Regulatory Initiatives

Hong Kong refers to neobanks as Virtual banks. The regulatory rules for virtual banks in Hong Kong are the same as the traditional banks. The Hong Kong Monetary Authority (HKMA) did so to ensure a level playing field between the traditional and the virtual banks. Some of these important regulatory procedures are:

- A minimum paid-up capital requirement of HK$300 million for virtual bank applicants

- The priority of being granted a virtual banking license would be given banks which can demonstrate:

- Have sufficient financial, technology, and other relevant resources to operate a virtual bank

- A credible and viable business plan that would provide a new customer experience

- Developed or can develop an appropriate IT platform to support their business plan

- Ready to commence operation soon after a license is granted

- Deposits are protected up to a limit of HK$500,000 per depositor

- The HKMA considers it prudent to require virtual bank applicants to develop an exit plan. The purpose of an exit plan is to ensure that, a virtual bank can unwind its business operations in an orderly manner without disrupting the customers and the financial system

Snapshot of Hong Kong’s virtual banks

Table 1: Profile for Hong Kong’s virtual banks

| Name | Founding Year | CEO | Annual Revenue |

| ZA | 2015 | Shim Sung-Hoon | Undisclosed amount |

| Airstar | 2016 | Alex Ryu | Undisclosed amount |

| WeLab | 2013 | Adrian Tse | Undisclosed amount |

| Livi | 2019 | Michael Wang | Undisclosed amount |

| Ant | N/A | Wang Lan | Undisclosed amount |

| Fusion | N/A | Eric Sum | Undisclosed amount |

| Mox | 2019 | Deniz Güven | Undisclosed amount |

| Ping An OneConnect (PAOB) | 2018 | Ryan Fung | Undisclosed amount |

Note: The annual revenue is an undisclosed amount as the banks are privately held

Table 2: Learning list of Hong Kong’s virtual banks funding capital

| Name | WeLab |

| Total funds raised | US $581 Million |

| Seed Round | (Jan 2013) |

| Series A | US $20 Million (Jan 2015) |

| Funding Round | (Dec 2015) |

| Series B | US $160 Million (Jan 2016) |

| Debt Financing | US $25 Million (Sept 2016) |

| Venture Round | (Oct 2017) |

| Series B | US $220 Million (Nov 2017) |

| Series C | US $156 Million (Dec 2019) |

In-depth virtual bank analysis on the 5-building block framework

Customer Centricity

- 100% of the virtual banks in Hong Kong showcase a mobile-first approach

- 63% of the virtual banks offer multi-currency transactions to its customers

- Only Mox offers hyper-personalization, budget analytics, and save and spend goal setting

Figure 1: Hong Kong’s virtual banks showcase limited customer centricity

Note: The de-highlighted customer-centricity parameters indicate these are not prevalent in any of the neobanks

