Executive Summary

The first half of 2025 underscored a defining inflection point for Asia-Pacific telecoms. Non-connectivity revenues have become the new engine of differentiation and growth, expanding nearly four times faster than core connectivity revenues. This marks a decisive move away from traditional reliance on mobile and broadband toward diversified digital businesses.

However, this transformation is not uniform. Operators are taking distinct paths depending on market maturity, capability depth, and strategic focus. Some are repositioning as full-scale digital platforms; others are building niche capabilities in high-growth verticals such as enterprise AI, data infrastructure, and IoT.

A clear theme across the region is the rapid expansion of cloud, data centre, and AI-enabled service ecosystems. Operators are deploying significant capital to:

- Expand hyperscale data centre capacity,

- Embed AI-driven analytics and automation into enterprise offerings, and

- Commercialise GPU-as-a-Service to support high-performance computing needs.

While monetisation remains nascent, operators view this phase as a strategic build-up period. Enterprise adoption of AI is expected to accelerate, with demand for compute and data capacity deepening over the next 12-24 months.

Beyond infrastructure, diversification into adjacent digital verticals has become a key lever of growth.

- Integrated platform expansion: Leading operators are scaling into financial services, e-commerce, and digital content, positioning themselves as multi-service digital ecosystems rather than pure telecom providers.

- Industry-specific adjacencies: Others are investing in cybersecurity, IT professional services, and IoT-led industrial solutions, addressing the needs of sectors such as automotive, logistics, manufacturing, and energy.

Although performance across these adjacencies varies, some constrained by consumer sentiment or price competition, the long-term trajectory is clear. These verticals are becoming critical complements to connectivity, supporting revenue diversification and margin expansion.

This shift signals a disciplined pursuit of scalable, high-value growth where collaboration drives scale and focus drives returns. Non-connectivity revenues are now central to this evolution, positioning diversified digital ecosystems as the foundation of the sector’s new growth equation.

Beyond connectivity revenue analysis of APAC telcos: H1-2025

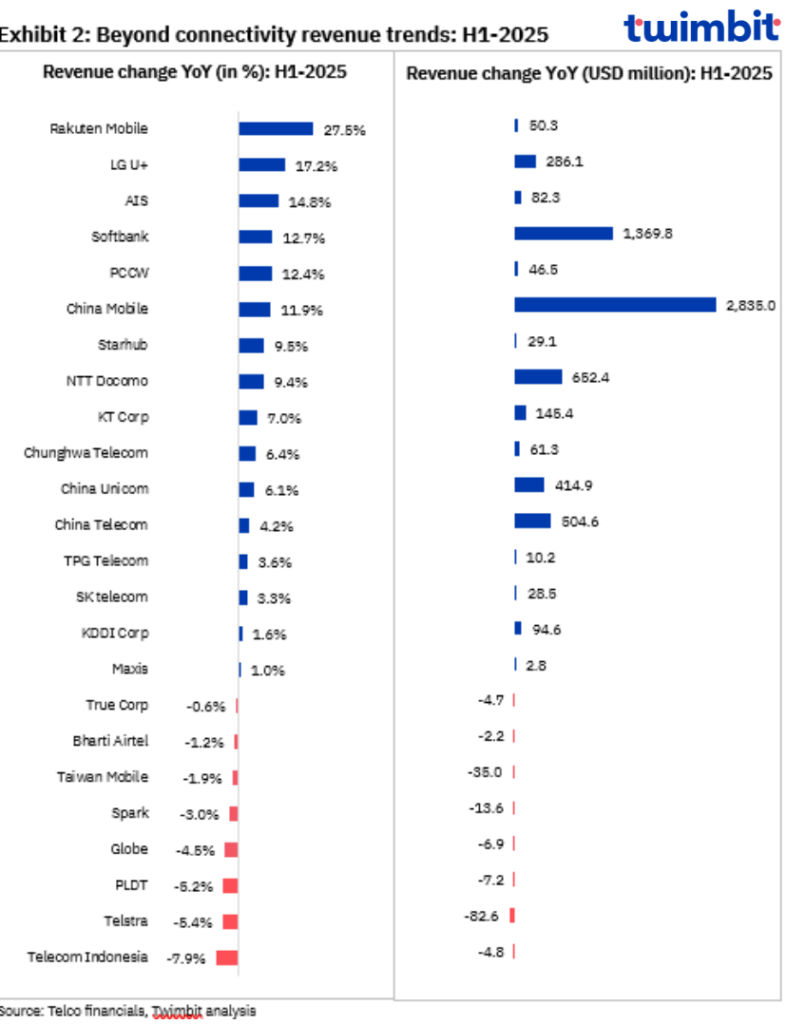

Within the Asia-Pacific region, beyond-connectivity segment revenue experienced a robust 8.7% YoY growth in H1-2025. The growth significantly outpaced the telcos’ overall revenue growth of 2.3% for these companies during the same period.

