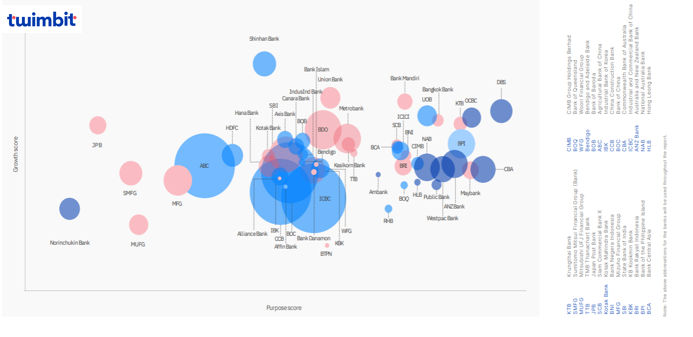

Twimbit Purpose Index, a framework designed to measure how effectively organizations integrate purpose into their core operations. Through this index, we evaluate banks not just on financial performance, but on how well they align their business practices with values that promote positive stakeholder experience.

The last 3 editions of the Twimbit purpose index presents insights and best practices for guiding industry leaders in shaping the future of banking. By providing a comprehensive assessment, it empowers stakeholders to identify banks that are leading the way in creating long-term value beyond the top line.

The table presents key financial metrics and purpose-driven performance of industry leaders from 2021 to 2023, illustrating trends in revenue growth, operating revenue, EBITDA margin, and their commitment to purpose.

| Metrics | 2021 | 2022 | 2023 |

| Number of banks | 28 | 43 | 55 |

| Revenue growth | HDFC Bank was at the forefront of the industry with a revenue growth of 56.25%. | Canara Bank led the industry with an impressive revenue growth of 87.3%. | Shinhan Bank is excelling in the industry with a revenue growth of 44.21%. |

| Operating revenue | ICBC Bank had an impressive USD 116.2 billion in revenue. | ICBC Bank maintained the top spot, generating an operating revenue of USD 133.4 billion. | ICBC Bank leads with a revenue of USD 222.8 billion. |

| EBITDA margin | China Construction Bank excelled in profitability, while SBI falls short of the 62% industry average. | ICBC Bank surpassed the 69.33% industry average, whereas BNI and AMMB fall below this benchmark. | OCBC, DBS, CBA, ANZ, Westpac, Public Bank, NAB, and HLB excel the 63% margin, while BNI and AMMB lag. |

| Purpose Pillars | DBS led purpose driven banking with the highest score for the purpose pillars. | DBS stood out again as the leading bank in the purpose pillars. | DBS continues to lead the purpose pillars. |

Twimbit Purpose Index 2024

Source: Twimbit analysis, bank financials

Key financial metrics and growth analysis

This analysis reviews essential financial metrics for banks in the APAC region, identifying performance trends and underlying drivers.

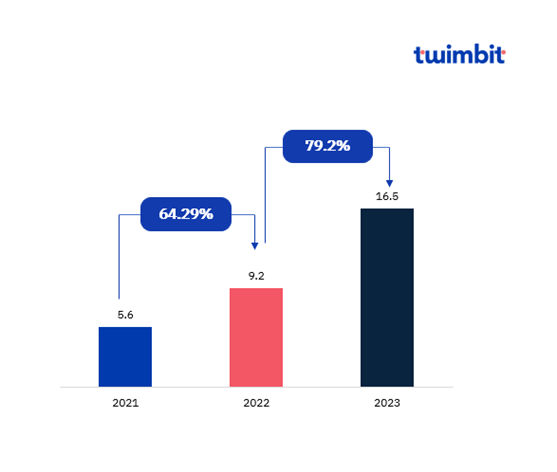

Median average operating revenue

Source: Twimbit analysis, bank financials

- In FY-22, banks in the APAC region experienced a 64.29% YoY increase in their median average operating revenue, rising from 5.6% to 9.2%. This positive trend continued into FY-23, with a further 79.2% YoY growth, pushing the ratio up to 16.5%.

- ICBC Bank achieved the highest YoY growth among all APAC banks, with a remarkable 14.8% growth in FY-22, followed by an exceptional 67.02% growth in FY-23.

ICBC Bank

- At the end of 2023, ICBC’s non-performing loan ratio was 1.36%, reflecting a decrease of 0.02 percentage points compared to the end of 2022.