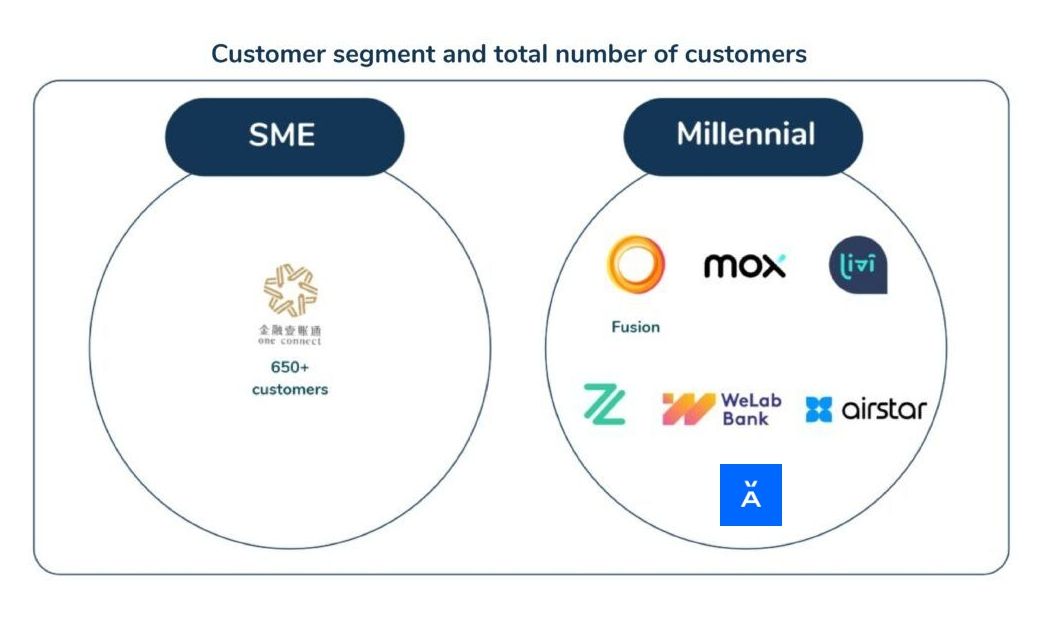

Customer Reach

- 14% of the virtual banks in Hong Kong cater to small businesses

- 86% of the virtual banks in Hong Kong cater to the Gen Z and Millenial population

