Being one of Singapore’s ‘Big 3’, UOB Bank has approximately 73 branches and offices in Singapore, offering sensational customer service in 19 countries and regions. Currently, UOB’s four core markets are Singapore, Indonesia, Malaysia and Thailand, while establishing an external presence in Mainland China, Vietnam, and Hong Kong.

Financial highlights

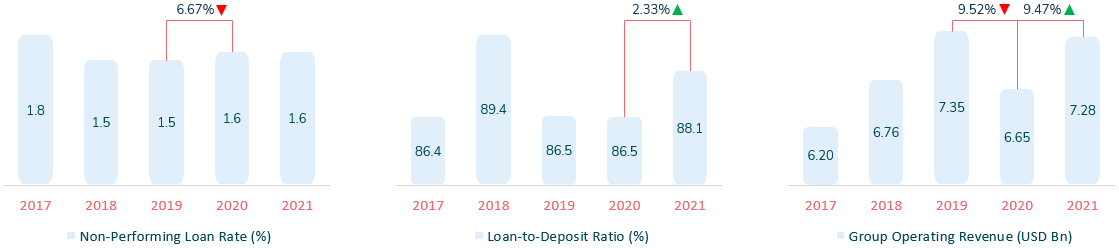

The NPL (Non-Performing Loan) rate at UOB increased by 6.67%, from 1.5% in 2019 to 1.6% in 2020. And with a constant 1.6% maintained in 2021, it becomes clear that UOB’s loans are of reasonable quality.

Meanwhile, the LDR (Loan-to-Deposit) ratio increased by 2.33%, from 86.5% in 2020 to 88.1% in 2021. It came close, but not quite, as it struggled to top its remarkable 89.4% in 2018, proving UOB’s decline following 2018. Ideally, the LDR ratio should be between 80% to 90%. Fortunately, as it stands, UOB is on the positive, standing on the higher end of the threshold.

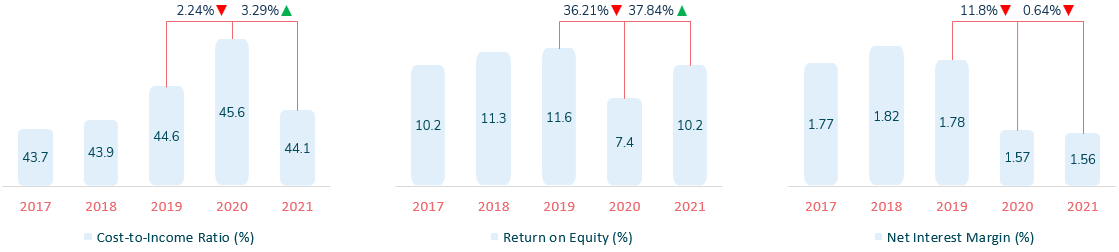

As for the net interest margin (NIM), UOB experienced a significant dip of 11.8%, from 1.78% in 2019 to 1.57% in 2020. The NIM currently stands at 1.56% in 2021. Hence, if UOB aims to keep the NIM from falling deeper in the following years, the bank should look to maintain its current LDR ratio.

When it comes to Singaporean banks, they generally operate at high cost-to-income ratios compared to banks in other regions of APAC. For example, in 2019, banks in Singapore reported a cost-efficiency ratio of 57.96%. However, UOB reported a much lower cost-to-income ratio, charting only 44.6% in the same year (Figure 1), marking a negative difference of 13.36% against other Singaporean banks.

If that wasn’t enough, UOB took another hit, with the cost-to-income ratio increasing by 2.24% in 2020. Fortunately, the bank has managed to keep it in check in 2021, operating at a cost-to-income ratio of 44.1%.

Strategic focus areas

- #1 Being SMEs preferred banker

UOB’s clients needed help, and UOB were well-aware of the situation. Thus, the bank made it its mission to help its clients build resilient business models for the long run. It began by introducing three specialised programs to help make this mission a reality.

i. UOB BizSmart – an integrated suite of cloud-based business solutions targeted at SMEs. Since its launch, it has benefitted more than 16,000 SMEs in Malaysia, Indonesia, Singapore and Thailand. UOB BizSmart encompasses 6 key areas, which are;

– accounting,

– HR and payroll,

– digital transaction,

– digital marketing and collaboration,

– POS and payment,

– and corporate services.

ii. UOB BizMerchant – an unsecured loan program tailored to help online businesses on e-commerce platforms. The bank used a unique approach to determine the creditworthiness of borrowers, which involved analysing the revenue data gathered from the various e-commerce platforms.

iii. EasyStore – a platform for e-commerce sellers to sell and manage their business across multiple channels. It works to compile data from Shopee, Lazada, WhatsApp, Facebook, Instagram, Facebook Live and other platforms.

