Context

The global telecoms industry is experiencing a profound transformation, fueled by rapid advancements in technology and shifts in consumer expectations. As traditional revenue streams mature, telecom leaders are increasingly pivoting to new growth engines centered around non-connectivity and sophisticated enterprise solutions.

This inaugural report aims to highlight best practices, identify areas for improvement, and celebrate the innovators who are reshaping the telecom industry.

We have strategically selected thirty telecom operators from diverse geographies to provide a global perspective on the industry performance, covering critical financial and operational benchmarks as well as insights into their growth strategies.

Exhibit 1: The thirty operators selected from diverse geographies

Overview of global in 2023

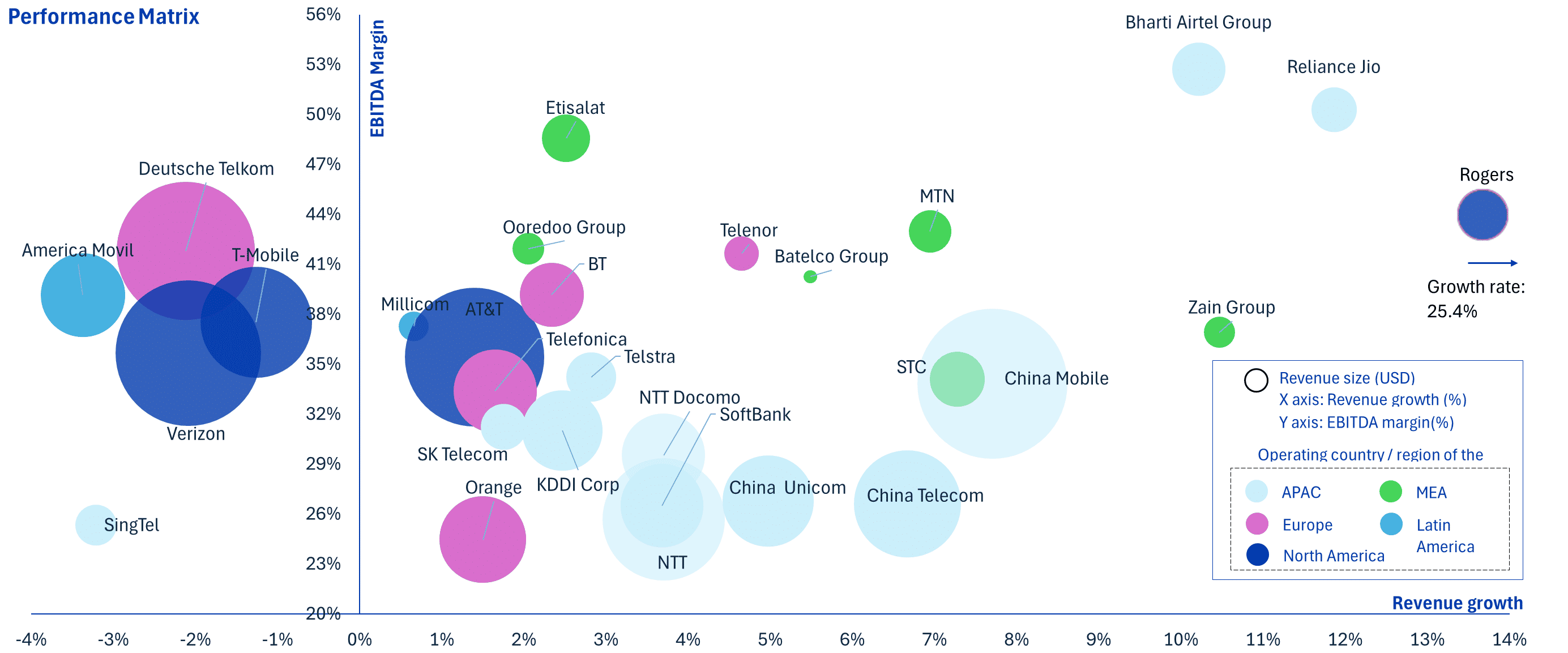

Exhibit 2: Performance benchmark of leading 30 telecom operators across key financial metrics

