Key Highlights

The Indonesian banking sector demonstrated significant growth in Q3 2024, showcasing resilience amid evolving market conditions, including the hike and fluctuations in interest rates.

- Revenue Growth:

- Net revenue of the top 5 banks- BCA, BNI, Bank Mandiri, BRI and Bank Danamon- increased by 8.94% YoY, reaching USD 12.8 billion, compared to USD 11.7 billion in Q3 2023.

- Bank Central Asia (BCA) led with an 11.24% growth, achieving USD 2.7 billion in net revenue.

- Profitability:

- Consolidated net profits rose 9.52% YoY, amounting to USD 5 billion in Q3 2024.

- Top performers included:

- BCA: Net profit growth of 16.39%.

- Bank Mandiri: Net profit increase of 11.81%.

- Bank Danamon’s profits declined by 16.71%, driven by a 47.2% rise in interest expenses.

- Fee-Based Income:

- Fee income grew 10.47% YoY, reaching USD 2 billion in Q3 2024.

- Strong growth was recorded by:

- Bank Danamon: 27.2% increase.

- Bank Mandiri: 15.73% increase.

This growth was driven by the expansion of digital banking services and the rise in digital transactions.

- Net Interest Margin (NIM):

- Average NIM declined by 39 basis points to 6.01%, primarily due to higher funding costs.

- Largest declines were reported by:

- Bank Danamon: -100 bps, now at 7.1%.

- Bank Mandiri: -73 bps, now at 4.86%.

- Non-performing loans

- Non-performing loans (NPL) improved, with the average decreasing to 2.03%.

- Notable changes:

- Bank Mandiri: Significant improvement, NPL reduced to 1.13.

- BCA: Slight rise in NPL to 2.1%.

- Cost Efficiency:

- The cost-efficiency ratio slightly increased, moving to 41.61% in Q3 2024 from 42.05% in Q3 2023.

- Bank Danamon recorded the highest cost-efficiency ratio at 57.7%, exceeding the industry average of 42% in Indonesia, driven by a 10% QoQ growth in non-interest income in Q3 2024.

Embracing digital transformation

In a landscape increasingly defined by digitalisation, these banks are leading in initiatives that enhance both security and customer engagement:

- Bank Danamon’s innovation through technology

- Machine learning for efficiency: Implemented a Cloudera-powered machine-learning platform to enhance customer marketing, fraud detection, and anti-money laundering processes by processing over one terabyte of data daily.

- AI in HR management: Integrated SAP Business AI, including Joule, for personalized candidate matching and improved employee engagement with AI-driven insights.

- BNI’s innovative digital solutions

- Support for MSMEs via digital financing: Partnered with fintech lender Batumbu to provide IDR 1.2 trillion in loans to MSMEs, demonstrating support for economic growth through digital solutions.

- Seamless corporate banking with BNIdirect: Integrated all wholesale channels with Single Sign-On to simplify corporate banking experiences.

- Financial wellness with Wondr: Offers an automated financial recap to help customers monitor income, expenses, and spending habits, thereby promoting informed financial decisions.

- Bank BRI’s BRIMO app enhancements

- Enhanced app features: Introduced NFC payments, multi-currency cards, and QR cross-border payments, boosting the customer experience. Additional features include gold savings, travel, groceries, and the Sabrina chat banking service.

- Bank Mandiri’s Livin app upgrade

- Investment and financing features: Launched smart investment options through Growin integration and flexible vehicle financing, catering to varied customer needs.

