Key Takeaways

- Beyond Connectivity services accounted for 22.5% of total revenue for the telcos in the Asia-Pacific region in FY-2024, a modest increase from 21.3% in FY-2023 and 19.3% in FY-2022. This growth reflects a gradual but steady shift in the industry’s revenue mix, as operators increasingly pursue diversification strategies beyond traditional network services.

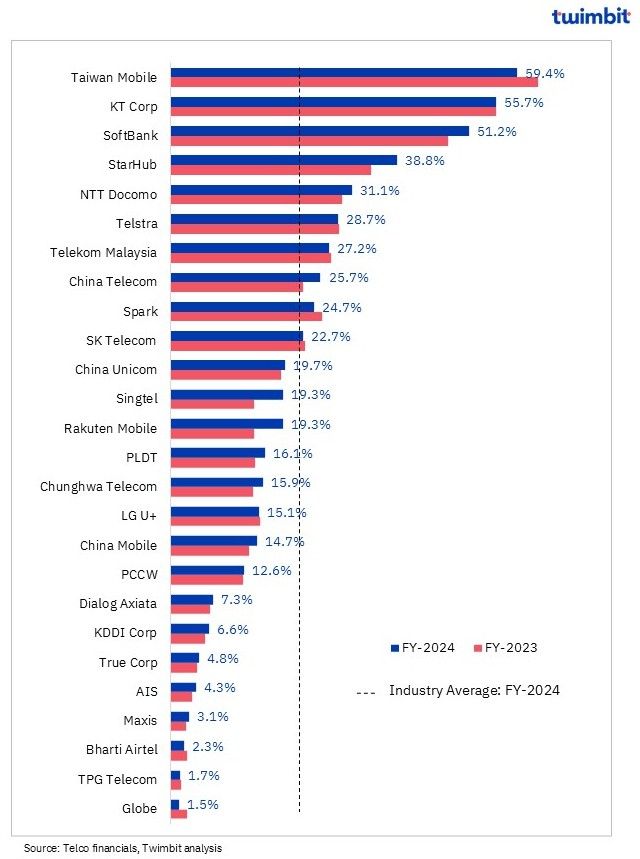

- Revenue from beyond connectivity offerings grew by 9.4% YoY in FY-2024, reaching approximately USD 120.8 billion. Nearly 77% of the telcos reported YoY growth in beyond connectivity revenue, of which around 39% reported beyond connectivity revenues exceeding the regional average contribution of 22.5%. Companies such as Taiwan Mobile, KT Corp, SoftBank, StarHub, and NTT Docomo emerged as leaders in this transition, underscoring their strategic focus on broadening service portfolios.

- Enterprise non-connectivity solutions remained the most significant contributor to this category, particularly among operators in China-such as China Mobile, China Telecom, and China Unicom – where digital transformation services continue to play a central role in revenue growth.

- At the same time, other verticals-including content and media, payments, and e-commerce gained traction across the region. For example, financial services were a key source of revenue expansion for SoftBank in Japan, while enriched media offerings contributed to the growth of PCCW and Bharti Airtel. Similarly, companies like True Corp, NTT Docomo, and Bharti Airtel have seen meaningful gains from their investments in content platforms and digital commerce.

Beyond connectivity revenue analysis of APAC telcos: FY-2024

- In the Asia-Pacific region, revenue from beyond connectivity services grew by 9.4% YoY to ~USD 120 billion in FY-2024, significantly outpacing the overall revenue growth of 3.4% reported by telecommunications companies during the same period. (This analysis excludes telcos that do not publicly disclose their beyond connectivity revenues).

- Enterprise solutions, alongside content and entertainment services, continue to be the most prominent areas of diversification, with enterprise solutions emerging as the principal driver of revenue.

Exhibit 1: Beyond connectivity revenue as a % of total revenue: FY-2024

Enterprise non-connectivity services continued to drive growth for leading operators such as Rakuten Mobile and AIS. Meanwhile, other segments—including content and media, digital payments, and e-commerce—also contributed notably to the performance of companies like True Corp, NTT Docomo, SoftBank, and Bharti Airtel.