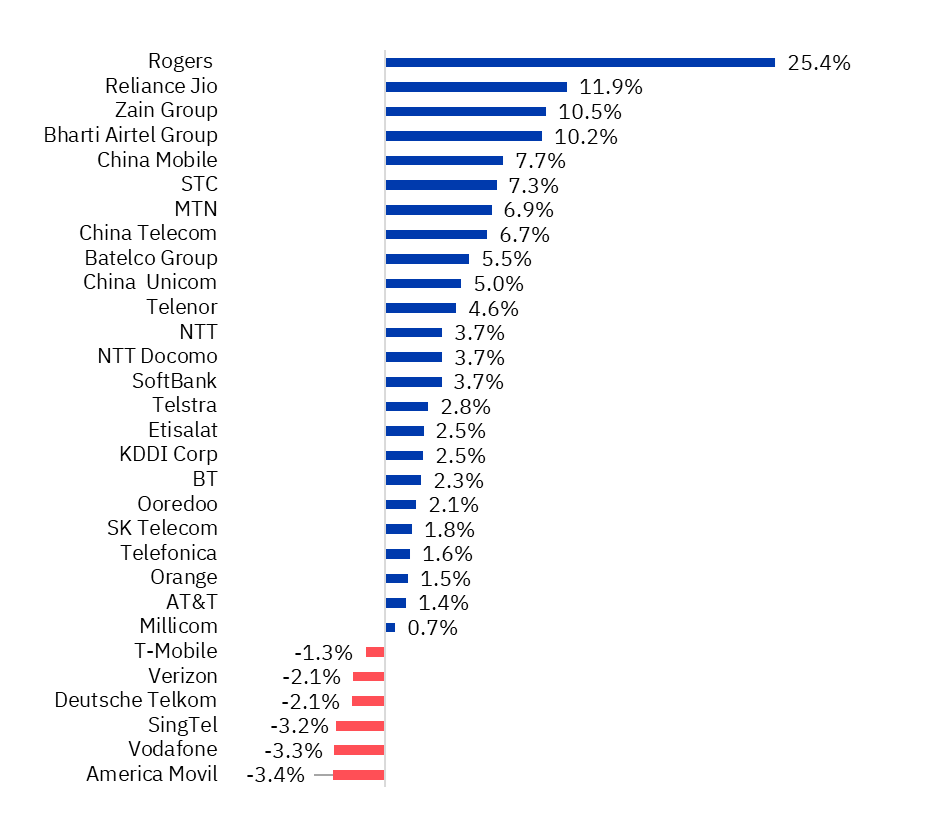

- In 2023, global telecommunications industry faced a nuanced performance landscape, marked by a slight dip in average revenue growth from 3.1% in 2022 to 2.8% in 2023.

- The decrease was paired with a marginal contraction in EBITDA margins from 36.6% to 36.2%.

- Notably, Chinese, Middle Eastern, and Indian operators emerged as key growth engines, with Chinese operators leveraging 5G and cloud services, Indian companies focusing on postpaid subscriber gains, and Middle Eastern telcos benefiting from regional growth trends.

- Despite the revenue uptick, the sector saw a significant pullback in capital expenditures, which decreased by 12.5% due to the advanced stages of 4G and 5G network deployments.

- The industry landscape was also reshaped by numerous mergers, notably Rogers’ strategic merger contributing to a notable 25.4% revenue growth, marking the highest among evaluated operators.