Revenue

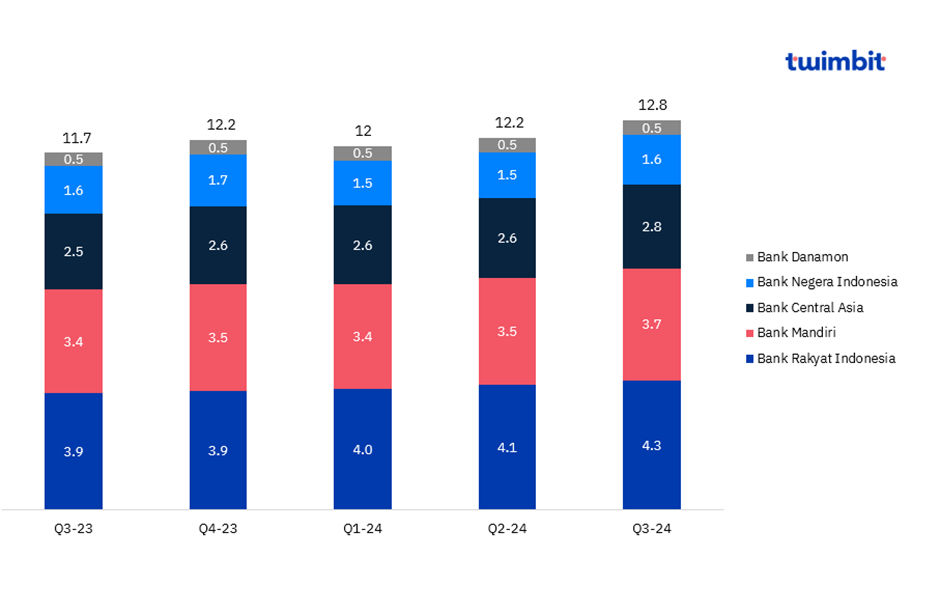

Exhibit 1: Net revenue of the top 5 banks in Indonesia

Figures in USD Billion

Source: Bank Financials, Twimbit analysis

Net revenue increased by 8.94% YoY, reaching USD 12.8 billion in Q3 2024, up from USD 11.7 billion in Q3 2023.

The top five banks in Indonesia saw their revenues rise from USD 11.7 billion in Q3 2023 to USD 12.8 billion in Q3 2024.

Bank Central Asia

- BCA reported the highest YoY growth in net revenue, with an increase of 11.24% in Q3 2024.

- Net revenue grew from USD 2.4 billion in Q3 2023 to USD 2.7 billion in Q3 2024.

- Net interest income grew by 9.04%, increasing from USD 5.2 billion to USD 5.6 billion.

- Loan receivables grew by 17% YoY, rising from USD 4 billion in Q3 2023 to USD 4.6 billion in Q3 2024.

Profitability

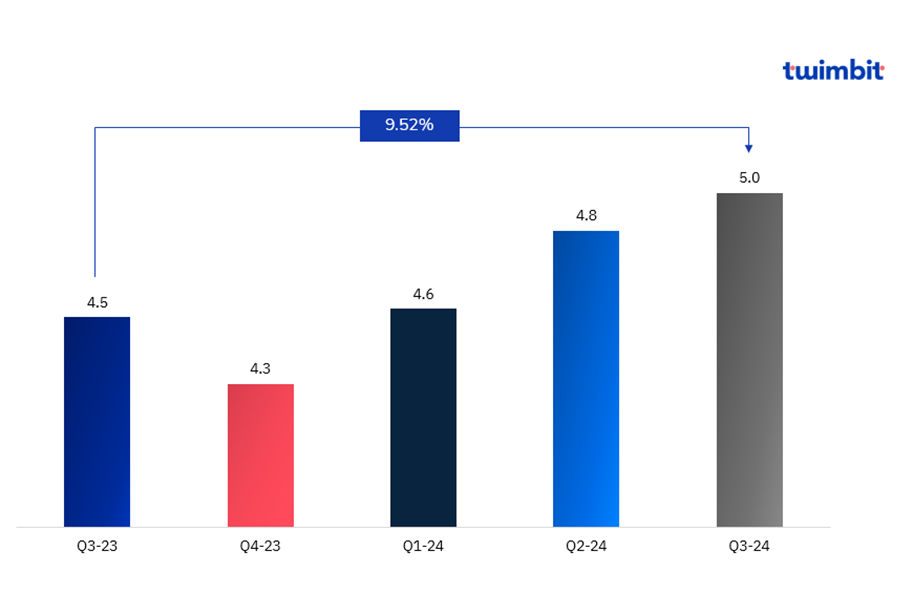

Exhibit 2: Consolidated net profit of the top 5 banks in Indonesia

Figures in USD Billion

Source: Bank Financials, Twimbit analysis

Net profits grew by 9.52% YoY to USD 5 billion in Q3 2024 compared to Q3 2023.

