BNPL (Buy Now Pay Later) is quickly becoming a disruptive growth opportunity for banks, fintech, platform companies, and the retail industry. BNPL facilitates consumption without incurring any upfront costs, proving itself as an alternative to traditional lending methods. It is a point-of-sale financing option that allows users to finance their purchase with a 0% interest loan.

The pandemic accelerated the shift to online shopping across all categories for everything from groceries to clothing and other daily necessities. BNPL became more than just a payment mechanism; it eased borrowers’ financial stress by offering no-cost EMIs. The symbiotic relationship between e-commerce and BNPL proves to hold a promising future. Consumer demand is expected to propel the Indian e-commerce industry to a $99 billion market by 2024. Following this, BNPL looks to be the fastest-growing online payment method, rising from 3% of total sales in 2020 to 9% in 20241.

There is considerable growth in demand for credit products in the country. The domestic credit growth in India from 2000 to 2021 averaged 15.1%. However, credit is still very complex and expensive with numerous hidden clauses, leading to extra charges and penalties for consumers.

A significant gap exists when accessing formal credit compared to other developed countries. Banks and financial institutions (FIs) are working to address this gap by introducing new payment products and instruments to make formal credit easily accessible.

With Fintech players releasing new and innovative products and services to consumers, they have disrupted the market, pushing for adopting online payments and BNPL.

Although BNPL initially targeted millennials because of their lack of access to credit cards, it has also gained popularity among the older age groups (35 – 54). In addition, BNPL can enter previously untapped markets, such as customers with no or low bureau scores. The enhanced customer satisfaction also allows BNPL users to become more integrated into day-to-day financial transactions. Overall, the Indian fintech market is flourishing, and it has been a favourite of venture capitalists.

Benchmarking India’s top 8 BNPL operators

Whether you’re planning to buy a brand-new iPhone or a new Zara blazer, you can opt to finance and split the cost over the next few days or a few months with BNPL. However, with numerous service providers entering this space, competition is very high, making it difficult to determine who is the best.

Therefore, we decided to benchmark India’s top 8 BNPL service providers against various parameters like credit limit, shopping experience, onboarding, repayments, and more. This benchmarking report will help users and businesses evaluate the primary clauses of these companies to help them make better-informed decisions.

Methodology

We made the initial shortlist based on the overall popularity of the service providers amongst the consumers. To ensure the data is accurate and relevant, we collected the data points in May 2022. Any new data published or posted to this date has not been included or updated in this report.

Then, we determined 10 parameters to benchmark BNPL service providers. These 10 parameters can be grouped into 3 primary categories. These categories include:

- Onboarding

- Payments

- Shopping experience and loyalty programs

Step 1

We opened basic (free) plan accounts with various top BNPL service providers – Paytm Postpaid, Slice, Amazon Pay, Flipkart Pay Later, ZestMoney, Simpl, LazyPay, and OlaMoney Postpaid.

Step 2

We created a framework to conduct a detailed evaluation and rank them. This framework assesses how these BNPL service providers performed based on the above categories, essential to delivering a seamless user experience.