Exhibit 3: % Revenue change 2023 (YoY)

Capital market analysis

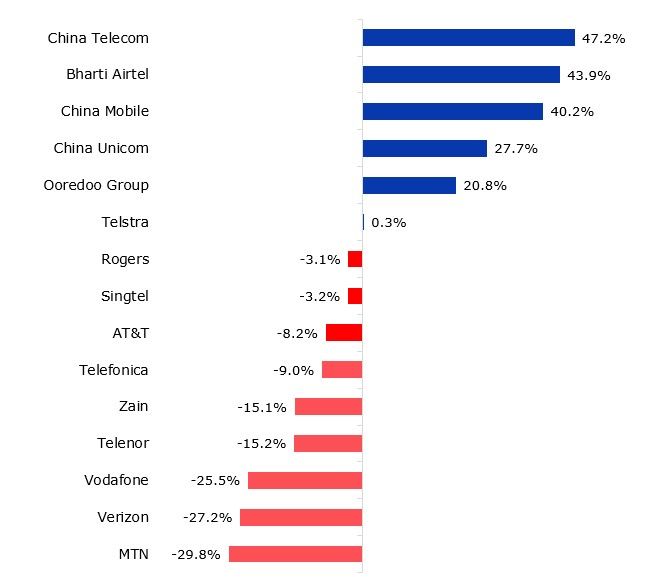

- Capital market sentiments in 2023 reflected regional disparities: Indian and Chinese telcos experienced appreciable stock price appreciation due to robust operational performance and market optimism.

- In contrast, European operators saw declines amid tougher regulatory and competitive environments.

- The stock performance also highlighted an emerging divergence in valuation metrics, with enterprise value-to-EBITDA ratios and P/E ratios varying significantly across regions, underscoring differing investor expectations and market potential

Exhibit 4: % Stock price change 2023 (YoY)

