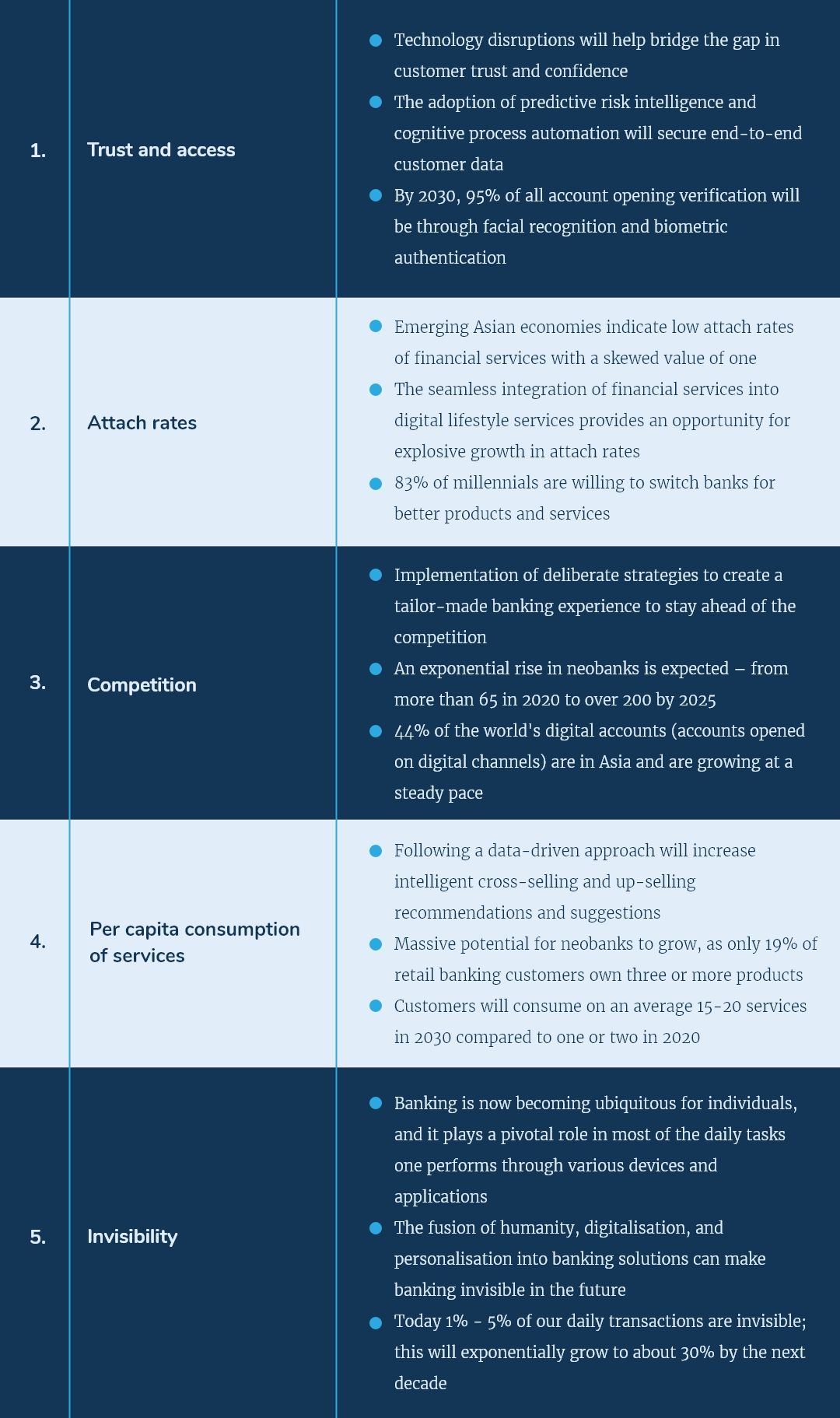

Do neobanks offer billion-dollar experiences, or is it just another fad?

Traditional boundaries within the banking industry are slowly dissipating. Incumbent banks have failed to address customers’ specific pain points with their ‘one-size-fits-all’ approach. The emergence of neobanks poses a threat to existing revenue streams and has radically transformed the customer experience. There is a growth spurt in the number of neobanks largely fuelled by aggressive private equity investors, venture capitalists, and technological giants. The total funding amount has exceeded USD 5.29 billion across the Asia Pacific countries.

