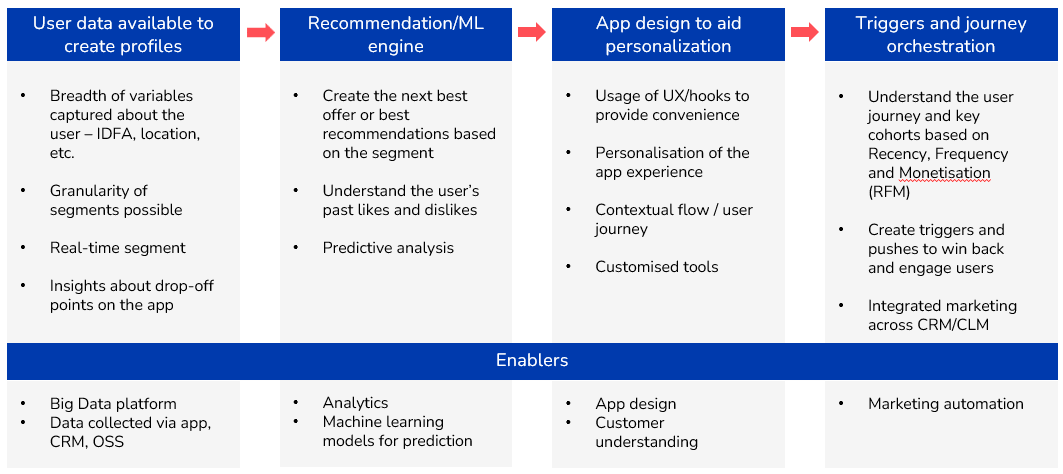

4 pillars of the personalisation framework

4 key functions of a hyper- personalised app

- Convenience

Make banking apps easy to use and simple to access. Usually, customers look for frictionless onboarding, negligible abandonment rate, and seamless navigation.

- Personalisation

Personalisation is beginning to shape the future of digital banking, as more banks look to capture the type of personalization that platforms like Netflix, Amazon Prime and Shopee presents.

- Gamification

Gamification and social engagement

- Use of icons and images

- Set goals and alerts

- Offline to online engagement

- Insights and tools

Integrating analytical tools and features which provides insights and are customisable according to the customer’s needs

twimbit approach

A three-pronged approach to shortlist the best-in-class banking apps:

- Meticulously selected apps with a rating of 4.3+ on the Apple App Store and Google Play Store.

- Analysed banks and fintech companies to identify best practices.

- In-depth exploration of hyper-personalisation features within mobile banking applications.

Top 4 banks to ace hyper-personalisation

Commonwealth Bank

Background

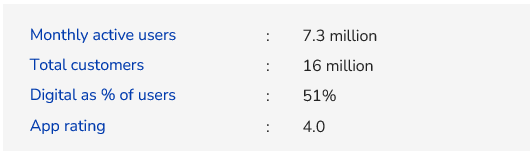

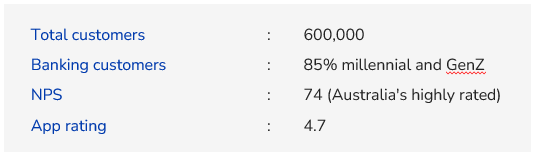

- Commonwealth Bank of Australia (CBA) is among the ‘Big Four’ banks in the Australian financial services market

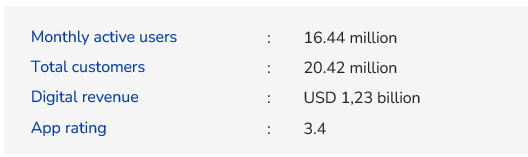

- The bank has a customer base of more than 16 million customers

- CBA is also a fintech leader with 8 million digital active users

Great app, the best among the ‘BigFour’ banks by far. Easy enough to ignore most of the advertising.

-(CommBank user)

#1 Tools and analytics

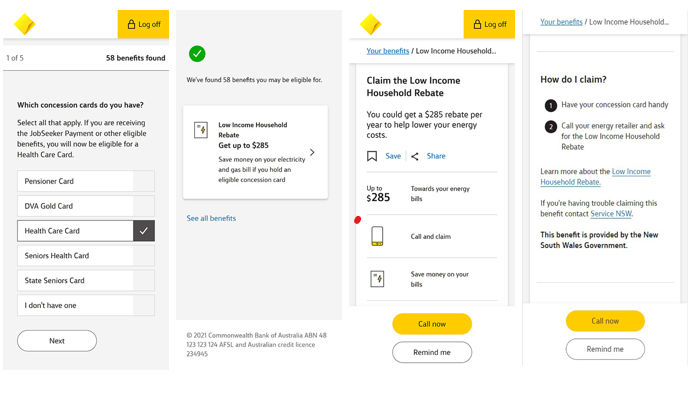

Benefit finder tool

- The benefits finder tool is available both in the mobile app and online banking website (NetBank).