Operator playbook for 2024

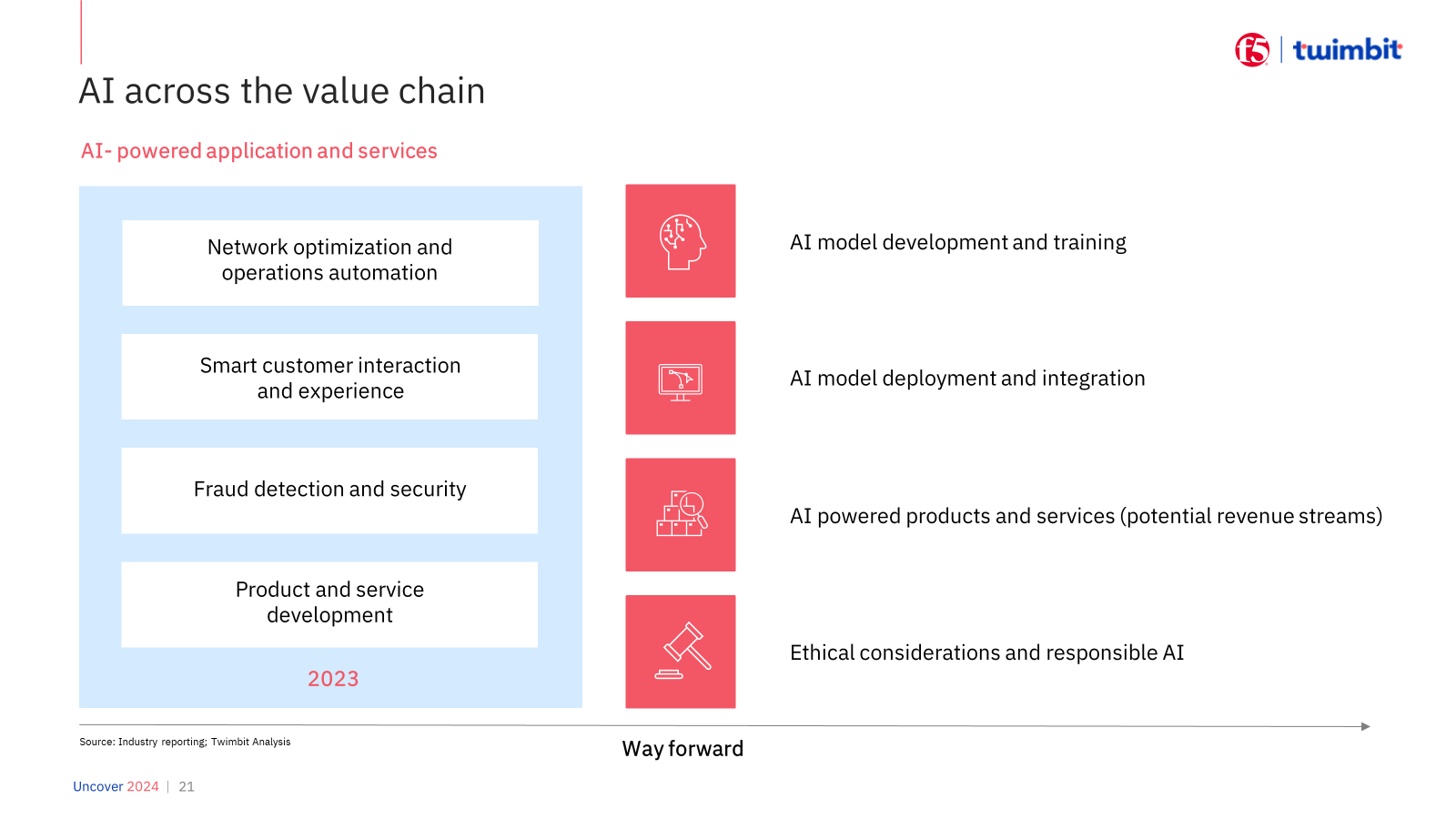

AI a potential game changer: The inception of the Global Telco AI Alliance marks a pivotal moment. Operators should not only adopt AI technologies but also pioneer developments to gain a competitive edge. AI’s potential to optimize network operations and enhance customer experience is immense. Forward-thinking firms will use AI to differentiate their services, optimize costs, and spearhead innovations.

