Key takeaways

- The average contribution of beyond connectivity revenues to total revenues has been increasing consistently: 14.8% in 2021, 17.3% in 2022, and 19.6% in 2023 (refer to Exhibit 1).

- Enterprise solutions and content and entertainment services remain the most popular routes for diversification.

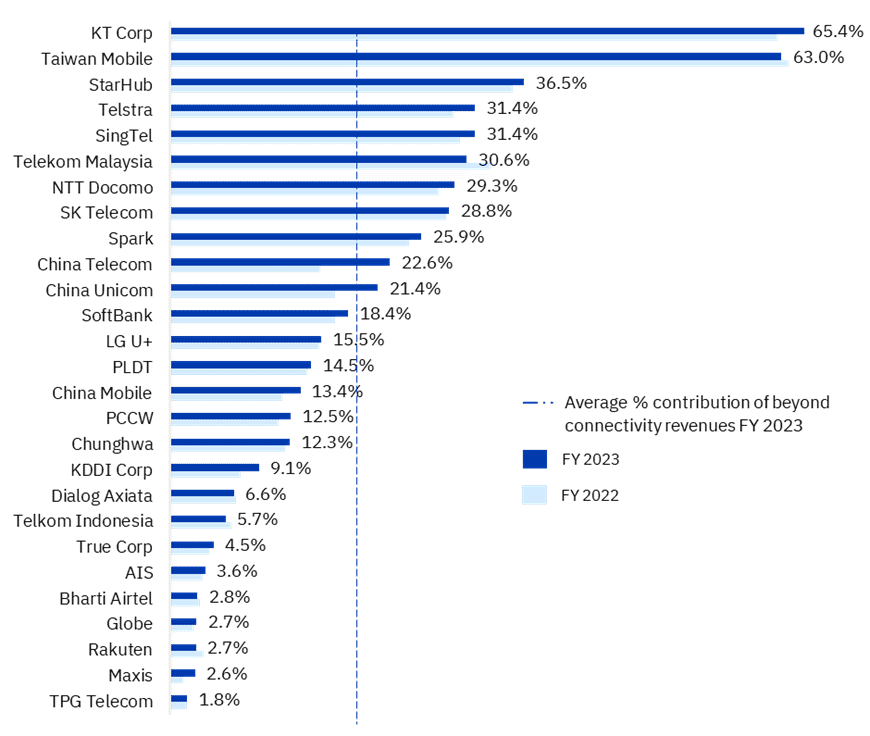

- KT Corp is a prime example of successful diversification, with revenues from non-connectivity services comprising 65.4% of its total revenue (the highest among any operator).

- The beyond connectivity to total revenue contribution for China Telecom grew from 15.5% in 2022 to 22.6% in 2023. This 7.1 percentage point increase (the highest among its peers) is driven primarily by the incredible growth of China Telecom Cloud.

- In 2023, nine operators surpassed the 25% threshold in beyond connectivity revenue contribution, demonstrating their effective diversification into a broad range of services.

Exhibit 1: Beyond connectivity revenue as a % of total revenue, 2022 – 2023

- While overall revenue growth in 2023 was 5.1%, beyond connectivity revenues surged by 18.2%, emerging as the fastest-growing segment for telcos.

- Overall revenue growth and growth in beyond connectivity have slowed from 2021 to 2022 compared to 2022 to 2023. Despite this, the trend remains positive (refer to Exhibit 2).