Exhibit 2: Beyond connectivity revenue trends: FY-2024

Beyond connectivity performance of APAC telcos: FY-2024

Consumer and Enterprise segment fuel beyond connectivity growth for Taiwan’s telcos

Taiwan Mobile stood out among APAC telcos in for having the highest proportion of beyond connectivity revenue relative to total revenue, at 59.4% in FY-2024. This leadership position came despite a YoY decline in the segment’s overall contribution, largely due to a 6% drop in cable television (CATV) revenue following the reduction in content offerings associated with Disney’s market exit.

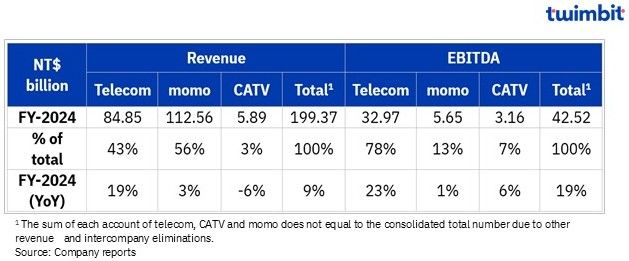

- Nevertheless, total revenue saw a notable 8.7% YoY growth in FY-2024, primarily driven by merger synergies realized after the completion of Taiwan Mobile’s acquisition of Taiwan Star Telecom (T Star) in December 2023. The momo segment—focused on e-commerce—posted a 3% YoY growth in FY-2024, partially offsetting the decline in CATV revenues. In FY-2024, momo and the “pay TV, content, and channel leasing” segment contributed 56% and 3% of total revenue, respectively.

- Strategic partnerships were instrumental in sustaining growth in the momo segment. In response to muted demand for online retail relative to services and leisure categories, the telco expanded into third-party logistics (3P) and retail media network (RMN) services in 2024, diversifying its revenue base.

- Beyond the benefits of the T Star merger, Taiwan Mobile also experienced strong growth in gaming and international roaming revenues, which rose by approximately 20% YoY in FY-2024. On the enterprise side, the telco also stated of services related to IoT, cloud computing, and cybersecurity also delivered strong growth, reinforcing the company’s position in high-growth digital infrastructure domains.

Exhibit 3: Taiwan Mobile’s performance by business segment: FY-2024

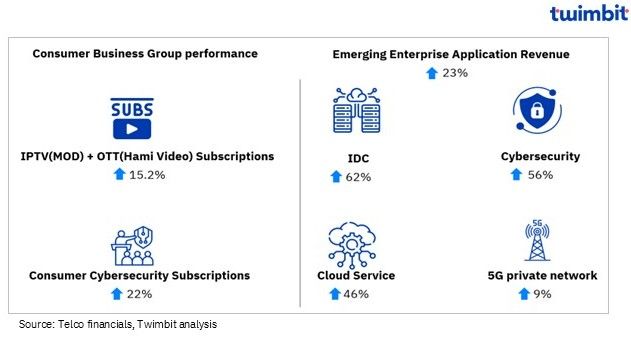

Chunghwa Telecom’s beyond connectivity revenue increased by 16.2% YoY in FY-2024, accounting for 15.9% of total revenue, up from 14.1% in FY-2023. Growth in the Consumer segment was primarily driven by higher IPTV+OTT and cybersecurity subscriptions, while expansion in enterprise applications supported growth in the Enterprise segment.

- IPTV+OTT subscriptions increased by 15.2% YoY in FY-2024, reaching 3.3 million, supported by increased viewership of events such as the WBSC Premier 12 tournament.

- Strong momentum in IDC, cloud, and cybersecurity services led to approximately 50% YoY growth, driven by both project-based and recurring revenues. The telco also completed its first overseas advanced IDC (AIDC) facility in Mexico for an enterprise client. In addition, Chunghwa Telecom continues to harness generative AI technologies to pursue new opportunities and secure projects in the smart government and smart healthcare sectors.

Exhibit 4: Chunghwa Telecom Digital offering performance: FY-2024

Chinese telcos lead enterprise digital growth with Cloud and AI

The Enterprise segment remains the primary driver of non-connectivity revenue for China’s three major telecom operators, each of which is strategically investing in digital capabilities such as cloud computing, artificial intelligence (AI), digital applications, and content services.