- At the end of 2023, the balance of domestic RMB loans reached 24.4 trillion yuan, reflecting an increase of 2.9 trillion yuan compared to the start of the year.

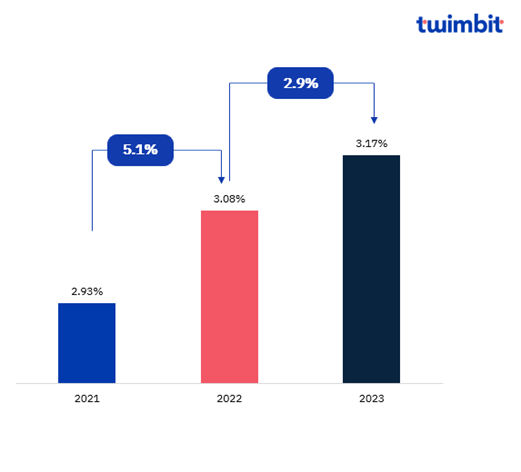

Average net interest margin

Source: Twimbit analysis, bank financials

In FY-22 and FY-23, banks across the APAC region experienced varied trends in their net interest margins (NIMs):

- In FY-22, APAC banks saw a YoY increase of 5.1% in their net interest margin, rising from 2.93% to 3.08%. This growth continued into FY-23, with a further YoY increase of 2.9%, from 3.08% to 3.17%.

- China’s banks experienced the largest decline in Net Interest Margins (NIMs), with an average YoY decrease of 13.57% from FY-22 to FY-23.

- Singapore’s banks saw the highest rise in Net Interest Margins (NIMs), with an average year-over-year increase of 18.2% from FY-22 to FY-23.

China

Some of the drivers of the declining NIMs in China are as follows

- A slowdown in economic growth, particularly in sectors like real estate, has led to reduced demand for loans.

- The reduction in the loan prime rate, which serves as the benchmark for lending rates, has contributed to the compression of net interest margins.

Singapore

- A heightened interest rate environment primarily drove this increase.

- Loan demand saw a significant increase across multiple sectors, including corporate lending.

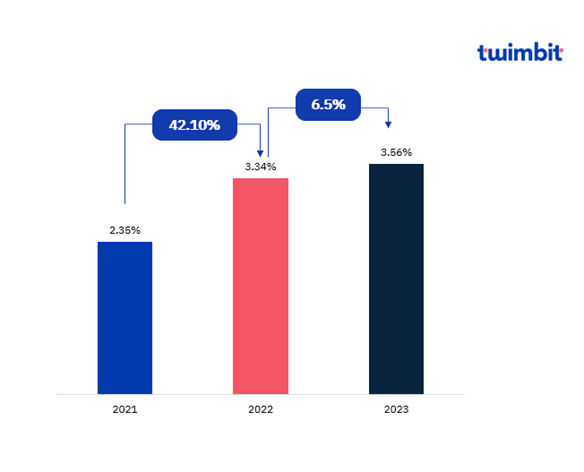

Average non-performing loans

Source: Twimbit analysis, bank financials

In FY-22 and FY-23, APAC banks saw a significant rise in non-performing loans (NPLs):

- In FY-22, APAC banks experienced a 42.1% YoY increase in non-performing loans (NPLs), rising from 2.35% to 3.34%. This upward trend continued into FY-23, with NPL increasing by an additional 6.4%, from 3.34% to 3.56%.

- Indian banks experienced the largest decline in Net Interest Margins (NIMs), with an average YoY decrease of 14.7% from FY-22 to FY-23.

- South Korean banks saw the highest rise in Net Interest Margins (NIMs), with an average year-over-year increase of 37.9% from FY-22 to FY-23.

India

- Strong focus on digital transformation and enhancing customer service, which has collectively contributed to improved asset quality management.

- There has been a significant shift towards retail lending, which generally carries lower default rates than corporate lending. By increasing the proportion of retail loans in their portfolios, banks have effectively reduced their exposure to higher-risk sectors.