Exhibit 2: Total revenue growth and beyond connectivity revenue growth

| Year | Total revenues growth % | Beyond connectivity revenue growth % |

| 2022 | 6.8 | 22.7 |

| 2023 | 5.1 | 18.2 |

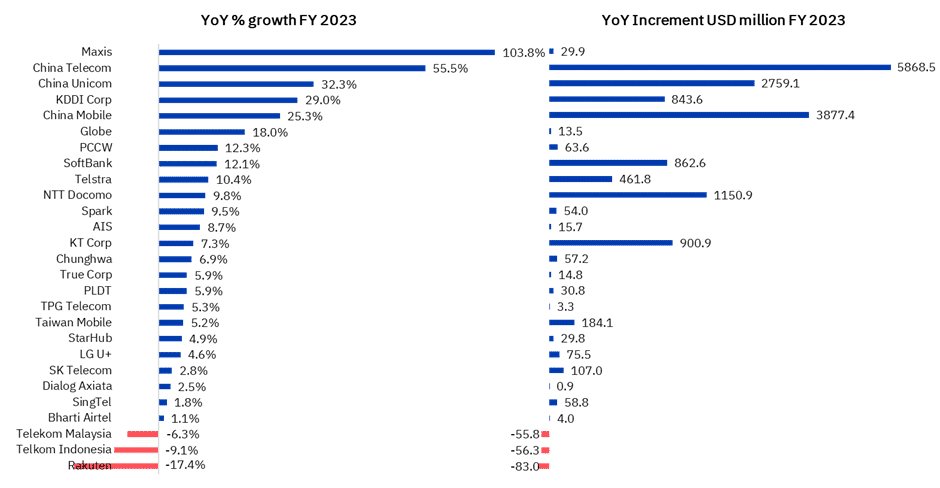

- Maxis recorded the highest growth in beyond connectivity revenues at 103.8%, adding 29.9 million net revenues in 2023.

- China Telecom followed with the second-highest growth at 55.5%, adding USD 5.8 billion (RMB 41.5 billion) (its highest net revenue increase) in 2023.

