Introduction

6.8% – 7.2% — is Indonesia’s BFSI (Banking and Financial Services) industry’s contribution to the GDP, whose total annual growth is currently at 5.7%. It is because Indonesia currently operates 3 state-owned banks: Bank Mandiri, Bank Rakyat Indonesia (BRI), and Bank Negara Indonesia (BNI). There is also the addition of Bank Central Asia (BCA) and BTPN (Bank Tabungan Pensiunan Nasional) to Indonesia’s lineup of winning banks.

With that in mind, this report aims to examine how financial services in Indonesia have flourished by identifying the growth drivers that have led to their success. In addition, this report will also aim to highlight several growth opportunities that new and existing banks across Indonesia can focus on to improve their success.

Benchmarking the best of Indonesia’s banks

It is crucial to underline the best of Indonesia’s financial institutions, as it can yield valuable information in understanding the core issues Indonesia needs to solve to expand and grow even further. Hence, the twimbit Purpose Index proved helpful in our benchmark, as its metrics were able to successfully analyse the 4 key purpose pillars:

- Customer experience (CX)

- Employee experience (EX)

- Supplier satisfaction

- ESG (Environmental, Social and Governance) impact

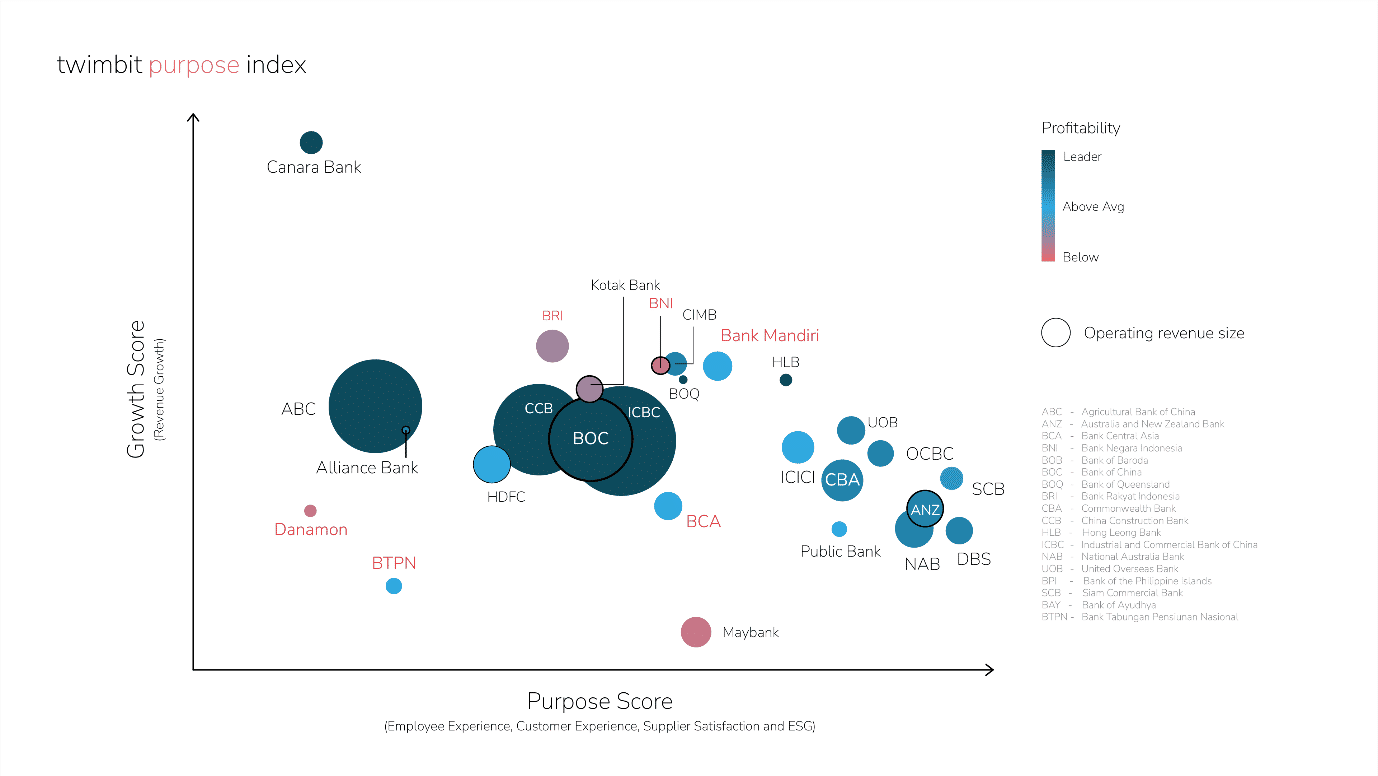

Benchmarking top Indonesia banks on the twimbit Purpose Index

Source: twimbit analysis

| Growth Score | The growth in revenue Y-o-Y (Year on Year) |

| Purpose Score | The aggregate purpose score for each pillar |

| Bubble Colour | The colours indicate the bank’s profitability |

| Size of Bubble | The size denotes the operating revenue size of the banks |