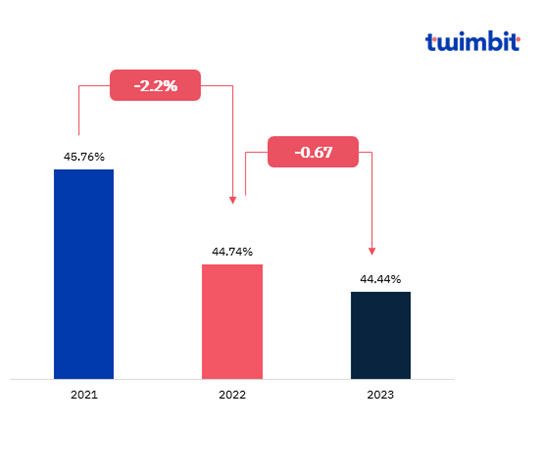

Average cost-efficiency ratio

Source: Twimbit analysis, bank financials

In FY-22 and FY-23, APAC banks generally improved cost-efficiency ratios:

- In FY-22, banks in the APAC region saw a 2.2% YoY decrease in their cost-efficiency ratio, dropping from 45.76% to 44.74%. This downward trend continued into FY-23, with a further reduction of 0.67%, bringing the ratio down to 44.44%.

- Singapore banks experienced the largest decline in cost efficiency with an average YoY decrease of 7.05% from FY-22 to FY-23.

- Malaysian banks saw the highest rise in cost efficiency with an average YoY increase of 10.9% from FY-22 to FY-23.

Malaysia

- Malaysian banks have seen higher operational costs due to inflation and increased spending on technology, staffing, and compliance, which has negatively affected their cost-efficiency ratio as they balance rising expenses with maintaining profitability.

- The highly competitive banking sector in Malaysia has led banks to engage in price wars over deposits and loans, squeezing profit margins. To stay competitive, banks are also increasing spending on marketing and customer acquisition, driving up operating costs relative to income.

Singapore

- The top three banks in Singapore reported strong financial performance, with net revenues growing by 19.2%, from USD 29.7 billion in FY 2022 to USD 35.4 billion in FY 2023. The higher revenue relative to costs indicates improved operational efficiency and profitability for the banks.

- Net interest income rose by 22.2%, from USD 20.1 billion to USD 24.5 billion, driven by increased lending activity and favourable interest rate conditions. This growth in interest income has bolstered profitability and contributed to a reduction in the cost-to-income ratio, reflecting improved operational efficiency.

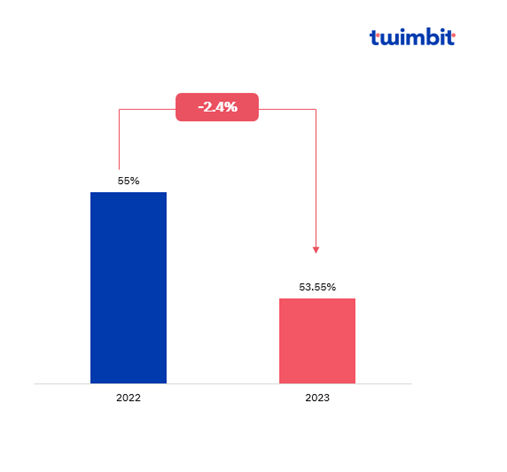

Average CASA

Source: Twimbit analysis, bank financials

- In FY-23, banks in the APAC region experienced a 2.4% YoY decrease in their average CASA ratio, declining from 55% to 53.5%.

- Philippine banks recorded the steepest YoY decline among all APAC banks, with a drop of 9.4%.

Philippine

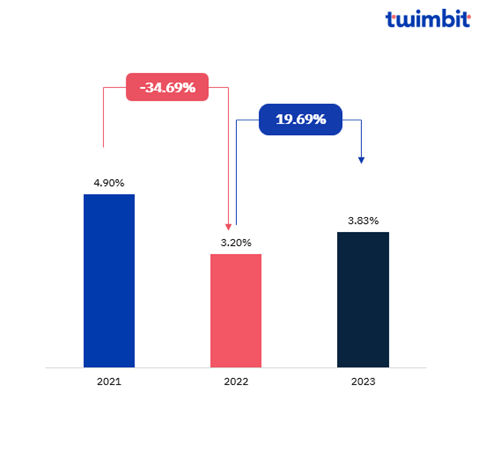

ICT spending to revenue ratio

Source: Twimbit analysis, bank financials

In FY-22 and FY-23, APAC banks saw a decline and subsequent rebound in their ICT-to-revenue ratios, with Australian banks leading in ICT investment, focusing on digital platforms and advanced technologies to boost efficiency and customer engagement.