Exhibit 3: Beyond connectivity revenue trends, 2023

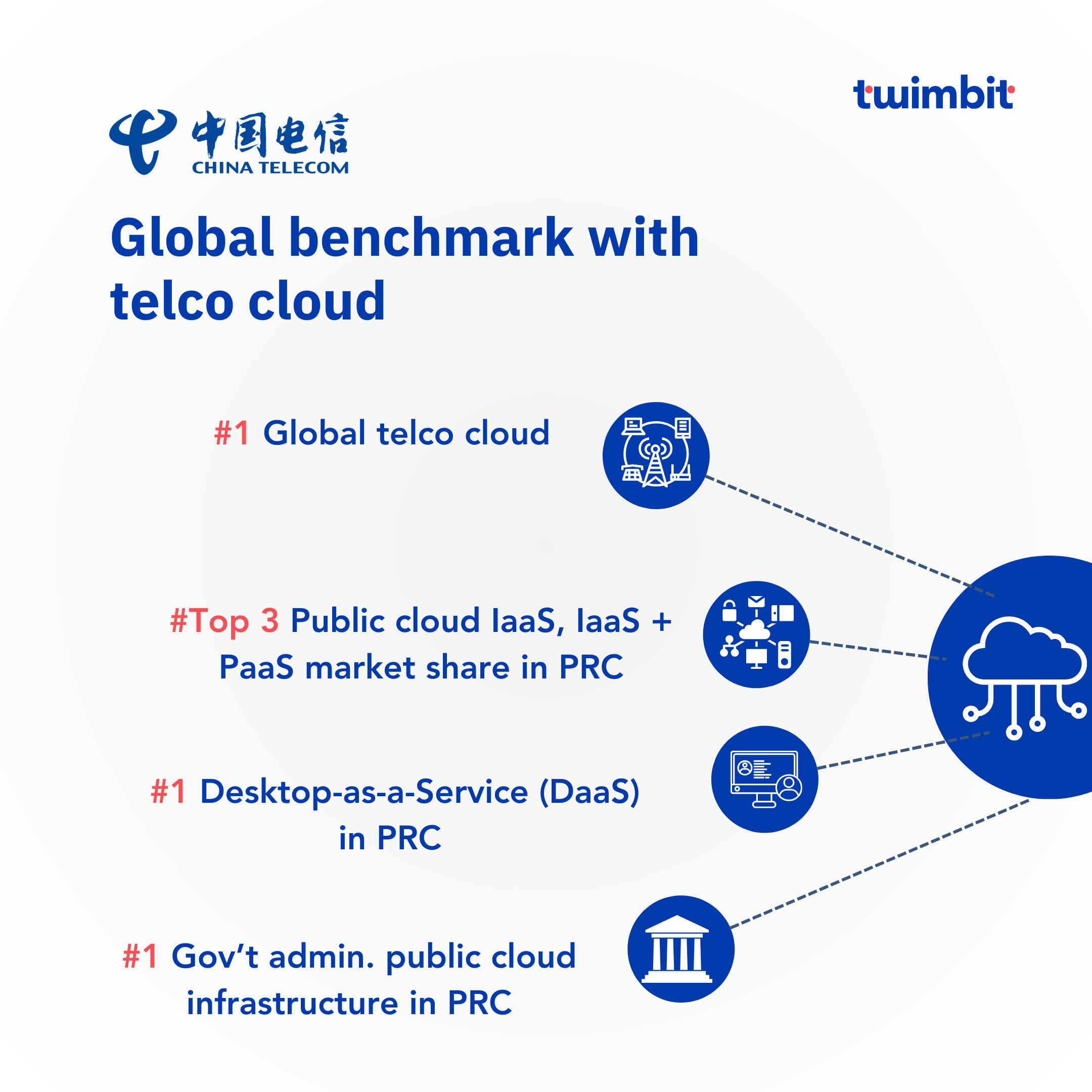

China Telecom, setting a benchmark in global telco cloud services

China Telecom recorded cloud revenue growth of 67.9% YoY to reach USD 13.7 billion (RMB 97.2 billion) in 2023, comprising roughly 19% of its total revenue. Their cloud business exhibits top rankings in several key areas:

- Leading position in the global telco cloud market

- Top 3 in the domestic public cloud IaaS and IaaS+PaaS markets

- Number 1 in the domestic Desktop-as-a-Service (DaaS) market

- Number 1 in government and administration public cloud infrastructure

Exhibit 4: Benchmark of China Telecom Cloud

China Telecom Cloud serves several industries with cloud migration and other cloud applications. These include breakthroughs in key technology areas, such as the development of:

- TeleCloudOS 4.0 operating system

- Yunxiao (an AI-driven computing acceleration platform integrating cloud, intelligent computing and supercomputing)

- Huiju (a one-stop intelligent computing service platform)

PCCW drives innovation in media with Viu

PCCW and its content and media division remain a source of inspiration for other operators in how it has growing its business outside of the home market. While PCCW’s overall revenue growth was modest at 0.8% YoY in 2023, the content and media revenue surged by 12.5%, primarily due to its OTT platform, Viu.

Viu’s success positions it alongside global OTT giants such as Netflix and Disney+ (Exhibit 5).

Exhibit 5: Viu market standing

Viu is popular in 16+ markets across Asia, the Middle East, and South Africa and had 62.4 million monthly active users (MAUs), with paid users increasing by 10% YoY to reach 13.5 million in 2023. These efforts led to revenues of USD 434 millon (HKD 3,404 million) accounting for 9.5% of total revenue.

KT Corp leads the non-connectivity pack

A frontrunner in non-connectivity services, KT Corp, boasts the highest contribution to total revenue among operators at 65.4% in 2023, up from 62.7% in 2022.

Previous ‘Beyond Connectivity’ insights by Twimbit have consistently highlighted KT Corp’s strides, with the operator reporting impressive growth figures each time. Explore a detailed insight of KT Corp’s strong foothold in the beyond connectivity streams here

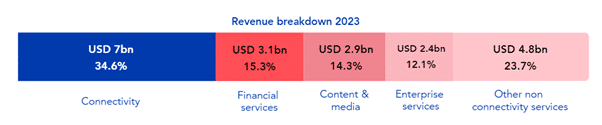

Exhibit below illustrates breakdown of KT Corp’s revenue streams by key segments.