Step 3

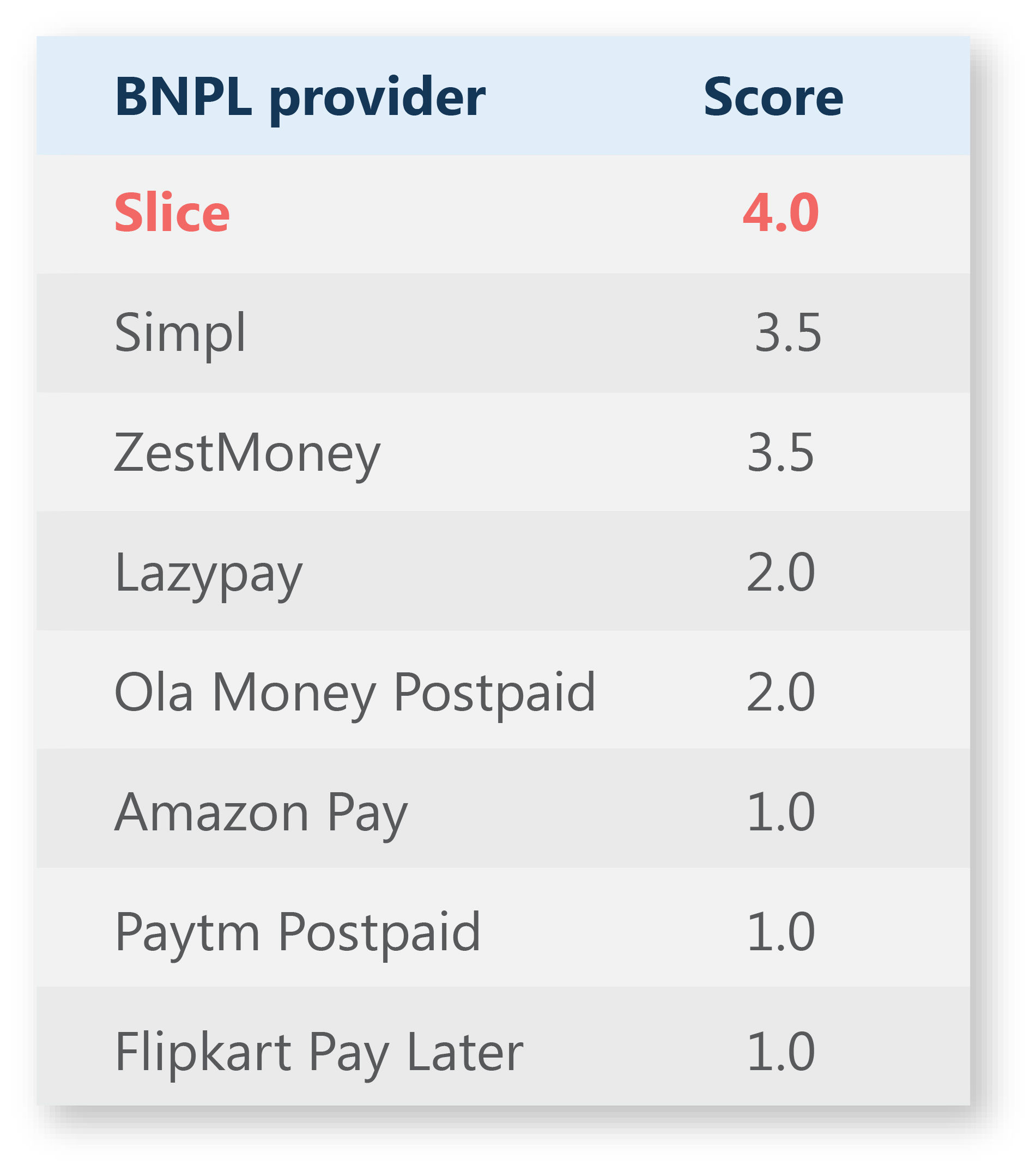

We scored them on a scale of 1 to 4 based on a customer’s relative experience with various service providers. On a scale of 1 to 4, 4 depicts best user’s relative experience and 1 depicts poor user’s relative experience.

twimbit’s top 8 BNPL service providers acing CX

Framework analysis for each parameter

#1 Onboarding

To get started with using BNPL, we analysed the following:

- Clarity of process

- Documents required

- Number of steps involved

- Time to onboard

We found that ZestMoney, Lazypay, and Simpl listed the clear steps and documents required for an account opening on their homepage or have a direct link to the same, providing easy access for users to any necessary information with just a few clicks. On the other hand, Paytm Postpaid has a static page with no option for a user to check the details for the onboarding process.

In the time taken to onboard user accounts, Simpl, Flipkart Pay Later, and ZestMoney scored a perfect 4. These service providers instantly activate the account, while others take somewhere from 5 minutes to 48 hours.

Simpl aced the onboarding parameter by clearly defining the processes and documents required. It also activates the account immediately, having the least number of steps.