- In FY-22, banks in the APAC region saw a 34.69% YoY decline in their average ICT to revenue ratio, dropping from 4.9% to 3.2%. However, in FY-23, the trend reversed, with the ratio increasing by 19.69% YoY, rising to 3.83%.

- Australian banks led the way in ICT investment, recording an average YoY increase of 6.1% from FY-22 to FY-23.

Australia

- The growing investment in digital platforms aimed at driving operational efficiency, as well as in digital channels and customer engagement technologies designed to strengthen customer relationships and support them through challenging economic conditions.

- The investment in advanced data analytics, including AI and machine learning, to enable real-time monitoring and alerts in response to the rising threat of fraud and scams.

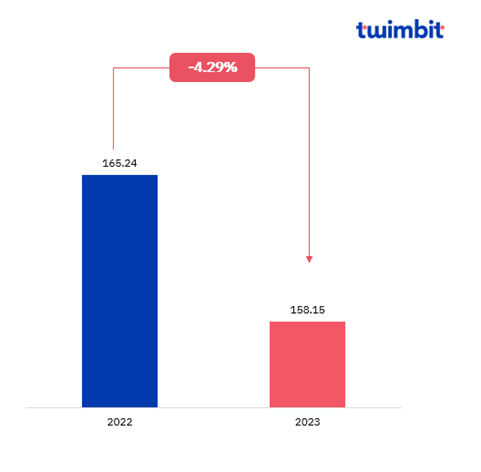

Net fee income

Source: Twimbit analysis, bank financials

- In FY-23, banks across the APAC region saw a 4.29% YoY decrease in net fee income, declining from USD 165.24 billion to USD 158.15 billion.

- Philippine banks experienced the highest YoY growth among all APAC banks, with an increase of 10.06%.

The Philippine’s

- The surge in credit card adoption in the Philippines has significantly contributed to elevated non-interest income growth for banks.

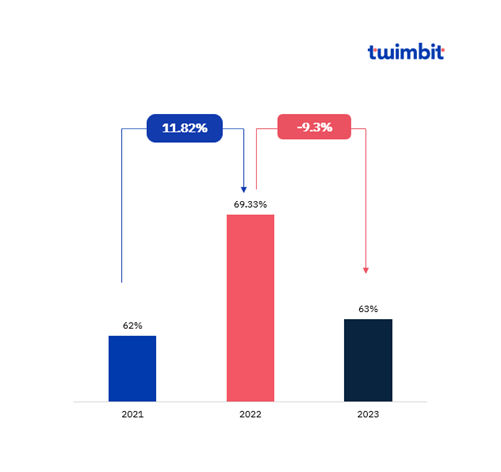

Average EBITDA margin

Source: Twimbit analysis, bank financials

- In FY-22, banks in the APAC region experienced an 11.82% YoY increase in their average EBITDA margin, rising from 62% to 69.33%. However, in FY-23, this trend reversed, with the margin declining by 9.3% YoY to 63%.

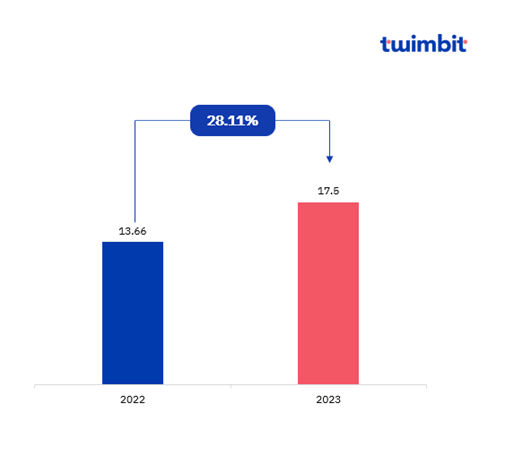

Fee income to revenue ratio

Source: Twimbit analysis, bank financials

- In FY-23, banks across the APAC region saw a 28.11% YoY increase in their fee income-to-revenue ratio, rising from 13.66% to 17.5%.