Enterprise non-connectivity continued to be a key growth driver for leading telcos such as Softbank, Bharti Airtel and Spark. However, content and media, along with payments and e-commerce, also emerged as notable growth contributors for telcos like True Corp, NTT Docomo, SoftBank, and Bharti Airtel.

Beyond connectivity performance of APAC telcos: H1-2025

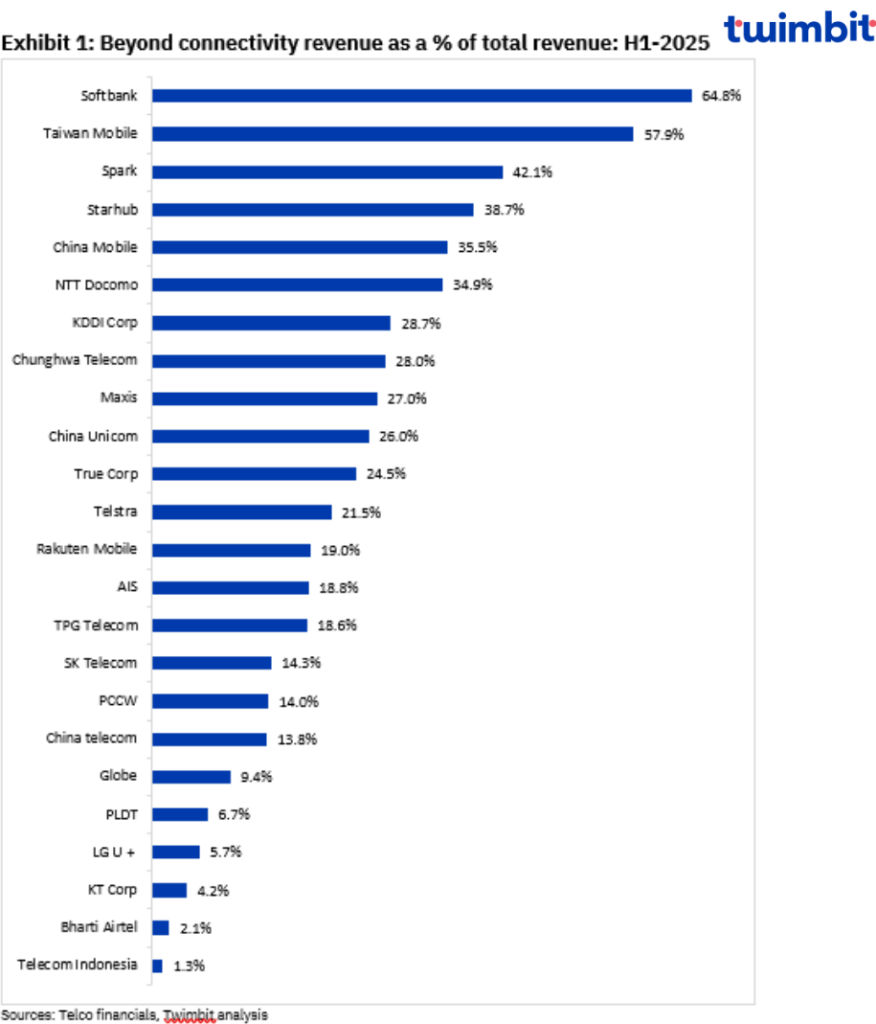

Softbank leads the region in beyond-connectivity diversification

- SoftBank stands out among APAC telcos for its aggressive diversification beyond connectivity. Non-connectivity revenues rose to 64.8% of total revenues in H1-2025, up from 61.5% YoY, the highest share across regional peers.

- The operator delivered one of the region’s strongest beyond connectivity performance, growing 12.7% YoY with net additions of USD 1,962.6 million in H1-2025, driven primarily by distribution revenues and robust device sales through B2C channels.

- Financial services, distribution, strategy and commerce platforms contributed 36.1% of total revenues, underscoring the growing strategic importance of ancillary services in driving diversification and strengthening the operator’s beyond-connectivity portfolio. The operator has been systematically focusing on these 3 as growth pillars in beyond connectivity space.

