The Indonesian banking sector delivered an excellent performance in Q2 2023, with net revenues growing by 6.7% YoY (year-on-year). This performance was underpinned by the country’s continued economic expansion and its ability to withstand global headwinds. This performance was further boosted by robust loan growth of 11.4% YoY, driven by the strong demand from the corporate and retail sectors. The decline in non-performing loans also helped Indonesian banks boost their interest incomes.

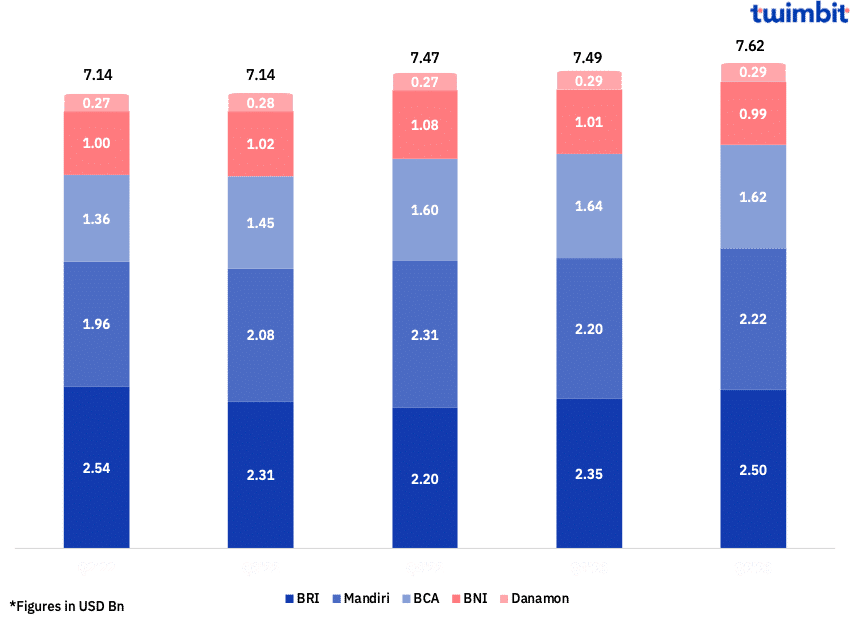

Net revenues for the top 5 banks in Indonesia grew by 6.7% YoY

The top 5 banks in Indonesia grew from USD 7.14 billion in Q2 2022 to USD 7.62 billion in Q2 2023.

BCA reported the highest YoY growth rate at 19.48%, increasing net revenues from USD 1.36 billion in Q2 2022 to USD 1.62 billion in Q2 2023. This growth was driven by a 21.5% increase in net interest income and a 13.7% increase in non-interest income. The loan portfolio of the bank increased by 9% from USD 44.8 billion to USD 48.8 billion.

BRI reported a YoY decline at 1.82%, decreasing net revenues from USD 2.54 billion in Q2 2022 to USD 2.50 billion in Q2 2023. Throughout 2022, the bank disbursed MSME loans worth USD 56 billion to more than 14 million micro entrepreneurs. This represented a YoY growth of 10.1%. Despite this, the increase in the bank’s overall income has been modest in recent quarters. The total income grew by a mere 2.61% between Q2 2022 and Q2 2023, this overall increase was not adequate to offset the 2.78% increase in overall operating expenditure. The major contributor towards this increase were the general and administrative expenses which grew by 13.7% from USD 406 million in Q2 2022 to USD 462 million in Q2 2023.

Exhibit 1: Net revenues of the top 5 Indonesian banks

Net profit for the top 5 banks in Indonesia grew by 13.4% YoY

The top 5 banks in Indonesia aggregated their net profits from USD 2.55 billion in Q2 2022 to USD 2.9 billion in Q2 2023.

On average, the top 3 Indonesian banks were Bank Mandiri, BRI and BCA, which led the chart with an average net profit of USD 836 million in Q2 2023. Individually, Bank Mandiri and BCA net profits grew by 24.5% and 26.8%, while BRI reported a decline of 1.47% in net profits, respectively.

Exhibit 2: Consolidated net profits of the top 5 Indonesian banks

There were several factors for the increase in net profits – improving asset quality, higher margins and a robust loan growth at 11.4% YoY.