The neobanks in Asia capitalise on the opportunity of large unbanked, underbanked, and previously ignored society segments by offering customised digital services to satisfy their financial needs. This move has resulted in an expansion of the neo banking customer base to over 826 million clients.

A Customer-centric organisational approach focuses on building an omnichannel, hyper-personalised, frictionless, and secure banking experience. There are many innovation opportunities for banks to consider:

Table 1: Key innovation opportunities

Eight customer-centricity parameters

Our research assesses eight parameters in sixty-three neobanks present within the various Asia Pacific countries to understand how they effectively cater to their customers’ needs compared to the incumbents.

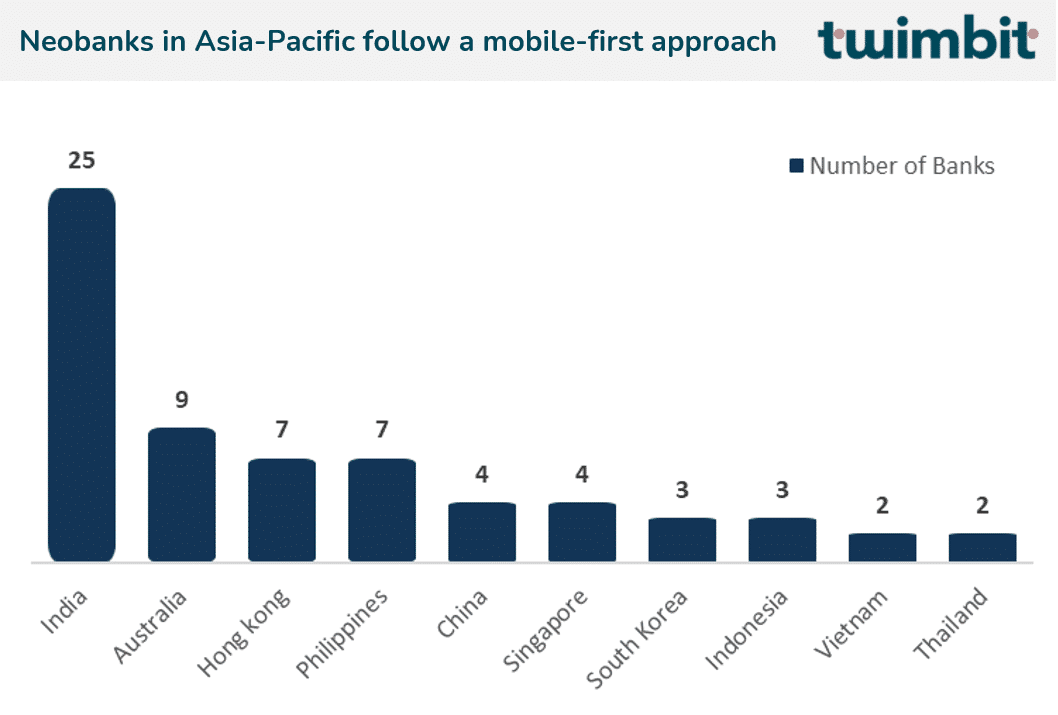

- Mobile-first approach

Today’s individuals spend an average of five to six hours on their phones – gone are the days of basic voice calls and SMS. This trend is prevalent in the banking sphere, as well. A banking application is not a standalone service anymore but rather an integration of digital and traditional touchpoints. These touchpoints enable customers to seamlessly access their banking information and conduct transactions throughout their financial journey.

The key reason for the popularity of mobile-first solutions in the banking sector is cost-effectiveness. In web page development, the design incorporates into the core structure of the neobank’s website. This design, in turn, responds to the screen size of a customer. There is no replication of effort and design since webpages are mobile-optimised, enabling neobanks to reduce costs significantly.

Neobanks’ lean infrastructure allows their customers to enjoy smaller fees and higher-than-average interest rates. By practising a mobile-first, device and channel-agnostic approach, neobanks can create end-to-end capabilities that various channels and applications can easily deploy. Winning neobanks of the future should provide an omnichannel, frictionless, and personalised experience across devices with the ability to plug-and-play specific features.

