Learn, ideate and collaborate on the biggest innovation opportunities

Top 10 millennial banks in the Asia Pacific

@ Varnika Goel

“If banks can’t offer something more valuable than Amazon Prime, then we are probably in the wrong business” – Bradley Leimer

Introduction

The millennial generation falls under the age bracket of 18 to 40, that demands convenience, personalisation, and design experience in every engagement. This experiential persona is translated into millennial’s banking needs as well. A bank providing feature-embedded products and services powered by new-age technologies in a few clicks will succeed in the market.

Millennial growth opportunity

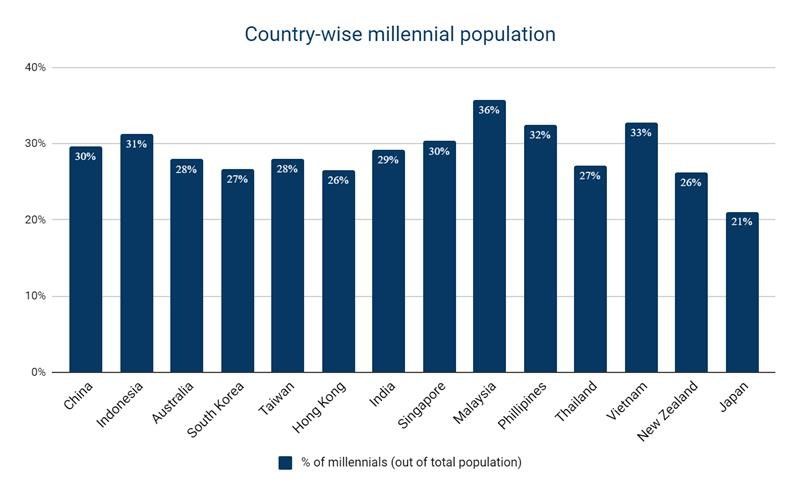

For millennials, to achieve financial independence, opening a bank account is the first step. However, many millennials struggle to do so as their first-hand banking experience results in them feeling disengaged. Having said that, in the coming 5 to 10 years, millennials will account for more than 60% of the workforce in the Asia Pacific countries, and to tap this market, traditional banks will have to go through a radical change.

With the vision of millennials as a growth opportunity, we see several neobanks creating state-of-the-art product propositions, catering to specific millennial needs. This further brings disruption and competition in the market as these banks operate as technology companies with an agile mindset, unlike the traditional banks’ incremental change approach.

Our approach

To identify the best-in-class product and service propositions while fulfilling the experiential needs of the millennials, we studied 60 banks in the 7 Asia Pacific countries. Based on our in-depth analysis, we have come up with a list of Twimbit’s top 10 millennial banks in the Asia Pacific, which are setting up a benchmark for banks that cater to millennial needs.

To narrow down the top 10 banks from an exhaustive list of 60 banks, we assessed each of them on five key features stated below, listing the millennials’ expectations from their respective banking partners. Further, we ran a short survey inviting 200 millennial respondents across these countries to determine their preferences in banking services.

Evaluation Criteria

A strong and secure digital identity

Presence of personalised offers

End-to-end digitalisation

Significant corporate social responsibility

Advanced social media integration

Top 10 millennial banks

Rank 1, Frank, Singapore

The brand name is stylish, quick, and enables instant recollection

The physical presence is in millennial-centric areas such as college campuses and popular malls

The physical interface is more like a casual café than a boring bank branch

Rank 2, Kakao, South Korea

The bank uses its social media messaging app KakaoTalk, popular among millennials to cross-sell banking products

Popular cartoon-based cards named ‘Friends’ strike an immediate resonance

Nostalgia-based ‘piggy bank’ saving plans

Rank 3, DBS, Singapore

Online banking through facial recognition – First of its kind

DigiPortfolio is a robo technology-enabled portfolio management

Quick and hassle-free money transfer using only mobile numbers

Rank 4, TMRW by UOB, Indonesia/ Thailand

Popular cartoon-inspired UI strikes immediate resonance among millennial population

Financial insights based on spending patterns, allowing better expense and saving decisions

Personalised discounts and cashback at restaurants and shopping centres

Rank 5, WeBank, China

The bank uses its social media messaging app WeChat, with a 90% customer penetration in China to cross-sell banking products

Partnered with China’s leading car dealerships Weichedai auto loan for easy access to vehicle loans

WeBank app allows Withdrawals, money transfer and wealth management all in one application

Rank 6, Jenius, Indonesia

An integrated one-stop solution for multiple banking accounts

Dream Saver is an auto mechanism to calculate and save money every day/week/month

Pay Me and Split Bill features help avoid awkward conversations with friends by enabling direct expense sharing

Rank 7, Bank Danamon, Indonesia

Financial protection to overcome monetary challenges- Proteski Prima Ema Plus (PPEP)

Personalised offers on purchasing a favourite sports team’s kit or reserving a luxury hotel room

Pilgrimage Savings accounts to help individuals save for a lifelong desired trip to Mecca

Rank 8, Axis Bank, India

The Axis Pay UPI App is an integrated one-stop solution for multiple banking accounts

Axis OK allows banking without internet on any android device

Axis AHA, a virtual assistant to carry out tasks such as transferring money or paying bills

Rank 9, Westpac, Australia

An international student account with no monthly service or withdrawal fee along with a complimentary student card

A zero service fee Mastercard along with online banking if you are under 21

BT Invest, a platform to create a diversified investment portfolio

Rank 10, SBI YONO, India

YONO mobile app allows access to everything from calling a cab to repaying a loan

SBI’s YONO Omni Channel helps maximise returns on investments with interactive portfolio dashboards

YONO Omni Channel helps maximise returns on investments with interactive portfolio dashboards

Key takeaways

The banks discussed in the list have made incredible shifts to identify, cater to, and continuously support the ever-changing needs of the millennial population. Therefore, based on our analysis, there are four key best practices to successfully attract and engage millennials:

Unique digital brand identity

User interface inspired by cartoon and social media

Enjoyable, accessible, and aesthetic physical and digital presence

Reduction in clicks through facial and biometric recognition

Despite the new and upcoming challenger and neobanks, whose value proposition is far more superior to traditional ones, they struggle to acquire customers due to their loyalty and security trust with traditional banks. However, we see these banks as strong competitors for the future years when customers will have developed a broader mindset and will be more willing to prioritise services over safety.

Note

This research was contributed by Saksham Verma and Rajvardhan Bhatia