The top 5 banks in Indonesia aggregated their net profits from USD 4.5 billion in Q3 2023 to USD 5 billion in Q3 2024. The top 3 – Bank Mandiri, Bank Rakyat Indonesia, and BCA reported combined net profits of USD 4.3 billion (86% of overall net profits) in Q3 2024.

- Bank Mandiri saw an increase of 11.81% in their net profits

- BCA boosted its net profits by 16.39%

- BRI reported an increase of 5.41% in net profits

- Bank Negara Indonesia reported a modest 3.03% increase in net profits.

- Bank Danamon saw a decline of 16.71% in their net profits

The decline in Bank Danamon’s performance was mainly driven by a 47.2% increase in interest expenses, rising from USD 356.7 million in Q3 2023 to USD 525.1 million in Q3 2024.

Fee-based Income

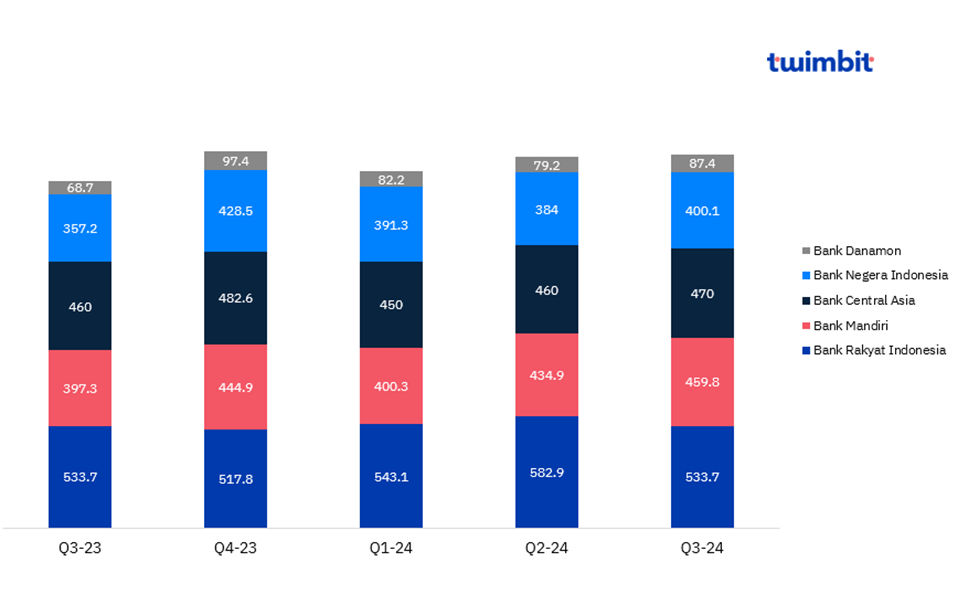

Exhibit 3: Fee Income of the top 5 banks in Indonesia

Source: Bank Financials, Twimbit analysis

Fee income increased by 10.47%, reaching USD 2 billion in Q3 2024, compared to USD 1.8 billion in Q3 2023.

Bank Danamon reported the highest growth at 27.2% YoY, from USD 68.7 million in Q3 2023 to USD 87.4 million in Q3 2024. Bank Mandiri reported the second-highest growth at 15.73%, from USD 397.3 million to USD 459.8 million.

Overall, the top 5 banks in Indonesia have experienced growth in fee income, driven by the following factors:

- Growth in digital transactions: As digital banking users grow to 69% of the total customer base in 2024, higher transaction volumes on online platforms drive an increase in fee-based income, with fees from services like fund transfers, bill payments, and premium features.

- Diversification and innovation and services: Banks have expanded their service offerings, including wealth management, insurance, and investment products while introducing new, customer-tailored financial solutions. As banks offer specialised financial solutions, customers are charged fees for advisory services, asset management, and transactions.