- #2 Helping businesses grow

Singapore: UOB managed two ASEAN tech summits, where more than 25 of the tech start-ups from the region displayed their solutions to more than 300 SMEs.

Malaysia: UOB conducted two cohorts of the ‘Jom Transform’ programme to equip businesses with the tools, know-how and confidence to transform digitally.

Thailand: UOB organised multiple webinars to better comprehend how data analytics helps to analyse consumer needs, customise products and develop advertising campaigns, all a part of the ‘Smart Business Transformation’ programme.

China and Indonesia: UOB facilitated the currency exchange as the appointed cross-currency dealers (ACCDs) for the Indonesian Rupiah (IDR) and Renminbi (RMB), making UOB the first Singapore bank to hold licences in both markets.

- #3 Delivering an exceptional and omni-channel CX

UOB adopted an omni-channel approach to provide a progressive and personalised customer experience in both the physical and online space.

On the physical front, UOB engineered;

– lifestyle branches for young professionals and young families,

– wealth centres for the rich and the emerging affluent,

– and a business centre for entrepreneurs and small businesses.

In the online space, UOB developed UOB TMRW with several unique services, such as;

– SimpleInvest,

– UOB Rewards+

– PayNow-PromptPay

- #4 Sustainability & ESG integration

UOB provides a suite of green loans and sustainable investments to help encourage a sustainable lifestyle, which covers property, electric vehicles (EV), and solar panels.

UOB Sustainable Future Home Loan: For home buyers searching for properties with the Green Mark certification by the Building and Construction Authority Singapore.

UOB Sustainable Future Car Loan: For EV buyers, with a loan applicable to over 90% of new EV models in Singapore.

The U-Solar programme: An interest-free instalment plan for solar panels that customers can purchase with their UOB credit card.

UOB quadrupled their total asset under management in ESG-focused investments for their retail customers in 2021. UOB has also issued Singapore’s first sustainability bond and has introduced a handful of ESG-focused investments.

- #5 Championing employee experience

Everyone knows the customer is king, yet UOB believes their employees should also be treated with the same level of care and attention. To demonstrate, OCBC developed the Better U Programme to equip employees with five core competencies: growth mindset, problem solving, digital awareness, human-centred design and data storytelling.

Welfare is also a primary concern for UOB, with the bank providing vaccination support for the employee. In addition, UOB provided vaccination exercises at UOB premises and teleconsultations for employees to seek medical advice at home.

On top of that, UOB provides exclusive staff deals through merchant collaboration for the employee. For example, the bank offers various lifestyle and wellness promotions on its staff exclusive, MyUOB portal.

Digital strategy

- #1 Building superior digital experiences

Looking to overhaul its digital experience, UOB launched its new and improved UOB TMRW in 2021, acting as the successor to UOB Mighty. Currently, the new platform has sealed its position as UOB’s primary mobile digital banking application. This is because it rectified several pain points of its predecessor, from its complicated design to the stability issues and bugs. The best part is that UOB guarantees its customers to consistently update the current platform, ensuring its security while adding new features to keep its competitive edge.

The bank also introduced regional-based services to serve the market’s unique needs.

– Indonesia: TMRW Pay and TMRW Power Saver

– Thailand: TMRW CashPlus

UOB did not forget about its customers as well, launching specialised applications to serve the varying types;

– UOB TMRW for consumers

– UOB SMEs for SMEs

– UOB Infinity for corporate clients

- #2 Hyper-personalised online offerings

To capitalise on personalising its offerings for the customer, UOB split this strategy into 3 categories, prioritising:

– digital solutions – UOB BizMerchant and SimpleInvest are digital solutions targeted to particular customer services.

– phygital accessibility – UOB enabled online account opening and allowed customers to apply for a loan online with UOB Property Loan.

– exclusive rewards and benefits – UOB offers preferential rates for corporate clients that book foreign exchange online directly with UOB Infinity and provides cashback or gift cards for customers that apply for a loan online with UOB Property Loan.

- #3 Preparing for the digital future

UOB frequently hosts or participates in events such as fintech exhibitions, summits and panel discussions to communicate UOB’s vision of the future for disruptive technologies and its implementation possibilities in the UOB ecosystem.

UOB also intends to build a team capable of quickly adapting to new technology. To achieve this, the bank assembled a specialised department, better known as the ‘TMRW and digital banking division’, with two main objectives: accelerating growth and maintaining its competitive edge in the digital space.

UOB’s digital consolidation with TMRW

- #1 UOB TMRW – An all-in-one banking app

Features AI-driven insights that are personalised for customers.

Provides benefits and perks through Rewards+

Allows customers to manage their accounts, credit cards, investment, and transaction on the go.

Unlocks access to bill payment, Buy Now Pay Later (BNPL), and various instant payment facilities locally and in Thailand.