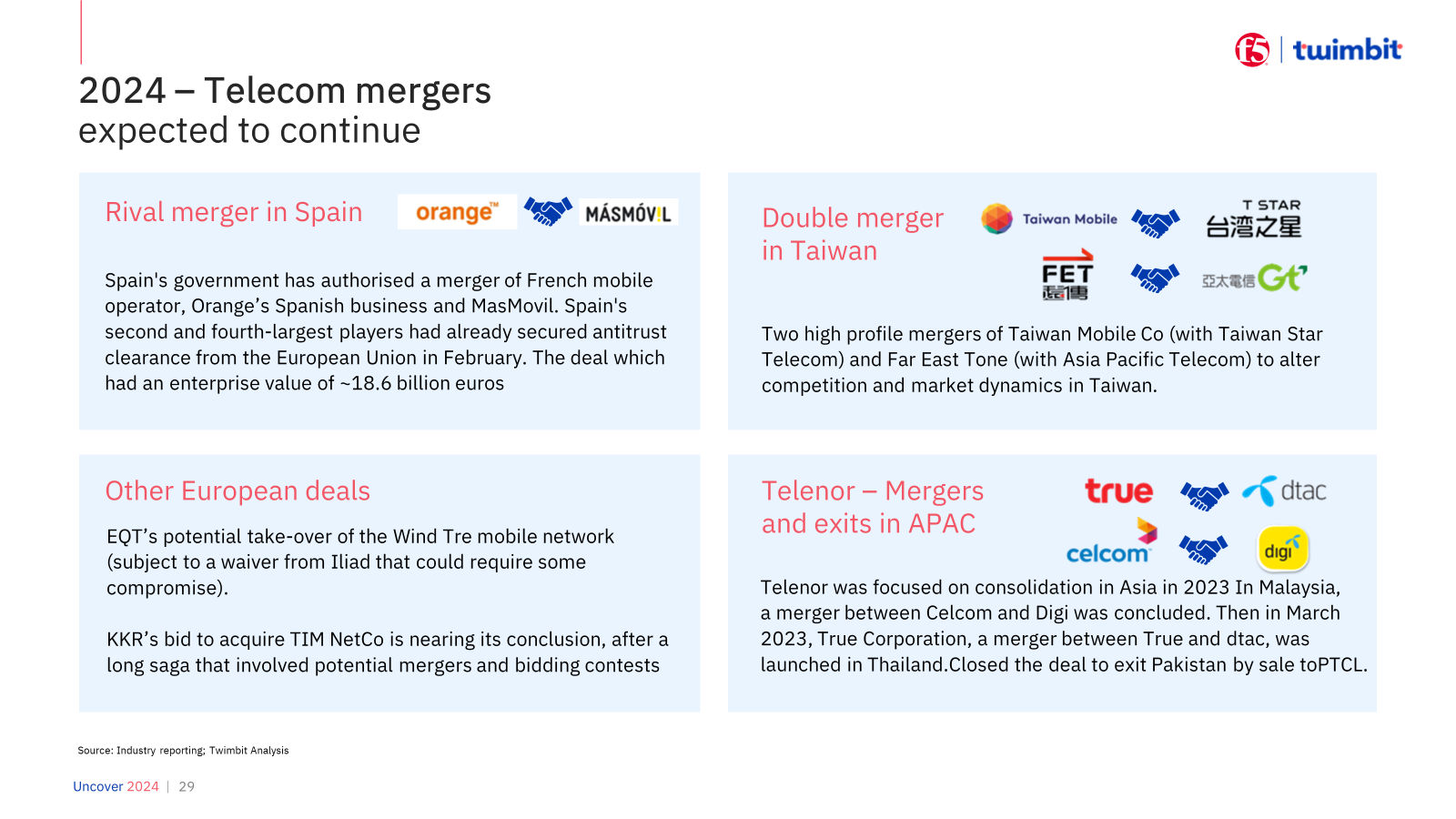

Consolidation gains momentum: The trend of strategic mergers is reshaping the telecom landscape, allowing companies to amalgamate resources, expand service territories, and enhance service quality. Operators must view mergers as opportunities to drive scale, synergize technologies and capabilities, thereby delivering superior customer value.

Capitalizing on regional growth dynamics: With significant growth noted in the Middle East, China, and India, operators in these regions continue to see growth with expansion into rural markets and improving data consumption. For European operators facing declines, enhancing the customer value proposition will be crucial. Several Asian telcos have led the way in driving non-connectivity and enterprise business growth. This could be the conduit to reignite growth in the region.