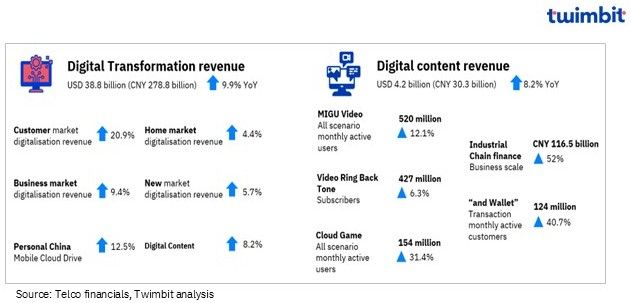

China Telecom recorded a 17.1% YoY increase in beyond connectivity revenue in FY-2024, driven by its strong focus on digital transformation for enterprise and government clients through its cloud, big data, and AI solutions.

- A key contributor to this growth was China Telecom Cloud, which also saw a 17.1% YoY revenue increase, reaching USD 15.9 billion (CNY 113.9 billion). The number of B2B customers rose by 8% to 4.9 million, signalling increased enterprise adoption.

- Additional momentum came from Internet Data Center (IDC) and cybersecurity services. IDC revenue rose 7.3% YoY to USD 4.6 billion (CNY 33 billion), while security services grew 17.2% YoY to USD 2.3 billion (CNY 16.2 billion) in FY-2024.

- The telco also ramped up its AI initiatives, serving over 10,000 industry-specific enterprise use cases, including 8,700 SaaS-based industrial clients and over 1,600 AI + DICT projects aimed at driving digital transformation across sectors.

China Unicom posted a notable 8.8% YoY increase in beyond connectivity revenue in FY-2024, largely underpinned by its enterprise-focused strategy.

- Growth was led by the Computing and Digital Smart Applications (CDSA) business, which prioritized scale and quality improvements. Within this segment, China Unicom Cloud revenue increased by 17.1% YoY, while IDC revenue grew by 7.4% YoY in FY-2024.

- The intelligent computing division also gained traction, with newly signed contracts exceeding USD 3.6 billion (RMB 26 billion) in FY-2024, reflecting rising enterprise demand for high-performance computing capabilities.

- China Unicom further advanced its digital government initiatives, integrating network, cloud, big data, and intelligent applications. Revenue from intelligence services surged 26.5% YoY to USD 1 billion (CNY 7.1 billion), while data services revenue rose by 20.8% YoY to USD 891 million (CNY 6.4 billion) in FY-2024.

China Mobile delivered robust performance as well, with beyond connectivity revenue rising 13.1% YoY in FY-2024, driven by the Data, Information, and Communications Technology (DICT) segment and growing expanding enterprise client base.

- The company added approximately 4.2 million new enterprise customers, bringing the total to around 32.59 million. It also enhanced its competitive edge in public tenders, improving its win rate from 14.3% in FY-2023 to 16.4% in FY-2024.

- Mobile Cloud continued to be a major revenue engine, with 20.4% YoY growth, reaching ~USD 14 billion (CNY 100.4 billion) in FY-2024, reinforcing China Mobile’s leadership in cloud-enabled enterprise solutions.

Exhibit 5: China Mobile Digital offerings KPIs: FY-2024

Beyond connectivity gains momentum via digital moves by Japan telcos

SoftBank’s growth in beyond connectivity revenue during FY 2024 was underpinned by strong performance across its Enterprise, Media & E-Commerce (EC), and Financial Services segments.

- The Media & EC segment, together with Financial Services, contributed approximately 28.6% of SoftBank’s total revenue in FY-2024. Media revenue rose by 2.7% YoY to USD 3.5 billion (JPY 534.3 billion), largely driven by increased revenue from account-based advertising.

- The Financial Services and Commerce business, which includes SB Payment Service and PayPay, recorded an 8.1% YoY growth, reaching ~USD 5.3 billion (JPY 808.2 billion).

- This growth was primarily fuelled by a surge in transaction volumes through PayPay Corporation, with QR code payments and credit card services seeing notable expansion. PayPay’s standalone payment volume grew 22.1% YoY, and its monthly transacting users (MTU) rose by 13.7% YoY to reach 36.2 million. The MTU penetration among SoftBank’s mobile subscribers increased from approximately 79.3% in FY 2023 to 88.9% in FY 2024.

- The Enterprise segment also demonstrated robust performance, contributing significantly to beyond connectivity revenue growth with a YoY increase of approximately 24.7%.