Exhibit 6: Revenue breakdown of KT Corp by segment type

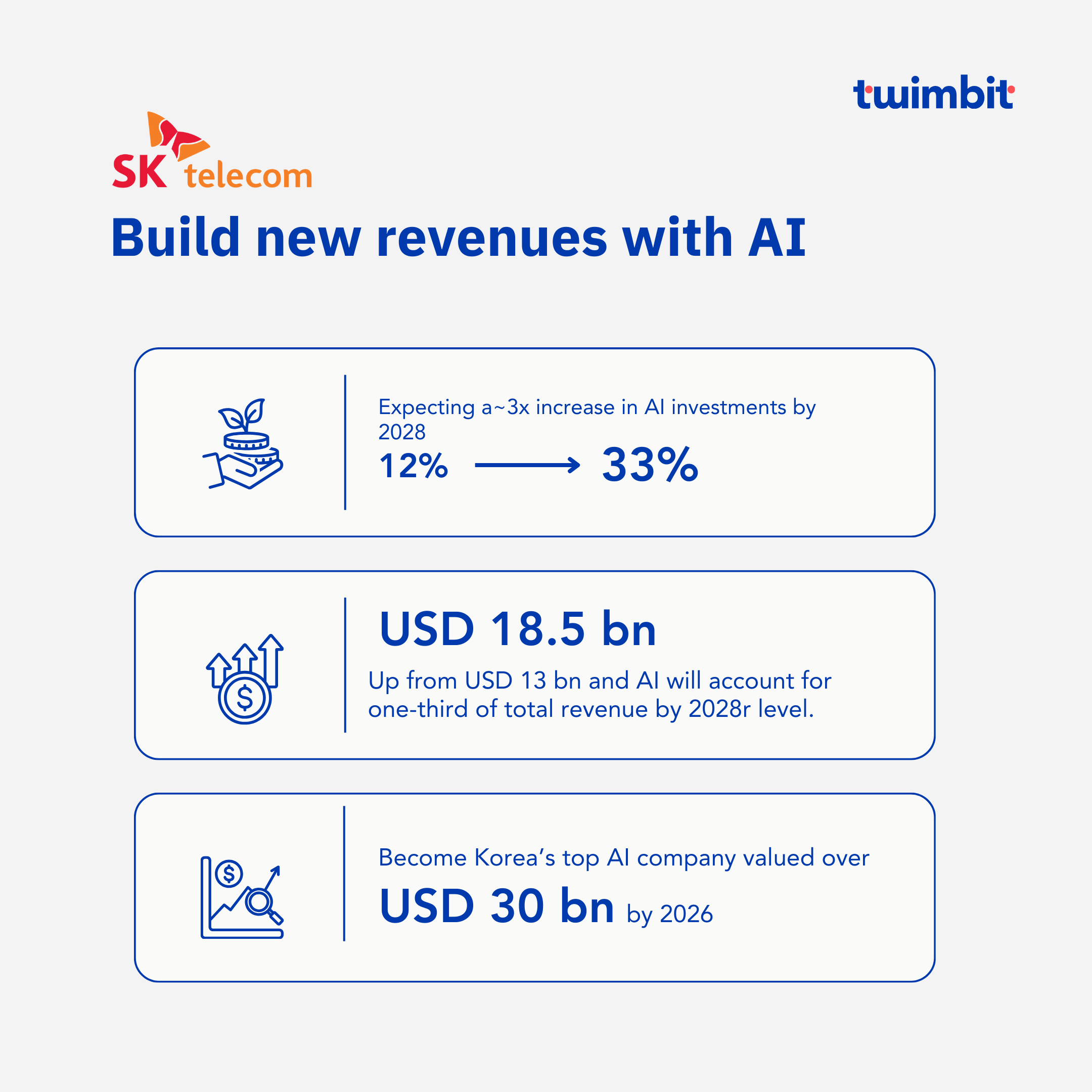

SK Telecom aspires to build a new revenue stream with AI

SK Telecom is now recognized globally as pioneer in AI within the telecom sector, Explore how SK Telecom became a prominent figure in advancing AI within the telecommunications landscape here:

SK Telecom indicates increased investments in the size and scope of its AI operations (Exhibit 7).

