Introduction

The Open Finance market in APAC is rapidly evolving, driven by technological advancements and regulatory support. As financial institutions embrace this shift, they unlock new avenues for innovation and collaboration, positioning themselves at the forefront of the digital finance landscape.

Open finance serves as a critical growth engine for both banks and fintechs, fostering a competitive environment where seamless access to customer data leads to the development of personalized financial products and services. This collaborative ecosystem not only enhances customer experiences but also accelerates financial inclusion across the region. As we delve into the latest updates for this quarter, it’s essential to explore how open finance is reshaping the financial services industry in APAC and the profound impact it has on stakeholders, consumers, and the economy as a whole.

Twimbit open finance radar

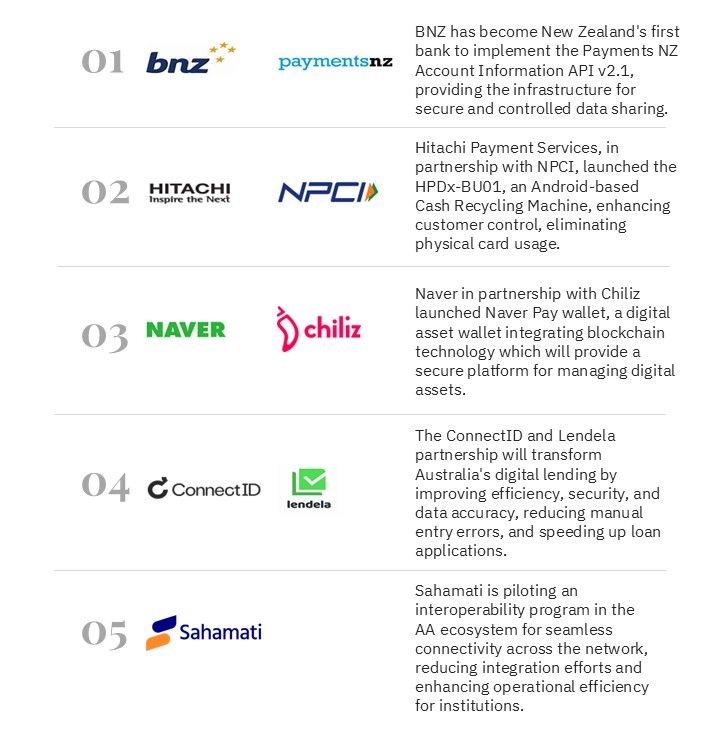

Exhibit 1: Summary of Q3 open finance initiatives

Source: Twimbit analysis

#1 BNZ secures data sharing with Payments NZ API v2.1

Bank of New Zealand’s (BNZ) implementation of Payments NZ Account Information API v2.1 provides the infrastructure for secure and controlled data sharing. This allows customers to decide what data to share, with whom, and when to withdraw access.

BNZ reached this milestone three months ahead of the November 2024 deadline. In 2023, the bank also met another Payments NZ requirement by enabling payments via APIs. Currently, over 250,000 BNZ customers benefit from services like Xero, Volley, and Blinkpay, which connect securely through BNZ’s APIs.

API v2.1 opens the door for fintechs to create valuable services, such as:

- Personalised budgeting tools: Real-time data helps create custom budgeting plans based on spending habits.

- Custom savings plans: Automated savings based on financial behavior and goals.

- Advanced financial insights: Analysis tools that help users understand spending patterns and identify opportunities.

- Streamlined loan applications: Faster and more efficient loan approvals due to comprehensive data access.

- Enhanced fraud prevention: Real-time data access enables better fraud detection by third-party apps.

Adoption of open banking in New Zealand remains low. BNZ must focus on building customer trust in data sharing while maintaining security and transparency. Long-term success depends on increasing customer adoption, collaborating with fintech partners, and addressing data privacy concerns.

Source: Bank New Zealand, Twimbit analysis

#2 Hitachi redefines ATMs with UPI enabled smart machines

In Q3 2024, Hitachi Payment Services, in partnership with the National Payments Corporation of India (NPCI), launched India’s first Android-based Cash Recycling Machine (CRM), known as HPDx-BU01.

This innovation addresses the declining trend in ATM transactions, which fell by 3% from 528 million in January 2024 to 513 million in August 2024, while UPI transactions grew by 23% in the same period.

The HPDx-BU01 Android-Based Cash Recycling Machine is designed to meet a variety of banking needs, offering both banking and non-banking services. Some of the prominent features include:

- QR-based UPI cash withdrawal and deposit

- Account opening services

- Credit card issuance

- Personal loans and MSME loans

- Insurance services

- FASTag application and recharge

A unique feature introduced for the first time in India is the QR-based UPI cash deposit, allowing 24×7 card-less deposits into the customer’s or another account. This innovation enhances customer control, eliminates physical card usage, and improves customer experience with intuitive touch screens.