As it stands, Bank Mandiri is the largest bank in the nation with the most forward-thinking digital propositions. And with the help of the twimbit Purpose Index, this report discovered that:

- Bank Mandiri, BRI and BNI have higher growth compared to BCA and BTPN

- Bank Mandiri, BCA and BTPN have an above-average profitability rate

- Bank Mandiri currently possesses the largest operating revenue size

- Bank Mandiri has the highest purpose score, followed by BCA, BNI, BRI, and BTPN

The analysis also revealed 4 growth opportunities across the 4 key areas that banks must focus on for future success:

- Enable frictionless digital banking proposition for elevated CX

- Develop a partner ecosystem to expand embedded offerings

- Embed more integrated experiences through SuperApps

- Drive phygital (physical + digital) experiences sustainably

Industry challenges and growth drivers

With a population of 227.5 million, Indonesia is the largest economy in Southeast Asia. The country’s digital industry stood at US$ 77 billion in 2022. And internet penetration in Indonesia stood at around 70% as of 2021. This has set Indonesia on the path to the next digital revolution.

While Indonesian banks have embraced digitalisation wholeheartedly with various digital offerings, they face challenges, such as average revenue growths, despite strong operational performance and high CASA ratios. Other factors include the following:

- Higher cost-efficiency ratios

- Higher ICT expenses leading to high operating expenditure

- Low fee-based income

Top initiatives by the Indonesian banks

Indonesian banks have upped their CX game through digital banking apps, SuperApp offerings and embedded finance solutions. Here are the top initiatives that the banks have taken in these 3 areas:

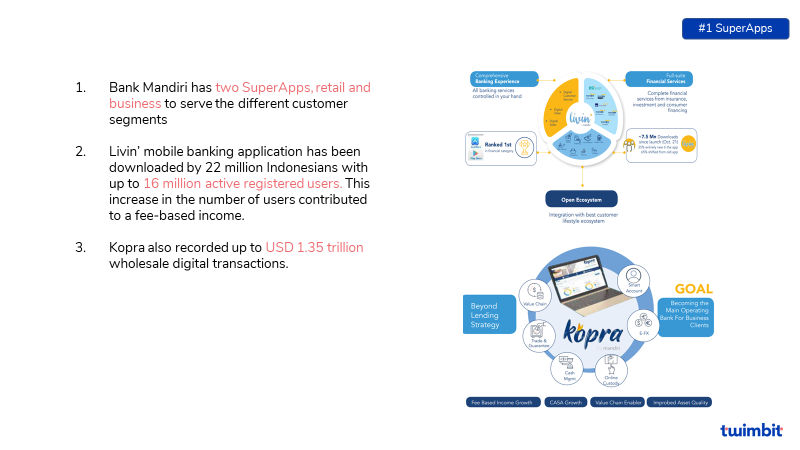

- Bank Mandiri has two different Superapps

Bank Mandiri’s Superapp offerings and their user penetration

Source: twimbit analysis

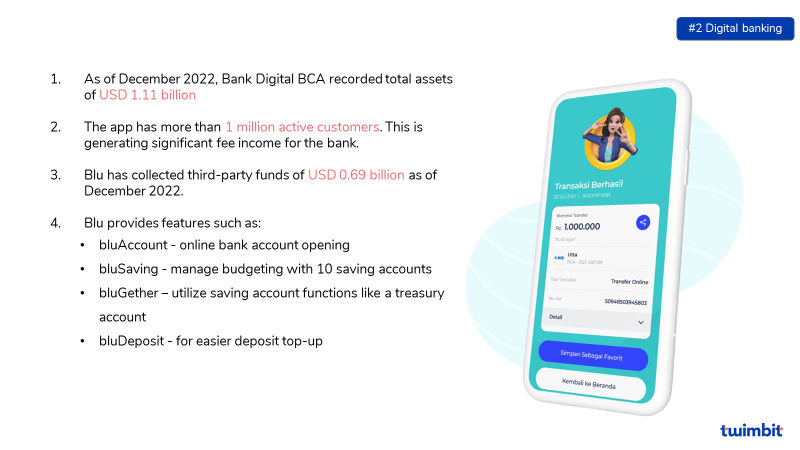

- BCA steps towards branchless banking with a digital-only bank – Blu

Impact of Blu on BCA’s digital growth

Source: twimbit analysis

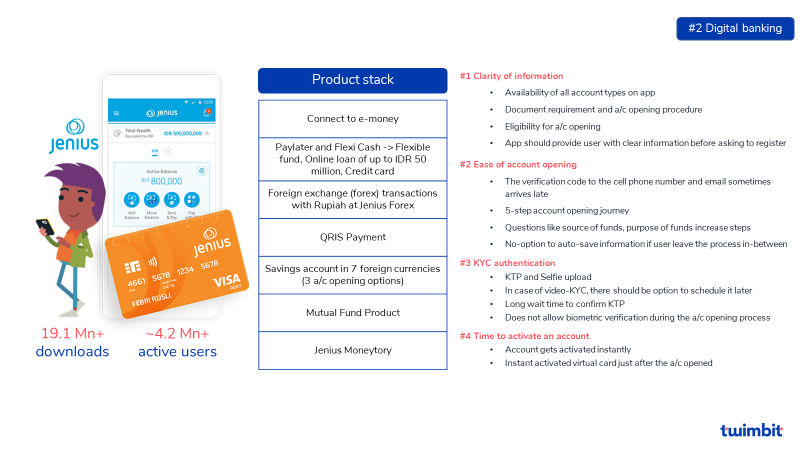

- Jenius by BTPN revolutionised banking in Indonesia by being the first digital banking app

Analysis of Jenius

Source: twimbit analysis

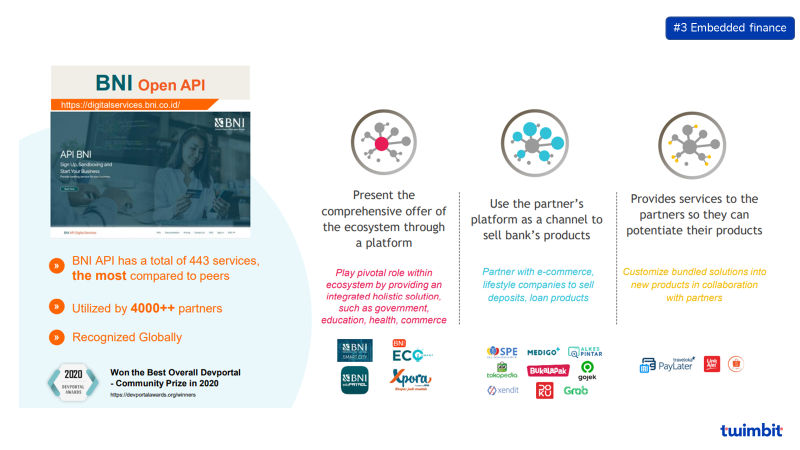

- BNI has the largest API stack in Indonesia, enabling BAAS (banking as a service) solutions for partners