Exhibit 7: AI strategy SK Telecom

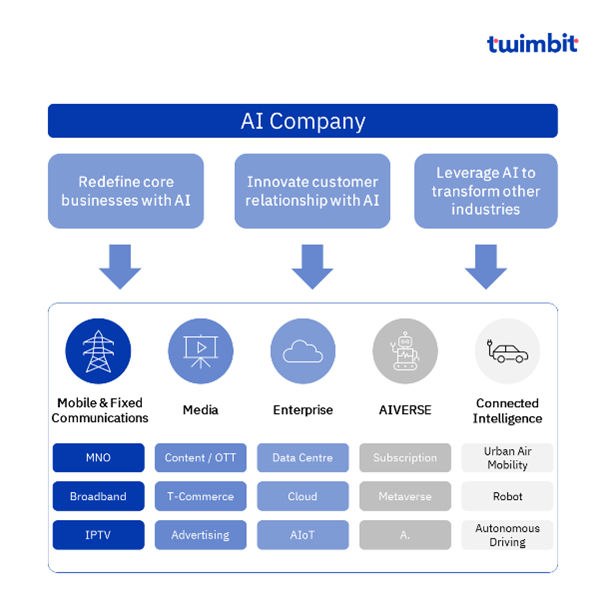

What’s more captivating is the strategic deployment of AI across various business segments, particularly in areas beyond traditional connectivity. (refer to exhibit 8)

Exhibit 8: SK Telecom – Use of AI across the value chain

SK Telecom’s beyond connectivity revenues reached approximately USD 3.9 billion, accounting for 28.8% of its total revenue. The company has laid out an ambitious plan leveraging AI to transform traditional telecom services into a dynamic and highly adaptive ecosystem.