DBS Bank’s purpose-driven approach to innovation

“We aim to build a company that is here for the long term, based on responsible banking, responsible business practices, and impact beyond banking. Rooted in our culture is a sense of purpose and an innovative drive to create social value and achieve meaningful impact, while balancing our risk and compliance responsibilities.”

— DBS Bank

DBS Bank, headquartered in Singapore, is recognized as one of the leading financial institutions in Asia. It has been at the forefront of adopting purpose-driven banking to transform its business, enhance customer experience, and positively impact society. Over the past few years, DBS has moved beyond being just a traditional bank to becoming a “bank for the future” by embedding purpose into its core strategy. The bank initially focused on economic development, but as it grew, DBS shifted to becoming a customer-centric and technologically advanced bank.

In recent years, DBS has embraced a purpose-driven banking model, guided by its corporate mission to be the “Best Bank for a Better World”. This involves aligning its operations with Environmental, Social, and Governance (ESG) principles, sustainable financing, digital innovation, and community engagement. This strategic approach leverages tech-driven innovation and customer-centricity to drive sustainable financial growth and bolster shareholder returns.

To accelerate this transformative agenda, DBS Bank invested USD 961.2 million in information technology in FY-2023. This significant investment underscores its commitment to leveraging advanced technologies like AI, blockchain, data analytics, and automation. These tools are pivotal in creating holistic value for customers, employees, shareholders, and the planet, reflecting DBS’s comprehensive approach to digital transformation.

DBS strategic initatives

DBS has effectively utilised several strategic initiatives to strengthen its market position and enhance customer experiences:

- Personalising customer experiences: DBS enhances engagement with personalised nudges and alerts, offering investment insights to strengthen relationships.

- Focus on key customer segments: The bank’s strategic focus on retail clients, wealth customers, and SMEs allows tailored offerings for sustained leadership.

- Defending market share in deposits and mortgages: Utilisation of AI/ML, increased digitalisation, and partnerships to effectively manage deposits and reduce mortgage attrition.

- Improving customer experience in Singapore retail: In the Singapore retail sector, DBS has enhanced the customer experience by reducing turnaround times and streamlining the onboarding process.

- Strengthening market leadership: Reinforced market leadership, particularly in Bancassurance, across digital and traditional channels.

- Adopting managing through journeys (MtJs): The wider adoption of MtJs has improved cross-functional collaboration within the bank, resulting in more tailored, data-driven solutions.

- Leveraging AI, machine learning, and experimentation: Through the integration of AI/ML and fostering a culture of experimentation, DBS continues to refine its offerings, ensuring ongoing improvement and innovation in customer experience.

- Digital and financial literacy: DBS Bank had invested SGD 1 million, through the DBS Foundation to boost digital inclusion in Singapore via the Digital for Life initiative alongside the Infocomm Media Development Authority (IMDA).

- Empowering education via digital payments: Partnership with the Ministry of Education to implement digital payments in 330+ schools for 400,000 students.

- Digitisation of operations: The operations processes and platform re-engineering program enhanced employee productivity by over one million hours. The digitalisation reduced risk incidents by 54%, even as transaction volumes have doubled, showcasing operational efficiency and risk management improvements.

Collectively, these efforts position DBS as a leader in delivering differentiated banking services, underpinned by cutting-edge technologies and strategic customer focus.

Impact

DBS’s transformation initiatives have delivered substantial outcomes, including

- Engaging over 3.5 million users monthly and facilitating more than 30 million personalised interactions underscores the success of DBS’s digital-first strategy.

- Between 2021 and 2023, the organization expanded its customer journeys from 25 to over 60 by implementing managing through journey (MtJ). This strategy led to enhanced customer satisfaction, faster turnaround times, and a positive impact on revenue.

- In FY-23, DBS Bank’s consumer banking achieved a customer engagement score of 4.22.

Key takeaways from DBS’s digital transformation include:

DBS Bank’s focus on digital transformation, personalization, customer-centric innovation, and purpose-driven initiatives has set a benchmark for customer experience in the banking industry. By adopting DBS’s strategies, other banks can enhance customer satisfaction, loyalty, and overall business growth.

- Digital-first approach:

- Streamline services with mobile banking to reduce friction.

- Use AI and automation for tasks like onboarding and customer queries.

- Data analytics for personalisation:

- Leverage data for personalized recommendations and financial advice.

- Implement AI tools for targeted customer engagement and cross-selling.