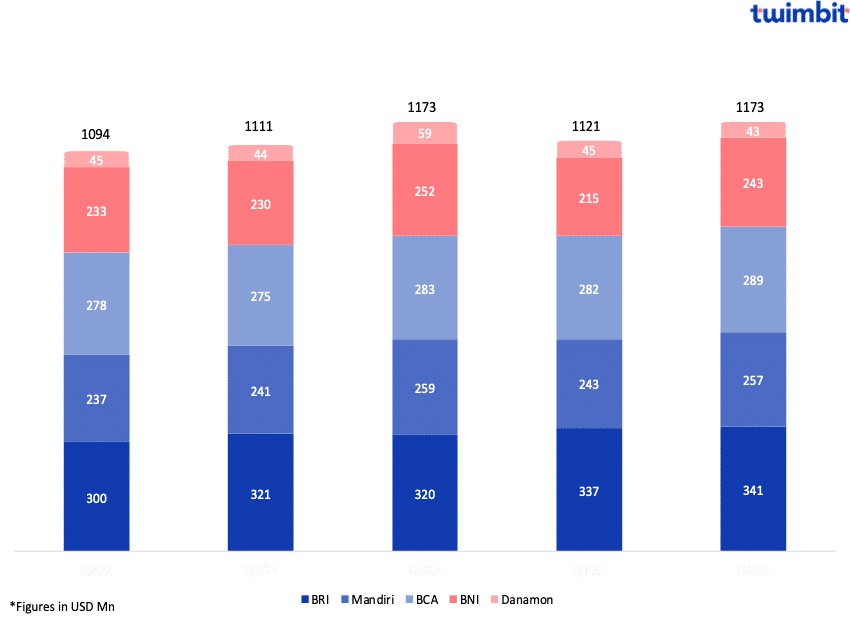

Fee income for the top 5 banks in Indonesia grew by 7.26% YoY

The top 5 banks in Indonesia increased their fee income from USD 1.09 billion in Q2 2022 to USD 1.17 billion in Q2 2023

BRI reported the highest increase in fee income at 13.61% YoY, from USD 300 million in Q2 2022 to USD 341 million in Q2 2023. This growth was primarily driven by traditional sources and included a 50% increase in trade finance and investment banking fees and a 37% increase in loan administration fees.

Exhibit 3: Fee incomes of the top 5 banks in Indonesia

Overall, the top 5 banks in Indonesia have witnessed an increase in their fee incomes due to the following factors:

- Digital transformation – The shift to being more digital-centric has opened up fresh opportunities for banks to generate fee revenue. Banks can now charge fees for a variety of digital services, such as mobile banking transactions, online bill payments and various digital financial products.

- Growing middle class – The substantial and expanding middle-class population of Indonesia currently drives the demand for financial products and services, fuelling the need for financial offerings. This encompasses fee-generating products and services, such as credit cards, investment opportunities and insurance.

- Rising incomes – Rising income levels in Indonesia are driving fee income growth. Higher-earning consumers are more willing to make purchases using credit cards, use BNPL services, buy bancassurance and invest in wealth management, all of these services attract fees.

BCA is considering forming a joint venture with a foreign partner, forging a bancassurance partnership. This will enable the insurer to offer its products and services in the bank’s branch for a specified duration. This could help BCA create a new source of non-interest income through fee income.