Figure 1: All operational neobanks in Asia-Pacific follow a mobile-first approach

- User-friendly User Interface (UI) – User Experience (UX) design

The UI-UX design has advanced from clicking and tapping buttons to using fingers to swipe, tap, hold, and even tilt a phone to perform actions. In the future, neo banking UIs will use less graphical tools and shift to building real-life experiences. The design industry’s recent developments include virtual reality (VR), augmented reality (AR) and holographic technology. These tools can create an authentic and real-life banking environment for customers. The banking industry is, however, still at the nascent stage of adopting these next-gen technologies.

Figure 2: More than 90% of the neobanks in Asia-Pacific have a robust UI-UX design

VR and AR are the game-changers for differently-abled and blind customers who wish to bank from the comfort of their homes while still enjoying some semblance of personal touch. Additionally, the virtual environment can layer visual tools such as virtual arrows, auditory tools like audio-enabled GPS tracking and text-to-speech integration, as well as haptic tools to feel and touch the interface. These designs will help neobanks guide customers who face difficulties locating the nearest branch, ATM or customer service point.

AR tools can engage customers and help neobanks to offer them spend-based and location-based offers. For example, when a coffee-lover crosses his favourite coffee shop, neobanks can immediately send them a reward for the coffee shop and guide them to the shop using AR tools.

While predictions into the future are rife with uncertainties, virtual reality and augmented reality will play a major role in incrementally improving the customers’ quality of life.

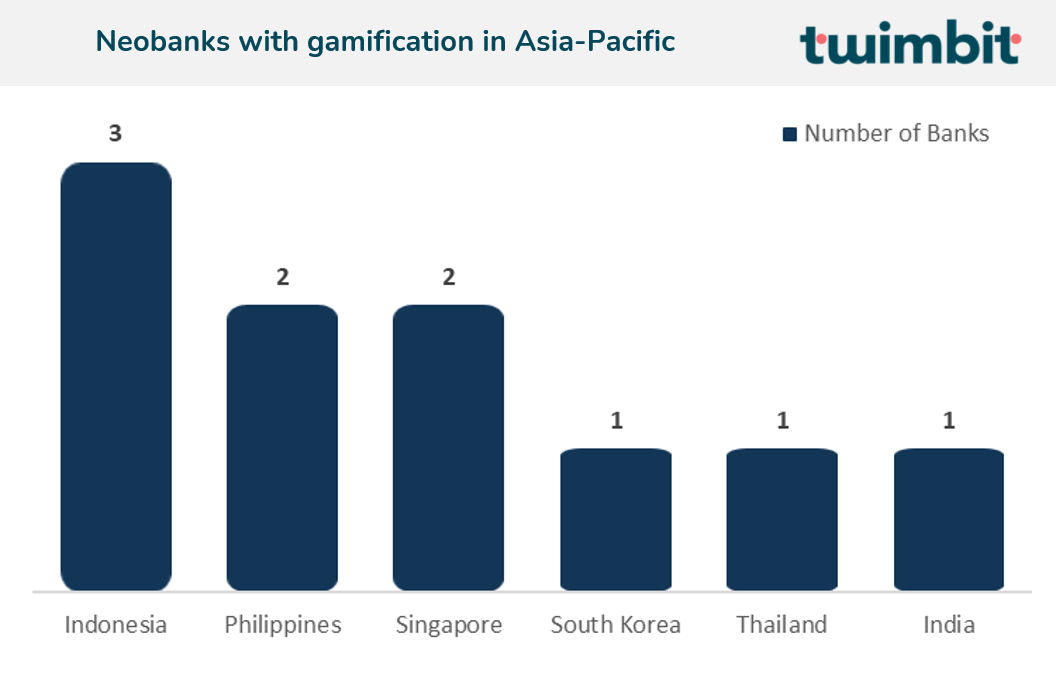

- Gamification

Gamification is the application of gaming design elements and principles to different non-game concepts and businesses. Gamification in the banking industry has been around since the early 2010s in awarding users with badges, stickers, and points for the transactions made. However, the gamification of money management tools and interactivity has evolved since then.

A noteworthy example comes from TMRW by UOB. TMRW uses a simple yet engaging game- the City of TMRW- its design encourages customers to save. The City of TMRW allows them to build their virtual city and unlock various game levels as they save more.