- In financial services, Softbank is scaling PayPay towards an IPO in the US while embedding AI in payments and fraud detection. The Distribution segment is expanding ICT sales and cloud/SaaS subscriptions, leveraging AI infrastructure to streamline supply chains and lift margins. Meanwhile, the Media & EC arm is driving growth through stronger advertising and deeper monetisation of e-commerce platforms like ZOZO and ASKUL. Together, these moves reinforce SoftBank’s role as a diversified digital solutions provider, reducing reliance on core connectivity.

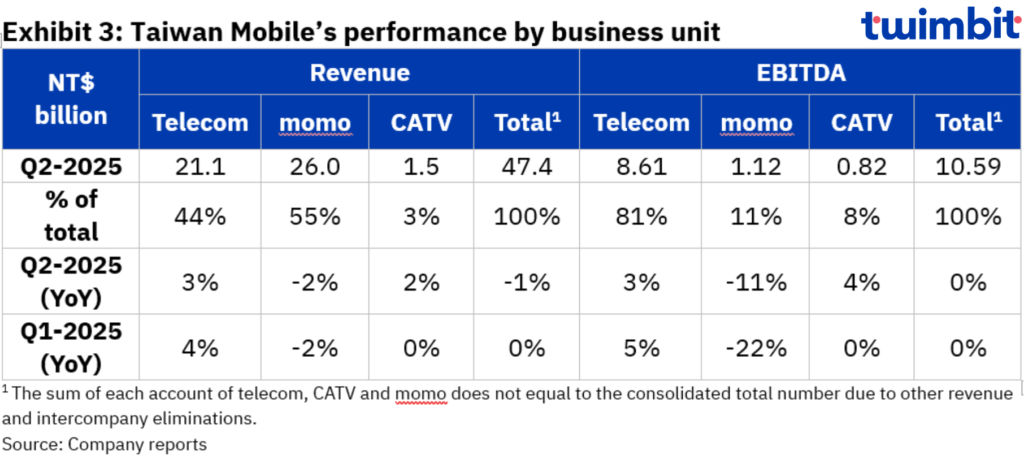

Taiwan Mobile’s commerce revenues face slowdown, yet remains as a strategic priority

- Taiwan Mobile remained a leading player in the beyond-connectivity space, driven by its sizeable commerce portfolio. Non-connectivity revenues contributed 57.9% of total revenues in H1-2025, down 90 bps from 58.8% a year earlier.

- A 2.0% YoY decline in revenues from Momo Inc., the operator’s commerce arm, more than offset cable TV growth, weighing on overall performance and pulling total revenues lower.

- Momo’s revenue decline reflects post-COVID e-commerce normalisation, weaker consumer sentiment, and intensifying competition driving pricing pressure. Elevated investments in marketing, technology, and new platforms like mo-shop+ and retail media, still in early monetisation, further weighed on near-term performance despite steady GMV.

- Nevertheless, the operator continues to invest in commerce, with Momo expanding in-store pickup across 800 myfone outlets and strengthening logistics through new warehouses and Fu Sheng Logistics to enhance omni-channel capabilities and revenue resilience.

Chinese telcos strengthen on back of cloud, AI-push and digital platforms

Chinese telcos are driving strong beyond-connectivity growth through cloud, AI, fintech, and digital content, supported by rising data centre contracts and AIDC integration, reinforcing their transition from traditional telecoms to diversified digital ecosystem leaders in Asia.

- China Unicom reported a 6.1% YoY increase in beyond-connectivity revenues for H1-2025, with the segment contributing 26.0% of total revenues, up from 24.8% in the prior year. This growth was primarily driven by strong performance in cloud and data centre businesses, as data centres saw a notable increase in signed contract value during the period. At the same time, the cloud segment benefited from the integration of AI capabilities and proprietary solutions, which enhanced competitiveness and drove customer adoption. Together, these factors underscore China Unicom’s ability to expand its digital services portfolio and strengthen its positioning in the enterprise solutions market.