#2 Payments

The flexibility and the terms at which a user gets to make payments make or break a BNPL product. From this, we identified 4 key parameters as follows:

- Initial spending limit

- Scope of increasing the credit limit

- Maximum late fee charges

- Repayment cycle

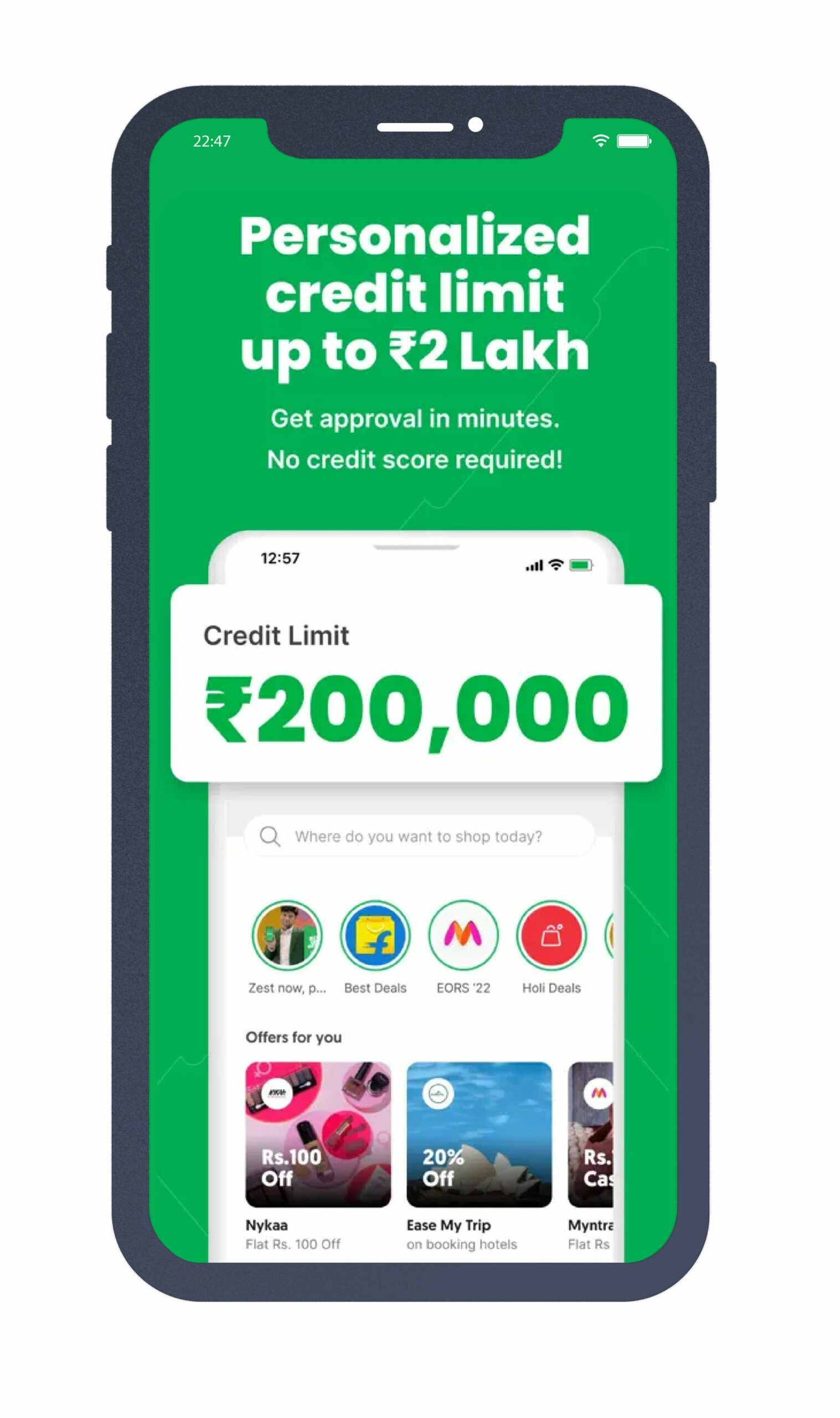

Most BNPL service providers keep the credit limit from INR 20,000 (USD $251.26) to INR 60,000 (USD $753.79), while Lazypay and ZestMoney offer up to INR 1,00,000 (USD $1256.32) and INR 2,00,000 (USD $2512.63), respectively. However, these limits may require a user to complete a full KYC per government mandate. Simpl allows users to request via the application directly, while others require users to get in touch with customer support to increase this limit.

Most BNPL service providers have a clause of grace period in case a user misses a payment, which is available for viewing in the documentation section or help centre. Post-grace period, the service provider charges a late payment fee, categorised into various tiers depending on loan size.

Maintaining all the parameters equally, we observed that most service providers charge anywhere between INR 150 (USD $1.88) to INR 800 (USD $10.05). However, Ola Money Postpaid has the highest fee, INR 1,000 ($12.56 – one time), while Simpl charges around INR 118 (USD $1.48).