- Upon successful login, the benefit finder tool will ask the customer a few simple questions to know about their financial standing and any dependents that they might have.

- Based on the answers provided by the customer, it then suggests all the ‘benefits’ they might be eligible for.

- To apply for a benefit, the customer can then go to the respective benefit provider’s website from within the bank’s app.

- The app has an extensive list of 270 different benefits, which differ from state to state.

- Since launch, the tool has helped register 2.2 million claims, amounting to more than USD 670 million

#2 Budgeting

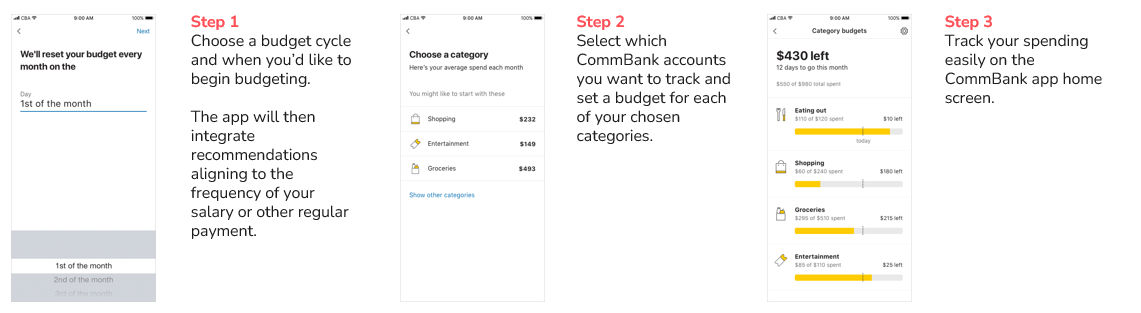

Category budget

Category budgets lets you set fortnight, weekly, or monthly budgets for different categories of your spending – from entertainment to transport, eating out and shopping. It allows you to instantly assess and compare your actual spending against your budgeted spending to help you stay on track.

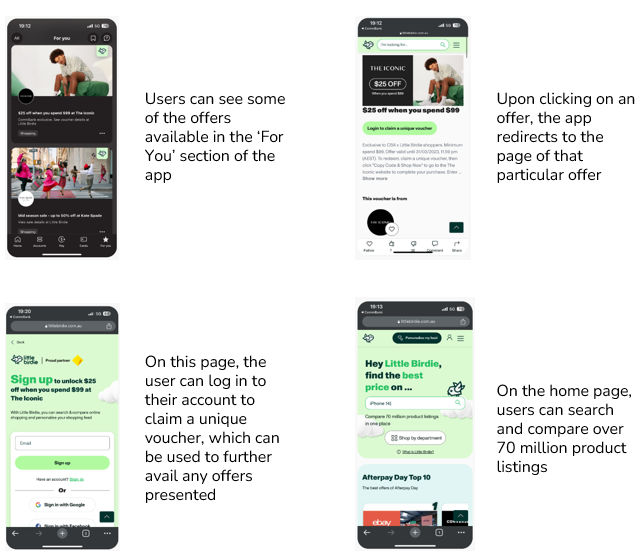

#3 Personalised offers

Little Birdie

- Little Birdie is integrated into the ‘For You’ section of the bank’s app and can also be accessed through the bank’s website and the Little Birdie website.

- Being a partner of CBA, the app provides certain exclusive offers which are only available to CommBank’s customers.

- The website includes certain popular categories like Afterpay, Day Top 10, Top 10 in Australia today, and various other Top 10 listings where the users can see what products are trending on certain days.

- Customers can also personalise their shopping feed based on the departments, brands and stores of their liking.

Kakao Bank

Background

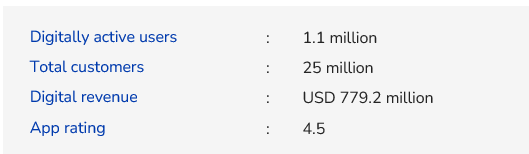

- Kakao bank is a South Korean mobile-only digital bank founded in 2016 by Korean Investment Holdings Kakao Corp.

- The association with KakaoTalk helped the bank capture more than 300,000 users within 24 hours of its launch and another 5 million users within six months.

I love it. Sending and receiving money to and from abroad is quick. It also helps me save money on these transactions.