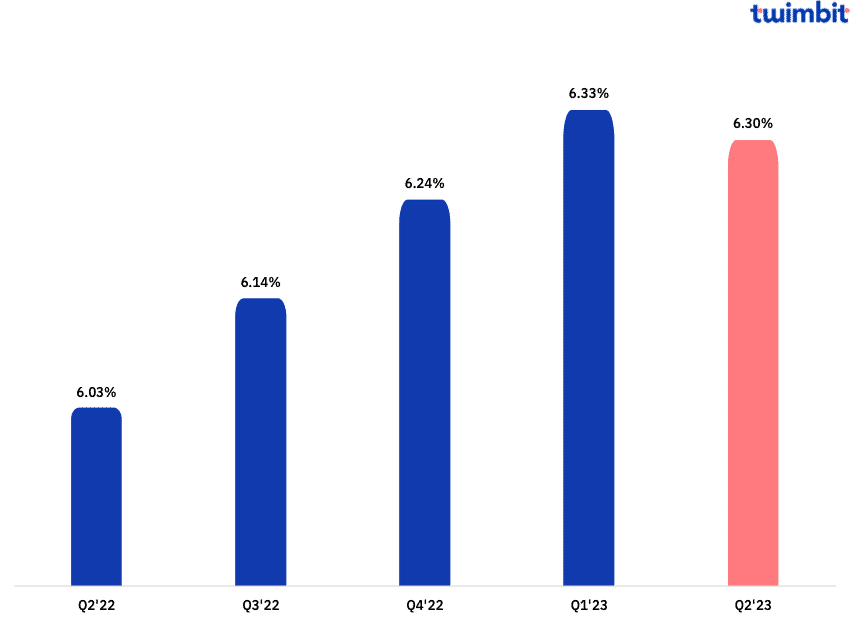

Net interest margins (NIM) dipped slightly by 3 basis points in Q2 2023

The average NIM dropped from 6.33% in Q1 2023 to 6.3% in Q2 2023. However, theimproving asset quality led to a 27 bps increase (Figure 4) in the average NIMs between Q2 2022 and Q2 2023. The current average NIM for Indonesian banks stands at 6.3% which is the highest in APAC and double the APAC average of 3.16%. It should be noted that Danamon and BRI have very healthy NIMs at 8.1% and 7.85% respectively and have the highest NIMs in APAC.

Exhibit 4: Consolidated net interest margins of the top 5 banks in Indonesia

Indonesian banks tend to have high NIMs when compared to other APAC regions due to the following factors:

- High loan rates – Indonesian banks charge higher interest rates on loans than banks in other countries due to the country’s high risk of default and high cost of funds.

- Low deposit rates – The large savings pool in the Indonesian banking sector gives banks more flexibility, as they do not need to compete as aggressively for deposits. This allows the banks in Indonesia to pay lower deposit rates than banks in other countries.

The difference between the high loan rates and low deposit rates in Indonesian banks has helped best position them to boost their margins.

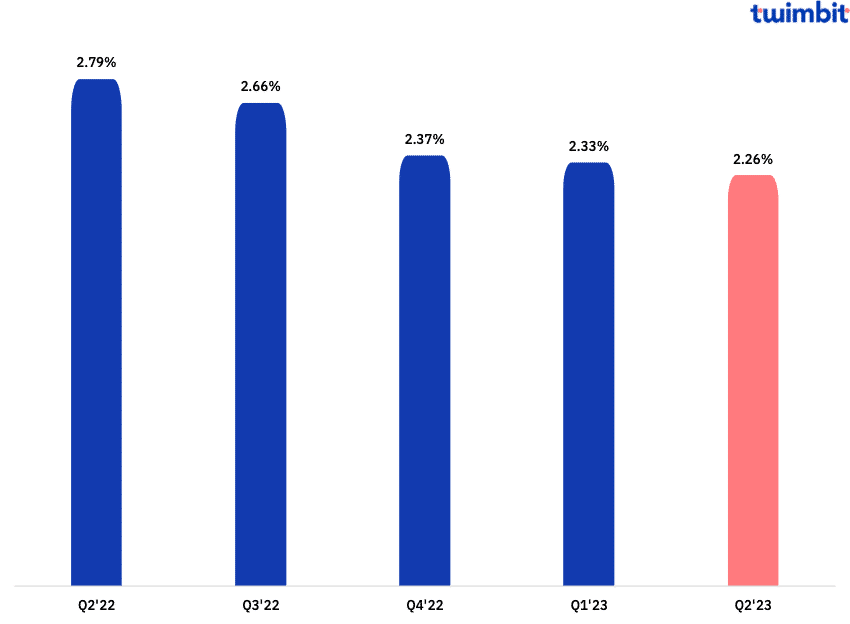

NPLs for the top 5 banks in Indonesia declined by 53 basis points

The top 5 banks in Indonesia reported a decline in average non-performing loans (NPLs), from 2.79% in Q2 2022 to 2.26% in Q2 2023.

Bank Mandiri reported the lowest non-performing loan (NPL) in Q2 2023, with a decline of 32.35% YoY, from 2.42% in Q2 2022 to 1.64% in Q2 2023.

BCA reported the second-lowest NPL in Q2 2023, with a decline of 13.64% YoY, from 2.2% in Q2 2022 to 1.9% in Q2 2023.

BRI reported the highest NPL in Q2 2023 at 2.95%, however, the bank witnessed a decline of 11.14% YoY from the previous NPL of 3.32% in Q2 2022.

Exhibit 5: Consolidated NPL of the top 5 banks in Indonesia

Indonesian banks have been able to maintain low levels of NPLs due to the following factors:

- Government support – The Indonesian government supports the banking sector with loan guarantees and other forms of assistance. This helps to reduce the risk of defaults and NPLs.

- Conservative lending practices – These practices include stringent credit checks. This helps banks in Indonesia to reduce the number of loans made to borrowers.