Figure 3: 8 out of the 10 neo banking countries offer gamification

In the future, gamification will evolve from merely being a set of tools used to attract customers to a strategic management tool to analyse the customer’s thought process and behaviour. Psychometric evaluation tools will infuse with gaming and virtual reality elements to bring intuition factor in banking.

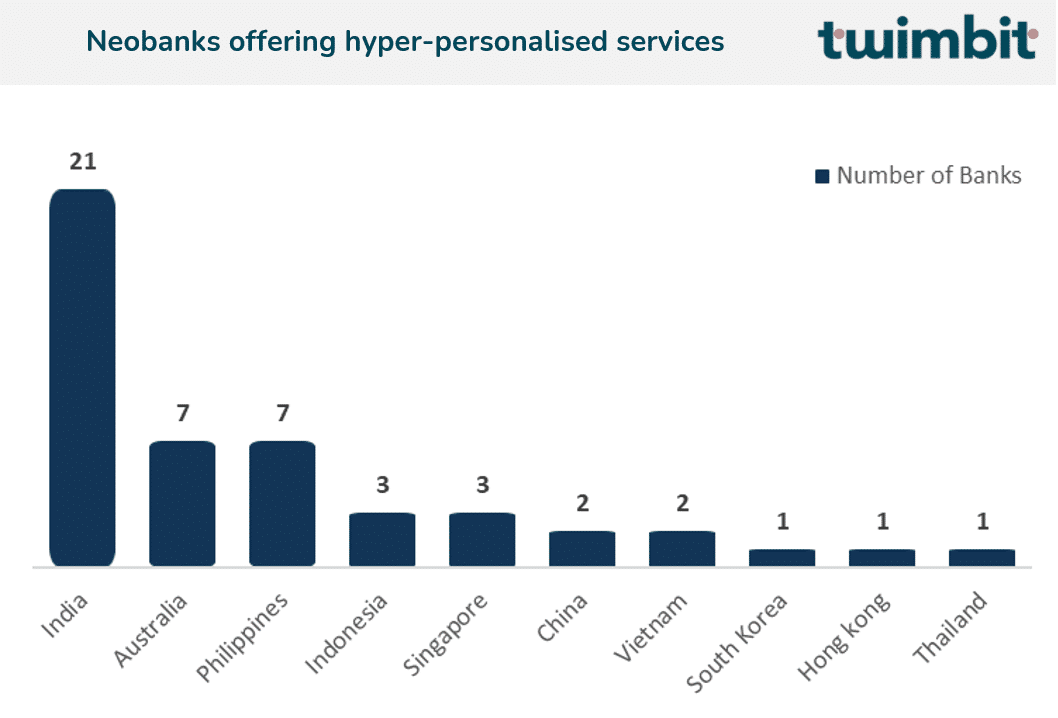

- Hyper-personalisation

The progress in the entertainment and e-commerce industries have resulted in customers expecting hyper-personalisation from financial service providers. Customers are willing to share their data, assuming that their financial provider and other entities will utilise it optimally to create experiences unique to their taste and preferences, similar Netflix suggestions and Spotify playlists. A well-established open infrastructure can deliver this enhanced personalised experience, which allows data monetisation.

In the past five years, neobanks have taken the reins to build hyper-personalised experiences by mastering data-driven approaches across channels. Neobanks provide hyper-personalised offerings such as:

- Spending and budgeting analytics

- Goal setting for spending and saving

- Customised virtual cards

- Tailor-made investment schemes and advisories

Figure 4: More than 70% of the neobanks in APAC offer hyperpersonalised services

Artificial intelligence (AI) and machine learning (ML) methodologies play a crucial role in making the above-stated offerings unique to each individual. The two methodologies harness real-time data to deliver fine-grained services that satisfy a customer’s distinct and latent needs.

To stay relevant in the future, neobanks should have a robust open bank ecosystem to collect, assimilate, and analyse their customers’ information from third-party providers. This move also builds opportunities for industry convergence and synergies, where neobanks interact with customers and clients beyond the point of sale.

- Real-time notification

There has been an upsurge in data transfer, third-party interactions, and the number of banking transactions done via mobile banking, online banking, ATM, and physical banking. Real-time notifications alert customers about banking transactions through their accounts in a timely and cost-effective manner while protecting them from fraud and identity theft. These notifications are a proactive way of communicating information as it increases the engagement rate and adds a significant value to the banking experience.