The average repayment cycle can be 15 to 30 days. The only service provider providing a better repayment duration is Flipkart Pay Later (35 days). However, it is imperative to note the days represent the first partial payment due after purchase using the BNPL line of credit. In addition, many service providers allow users to convert the BNPL loan to a personal loan at attractive interest rates.

ZestMoney aced the payments parameter by offering an initial spending limit of INR 1,00,000 (USD $1256.32) and INR 2,00,000 (USD $2512.63), which the customer can raise upon request.

#3 Shopping experience and loyalty program

A customer stays for the experience and less for the features. To quantify the experience, we considered the following:

- Total partner stores where a user can transact using the BNPL line of credit

- Total cashback and rewards a user can attain and the frequency of rewards and cashbacks

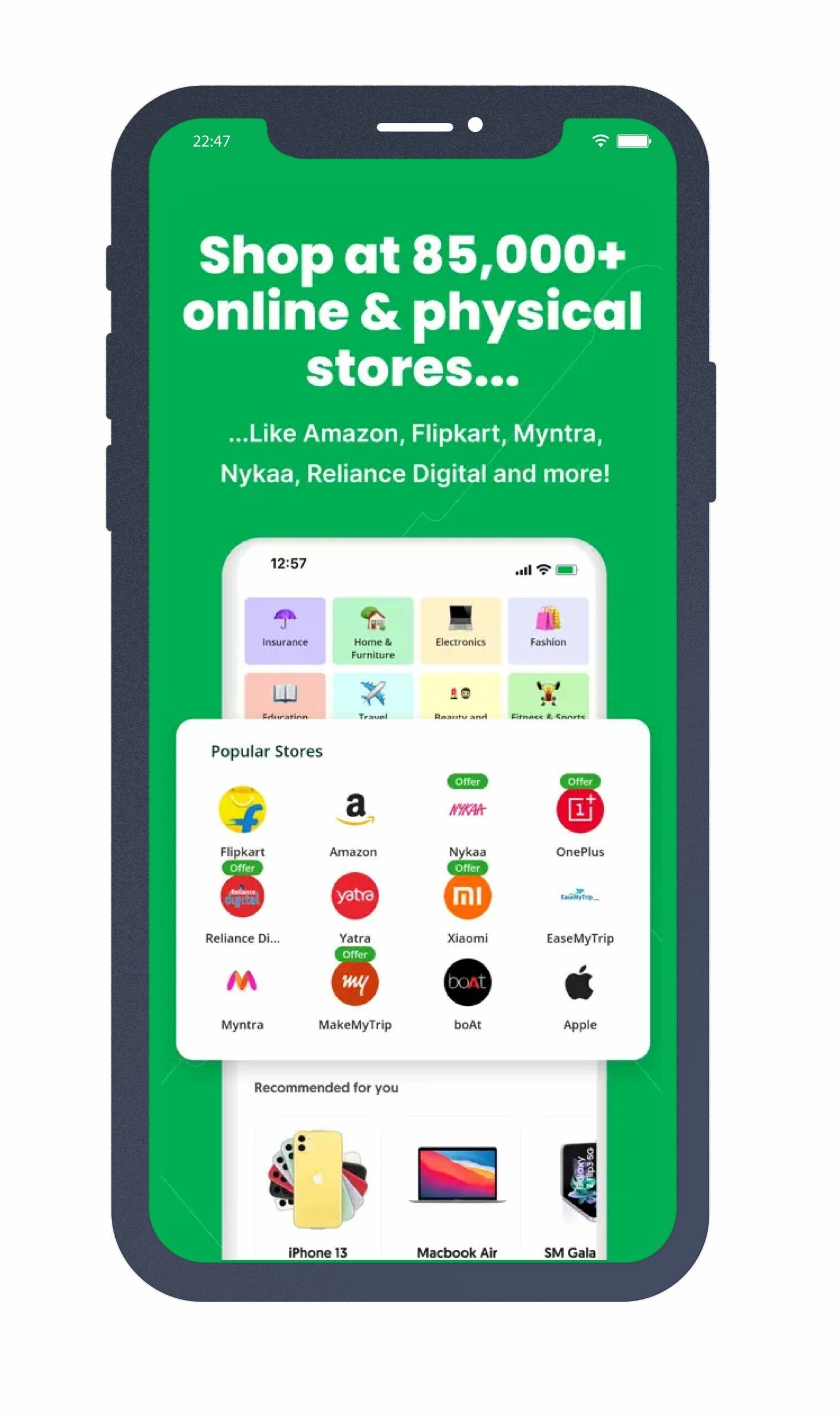

Zestmoney and Simpl have the largest network of partner stores, with 85,000 and 10,000+ stores, while Lazypay has an extensive network of offline stores.