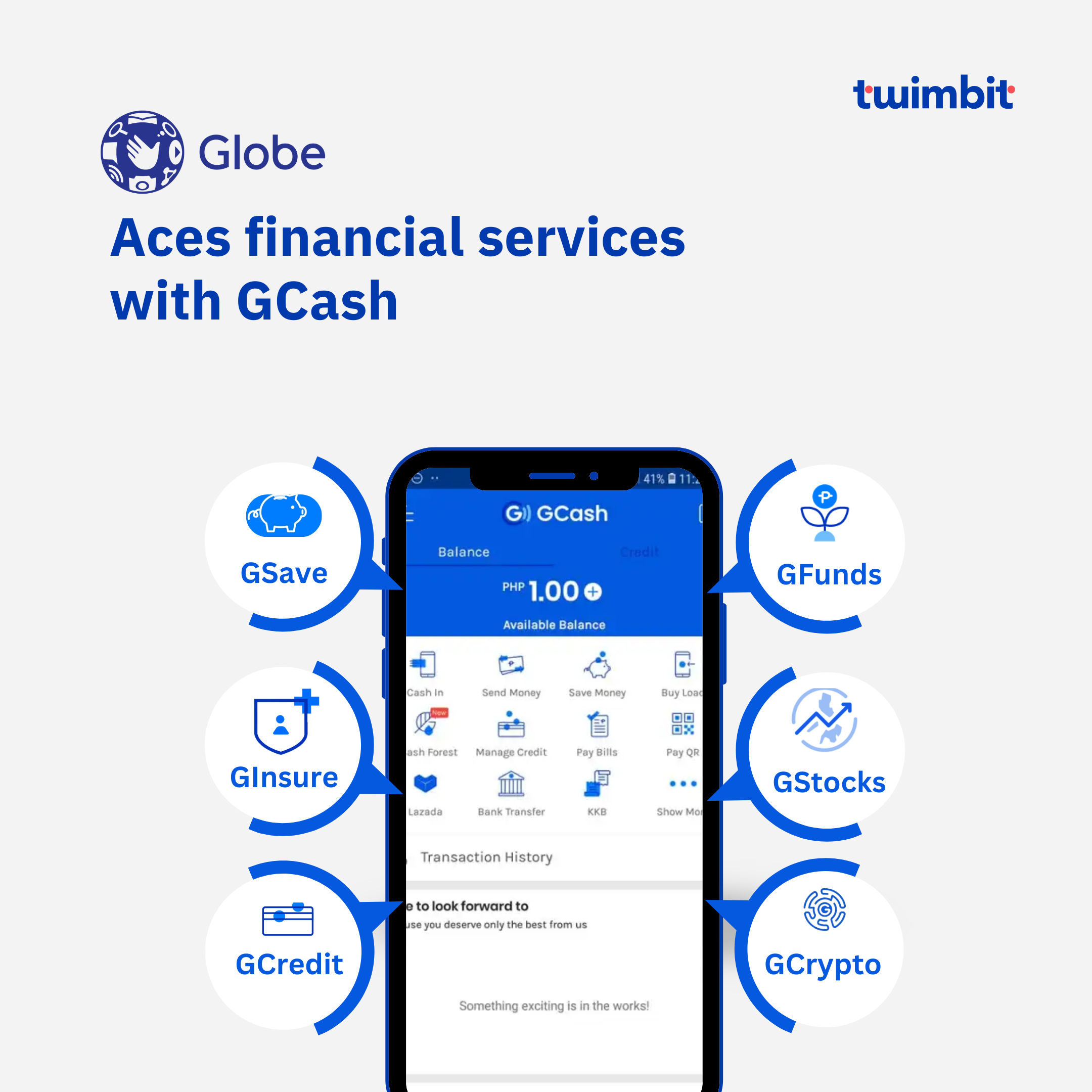

Globe aces financial services with GCash

Globe has been a topic of discussion in our previous “Beyond Connectivity” reports, primarily due to its impressive strides in the financial services sector with GCash, the most widely used finance app in the Philippines, boasting over 90 million users.

Exhibit 9: Gcash’s comprehensive suite of financial services

Its ambitious transformation into a tech company sets Globe apart, focusing intensively on various digital initiatives. Despite the still modest contribution from beyond connectivity services, the percentage of these revenues to total revenue has shown notable growth over the past three years:

- 2021: 1.2%

- 2022: 2.4%

- 2023: 2.7%

For an in-depth look at this best practice and Globe’s digital ecosystem, explore our detailed insight here

M1, expanding enterprise capabilities through strategic acquisitions

M1 has significantly bolstered its enterprise segment, making strategic acquisitions that enhance its technological capabilities and market reach. This includes the acquisition of 70% of Glocomp for USD 26.8 million (SGD 36 million) in 2021 and 100% of AsiaPac for USD 15 million (SGD 20 million) in 2018. These acquisitions have strengthened M1’s cloud and managed services portfolio helping it now compete effectively with established players and win business.

M1 has also innovated within the maritime industry by launching telemedicine and maritime surveillance solutions supported by 5G. Furthermore, the introduction of the ‘Pinnacle’ 5G MEC platform, developed in collaboration with ST Engineering, is set to evolve enterprise applications through AR/VR, live analytics, and IoT.