- Use of AI for credit assessment – Automated loan processing with predetermined creditworthiness levels can reject applicants who do not meet the bank’s minimum credit criteria.

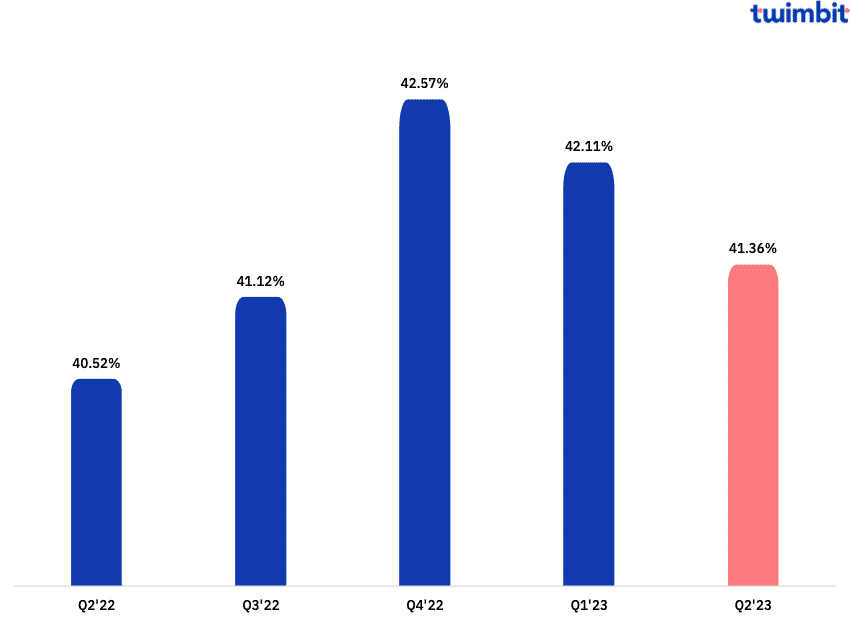

Cost efficiency for the top 5 banks in Indonesia declined by 0.84% between Q2 2022 and Q2 2023

The average cost efficiency for the top 5 banks in Indonesia stood at 41.36% in Q2 2023, below the APAC average of 42% in Q2 2023. This indicates a greater level of operational efficiency in Indonesian banks as compared to their APAC peers. However, it should be noted that these banks have experienced a higher cost efficiency in this quarter compared to Q2 2022 when the cost efficiency stood at 40.52%.

Exhibit 6: Consolidated cost-efficiency ratio of the top 5 banks in Indonesia

Four of the five banks analysed have their cost efficiency ratios way below the threshold value of 50% with BCA leading with an impressive ratio of 31%. However, Danamon reported a cost-efficiency ratio of 56% which is above the threshold value.

Initiatives by the top 4 banks in Indonesia

- #1 BRI

Hybrid Bank Business Model – The Bank is trying to combine its physical presence and digital capabilities to provide a phygital experience for its customers. This experience is further driven by Big Data and Artificial Intelligence.

Physical:

- 7,980 outlets and 587,839 e-channels

- 666,038 BRILink agents for branchless banking

- 27,000+ financial advisors

Digital capabilities:

- Digitising core – Digitise business processes to boost productivity.

- BRISPOT – It is a digital initiative by BRI to improve productivity and efficiency by digitizing loan processes through the use of a mobile application. The mobile application has allowed for the following:

- Paperless loan application with approvals in less than a day

- Automatic prescreening and disbursement

- Built-in cross-selling modules

- BRISPOT – It is a digital initiative by BRI to improve productivity and efficiency by digitizing loan processes through the use of a mobile application. The mobile application has allowed for the following:

- Digital ecosystem – Building ecosystems will help BRI leverage new liquidity, new opportunities and new growth avenues.

- New digital propositions – Create an independent greenfield digital bank to tap the untapped segment and embed it in customers’ lives.

- #2 Bank Mandiri

Livin Super App – 70 comprehensive use cases for banking and beyond banking solutions for retail customers

- Customers can open an instant account in less than five minutes

- Allows customers to open a savings account in 120 countries using a local SIM card

- Allows customers to use multiple options for QR payments, including savings accounts, and credit cards and pay later

- Became the first bank in Indonesia to integrate four e-wallet market leaders into the app

- Offers a wide range of investment options ranging from bonds to mutual funds

- Became the first bank in Indonesia to offer instant cross-border remittances

- Provides an extensive array of retail loans catering to the extensive needs of customers

- Digitised personal loans with instant approvals

- Credit card instalments of up to 36 months

Kopra – A comprehensive digital super platform for business clients

- Provides complete wholesale solutions from cash management and trade and working capital solutions to treasury solutions

- Host-to-host connectivity allows connection with the bank’s wholesale client-server and IT systems for seamless integration

*Bank Mandiri is expected to integrate Livin and Kopra into a unified platform by the end of 2023.