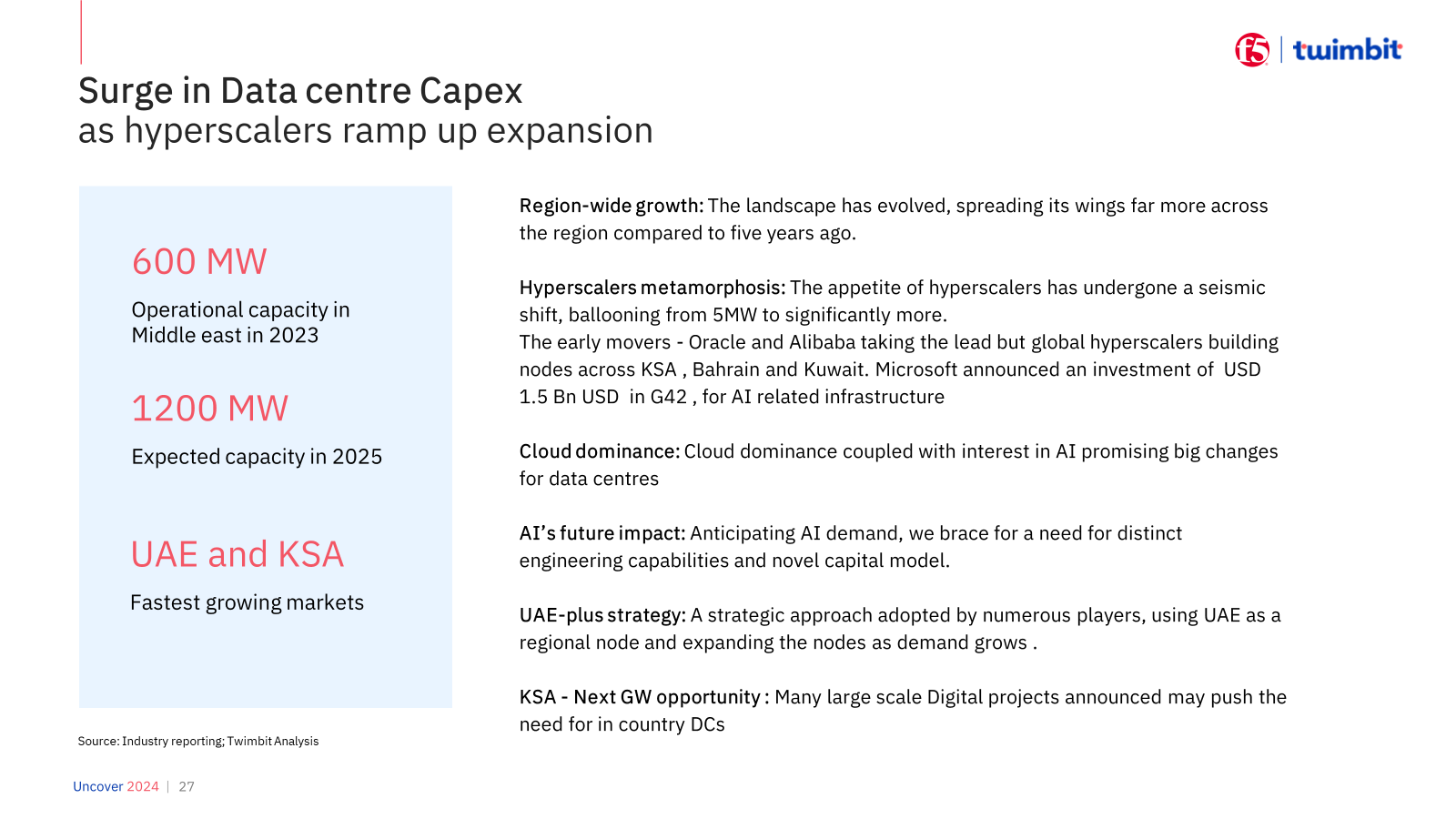

Investing in digital Infrastructure: The surge in demand for data center capacity and integration of AI are indicative of the sector’s growth potential. Operators should increase investments in these areas to ensure they remain at the forefront of the digital services revolution.

Strategic expansion via satellite communications: The embrace of satellite broadband to counter connectivity limitations in remote areas will help bridge digital divide. This not only diversifies service offerings but also expands market reach. Operators like Telstra partnering with Starlink are setting a precedent for global connectivity that others should consider emulating, especially to tap into underserved or unexplored markets.

Navigating regulatory landscape: Increased regulatory scrutiny, especially concerning mergers and digital expansions, requires operators to maintain agile compliance strategies. Engaging with regulators and shaping policy discussions can mitigate risks and favorably influence growth opportunities such as sovereign cloud and market consolidation.

In conclusion, telecom leaders should not only adapt to these changes but also actively shape them. The convergence of AI, digital infrastructure expansion, and strategic mergers provides a robust platform for sustainable growth. By staying ahead of technological trends and aligning them with business strategies, operators can secure a dominant position in the global telecom arena.

Uncover 2024 (Global telcos) is a strategic report developed in partnership with F5.

Read the coverage for APAC telcos here