Exhibit 10: M1 Revenue contribution by segment type

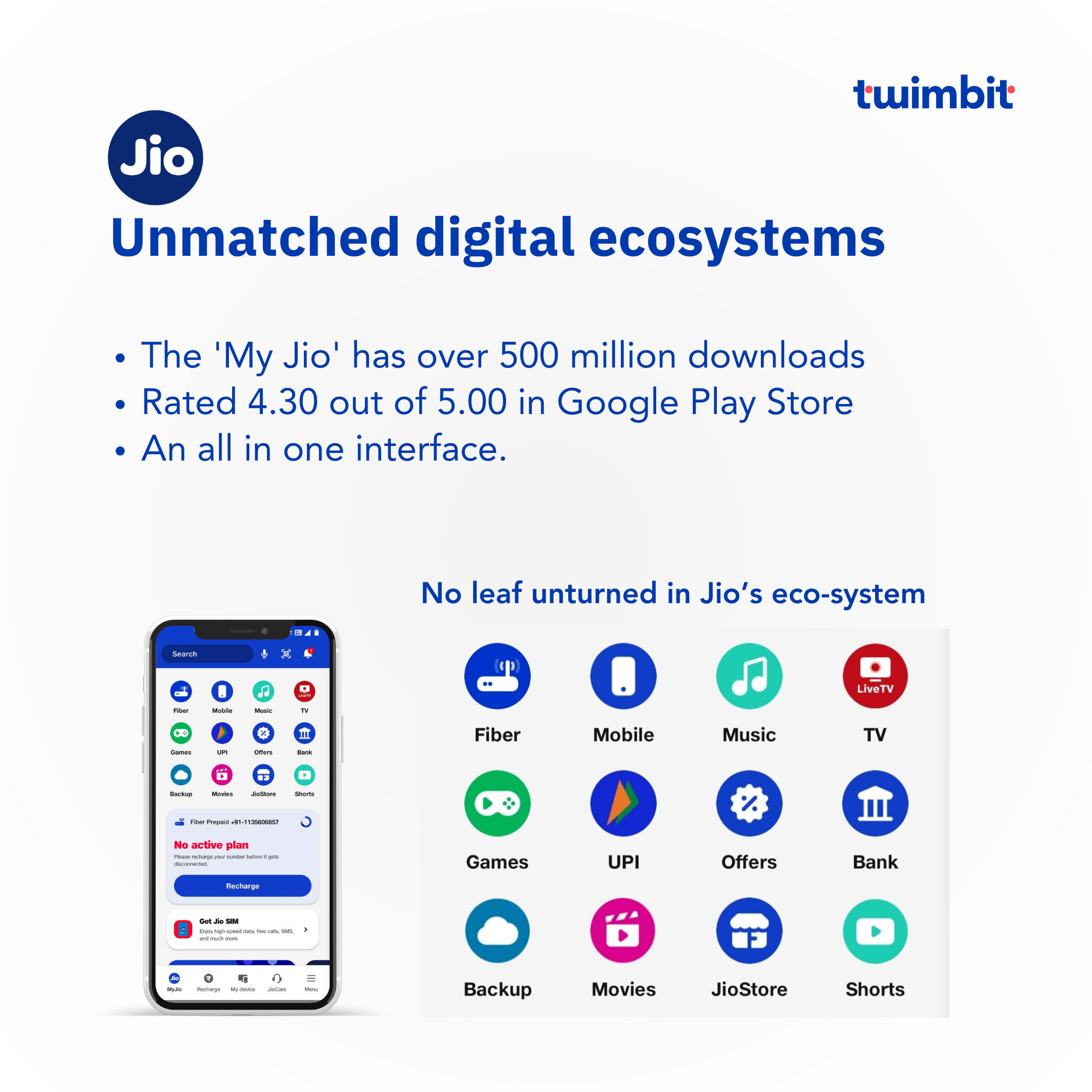

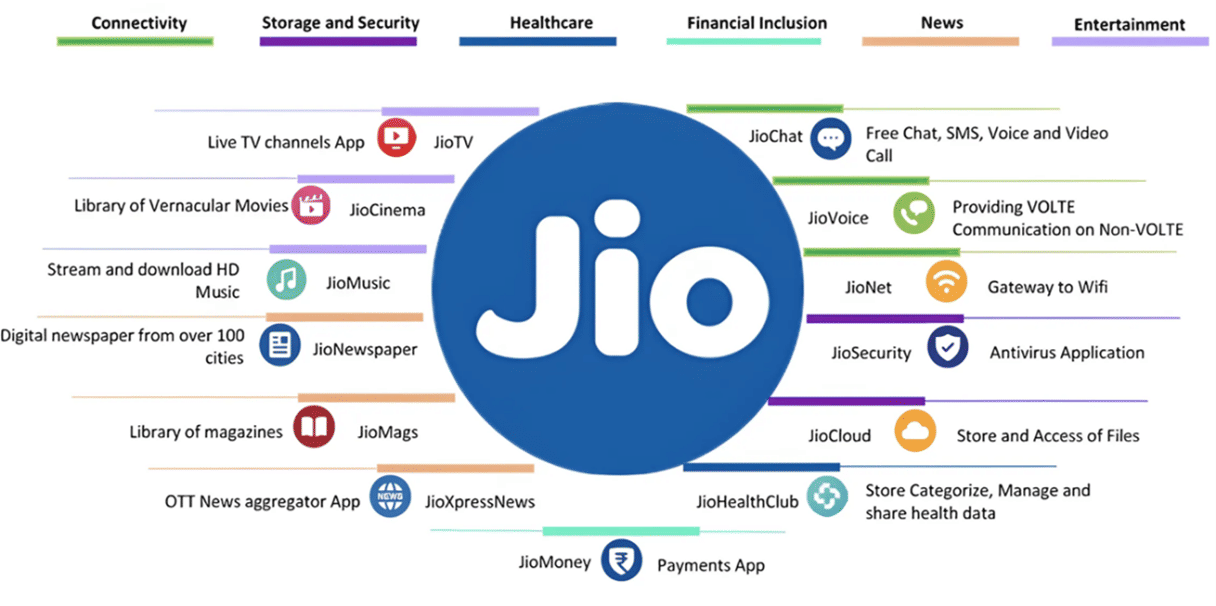

Reliance Jio builds a vast digital ecosystem of services

While Jio’s financial reporting structure does not separately detail non-connectivity revenues, its broad spectrum of services showcases an unmatched exemplary digital ecosystem.

Jio’s integration of a homegrown 5G stack is just one aspect of its comprehensive digital strategy that includes media, payments, music, security, cloud solutions, etc. The ‘My Jio’ app epitomizes this integration, having achieved over 500 million downloads with a user rating of 4.30 out of 5.00 (Google Play Store). It serves as a digital gateway, offering everything from mobile services and online banking to streaming music and video, all in one interface.

Exhibit 11: Reliance Jio Mobile app key metrics

Furthermore, 50% of branches of India’s top 10 banks utilize Jio’s network, having a strong influence in facilitating India’s digital finance landscape. This vast Jio ecosystem enhances customer engagement and sets a benchmark for how telecom companies can drive broader industry changes through digital technology.

Exhibit 12: Reliance Jio ecosystem

Research Methodology and Assumptions

- “Top APAC telcos to ace beyond connectivity revenue 2024” report provides a summarized view of beyond connectivity (non-connectivity) revenue performance of leading telcos in the APAC region for the year 2023.

- This report leverages secondary research methodologies and data provided by telecommunication companies (telcos) themselves. Twimbit employs a calendar year approach (January- December) for all telcos to ensure consistent comparison, regardless of their individual fiscal year ending periods.

- 27 out of the ~45 telcos have reported their beyond connectivity revenue. Telcos with beyond connectivity revenue contributing less than 2% to total revenue are not included in our analysis.