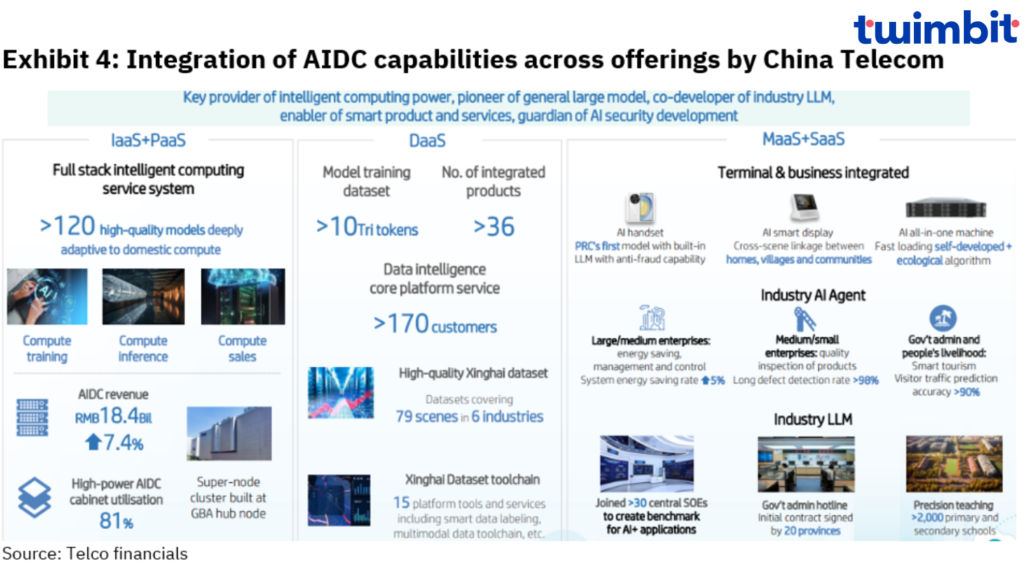

- China Telecom experienced a 4.2% YoY growth in beyond connectivity revenues, making the total contribution of non-connectivity revenues 33.6% increasing by 90 bps in H1-2025. The increase was fuelled by smart family, cloud, and B2C sales, with the operator strengthening its position as a regional innovation leader through large-scale AI integration and deployment of modern, curated digital solutions.

- China Mobile delivered strong performance in H1-2025, with beyond-connectivity revenues rising 11.9% YoY. The segment’s contribution increased to 35.5% of total revenues, up from 31.6% in H1-2024, underscoring its growing strategic importance. Growth was underpinned by an 11.3% YoY increase in cloud services, 24.5% YoY expansion in fintech platforms, and 11.3% growth in digital content revenues. Ongoing innovations and strategic investments continue to position China Mobile at the forefront of beyond-connectivity diversification.

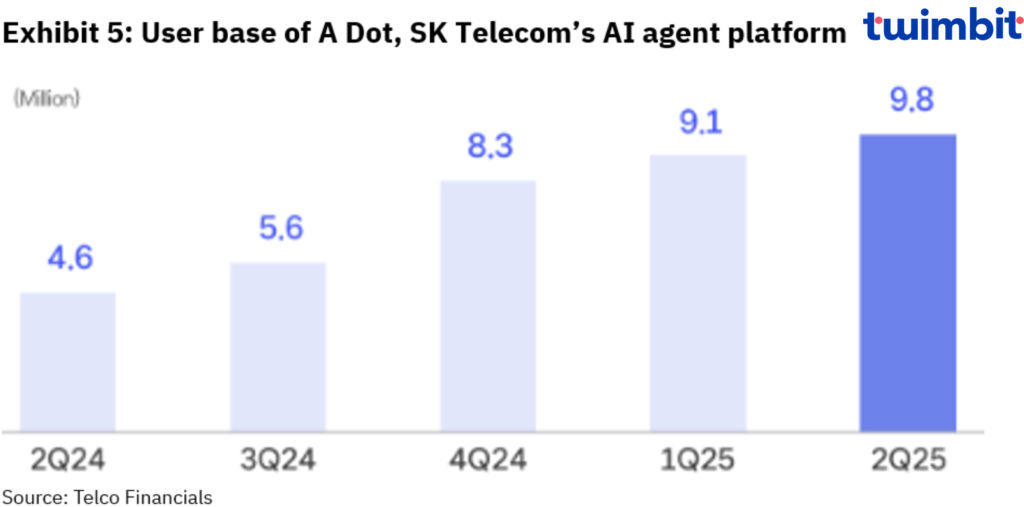

SK telecom repositions for future growth with AI DC and AIX segments, marking shift from legacy services

The South Korean telecom operator reported 3.3% YoY growth in beyond connectivity revenues, with contributions to total revenues reaching 14.3% in H1-2025, up from 13.7% in H1-2024. The growth is largely driven by AIDC and AIX revenues, which represents the data centres, international lease lines, AI cloud and AI-based solutions.

- The AIDC and AIX revenues rose 14.7% YoY in H1-2025, driven by SK Telecom’s entry into GPU supply, GPUaaS rollout, and major data centre partnerships. The operator targets scaling AIDC capacity beyond 300 MW by 2030, underscoring strong long-term growth potential.