API Stack of BNI and its role in the ecosystem

Source: BNI Investor presentation

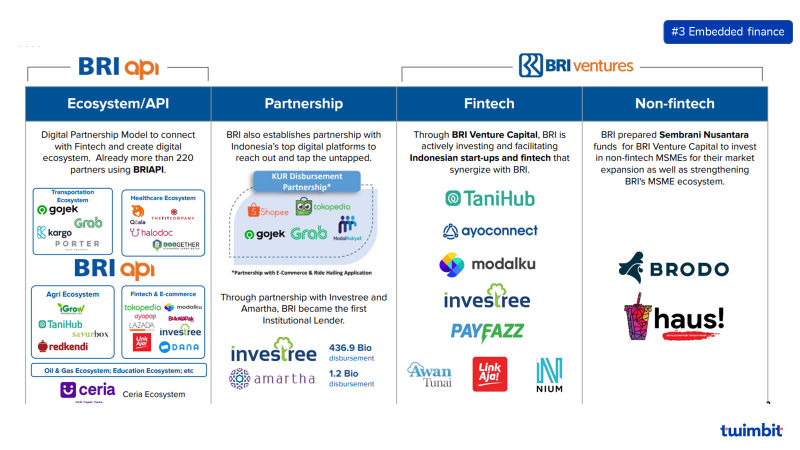

- BRI is building the fastest-growing ecosystem for data monetisation

API ecosystem of BRI

Source: BRI Investor presentation

Opportunities

The analysis uncovered 4 opportunities for the banks to grow their fee-based income while reducing costs. These opportunities include banks focusing on their digital adjacencies.

- #1 Enable frictionless digital banking proposition for elevated CX

Drivers for growth in digital banking offerings

Source: twimbit analysis

Currently, the top 5 banks in Indonesia possess digital-only offerings in the form of ‘Livin’, ‘BNI Mobile’, ‘BRImo’, ‘Blu’ and ‘Jenius’. While these offerings contribute well to the banks’ revenue and cater to over 72 million users, banks can further enhance their offerings in many other ways.

- Improve the digital onboarding process with the help of AI chatbots

- Minimise the steps taken for KYC (Know-Your-Customer) authentication

- Provide instant and seamless account activation for easier accessibility

- Utilise account activation time to highlight promos and other offers

- Hyper-personalise and gamify the customer journey to engage users

- Upgrade existing product stacks to include more embedded financial services

Read the detailed analysis to improve your digital-only banking experience – here.

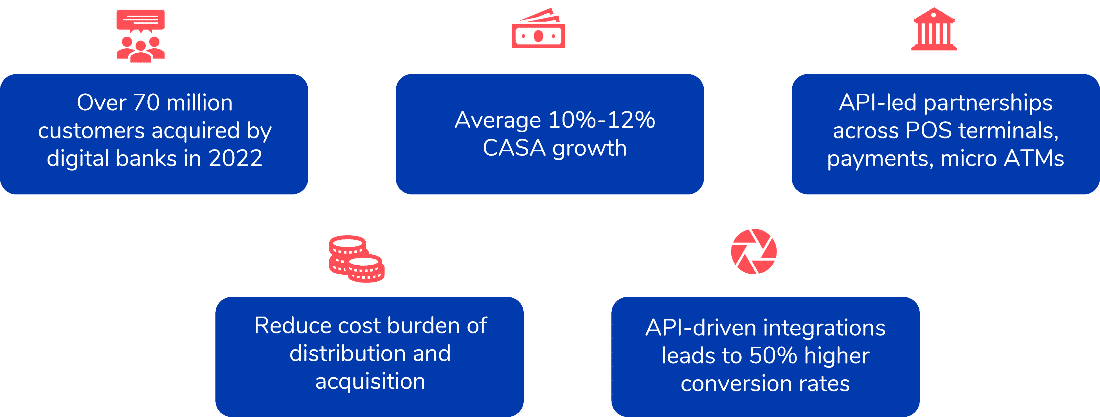

- #2 Develop a partner ecosystem to expand embedded offerings

For banks, embedded finance represents a significant opportunity to broaden their fee income by leveraging the customer reach of non-financial partners. Banks can also unlock new revenue streams and strengthen customer relationships by offering customised financial solutions through these partnerships.