These notifications instil a sense of confidence in customers as they are assured; they will alert the moment a problem arises. Neobanks should also give customers complete control over their communication and notification preferences by allowing them to choose to receive alerts via their preferred medium- SMS, email, or push-app notification, as well as its relevant content. Consequently, this enables neobanks to build trust and transparency with their customers.

Figure 5: All operational neobanks across the Asia Pacific offer real-time notification alerts

Real-time notifications, however, have evolved from merely being a tool used to enhance security to being an approach followed for generating new revenue streams and improving customer-centricity.

Three notable use cases for real-time notifications are:

- Using AI-ML algorithms, neobanks can understand customers’ spending patterns to send them notifications for offers, rewards, investment options, and e-learning material best suited to their needs.

- Similar to e-commerce websites such as Amazon, Goibibo, Grab, Shopee, and BookMyShow, neobanks should leverage the capabilities of social networking services for sending real-time notifications over messenger apps.

- Neobanks should embed GPS in their notifications and alert systems to provide their customers with location-based offers. They can confirm a customer’s location using GPS, Wi-Fi or cellular tracking to identify the city, metro area, state, or country their customer is going to or coming from by customising notifications.

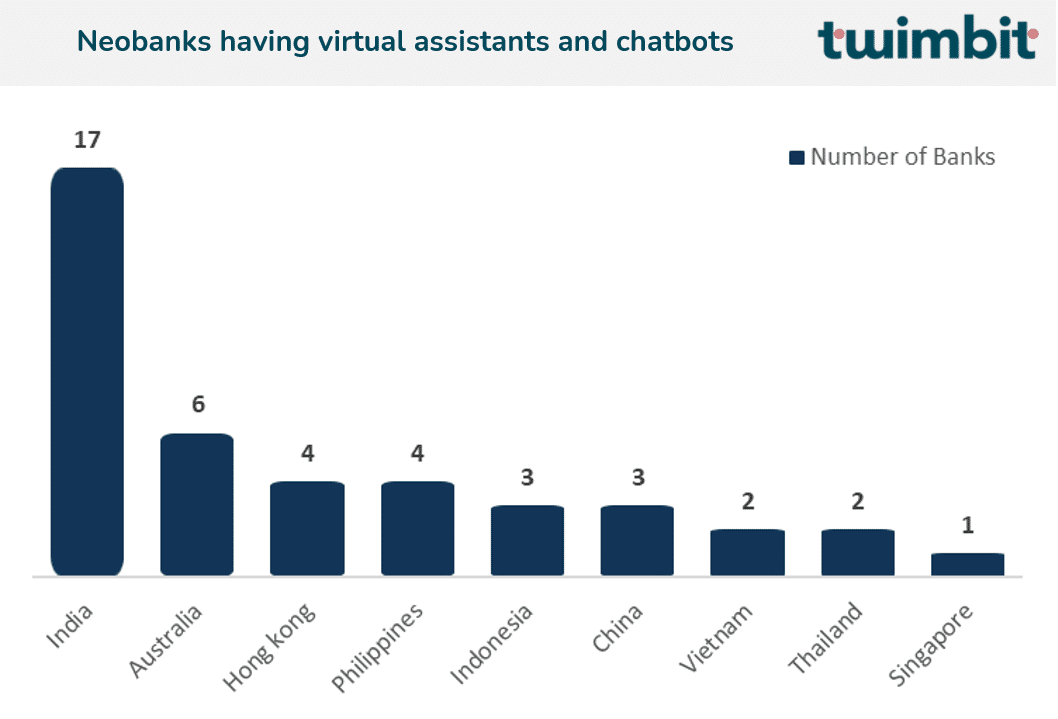

- Virtual assistants and chatbots

Chatbots are drastically changing the way neobanks interact with customers, employees, and vendors. Customers no longer have to wait on call for several hours, read through long pages of frequently asked questions (FAQs) or stand in queues for solving their queries. Chatbots enable customers to get their queries clarified within minutes over digital platforms. The availability of virtual assistants has significantly reduced human intervention and staff costs associated with customer relationship management.