Rakuten Mobile, the smallest among the major Japanese telecom operators by revenue, registered the highest growth in beyond connectivity revenue in FY-2024, underpinned by Rakuten Symphony’s efforts to streamline its operational structure while continuing to execute on international projects. In early 2025, it opened two Radio Access Network (RAN) Proof-of-Concept (PoC) centers in collaboration with Kyivstar (Ukraine) and Telkom Kenya (Kenya), underscoring its ambition to position itself as a global leader in cloud-native network software.

- The telco expanded its portfolio with the launch of “Rakuten AI for Business,” a generative AI service for corporate clients. Priced at USD 6.6 (JPY 1,100) per license per month (inclusive of tax), the solution will be bundled with Rakuten Mobile’s corporate offerings as part of its strategy to explore new enterprise revenue streams in artificial intelligence.

Subscriber growth in Viu and Now.com drives PCCW’s media expansion

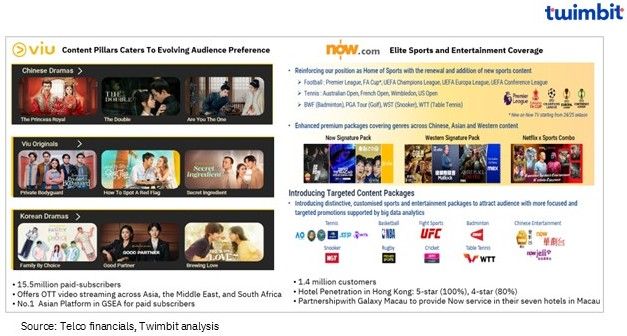

PCCW’s content and media offerings contributed nearly two-thirds of its beyond connectivity revenue in FY-2024, driven primarily by the performance of its over-the-top (OTT) platform, Viu, and its OTT multimedia platform, Now.com.

- Viu, PCCW’s flagship video streaming service, recorded a significant uplift in subscription revenue, underpinned by a 17% year-over-year (YoY) increase in paid subscribers, reaching 15.5 million by the end of FY2024. This growth was further bolstered by higher advertising revenues, sponsorships, event-related income, and title sponsorships for popular regional content.

- ViuTV also reported 11% YoY revenue growth in FY2024, largely driven by the robust performance of its artist and event management business. Digital engagement remained strong, with a 6% YoY increase in registered members across online platforms.

- Additionally, HKT, a PCCW Group subsidiary, contributed to the segment’s growth through its OTT media platform, Now.com, and its suite of industry-specific enterprise solutions, including cybersecurity, robotics, and managed services. Now OTT’s customer base grew by 15% YoY in FY2024, while the total value of newly secured projects rose by 11% YoY, exceeding USD 641 million (HKD 5 billion).

Exhibit 6: PCCW’s content engagement strategies

Korean telcos show mixed beyond connectivity performance amid shifting enterprise and media trends

KT Corp beyond connectivity revenue growth remained almost in FY-2024, as gains in its cloud segment were offset by declines in its media and financial service businesses.

- KT Cloud posted a 15.5% YoY revenue increase in FY-2024, reaching USD 5.2 billion (KRW 783.2 billion), driven by rising demand for IDC colocation services and Content Delivery Network (CDN) traffic.

- KT continued to strengthen its strategic alliance with Microsoft to jointly develop solutions in artificial intelligence (AI), cloud computing, and IT services, including the deployment of AI GPU farms and new data centres tailored to the Korean market.

- However, performance in other areas was weaker. BC Card revenue declined 5.4% YoY to USD 25.2 billion (JPY 3.8 trillion) in FY-2024, due to a reduction in acquisition volumes.

- KT Skylife, the company’s pay-TV subsidiary, saw a 1.5% YoY revenue drop to USD 6.8 billion (JPY 1 trillion) in FY-2024, attributed to a declining subscriber base.

- KT’s content subsidiary experienced a sharp 13.6% YoY decline, reflecting intense competition and changing consumer behavior in the digital content space.

SK Telecom, by contrast, recorded modest growth in its beyond connectivity revenue in FY 2024, led by its enterprise and pay-TV segments.

- Pay-TV revenue grew 0.7% YoY to USD 1.4 billion (KRW 1.9 trillion) in FY-2024, supported by a 0.6% increase in total subscribers to 9.6 million, and a 1.1% growth in IPTV users, especially those on high average revenue per user (ARPU) plans such as B tv All.