- SK Telecom is advancing its data centre strategy through major partnerships, highlighted by a multi-billion-dollar plan with AWS and SK Group to build Korea’s largest AI data centre in Ulsan, reinforcing its regional AI leadership.

- In H1-2025, SK Telecom launched GPU-as-a-Service with NVIDIA H100, advanced AI infrastructure partnerships, and proprietary AI platforms, enabling enterprises to access scalable compute, accelerate model training, and deploy industry-specific AI solutions efficiently.

- While monetisation of these large-scale AI investments is still at an early stage, the lag reinforces future upside potential, suggesting stronger revenue acceleration as enterprise adoption scales and demand for high-performance compute deepens across industries. This strategic positioning ensures SK Telecom is well-placed to convert its early-mover advantage into sustained long-term growth.

- In contrast, IPTV revenues remained flat in H1-2025, with subscriber declines highlighting the shift away from traditional beyond-connectivity services toward newer, AI-driven growth segments.

Bharti Airtel Sharpens Focus on Nxtra and digital TV to Drive Growth

Bharti Airtel reported a 1.2% YoY decline in beyond-connectivity revenues, with the segment’s contribution falling 300 bps to 2.1% of total revenues. However, this understates Airtel’s true diversification, as disclosures capture only digital TV, while detailed enterprise revenues, including data centre and cloud, are not separately reported.

- The operator has been continuously focusing on AI shift and data centre segments as the leading source of value unlock for future. The operator partnered with Perplexity AI and offered its users free 12-month subscription of Perplexity pro.

- Nxtra, Bharti Airtel’s data centre arm, has expanded to 15 hyperscale facilities with a combined capacity exceeding 230 MW. It has committed USD 563 mn over the next three years to scale capacity and support AI-driven workloads.

- Although a decline in digital TV revenues was reported, the operator has been focusing on strengthening the footprint and offerings of the segment. In H1-2025, Airtel revamped digital TV with IPTV expansion, AI-powered Glance TV, OTT bundling, and sharper content strategies, underscoring its shift toward converged, digital-first entertainment experiences. Merger with Tata Play will further solidify Airtel’s position in highly competitive digital TV space.

- Bharti has exited its commodity enterprise business to focus on IoT, security, and cloud services. A market leader in IoT, it is scaling SoC (security operations centre) investments while prioritising proprietary cloud solutions to deliver tailored offerings for internal and external customers.

Research Methodology and Assumptions

- “Top APAC telcos to ace beyond connectivity revenue: H1-2025” report provides a summarised view of Beyond connectivity (non-connectivity) revenue performance of leading telcos in the APAC region for the period Jan-June 2025.

- This report leverages secondary research methodologies and data provided by telecommunication companies (telcos) themselves. Twimbit employs a calendar year approach (January- December) for all telcos to ensure consistent comparison, regardless of their individual fiscal year ending periods.

- The research examined ~49 telcos across 20 Asia Pacific countries. Selection criteria included economic significance and reliable data availability. The research is based on the Beyond Connectivity segments revenues available for 24 telcos analysed.

- For consistent analysis, a constant exchange rate (average for Jan – June 2025) has been applied when converting local currencies to USD.

- Beyond connectivity services in this report exclude traditional voice, data, fixed-line, broadband, and enterprise connectivity services (e.g., IP-VPN, SD-WAN). These services are categorised into four primary buckets, which include, but are not limited to:

- Enterprise Non-connectivity: Managed services, Cloud/Data centres, Cybersecurity, IoT.

- Content and Media: Pay TV, IPTV, OTT services, Content leasing, entertainment services.

- IT Solutions: Professional IT services, curated IT applications, managed services, collaboration platforms, etc.

- Hardware sales: Sale of mobile devices, broadband devices, etc.

- Others: Any service beyond the above categories deemed as beyond connectivity (e.g., E-commerce, Digital marketing, Analytics, Tele-Health).

- The data from prior reports may exhibit variances when compared to the figures presented in this report. This discrepancy arises from meticulous approach, which excludes all previous assumptions and estimations when calculating beyond connectivity revenue.

- The data provided in the report are as reported by the respective telcos or on a calculated basis wherever feasible. These may or may not align with the exact numbers in case the respective telcos have either not disclosed or provided any reference for the above segments (or further sub-segment details).

- The data collected may be subject to reporting inconsistencies inherent to various telcos and hence can be leveraged for reference and guidance purpose. The analysis is based on publicly available information.

Read more:

Global telcos performance benchmarks: Summer 2025