Figure 2: Representation of each virtual banks’ customer reach

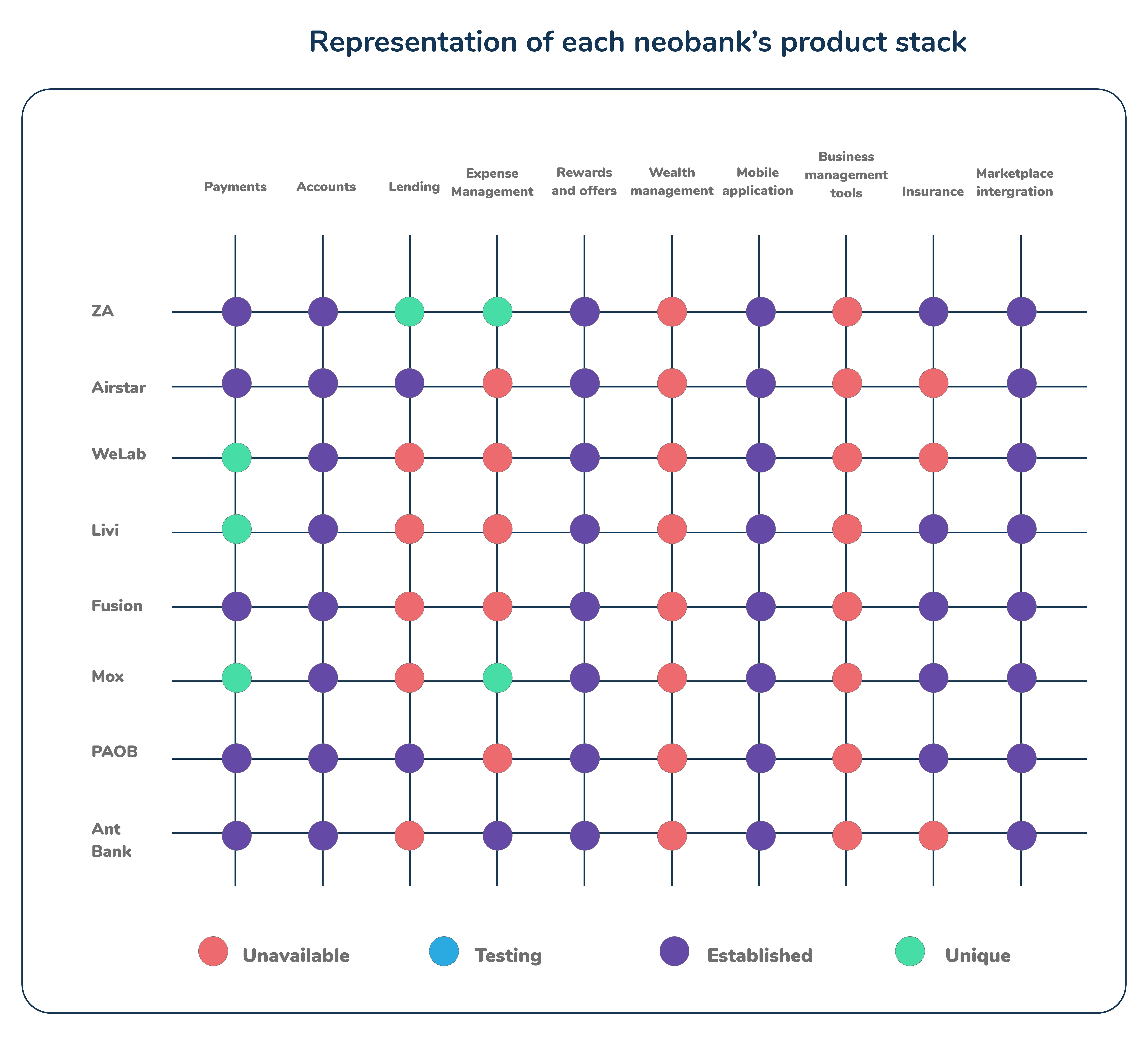

Product Stack

- Mox is the only virtual bank in Hong Kong to offer Google Pay services

- WeLab and Mox are the only virtual banks in Hong Kong that offer credit and debit cards

- ZA is the only virtual bank that extends mortgage loans to its customers

- 43% of the virtual banks offer the in-app virtual card feature

Methodology

Each virtual bank product stack is a representation of 4 key parameters across 9 product types:

- Unavailable: Does not have a product type in their stack

- Testing: The product is currently in the pilot-testing phase, not live to all customers

- Established: The product is a part of their stack and fully available for customers

- Unique: A unique offering within a product type that is exclusively provided by the virtual banks