Significance of embedded finance in the growth of fee income

Source: twimbit analysis

Currently, Indonesia has an unbanked population of 38%. Banks can drive financial inclusion through embedded financial solutions to improve the situation.

- An integrated, end-to-end retail lending solution: This solution should cover aspects such as mortgage, automotive and education expenses, covering all facets of the customer’s loan lifecycle from sourcing to disbursement. It should act as a unified interface for customers, third-party providers and sourcing channels.

- A merchant ecosystem: This solution should help grocers, supermarkets, small retail store chains, online businesses and e-commerce firms. The merchant ecosystem should be the one-stop shop for banking solutions and value-added services.

Embedded finance is set to transform how banks generate fee income and other financial services.

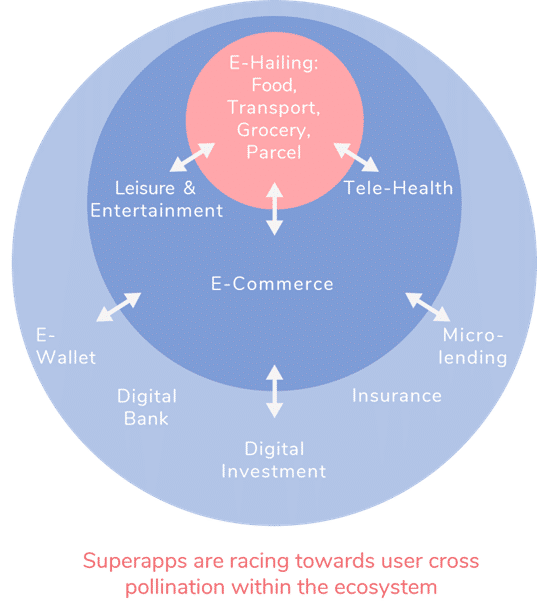

- #3 Embed more integrated experiences through SuperApps

CX is about integrating wonderful experiences for the customer. Thus, brands have created all-in-one SuperApps to ace this challenge, resulting in an ecosystem of services to cross-sell their offerings at a large and accessible rate.

SuperApp ecosystem

Source: Empowering Indonesia 2023

Currently, Bank Mandiri has 2 different SuperApps for different customer segments, contributing about 30% to the bank’s revenue.

SuperApps have significant potential to generate new revenue streams and increase cross-selling for banks. Furthermore, SuperApps can also help banks by:

- Providing a seamless CX at lower costs

- Streamlining day-to-day financial functions for customers

- Accessing new data sources

- Improving banks’ data management and analytics

- Creating a single source of information for all business lines

- Developing a better risk assessment view for lending

- Building targeted financial products for each customer

- Forging longer-term customer relationships

- #4 Drive phygital (physical + digital) experiences sustainably

There are 7157 branch networks among the top 5 banks in Indonesia, with all intending to expand their branch networks. This will result into increase in their cost to serve and deviate from their purpose of sustainability. Therefore, the first critical aspect of the expansion these banks should focus on is building branches with low carbon footprint and sustainable materials, following the likes of ANZ Bank.

ANZ bank branch in Australia is built on the ESG concepts to reduce emissions, create a healthy environment, and encourage a place to co-work and co-create

This would allow the banks to remodel and scale their branches cost-effectively. This will also help them to save waste while adhering to the changing needs of the environment and the customer.

They can also use branch technology infrastructure which they can easily disassemble, relocate and reuse.

The future of banking in Indonesia

Banks in Indonesia are on the path to being the centre of the next digital revolution. However, banks’ operational expenses are high, and revenue growth is average compared to other top banks in the Asia Pacific. Therefore, these banks must first reflect upon what it means to be future-ready, starting with:

- How can banks reduce their cost to serve?

- How can banks generate more fee-based income?

- How can banks transform to become experienced economy leaders?

For more detailed insights, download our State of Indonesian Banks report, above.