- Beyond connectivity services in this report exclude traditional voice, data, fixed-line, broadband, and enterprise connectivity services (e.g., IP-VPN, SD-WAN). These services are categorized into four primary buckets, which include, but are not limited to:

- Enterprise Non-connectivity: Managed services, Cloud, Cybersecurity, IoT.

- Content and Media: Pay TV, IPTV, OTT services, Content leasing, entertainment services.

- Payments and E-commerce: Financial services (wallet, banking, insurance, investing), Retail business.

- Others: Any service beyond the above categories deemed as beyond connectivity (e.g., Digital marketing, Analytics, Tele-Health).

- The data from prior reports may exhibit variances when compared to the figures presented in this report. This discrepancy arises from meticulous approach, which excludes all previous assumptions and estimations when calculating beyond connectivity revenue.

- For consistent analysis, a constant exchange rate (average for January-December 2023) has been applied when converting local currencies to USD.

- The primary focus of the analysis was to understand the contribution of the beyond connectivity performance and revenue to the telcos’ overall revenue. Additionally, a detailed peer comparison was conducted to identify leading telcos and their best practices.

- The data provided in the report are as reported by the respective telcos or on a calculated basis wherever feasible. These may or may not align with the exact numbers incase the respective telcos have either not disclosed or provided any reference for the above segments (or further sub-segment details).

- The data collected may be subject to reporting inconsistencies inherent to various telcos and hence can be leveraged for reference and guidance purpose. The analysis is based on publicly available information.

For more content on telecoms, click here

Recommended by Twimbit

Enterprise business update for Asia-Pacific telcos 2024

APAC telcos performance benchmarks – Winter 2024