Figure 6: At least 50% of the neobanks in the Asia Pacific have virtual assistants and chatbots

Investments in virtual assistance will be a top customer-centricity priority for the next five years. Chatbots will move from purely answering simple queries to having real-time conversations that use advanced predictive analysis and voice conversation AI techniques. These capabilities will lead bots to answer account-related queries, assist customers in performing banking transactions, and give personalised advice. To maintain a personal touch, neobanks can integrate AI-ML algorithms and text-to-speech techniques with sentimental analysis, such as Natural Language Processing (NLP) and Named Entity Recognition (NER). Messaging platforms will act as growth drivers for chatbots.

Winning neobanks of the future will forge strategic alliances with leading social media and internet giants to strengthen chatbots capabilities. These alliances will subsequently boost customer engagement and loyalty.

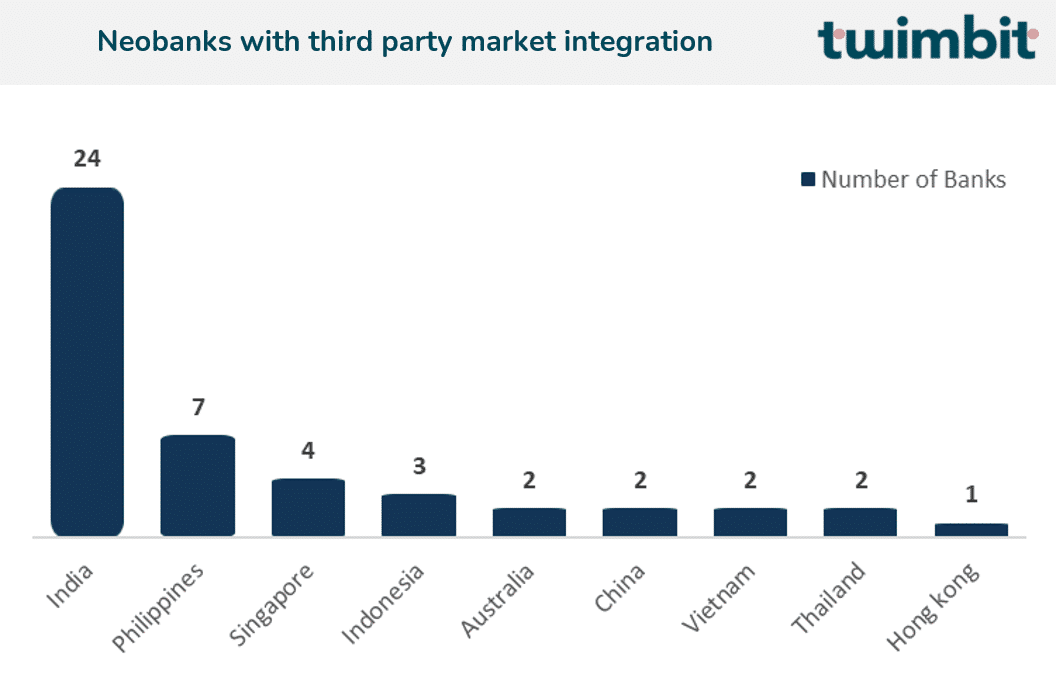

- Marketplace integration

A shift from a closed banking infrastructure to an open one has enabled neobanks to gain real-time customer data, thus opening an array of opportunities to provide additional value to their customers. The most notable of the newly emerged software is the Application Programming Interface (API) which developers use to get third-party data and services into their applications. API enables neobanks to increase its customers’ consumption of financial services through its proprietary platform. Consequently, neobanks can add new revenue streams to their product suite through interchange fees, commissions, transaction fees, and data monetisation. Moreover, to manage the high data flow, banks can employ Digital Ledger Technology (DLT), which records their customers’ transactions and other details in multiple places simultaneously to decentralise customer data management.

Figure 7: More than 90 % of the neobanks in APAC have an open banking infrastructure in place

Neobanks can develop a personalised suite of small and agile applications that are deployed independently onto the banking platform to cut the cost to serve significantly. These applications, in turn, provide customers with tangible benefits.