Slice is the only service provider promising cashback on every purchase, while all others have periodic offers. In addition, most of these service providers offer discount coupons when a user opts to shop with their partner store.

Slice aced shopping experience and loyalty program by being the only service provider promising cashback on every purchase with a vast network of partner stores.

Analyst opinion and recommendations

Out of the 8 BNPL service providers evaluated, ZestMoney aced our list, followed by Simpl. Both these service providers have a superior UI/UX with exceptional clarity of information. Furthermore, their applications are super intuitive and personalised to offer relevant products for the user.

The evaluation made it clear that most players have similar offerings with minor differences. It was evident that all BNPL service providers focused more on making the shopping experience seamless and personalised. With numerous similar product offerings, retaining customers will become a critical measure of success.

Reserve bank of India (RBI) stance on BNPL in India

The Reserve Bank of India’s (RBI) attention has been drawn to India’s booming Buy Now, Pay Later (BNPL) sector. According to the new RBI guidelines, nonbanks can no longer load prepaid instruments — digital wallets or stored-value cards — with credit lines. The only valid options for a buyer are to transfer cash into their wallet or to debit their bank or credit-card accounts.

BNPL has some serious issues that have intrigued the interest of regulators. According to various reports, BNPL service providers do not conduct strict KYC checks on customers applying for loans. Furthermore, the BNPL apps are said to be poor at credit reporting. As a result, the RBI stated that the BNPL model must be examined and guidelines for the new lending scheme must be developed.

Regardless of the RBI’s restrictions, high-risk borrowers are expected to continue using BNPL apps for various online transactions, given how difficult it is for them to obtain credit from a bank. These apps are also appealing to the middle class because they offer exclusive deals with food delivery apps, mobility apps, and e-commerce platforms.

Way forward

The credit industry has experienced tremendous growth, technological disruption, and structural changes in the last decade. BNPL and credit EMIs have progressed the industry further, becoming India’s primary source of credit expansion despite the current crisis and its impact on credit card adoption. Adopting a closer look into the lending practices of fintech firms, the RBI has increased its scrutiny to regulate the sector.

BNPL has high consumer acceptance and facilitates financial inclusion, generating the potential to lend to a credit-starved economy like India. And since most BNPL borrowers are new to credit, BNPL intends to pave the way for them, working hard to improve their credit ratings and break into the formal financial market. Through this effort, BNPL aims to improve the overall financial inclusion of the country. Furthermore, as smartphones and internet connectivity spread across India, the reach of BNPL payment providers is expected to expand.

Traditional financial institutions may also use credit history data to develop a more comprehensive and efficient credit risk assessment model. The result – the process is easier for people who were denied access to credit earlier. With these evolving models and numerous structural changes, an exciting time lies ahead for the credit industry.

Guiding checklist for a BNPL provider ensuring a perfect product

- #1 Onboarding – Service providers need to reduce the number of steps to open an account. All the necessary details around documents, KYC, and steps to onboard must be clear.

- #2 The user must have access to the onboarding time to know when they can start using the line of credit.

- #3 Credit limit and repayments – Repayments and initial credit limit are the most important aspects of customer onboarding. Although no specific data indicates the perfect number for both of these parameters, it is safe to say from a customer’s point of view that the higher the parameter, the better it is.

- #4 Allow users to check their initial credit limit via a calculator tool.

- #5 The repayment cycle and the late payment charges should be mentioned clearly.

- #6 When onboarding, the user must have an option to check and search the partner store network.

- #7 Partner stores and offers – Consumers need flexibility when it comes to options when shopping. Having an extensive network of online and offline partner stores spread across various domains is a must. Offers tend to attract new users and also help merchants convert better. Instant discounts and cashback do better than reward points.

- #8 BNPL service providers need to have lucrative active offers across their merchants.

References

1Goldman Sachs