- The enterprise segment, particularly the AIX (AI transformation) division reported 32% YoY revenue growth in FY-2024, also contributed meaningfully to growth. AI Cloud revenue rose in the double digits YoY in FY-2024, with AI B2B sales surpassing USD 44 million (KRW 60 billion). AI data centre (AI DC) revenue increased 13.1% YoY in FY-2024, driven by stronger utilization of newly established data centre infrastructure.

Airtel sustains digital TV revenue amidst industry-wide DTH decline

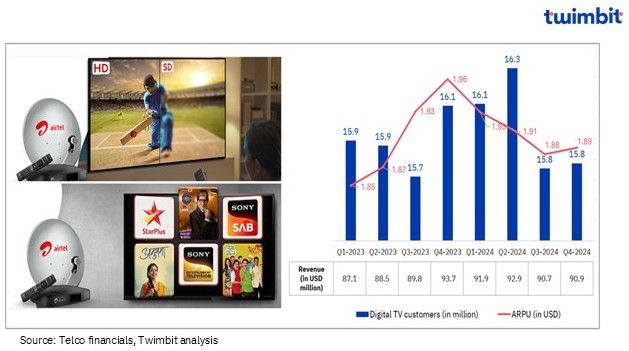

Airtel’s Digital TV business recorded a modest 2% YoY growth in revenue in FY-2024, reaching ~USD 366.4 million (INR 30.7 billion) and contributing 2.3% to the company’s total annual revenue. This growth was primarily driven by a rise in customer additions during Q2-2024.

- However, revenue and customer growth momentum softened in the latter half of the year, reflecting broader challenges faced by the Direct-to-Home (DTH) industry. The sector continued to experience subscriber erosion due to the growing popularity of OTT streaming platforms and free-to-air services like DD FreeDish. These pressures led to industry consolidation talks, including a proposed merger between Tata Play and Airtel Digital TV, which was ultimately called off.

- Airtel upheld ARPU and users via key tech alliances, notably debuting Glance TV in India to advance in the connected TV space. Additionally, Airtel partnered with ZEE5 to enrich its WiFi customer offering with premium digital content, further reinforcing its commitment to content-driven engagement and platform differentiation.

Exhibit 7: Bharti Airtel Digital TV revenue trends: Q1-2023 – Q4-2024

Research Methodology and Assumptions

- “Top APAC telcos to ace beyond connectivity revenue: FY-2024” report provides a summarized view of beyond connectivity (non-connectivity) revenue performance of leading telcos in the APAC region for the period Jan-Dec 2024.

- This report leverages secondary research methodologies and data provided by telecommunication companies (telcos) themselves. Twimbit employs a calendar year approach (January- December) for all telcos to ensure consistent comparison, regardless of their individual fiscal year ending periods.

- The research examined ~49 telcos across 20 Asia Pacific countries. Selection criteria included economic significance and reliable data availability. The research is based on the beyond connectivity segments revenues available for 26 telcos analysed.

- For consistent analysis, a constant exchange rate (average for Jan – Dec 2024) has been applied when converting local currencies to USD.

- Beyond Connectivity services in this report exclude traditional voice, data, fixed-line, broadband, and enterprise connectivity services (e.g., IP-VPN, SD-WAN). These services are categorized into four primary buckets, which include, but are not limited to Enterprise Non-connectivity (Managed services, Cloud, Cybersecurity, IoT), Content and Media (Pay TV, IPTV, OTT services, Content leasing, entertainment services), Payments and E-commerce: (Financial services like wallet, banking, insurance, investing, Retail business), Others (Any service beyond the above categories deemed as beyond connectivity like Digital marketing, Analytics, Tele-Health).

- The data from prior reports may exhibit variances when compared to the figures presented in this report. This discrepancy arises from meticulous approach, which excludes all previous assumptions and estimations when calculating beyond connectivity revenue.

- The data provided in the report are as reported by the respective telcos or on a calculated basis wherever feasible. These may or may not align with the exact numbers in case the respective telcos have either not disclosed or provided any reference for the above segments (or further sub-segment details).

- The data collected may be subject to reporting inconsistencies inherent to various telcos and hence can be leveraged for reference and guidance purpose. The analysis is based on publicly available information.

Click here for more contents on telecom

Enterprise business update for Asia-Pacific telcos 2025