The CRM machine aims to enhance banking accessibility for everyday users in several ways:

- Expanding banking service access in remote areas.

- Enhances security and convenience by offering a wide range of services through a single touch point.

The collaboration combines the benefits of traditional cash recycling machines with the agility and flexibility of the Android platform, enhancing customer control and cost efficiency for banks.

Source: Hitachi payment services, Twimbit analysis

#3 NAVER Pay wallet brings a new era of digital asset management in South Korea

In Q3 2024, South Korean tech giant NAVER partnered with Chiliz, a blockchain provider for sports and entertainment, to launch the NAVER Pay Wallet. This digital asset wallet is specifically tailored for the Korean market, integrating Chiliz’s blockchain technology into mainstream financial services.

The NAVER Pay wallet offers a secure platform for managing digital assets, starting with NFTs. Built on Chiliz Chain, the first Layer-1 EVM-compatible blockchain built for sports and entertainment. This partnership leverages the rapidly expanding crypto market, valued at USD 6.09 billion in 2023 and projected to grow at a CAGR of 8.8% through 2028.

With 33 million registered users and 18 million daily active crypto users, NAVER aims to streamline digital payments and boost customer engagement through the wallet. Users can benefit from rewards like fan tokens and merchant loyalty programs. Additionally, the wallet will support decentralized applications (DApps), enhancing security by eliminating single points of failure and ensuring data immutability.

This collaboration between NAVER and Chiliz highlights a pivotal moment in integrating blockchain with digital payments, setting a new standard for managing digital assets securely and efficiently.

Source: Naver pay. Chiliz, Twimbit analysis

#4 Lendela and ConnectID partner to accelerate digital lending processes in Australia

ConnectID, a digital identity solution developed by Australian Payments Plus (AP+), has partnered with Lendela, Australia’s first digital loan matching platform. This integration is set to transform the digital lending experience in Australia by improving efficiency, security, and data accuracy for borrowers.

The growing number of personal loan applications in Australia presents challenges related to data security and accuracy. According to the Australian Bureau of Statistics, Australians collectively borrow around USD 1.68 billion each month in fixed-term personal loans, excluding an additional USD 134.1 million in refinanced loans. With such high volumes, the risk of inaccuracies during manual data entry increases, alongside concerns about personal data security.

The partnership between Lendela and ConnectID streamlines customer onboarding and minimises data discrepancies, which are common in loan applications. This integration will pre-fill user information, significantly minimizing manual data entry and reducing discrepancies, which in turn will accelerate the loan application process.

This is a pivotal development for Australia’s digital lending landscape. By combining Lendela’s innovative loan matching platform with ConnectID’s robust identity verification, both companies are poised to deliver a more secure, efficient, and user-friendly experience for borrowers.

Source: ConnectID, Twimbit analysis

#5 Sahamati’s pilot program for interoperability in the Account Aggregator ecosystem

As of August 2024, India’s Account Aggregator (AA) ecosystem has achieved a significant milestone, surpassing 100 million consents, with approximately 80-90 million users actively utilizing the framework. The ecosystem comprises 155 Financial Information Providers (FIPs) and 475 Financial Information Users (FIUs).

Presently, customers must register with multiple Account Aggregators to conduct financial transactions, leading to a fragmented user experience and diminished operational efficiency. While AAs facilitate secure data sharing with explicit consent, the current model complicates management for users.

Sahamati, the industry body overseeing the AA ecosystem, is spearheading a pilot program called SahamatiNet to test interoperability among AAs, FIPs, and FIUs. This initiative aims to establish seamless connectivity across the network, significantly reducing integration efforts for institutions and enhancing operational efficiency.

- Efficiency gains: Interoperability allows institutions to access customer data from multiple sources without separate integrations, reducing costs and saving time.

- Enhanced customer experience: Customers can access their data across all participating financial institutions with a single consent, improving satisfaction and fostering long-term engagement.

Source: Sahamati, Twimbit analysis

Outlook

In Q3 2024, the evolution in open finance highlights the importance of secure, efficient data sharing, which fosters deeper engagement and financial inclusion.

With initiatives like BNZ’s integration of Payments NZ’s Account Information API and innovations such as Hitachi’s UPI ATM and Naver’s crypto wallet, the industry is moving towards frictionless transaction experience. ConnectID’s digital identity verification in Australia further streamlines processes and builds consumer trust. The anticipated launch of account aggregator interoperability promises to elevate data sharing and accessibility across the ecosystem.

As institutions develop dynamic API strategies, prioritise data security, and embrace innovative technologies to thrive in a changing landscape. This will enhance efficiency and transform challenges into exciting opportunities for growth.