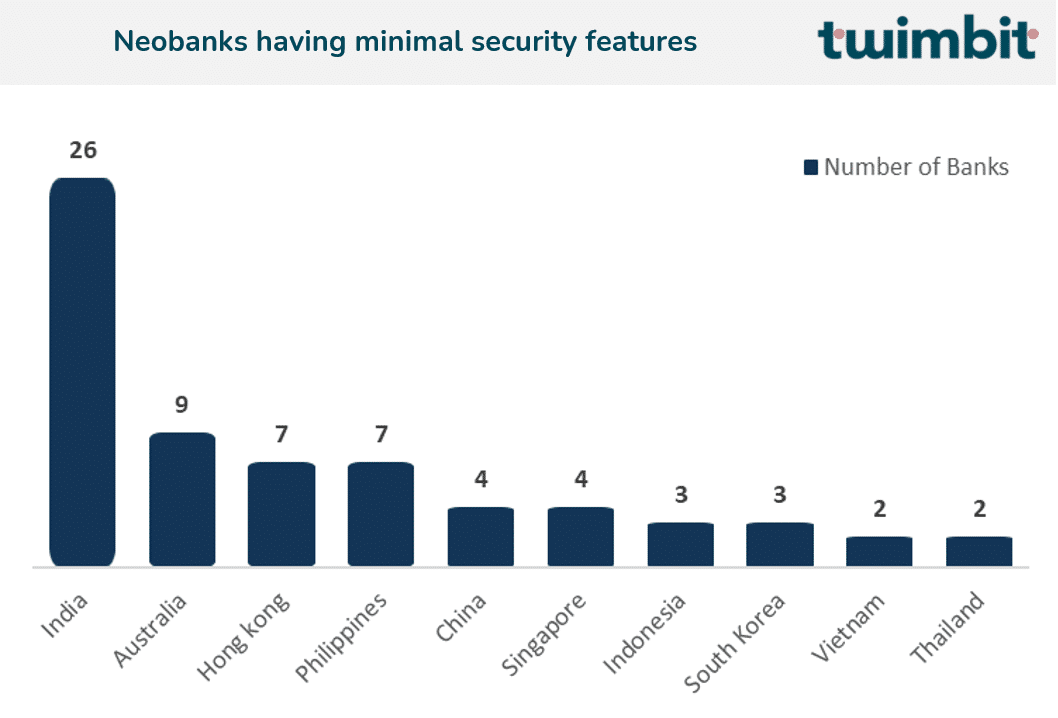

- Data security

Data has fundamentally transformed the way we bank. As open banking has resulted in a large amount of personal data transfer between companies, neobanks will have to reassure their customers that data is protected and follow customer consent norms.

In recent years, neobanks have employed various data security measures, including:

- Unique passcodes

- Captcha

- Biometric verifications such as fingerprints and facial recognition

- Two-factor authentication

Figure 8: All operational neobanks in the Asia Pacific have minimal security features

Three key ways to improve data security measures:

- Invest in building a sophisticated risk assessment and management system that allows continuous automated audit trails.

- Manage data with the same scrutiny as financial assets by allowing customers to choose the “to whom and for what” purpose they want to share their data.

- Utilise blockchain technology’s benefits to protect data by ensuring that past transactions and data cannot be read and altered by an unintended user.

Winning in future with customer centricity:

The winning neobanks of the future will emphasise on customer-centricity rather than product-centricity. These banks will also be adaptive to customers’ needs by putting them in the driver seat of their banking journey. To ensure neobanks remain customer-centric, they can:

- Listen: Conduct regular surveys and feedback sessions, allowing customers an opportunity to vocalise their preferences.

- Learn: Adopt an iterative approach with continuous improvement efforts by learning from each success and failure, irrespective of whether it has a small or big impact.

- Transform: Reorient cultural and organisational structure from top-down to a new agile organisation that prioritises the customers’ needs.

- Measure: Measure performance using customer-centric Key Performance Indicators (KPIs) such as Customer Lifetime Value, Customer Satisfaction Score and Net Promoter Score.

- Train: Build holistic programmes that support the overall professional and mental well-being of employees via a customer-centric approach while simultaneously designing products, strategies and addressing problems.

Endnotes

References:

Taking retail banking cross selling to the next level

You Already Have What Millennials Want

Share of banked population in the Asia Pacific region in 2020

Note: Neobanks Fi (formerly known as Epifi) in India and Robocash in The Philippines are newly launched neobanks; hence their public interface is not live yet.

Akshita Maruthavanan , Research Intern, contributed to this research by conducting a preliminary literature review, writing, and conceptualising the article.