- Customer-centric innovation:

- Foster a culture of innovation to solve customer pain points.

- Involve customers in co-creation and testing of new services.

- Integrate banking seamlessly into customers’ lifestyles (Banking-as-a-Service).

- Omnichannel experiences:

- Ensure seamless interactions across mobile, online, and physical branches.

- Integrate customer data for consistent service across channels.

- Enhance self-service options while maintaining human support for complex issues.

- Empowering employees:

- Invest in employee training to improve customer service.

- Automate routine tasks to focus on value-added customer interactions.

- Encourage employee innovation for better service delivery.

- Sustainability and social responsibility:

- Offer sustainable financial products like green loans.

- Align with ESG initiatives to resonate with socially conscious customers.

- Commit to a purpose-driven mission for deeper customer loyalty.

- Continuous feedback and improvement:

- Actively gather customer feedback to enhance products.

- Track metrics like Net Promoter Score (NPS) for service quality.

- Use customer insights to iteratively improve offerings.

DBS’s transformation provides strategic insights for banks aiming to modernise. It exemplifies how a digital-first mindset, combined with strategic technology deployment and personalised customer experiences, can reshape the banking landscape and drive a purpose driven growth.

Innovations by leading banks

These are the key initiatives by leading banks to improve customer experience, employee engagement, partner collaboration, and environmental impact throughout 2021 to 2023.

2021

- #1 Customer Experience

- DBS

- NAV planner: An intuitive financial tool offering over 30 million personalized insights to enhance digital banking.

- Property marketplace: An online platform for searching property listings with paperless transactions.

- Maybank

- GO Ahead. Take Charge Platform: Empowers customers to manage personal finances.

- ICICI Bank

- InstaSave Account: Simplifies onboarding in just 7 clicks.

- Online Real-time Dispute Resolution: Data science-powered real-time dispute resolution.

- #2 Employee Experience

- DBS

- Future Smart Programme: Equips employees with future skills in AI and ML.

- Hackathons: Regular events to foster innovation.

- Bank Rakyat Indonesia

- Employee Empowerment Initiatives: Continuous digital upskilling programs.

- HSBC Bank

- Diversity and Inclusion Initiatives: Engages younger employees in financial literacy projects.

- #3 Partner Experience

- Commonwealth Bank of Australia

- Digital Procurement Initiatives: Enhances supplier journey and transparency.

- Public Bank

- E-Procurement System: Streamlines supplier processes.

- National Australia Bank

- Programs: Commitment to diverse supply chains.

- Sustainability-focused Procurement: Integrates sustainability principles into procurement.

- #4 Planet Experience

- Hong Leong Bank

- HLB SME Solar Financing: Supports SMEs in adopting solar energy.

- HLB Jumpstart Initiative: Financial support for sustainability-focused start-ups.

- Public Bank

- Recycled Plastic Debit Card: Eco-friendly card to reduce plastic waste.

- Money Master Programme: Educates students on financial management.

- Bank of Queensland

- Commitment to Carbon Reduction: Ceasing funding for fossil fuel extraction.

- Energy Efficiency Initiatives: Trials for solar panels and LED lighting.

2022

- #1 Customer Experience

- National Australia Bank

- NAB Hive: A digital merchant portal for micro and small businesses, offering tailored advice and real-time transaction monitoring.

- NAB Now Pay Later: A BNPL service accessible from the NAB app, streamlining the credit check process.

- ANZ Bank

- ANZ Plus: A digital banking platform simplifying financial management with goal-saving features.

- Breathe Branches: Low-carbon footprint design initiative for branches.

- UOB Bank

- UOB TMRW: Digital platform providing AI-driven insights for personalized experiences.

- UOB Rewards+: Cashback program at over 20,000 merchants.

- #2 Employee Experience

- Bank of the Philippine Island

- Learning and Development: Provides robust learning with extensive training modules.

- Be Well Program: Focuses on holistic employee well-being.

- Maybank

- Digital HR Transformation: Streamlines HR processes for better employee experience.

- Empowerment through Career Ownership: Programs to enable employee career control.

- Commonwealth Bank of Australia

- Mental Health Support: Appoints a Chief Mental Health Officer for workplace initiatives.

- Wellness Initiatives: Various programs to support employee well-being.