Smart Branches – The bank is transforming its physical branches into three different types of smart branches based on the locations they are in. The bank has already transformed 241 existing branches into smart branches.

- Upgraded branch – These fully self-service digital smart branches are located in shopping centres, airports, train stations, bus terminals and public areas.

- Hybrid branch – These branches have limited assisted smart branches that focus on meeting customers’ business needs. These branches are located in hospitals, business centres and office buildings.

- Digital box – These are fully assisted smart branches that require expertise and various financial needs. These branches are located in traditional markets, factory areas and commercial areas.

- #3 BCA

Blu – A digital-only bank

- Bank Digital BCA recorded total assets of USD 1.11 billion as of December 2022.

- The Blu app has more than 1 million active customers. This is generating significant fee income for the bank.

- Blu has collected third-party funds of USD 0.69 billion as of December 2022.

- Blu provides features such as:

- bluAccount – online bank account opening

- bluSaving – manage budgeting with 10 saving accounts

- bluGether – utilize saving account functions like a treasury account

- bluDeposit – for easier deposit top-up

- #4 BNI

Mobile banking Super Apps ecosystem – BNI is continuously expanding its services leveraging its ecosystem. The aim is to respond to each evolving customer demand through digital banking and help customers achieve their financial goals.

- All in on digital wealth management – mutual funds, bonds and gold savings

- Digital loan & credit card – credit card, consumer loan, credit scoring, digital signatures

- Digital lifestyle – voucher games, voucher streaming, e-vouchers, phone & and data package

- Personal financial management – life goals, spending trackers, budgeting

Currently, the app has more than 6,500 billers offering ~450 services ranging from payments, ticketing and utility bill payments to e-wallets and finance solutions.

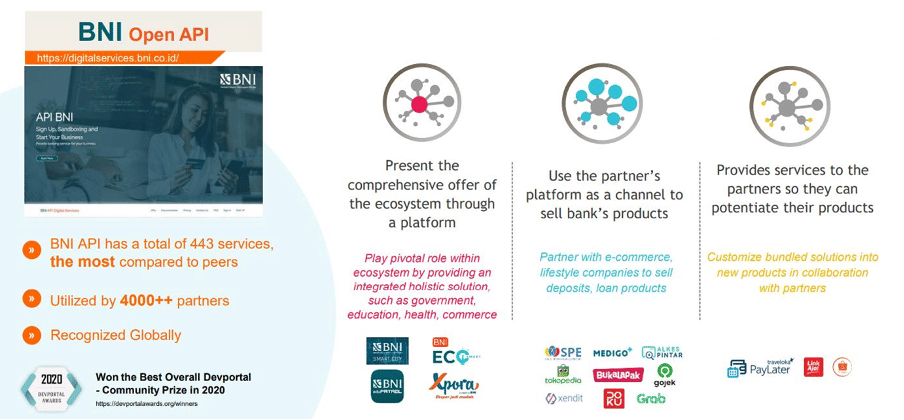

Open Banking – BNI Open API has 280 regulator-approved services which is the highest among its peers. These services are utilised by more than 4,000 partners. The bank optimises all three possible roles in every ecosystem.

Exhibit 7: BNI’s API stack

The Indonesian banking sector is set for a favourable H2 2023

The robust economic expansion and its capacity to withstand global economic disturbances are key factors to Indonesia’s continued success in the banking sector. Anticipated factors contributing to this positive outlook also include sustained vigour in loan expansion propelled by heightened demand from both corporate and retail segments.

Additionally, it is anticipated that asset quality will continue to be effectively managed. However, it should be taken into account that the rising interest rates (a result of multiple rate hikes by Bank Indonesia to combat inflation), may result in increased borrowing costs for both businesses and consumers, which could potentially offset the loan expansion.

To learn more about how the top banks in APAC performed in Q2 2023, click here.

To learn more about how the leading 8 banks in India performed in Q2 2023, click here.

To learn more about how the leading 9 banks in Malaysia performed in Q2 2023, click here.

To learn more about how the leading 4 banks in the Philippines performed in Q2 2023, click here.