– (Kakao Bank user)

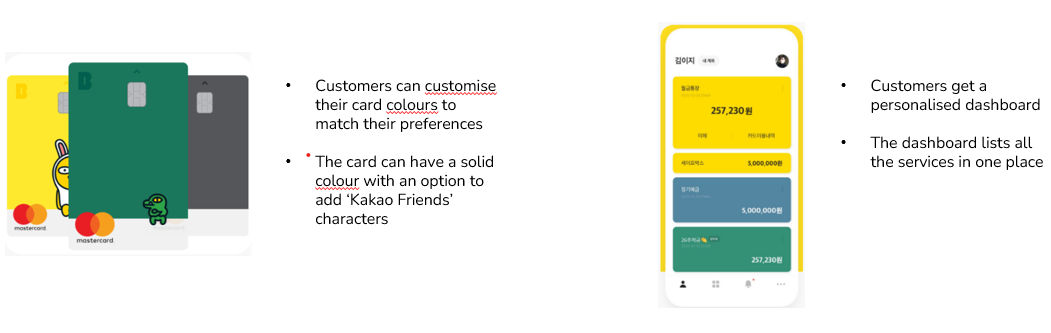

#1 Customization (Cards and dashboards)

#2 Gamification

Fun 26-week deposit challenges

- The 26-week challenge is a 26-week instalment savings feature

- Deposit payments grow incrementally by the initial subscription amount

- Subscription amounts can be from 1000, 2000, 3000, 5000 and 10000 won

- Customers can deposit together with Kakao friends and Niniz

Group account

- The feature allows customers to convert their account to a group account with up to 100 people

- Customers can invite their KakaoTalk friends directly to the group account

- A group member does not necessarily have to be a Kakao Bank customer

- The transactions details of each person are seen in real-time

#3 Saving tools

- A safe within the account for separate savings and surplus funds

- Customers can deposit up to 100 million won and earn a return of 2% per annum

- The Piggy Bank feature can automatically save up to 100,000 won by collecting small change within the main account

- Customers can choose from the automatic collection and coin collection modes

- The automatic collection allows collection according to the deposit and withdrawal patterns

- Coin collection only collects the loose change

Revolut

Background

- Revolut is a neobank and a financial technology company founded in 2015 and headquartered in London

- The bank conducted more than 330 million transactions each month towards the end of 2022

- The bank is expected to launch a Revolut ‘Lite’ app, which will be a streamlined version of the app for third-world nations with limited network infrastructure and slow internet speeds

Couldn’t ask for better customer service. Easy to use app. I received a virtual card as soon as I was verified. I had never used this type of financial app before. They made it very comfortable & easy to ask questions and figure out things.

– (Revolut user)

#1 Budgeting

- Pocket allows users to organise their bills and put money aside for these expenses

- Customers can view all their bills in one place under the primary dashboard

- Bills are automatically paid from Pockets

- The app calculates spending limits and recommendations based on the spending predictions

- Customers can also set how much they want to spend on the app

- Insights help track the financial progress on a weekly basis

#2 Analytics and personalisation

- Customers can link their other bank accounts to the app

- This allows them to see their external balances and transactions in the Revolut app

- Customers can earn up to 30% cashback when they eat out

- The app provides personalised offers and discounts for customers to spend on the brands they love

Up Bank

Background

- Up is an Australian neobank founded in 2018 and is based in Melbourne

- Up was established as a partnership between Bendigo bank and Ferocia, a fintech company

- Up Bank is known for its user-friendly app and customer service, as well as its commitment to transparency and ethical banking practices.

- It is a popular choice among Australians looking for a modern, digital banking experience.

I love being able to forward payments and set up multiple savers so I can see my progress on each one… Plus, they invest ethically. And they communicate.

– (Up bank user)

#1 Saving tools

Savers

- Savers allow customers to select between two modes – savings in general or for a particular expense

- Savers can be used individually or with another person sharing the same goal

- Savings can be automatically deposited in the saver on a fortnight, weekly, or monthly basis

Maybuy

- Maybuy is a form of Save Now, Buy Later (SNBL) model

- Customers can add a product to the bank’s app and start savings by picking a savings schedule

- This allows the customers to purchase products they really want with money they already have

- By the time the money is saved, a customer might not need the product, thereby eliminating impulsive purchases

#2 Gamification (2Up and Save Up)

2Up

- 2Up is an initiative that helps two individuals come together to share expenses, track their spending and save towards a common financial goal

- Allows 2 people to share 1 account, separate from their personal accounts

- Customers get a shared debit card, which they can use to set up joint savers and get instant digital cards

Save Up

- Save Up challenge aims to help customers save AUD 1000 (USD 672) in a year

- Customers can choose an amount to be set aside every week

- The customers move up a level every week they set aside the amount for that week

- Customers can challenge their friends on their savings journey

#3 Budgeting and tracking

Savers

- The Up tracker helps to track spending on different categories

- Customers can choose from the 40 available categories to track and set an upper spend limit on it and see the progress throughout the month

- Multiple trackers can be set on different categories and can be managed through ‘Monthly Insights’

Maybuy

- Upcoming bills allow customers to manage all their subscriptions in one place

- The app learns from regular charges and predicts when the next charge will be made

- This allows the customer to know how much money they will have to spend in future weeks

- The tool also helps customers save on penalties in case of late fee payments