Figure 3: Representation of each virtual bank’s product stack

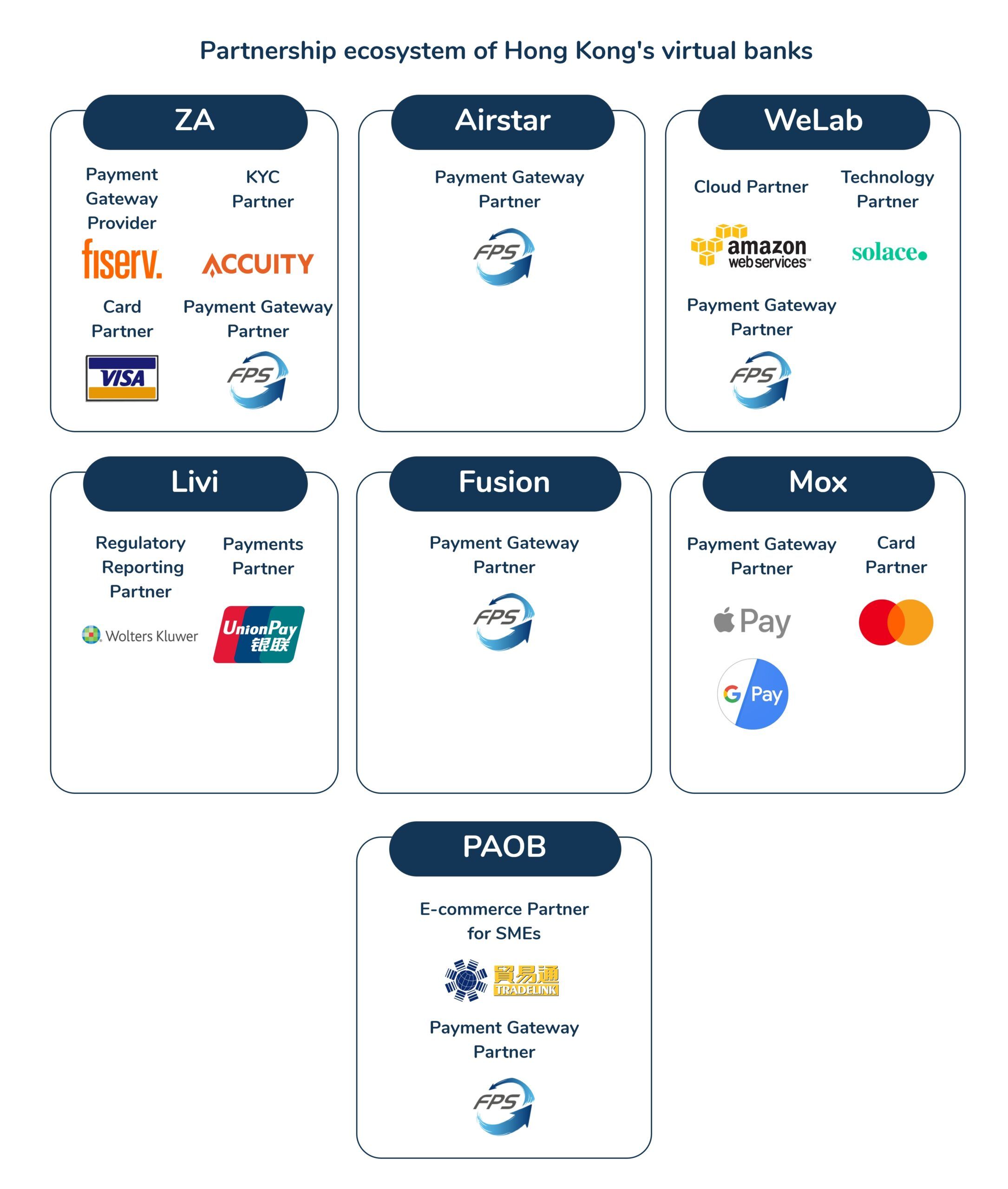

Partnership Ecosystem

- Mox became the first bank in Hong Kong to partner with Apple Pay and Google Pay

- All the virtual banks in Hong Kong offer real-time payments through the payment financial infrastructure created by HKMA called FPS

Figure 4: Representation of each virtual banks’ partnership ecosystem

Open Banking

The Hong Kong Monetary Authority (HKMA) in July 2018 published a four-phase approach to implement Open Banking:

- Phase 1: “read-only” product

- Phase 2: new applications and customer acquisition

- Phase 3: account information

- Phase 4: transaction processing

Table 3: API Developers for Hong Kong’s virtual banks

| Name of the bank | Developer |

| ZA | Fiserv, Inc. |

Fiserv, Inc. is the API developer for ZA bank:

- It is a global leader in Fintech and payments enabling innovative financial services experiences that are in step with the way people live and work today

- Finserv serves clients in more than 100 countries

Hong Kong’s virtual banks’ outlook

- The Hong Kong Monetary Authority received around 29 applications for granting virtual banking licenses out of which just 8 got approved. Due to HKMA’s strictness, Hong Kong is losing out on an ultra-competitive marketplace of virtual banks. However, they are willing to trade it off for a more robust and secure system.

- A recent survey by the Hong Kong Institute of Chartered Secretaries found that 76% of members said bank account-opening procedures were getting more difficult, Virtual banks came in and reduced that time drastically.

- The list of requirements to fill for virtual banks are too long. For a virtual bank to start, having at least HK$300 million is a lot.

Annexure

Table 4: List of investors in Hong Kongs’ virtual banks

| Name of the bank | Investor |

| ZA | ZhongAn Online P&C Insurance, Sinolink Group |

| Airstar | Xiaomi, AMTD Group |

| WeLab | WeLab |

| Livi | JD.com, Bank of China, Hong Kong |

| Ant | Ant Financial |

| Fusion | Tencent, the Industrial and Commercial Bank of China |

| Mox | Standard Chartered, HKT, PCCW and Trip.com |

| PAOB | Ping An Insurance |

Endnotes

We have sourced information pertaining to the funding value, round, customer base, revenue, and product information from Crunchbase, Owler, respective company’s annual reports, and their websites.

Aman Jindal, Business Research Analyst Intern, contributed to this research by assisting in writing, conducting preliminary analysis, and conceptualising the topic.