- #3 Partner Experience

- ANZ Bank

- Sustainable Procurement Practices: Development of practices prioritizing sustainability.

- Supplier Collaboration: Aligning with suppliers for sustainability goals.

- DBS

- Partnership with SAP Ariba: Streamlines supplier interactions.

- Supplier Benefits: Features like invoice automation and online catalogs.

- Westpac Bank

- Supplier Inclusion and Diversity Program: AUD $19 million investment for diverse suppliers.

- Supplier Sustainability Principles: Encourages adherence to responsible sourcing standards.

- #4 Planet Experience

- Siam Commercial Bank

- Launch of Robinhood: Non-profit food delivery platform supporting local restaurants.

- Support for Local Small Businesses: Provides education on sustainable practices.

- Bendigo and Adelaide Bank

- Energy Efficiency and Carbon Reduction Initiatives: Implemented energy-saving projects.

- Public Bank

- Recycled plastic debit cards to reduce plastic waste.

- Money master program: Improves financial literacy in the younger generation.

2023

- #1 Customer Experience

- Maybank

- M-CONNECT: Expanded ecosystem offering seamless digital experiences, including instant home loan approvals.

- Etiqa Digital Engagement: Advanced analytics driving customer interactions in insurance.

- ICICI Bank

- API Platform: Robust platform with over 600 APIs for personalised financial services.

- Krungthai Bank

- Pao Tang Mobile App: Offers diverse digital services for over 40 million users.

- Google Cloud Collaboration: Enhances API management and secure services.

- #2 Employee Experience

- ANZ Bank

- Cloud Migration and Employee Support: Enhanced resilience and efficiency through cloud migration.

- Westpac Bank

- AWS Cloud Training: Provides training in cloud solutions for employee productivity.

- Employee Assistance Program: Comprehensive mental health and counselling support.

- AmBank Group

- Digitalisation of HR Functions: Streamlining HR processes for better workplace satisfaction.

- Well-being and Safety Initiatives: Programs for mental health support and work-life balance.

- #3 Partner Experience

- China Construction Bank

- CCB Cloud: Comprehensive financial cloud solution for scalable services.

- Multi-Zone, Multi-Region Collaboration: Facilitates cross-regional partnerships.

- OCBC Bank

- Embedded Finance Solutions: Over 500 APIs for partner integration.

- Generative AI Tools for Partners: Collaboration with Microsoft for AI tools.

- AmBank Group

- Carbon Accounting Software for SMEs: Supports SMEs in tracking carbon emissions.

- #4 Planet Experience

- Bank of Queensland

- Charity-Linked Debit Cards: Debit cards contributing to various charities.

- Sustainability Partnerships: Integrating environmental and social considerations into partnerships.

- DBS

- Sustainability Reporting & Carbon Reduction: Framework for carbon reduction and sustainable infrastructure.

- Green Financing & Investments: Portfolio expansion supporting renewable projects.

- AmBank Group

- Greening Value Chain Programme: Carbon accounting software for SMEs.

- Carbon Credit Acquisition: Acquired carbon credits for sustainability commitments.

Conclusion

As the insights from the Twimbit Purpose Index reveal, banks that prioritise a higher purpose—whether through sustainable investments, ethical lending practices, or community engagement—are not only contributing to societal well-being but also positioning themselves for long-term success. By embedding purpose into their strategies, banks are better equipped to build trust, enhance customer loyalty, and create value that extends beyond financial returns. The journey toward purpose-driven banking may not be without its challenges, but the rewards are clear: a resilient, sustainable, and inclusive financial ecosystem that benefits all stakeholders.

A prime example is DBS, which has achieved the highest score in the Purpose Index, setting a benchmark for how banks can embed purpose into their core operations. By aligning its business model with values that prioritize customer trust, social impact, and environmental sustainability, DBS has demonstrated that banks can thrive while driving positive change.

Meanwhile, ICBC stands out with the largest operating revenue among APAC banks, proving that scale and profitability can go hand in hand with efforts to address broader economic and social issues. These examples illustrate that whether it’s through a commitment to purpose or financial scale, banks have diverse paths to creating meaningful impact.

As banks continue to transform, it is imperative that they embrace this paradigm shift—not just as a compliance exercise, but as a strategic imperative. Purpose-driven banking is not just a trend; it is the foundation of a future where finance is a force for good.