Net Interest Margin (NIM)

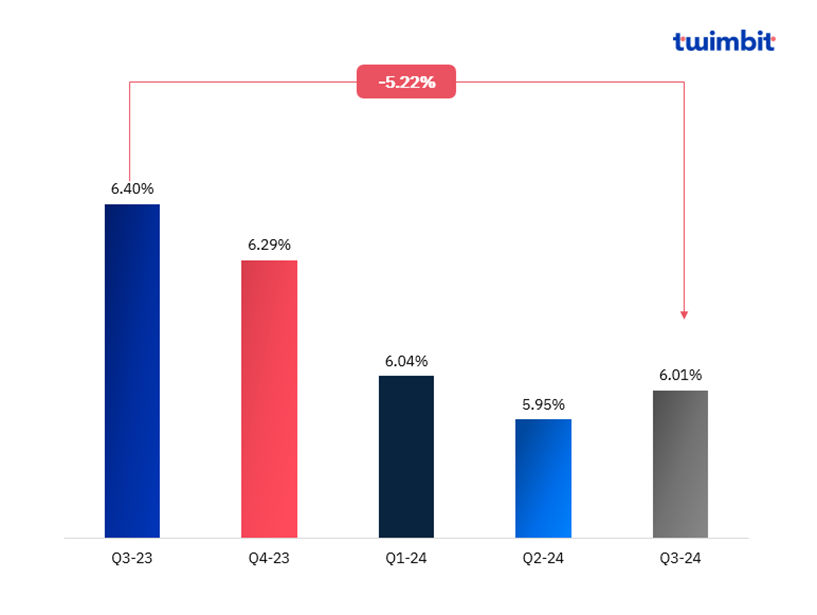

Exhibit 4: Average NIM of the top 5 banks in Indonesia

NIM decreased by 39 basis points, falling to 6.01% in Q3 2024, compared to 6.40% in Q3 2023.

- Bank Mandiri reported a 73-bps decline in its NIM, which now stands at 4.86%.

- Bank Danamon’s NIM dropped by 100 bps, now reaching 7.1%.

- BRI reported a 25-bps decline in its NIM, which now stands at 7.8%.

- BCA reported a 40-bps increase in its NIM, currently standing at 5.9%

- BNI reported a 38-bps decline in its NIM, which now stands at 4.4%.

Overall, banks in Indonesia have experienced a decline in their NIM, primarily driven by higher funding costs due to rising interest rates, which have negatively impacted their net interest margins.

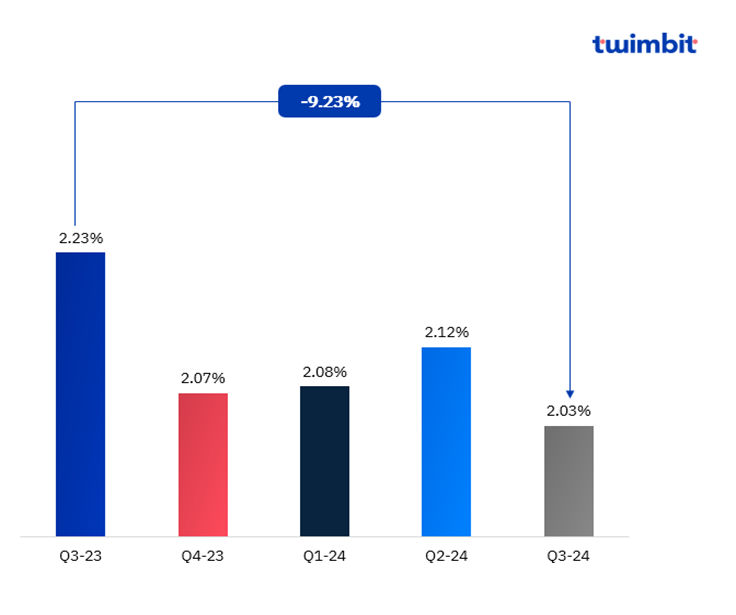

Non-performing loans (NPL)

Exhibit 5: Average NPL of the top 5 banks in Indonesia

The average NPL of the top 5 banks decreased from 2.23% in Q3 2023 to 2.03% in Q3 2024.