- #2 TMRW Pay – An e-commerce checkout loan

Allows Indonesian shoppers to defer payments of up to 9 months

Features 0% interest and no fees for up to 90 days

Offers affordable interest rates for 6 to 9-month loans at 3% per month with a 2% processing fee with instant approval for customers

A collaboration between UOB, Bhinneka, dinomart.com, Garuda Indonesia, Mapclub and Hartono

- #3 TMRW Power Saver – An online exclusive time deposit

Enables Indonesian customers to earn higher interest with a minimum tenure of one month

Features a low minimum entrance deposit of only IDR 8,000,000 (approx. USD 515) with a competitive interest rate of 3.5%-4.55%.

- #4 TMRW CashPlus – An online exclusive credit facility

Enables customers in Thailand to get instant cash of up to THB 1 million (approx. USD 26,500) at any time.

Equipped with a flexible monthly repayment, customers can decide between paying 2.5% of the total loan amount monthly or an easy instalment of up to 48 months.

Growth opportunities

- #1 UOB TMRW – The Superapp

UOB significantly enhanced its digital experience. The bank achieved this by unifying its consumer banking with its dedicated digital bank, TMRW by UOB, to form the rebranded UOB TMRW, an all-in-one banking app.

Moving forward, UOB should continue their efforts for a Superapp by;

– consolidating all consumer services onto one platform, leading to an ecosystem of banking facilities for consumers

– gathering all the data from the different departments to form a big data set, which is then processed to create a personal profile

– leveraging the personal profile to increase the consumption of services

- #2 Strengthening UOB digital proposition in Asia

UOB witnessed a fragmented launch of UOB TMRW in Asia, with Malaysia and Indonesia yet to receive the application. To minimise friction and ensure a seamless customer experience, the bank should quickly work on releasing the tested UOB TMRW into these countries.

Malaysia

For starters, UOB can work to import UOB TMRW into Malaysia. Following the transition period, the bank should continuously work to promote UOB TMRW to extend its potential market reach. Exclusive offerings for the account, such as higher saving interest rates and customisable debit cards, are excellent ways for UOB to widen its reach in the multinational country.

- #3 Banking in the Metaverse

SkyArtverse by UOB is a futuristic gallery in Decentraland and is the first property built by an Asian bank to reach art enthusiasts through the decentralised virtual reality (VR) platform. The gallery features 37 award-winning artworks from the 2022 UOB Painting of the Year competition.

UOB can expand their investments in the Metaverse by following the footsteps of JP Morgan and Union Bank and launch a virtual lounge for customers to learn more about UOB. Moreover, the lounge can act as a discussion and engagement hub for UOB to explore topics, such as disruptive technologies.

The bank can also integrate its API into the Metaverse, unlocking an immersive VR banking experience where customers can perform day-to-day transactions in the virtual space. With that, UOB can also help other businesses establish their presents in the Metaverse via programs such as UOB BizSmart.

The aspiration to create its own virtual currency is strong for UOB, envisioning a future where customers can save or spend it within UOB’s dedicated virtual bank. Taking a step further, UOB can then instate virtual branches and ATMs in popular regions within the Metaverse to provide the same convenience of a physical customer to a virtual customer.

- #4 Buy Now Pay Later (BNPL)

Currently, UOB has different BNPL solutions for different countries. For example, Singapore with SmartPay, Malaysia with “0% Instalment Payment Plan”, and Indonesia with TMRW Pay.

Unifying and standardising the product will most likely help UOB save marketing, software and operational procedure costs. It will also encourage UOB to innovate creative solutions from the shared resources, providing better promotions or deals due to the excellent cost-efficiency.

- #5 Cost to serve

UOB should improve their group’s loan management performance as the net interest income, net interest margin, and non-performing loans deteriorate. Here, the bank has three primary options to focus its attention on, that is to either;

– increase the amount of loan disbursed,

– increase the interest rate of loans,

– or improve the loan quality.

UOB should also control their staff cost, with staff cost especially share-based compensation rising. The overall staff cost has increased by 27%, while shared-based compensation has increased by nearly 49% since 2016.

On the other hand, UOB’s fee income has raised significantly due to UOB’s improved branding and customer service, as customers flock toward UOB’s unit trust, foreign exchange, BNPL and other offerings. Therefore, UOB should continue to maintain its group image, improve the customer experience, introduce new innovative services, and ensure its current service remains competitive.

Conclusion

Striving to be the next bank, it’s clear there is a lot of effort on display from UOB. From being the SMEs preferred bank to helping businesses grow and deliver an omni-channel customer experience, the bank is well aware of its vision and potential reach. Couple that with an enriched focus on sustainability, ESG integration and the desire to champion the employee experience, and it is clear to see why UOB stands as the top 3 banks, alongside OCBC and DBS.

See 2020’s report here