- Bank Mandiri’s NPL fell by 24.16% YoY, from 1.49% in Q3 2023 to 1.13% in Q3 2024.\

- Bank Mandiri’s reduction in NPLs is primarily driven by enhanced asset quality, supported by effective risk management and lower credit.

- BCA’s NPL increased by 5% YoY, rising from 2.0% in Q3 2023 to 2.1% in Q3 2024.

- The rise in NPLs is driven by a combination of slower economic growth, higher interest rates, and increased funding costs.

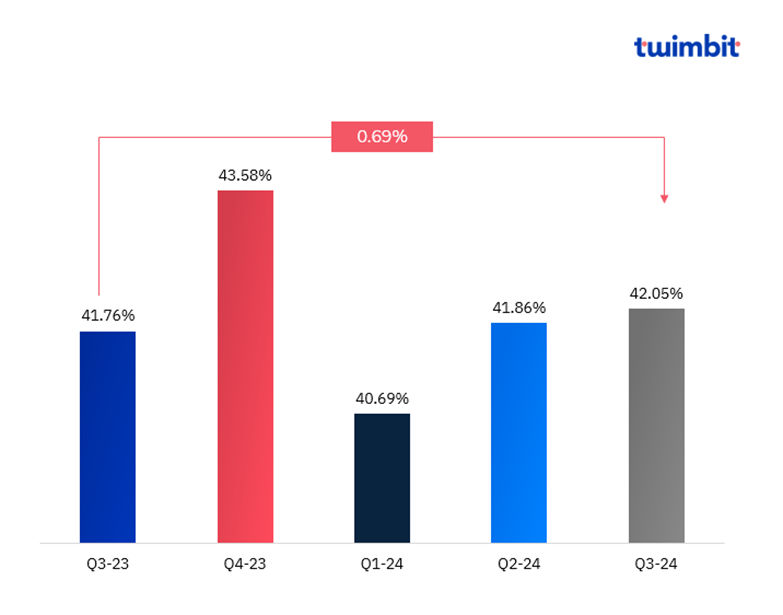

Cost Efficiency (CE)

Exhibit 6: Average cost-efficiency ratio of the top 5 banks in Indonesia

The average cost-efficiency ratio for the top 5 banks in Indonesia was 42.05% in Q3 2024. Indonesian banks generally exhibit stronger operational efficiency than their peers in the APAC region.

It is important to highlight that these banks have seen an increase in cost efficiency this quarter compared to Q3 2023, when cost efficiency was recorded at 41.76%. Additionally, the average cost efficiency has increased compared to the previous quarter, which saw a cost efficiency of 41.86%.

Four of the five banks analysed have cost-efficiency ratios well below the 42% threshold, which is the industry average in Indonesia. In contrast, Bank Danamon reported a cost-efficiency ratio of 57.7%, surpassing the threshold, driven by a 10% quarter-on-quarter growth in non-interest income in Q3 2024.

Outlook

Recent interest rate hikes by Bank Indonesia represent a calculated effort to stabilize the rupiah amid heightened geopolitical tensions and global economic uncertainties. These measures align with significant developments on the international stage, particularly in the United States. By adopting a proactive stance, the central bank aims to keep inflation within target levels while supporting Indonesia’s broader economic goals—such as boosting income per capita, establishing the nation as the world’s fifth-largest economy, and achieving social equity and poverty reduction.

Complementing these monetary policies, Indonesian banks are accelerating their digital transformation to drive growth and innovation. A notable initiative in this space is the launch of Sahabat-AI, a platform designed to enhance business-to-government (B2G) and business-to-business (B2B) interactions through AI-powered solutions. For the banking sector, Sahabat-AI offers an opportunity to deliver more personalized and efficient services, improving customer satisfaction and fostering loyalty. By leveraging this technology, banks can provide faster, more inclusive financial services, significantly boosting operational efficiency and expanding their customer reach.

As the sector adapts to these transformative changes, it must also navigate external pressures, such as interest rate volatility. Sustained investments in innovation and customer-centric solutions will be critical for Indonesian banks as they address challenges and capitalize on emerging opportunities. In doing so, they demonstrate resilience and position themselves to thrive amid shifting global economic dynamics.